Ontario Securities Commission Bulletin

Issue 49/04 - January 29, 2026

Ont. Sec. Bull. Issue 49/04

• Ontario Securities Commission and Ahmed Kaiser Akbar

• Oasis World Trading Inc. et al.

• Ontario Securities Commission and Ron Carter Hew

• Notice of Correction -- Ontario Securities Commission and Benjamin Ward

• Ontario Securities Commission and Ron Carter Hew -- ss. 127(1), 127.1

• Ontario Securities Commission and Ahmed Kaiser Akbar -- ss. 126.1(1)(b), 126.2(1)

• Oasis World Trading Inc. et al.

• Ontario Securities Commission and Ron Carter Hew -- ss. 127(1), 127.1

• Harvest Portfolios Group Inc.

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

SLC Holdings Inc. et al. -- s. 127

FILE NO.: 2026-6

BETWEEN:

Section 127 of the Securities Act, RSO 1990, c S.5

PROCEEDING TYPE: Application relating to a transaction

HEARING DATE AND TIME: January 27, 2026, at 3:00 p.m.

LOCATION: By videoconference

The purpose of this proceeding is to consider the application filed by SLC Holdings Inc. dated January 22, 2026, requesting an order that all trading in securities of Stracon Group Holding Inc., shall not commence, or shall immediately cease, unless and until the amalgamation between Stracon Canada and Stracon Holdings S.A. has been completed, and other related relief related to the amalgamation.

The hearing set for the date and time indicated above is the first case management hearing in this proceeding, as described in subsection 13(3) of the Capital Markets Tribunal Rules of Procedure.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT ATTEND, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

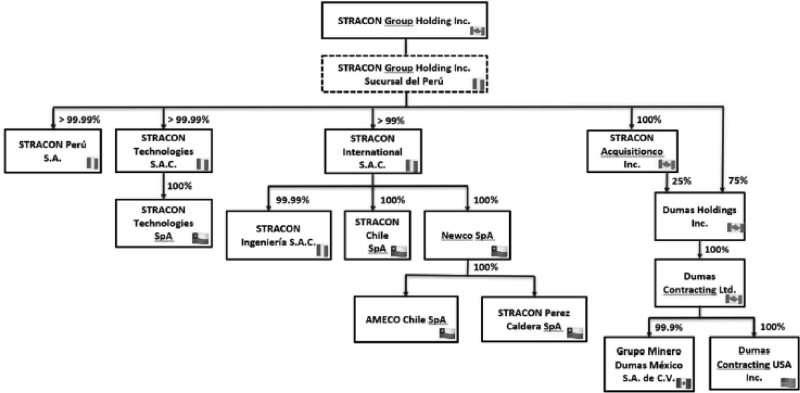

Dated at Toronto this 27th day of January, 2026

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@capitalmarketstribunal.ca.

File No. _____________

BETWEEN:

1. The Applicant, SLC Holdings Inc. ("SLCH"), requests that the Tribunal make the following orders:

(a) an order granting SLCH standing to bring this application under section 127 of the Securities Act, R.S.O. 1990, c. s.5. (the "Act");

(b) an order pursuant to section 127(1)2 of the Act that all trading in securities of the Respondent, Stracon Group Holding Inc. ("Stracon Canada"), shall not commence, or, if trading has commenced, shall immediately cease, unless and until the amalgamation between Stracon Canada and Stracon Holdings S.A. ("Stracon Original") (the "Amalgamation") has been completed and is effective under the laws of Peru;

(c) an order pursuant to section 127(1)5 of the Act prohibiting the Respondent from providing to any person or company: (i) the Respondent's prospectus dated December 16, 2025 (the "Prospectus"); and (ii) any other disclosure document that contains a material misrepresentation or materially misleading omission concerning the Amalgamation;

(d) in the alternative to paragraph 1(b), an order pursuant to section 127(1)2 of the Act directing that trading in any securities of the Respondent shall not commence, or, if trading has commenced, shall cease, unless and until the Ontario Securities Commission is satisfied that the Respondent has: (i) corrected the material misrepresentations and materially misleading omissions in the Prospectus concerning the Amalgamation; and (ii) made the necessary corrective disclosure, including by way of press release, concerning the past misrepresentations and omissions;

(e) an order for an expedited hearing;

(f) the costs of this proceeding, plus all applicable taxes; and

(g) such further and other relief the Tribunal may deem just.

Overview

2. SLCH seeks a cease trading order pursuant to section 127 of the Act in respect of the securities of Stracon Canada.

3. Stracon Canada's Prospectus contains a fundamental misrepresentation: that it owns all of the assets of Stracon Original, as a result of the cross-boarder Amalgamation purportedly completed on November 1, 2025.

4. Contrary to the Prospectus, the Amalgamation has not been completed as a matter of Peruvian law, and the assets of Stracon Original (worth hundreds of millions of dollars) have not transferred to Stracon Canada.

5. A cease trade order is necessary to protect the investing public from the harm that will undoubtedly occur if Stracon Canada's securities begin trading on the TSX based on this fundamental misrepresentation in the Prospectus.

The Parties

6. The applicant, SLCH, is an investment holding company incorporated under the laws of Barbados. It is the plaintiff in an ongoing Peruvian civil action against Stracon Original seeking US$26 million for breach of contract.

7. The non-party, Stracon Original, is a corporation incorporated under the laws of Peru. Stracon Original holds, directly or indirectly, a majority interest in five operating companies that provide mining services in Peru, Canada, Mexico, and Chile. Stracon Original 's assets are worth hundreds of millions of dollars.

8. The respondent, Stracon Canada, is a reporting issuer in Ontario. Following a continuation from the Yukon to Ontario in November 2025, it is a corporation existing under the Ontario Business Corporations Act, R.S.O. 1990, c. B.16.

9. Stracon Canada's shares have been conditionally approved for listing on the Toronto Stock Exchange under the symbol "STG".

The Option Action

10. On August 25, 2025, SLCH commenced a civil action against Stracon Original in Lima, Peru for US$26 million. SLCH alleges that Stracon Original breached the terms of an option agreement under which SLCH was entitled to purchase shares of a third-party company acquired by Stracon Original.

The Amalgamation

11. Steps related to the Amalgamation began in late 2024.

12. On December 17, 2024, 843636 Yukon Inc. (subsequently named Stracon Canada) was incorporated under the laws of the Yukon.

13. On March 11, 2025, Stracon Canada registered a "branch" in Peru, Stracon Group Holdings, Inc. Sucursal del Peru (the "Peruvian Branch").

14. On October 17, 2025, Stracon Original and Stracon Canada entered an amalgamation agreement (the "Amalgamation Agreement") that states:

[the parties] wish to proceed with a long-form amalgamation in accordance with section 183 of the YBCA; and that this transaction shall be considered, for all Peruvian and accounting purposes, as an amalgamation by virtue of which the assets and liabilities of [Stracon Original] shall be assigned to and absorbed into [Stracon Canada's] existing Peruvian Branch...

15. The Amalgamation Agreement provides that Stracon Original "shall transfer, universally and in bulk, its rights, obligations, legal relationships, and in general, all its assets..." to the Peruvian Branch, and that Stracon Original and Stracon Canada shall continue as Stracon Canada, ceasing to exist as separate entities.

SLCH's Objection to the Amalgamation in Peru

16. Under Peruvian law, a creditor (including a contingent creditor) of an entity participating in an amalgamation has a statutory right to object to the amalgamation on the basis that the transaction would prejudice the creditor's interests. Where a timely objection is made, the amalgamation does not take legal effect unless and until the objection is withdrawn or determined by the court.

17. The Peruvian statutory scheme requires the amalgamating entity to publish notice of the proposed amalgamation in an official gazette on three separate occasions. A creditor has 30 days from the date of the final publication to deliver an objection.

18. In Peru, an amalgamation does not take effect unless and until the transaction is formalized by public deed registered in the Peruvian corporate registry. To be validly registered, the deed must include a "certificate of no opposition" sworn by an officer of each amalgamating entity, confirming that they have not been served with an objection within the thirty-day objection period.

19. In this case, the final gazette publication occurred on November 25, 2025, and the objection period expired on December 29, 2025 (on account of the weekend and public holidays for Christmas and Boxing Day).

20. On December 5, 2025, SLCH commenced a proceeding in the Superior Court of Lima (Commercial Court) objecting to the Amalgamation. Stracon Original was served with notice of this proceeding on December 30, 2025.

21. Notwithstanding the foregoing, on January 2, 2026, Stracon Original and Stracon Canada attempted to register the amalgamation deed, relying on a "certificate of no opposition" sworn by Stephen Dixon (as CEO of Stracon Original) on December 26, 2025 and issued before the objection period had expired.

22. On January 19, 2026, the Registrar of the Peruvian Corporate Registry suspended the registration of the deed of amalgamation on the grounds that a judicial proceeding opposing the amalgamation is pending before the Court. The Registrar has suspended the registration until a final decision is issued by the Court in SLCH's proceeding opposing the Amalgamation. The Registrar's decision is subject to confirmation by the Registry Tribunal.

23. As a result, the Amalgamation has not been completed. The assets of Stracon Original have not transferred to Stracon Canada under Peruvian law.

The Fundamental Misrepresentations Contained in the Prospectus

24. The Prospectus ignores this reality.

25. It does not provide full, true and plain disclosure of all material facts relating to the securities of Stracon Canada, as required by section 56(1) of the Act.

26. The core misrepresentation in the Prospectus is the following (underlined for emphasis):

Amalgamation between STRACON Group Holding Inc. (formerly 843636 Yukon Inc.) and STRACON Holdings S.A.: On November 1, 2025, STRACON Group Holding Inc. (formerly 843636 Yukon Inc.) and STRACON Holdings S.A. completed a long-form amalgamation in accordance with Section 183 of the YBCA, and such transaction was deemed to be, for all Peruvian legal and accounting purposes, an amalgamation by virtue of which the assets and liabilities of STRACON Holdings S.A. were assigned to the Peruvian Branch in such a way that such Peruvian Branch absorbed in a single act and universally the assets and liabilities of STRACON Holdings S.A.

As a result of the amalgamation, on November 1, 2025:

(i) In accordance with Section 188 of the YBCA, STRACON Group Holding Inc. (formerly 843636 Yukon Inc.) continued its existence as the Company, organized under the YBCA with the same name and Canadian federal tax identification (i.e., the same Canada Revenue Agency business number). The Peruvian Branch remained the Peruvian Branch of the Company; and

(ii) STRACON Holdings S.A. ceased to exist separately from the Company for Canadian and Peruvian legal and tax purposes.

27. Contrary to the Prospectus, the Peruvian Branch has not "absorbed" the assets and liabilities of Stracon Original, and Stracon Original continues to exist separately from Stracon Canada under Peruvian law.

28. This misrepresentation is repeated throughout the Prospectus, including in the corporate organizational chart contained therein, which purports to identify the "material wholly-owned subsidiaries [of Stracon Canada] ... as of the date of this prospectus." The chart depicts Stracon Canada (through its Peruvian Branch, identified in the chart by the hashed outline) as the owner of several subsidiaries, that, in fact, continue to be held by Stracon Original (which is absent from the chart):

29. The Prospectus also fails to disclose SLCH's objection to the Amalgamation, which is pending before the Superior Court of Peru.

30. By virtue of the misrepresentation, the Prospectus also violates National Instrument 41-101 ("NI 401-101").

31. Section 3.1(1) of NI 401-101 requires a prospectus to be in the form of Form 41-101F1. Under Form 41-101F1, a prospectus must "[g]ive particulars of any material facts about the securities being distributed that are not disclosed under any other Items and are necessary in order for the prospectus to contain full, true and plain disclosure of all material facts relating to the securities to be distributed" (s. 29.1).

32. The Prospectus' failure to disclose SLCH's objection to the Amalgamation, as well as its misstatements that the Amalgamation is complete, are contrary to the disclosure requirement in Form 41-101F1, section 29.1. The Prospectus does not satisfy the requirements of Form 41-101F1 and accordingly violates NI 401-101, section 3.1(1).

The Order Requested is Necessary to Protect the Public and the Applicant Should be Granted Standing

33. An Order pursuant to section 127 of the Act cease-trading the securities of Stracon Canada unless and until the Amalgamation takes effect under Peruvian law is necessary to protect the investing public and maintain the integrity of Ontario's capital markets.

34. In the absence of such an order, Stracon Canada's securities will trade on the basis of a fundamental misrepresentation in the Prospectus: that Stracon Canada owns hundreds of millions of dollars in assets that, in fact, remain assets of Stacon Original under Peruvian law.

35. The Tribunal should exercise its discretion to permit SLCH to bring this application under section 127 of the Act because:

(a) the application relates to both past and contemplated future conduct regulated by Ontario securities law;

(b) the relief sought is future-looking and not purely enforcement in nature;

(c) the Tribunal has the authority to impose an appropriate remedy in the circumstances;

(d) SLCH is directly affected by Stracon Canada's conduct. SLCH has a USD $26 million claim against Stracon Original and Stracon Canada. SLCH therefore has a direct interest in Stracon Canada's ability to satisfy its liabilities. A class proceeding commenced by investors who purchase Stracon Canada's securities in reliance on materially misleading public disclosure would expose Stracon Canada to substantial liability and could materially impair SLCH's ability to enforce any judgment it may obtain against Stracon Canada; and

(e) it is in the public interest for the Tribunal to hear the applicable. This application engages the fundamental purposes of the Act, namely, protecting investors and fostering confidence in capital markets.

36. The Applicant intends to rely on the following evidence at the hearing:

(a) Affidavit(s) of the Applicant to be sworn; and

(b) Such further and other evidence as the lawyers may advise and the Tribunal may permit.

JANUARY 22, 2026 |

ADAIR GOLDBLATT BIEBER LLP |

|

401 Bay Street, Suite 3200 |

||

Toronto, ON M5H 2Y4 |

||

|

||

Simon Bieber (56219Q) |

||

Tel: 416.351.2781 |

||

Email: sbieber@agbllp.com |

||

|

||

Robert Trenker (68606A) |

||

Tel: 416.300.0660 |

||

Email: rtrenker@agbllp.com |

||

|

||

David Ionis (79542U) |

||

Tel: 437.222.0061 |

||

Email: dionis@agbllp.com |

||

|

||

Caroline Harrell (84738D) |

||

Tel: 416.583.1652 |

||

Email: charrell@agbllp.com |

||

|

||

Tel: 416.499.9940 |

||

Fax: 647.689.2059 |

||

|

||

Lawyers for the Applicant |

||

|

||

SLC HOLDINGS INC. |

-and- |

STRACON GROUP HOLDING INC. et al |

Applicant |

Respondent |

|

|

||

ONTARIO CAPITAL MARKETS TRIBUNAL |

||

|

||

NOTICE OF APPLICATION |

||

|

||

ADAIR GOLDBLATT BIEBER LLP |

||

401 Bay Street |

||

Suite 3200 |

||

Toronto, ON M5H 2Y4 |

||

|

||

Simon Bieber (56219Q) |

||

Tel: 416.351.2781 |

||

Email: sbieber@agbllp.com |

||

|

||

Robert Trenker (68606A) |

||

Tel: 416.300.0660 |

||

Email: rtrenker@agbllp.com |

||

|

||

David Ionis (79542U) |

||

Tel: 437.222.0061 |

||

Email: dionis@agbllp.com |

||

|

||

Caroline Harrell (84738D) |

||

Tel: 416.583.1652 |

||

Email: charrell@agbllp.com |

||

|

||

Tel: 416.499.9940 |

||

|

||

Lawyers for the Applicant |

||

Ontario Securities Commission and Ahmed Kaiser Akbar

FOR IMMEDIATE RELEASE

January 22, 2026

TORONTO -- The Tribunal issued its Reasons and Decision in the above-named matter.

A copy of the Reasons and Decision dated January 21, 2026 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

1-877-785-1555 (Toll Free)

FOR IMMEDIATE RELEASE

January 21, 2026

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated January 21, 2026 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Oasis World Trading Inc. et al.

FOR IMMEDIATE RELEASE

January 23, 2026

TORONTO -- The Tribunal issued its Reasons for Decision on a Motion in the above-named matter.

A copy of the Reasons for Decision on a Motion dated January 22, 2026, is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission and Ron Carter Hew

FOR IMMEDIATE RELEASE

January 26, 2026

TORONTO -- The Tribunal issued its Reasons and Decision and an Order in the above-named matter.

A copy of the Reasons and Decision and the Order both dated January 23, 2026, are available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Notice of Correction -- Ontario Securities Commission and Benjamin Ward

File No. 2025-21

(2026), 49 OSCB 756. Please be advised that the following typographical error has been corrected in the Reasons and Decision dated January 16, 2026 in the above matter:

• In the Citation on the cover page, "Ward (Re), 2026 ONCMT 2" is replaced with "Ontario Securities Commission v Ward, 2026 ONCMT 2".

FOR IMMEDIATE RELEASE

January 27, 2026

TORONTO -- The Tribunal issued a Notice of Hearing to consider the application filed by SLC Holdings Inc. dated January 22, 2026, requesting an order that all trading in securities of Stracon Group Holding Inc., shall not commence, or shall immediately cease, unless and until the amalgamation between Stracon Canada and Stracon Holdings S.A. has been completed, and other related relief related to the amalgamation.

A first case management hearing will be held on January 27, 2026 at 3:00 p.m. by videoconference.

A copy of the Notice of Hearing dated January 27, 2026, and Application dated January 22, 2026, are available at capitalmarketstribunal.ca

Members of the public may observe the hearing by videoconference, by selecting the "View by Zoom" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Katanga Mining Limited and Ontario Securities Commission

FOR IMMEDIATE RELEASE

January 27, 2026

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated January 27, 2026 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Katanga Mining Limited and Ontario Securities Commission

FOR IMMEDIATE RELEASE

January 27, 2026

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated January 27, 2026 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

File No. 2025-11

Adjudicators: |

Andrea Burke |

January 21, 2026

WHEREAS on January 20, 2026, the Capital Markets Tribunal held a hearing by videoconference regarding a motion brought by Jack Marks to vary the date for serving and filing Jack Marks' written submissions on the merits set out in the Tribunal's order dated November 17, 2025;

ON HEARING the submissions of the representatives for each of Jack Marks, CNSX Markets Inc. (CNSX), and the Ontario Securities Commission, and on reading the materials filed by Jack Marks and CNSX;

IT IS ORDERED THAT:

1. by no later than 4:30 p.m. EST on January 30, 2026, Jack Marks shall serve and file written submissions on the merits of the application and this date is peremptory to Jack Marks;

2. by no later than 4:30 p.m. EST on March 6, 2026, CNSX shall serve and file responding written submissions on the merits of the application;

3. by no later than 4:30 p.m. EDT on March 13, 2026, Jack Marks shall serve and file reply written submissions on the merits of the application, if any; and

4. by no later than 4:30 p.m. EDT on April 2, 2026, the Ontario Securities Commission shall serve and file written submissions on the merits of the application, if any.

Ontario Securities Commission and Ron Carter Hew -- ss. 127(1), 127.1

BETWEEN:

File No. 2025-19

Adjudicators: |

M. Cecilia Williams |

January 23, 2026

(Subsection 127(1) and s. 127.1 of the Securities Act, RSO 1990, c S.5)

WHEREAS the Capital Markets Tribunal held a combined merits and sanctions and costs hearing in writing to consider whether to make findings against, and impose sanctions on, Ron Carter Hew;

AND WHEREAS the Tribunal made findings against Hew in its Reasons and Decision issued on January 23, 2026;

ON READING the materials filed by the Ontario Securities Commission, and Hew having not filed any materials, although having been properly served;

IT IS ORDERED THAT:

1. pursuant to paragraph 2 of subsection 127(1) of the Securities Act (the Act), trading in any securities or derivatives by Hew shall cease permanently;

2. pursuant to paragraph 2.1 of subsection 127(1) of the Act, the acquisition of any securities by Hew shall cease permanently;

3. pursuant to paragraph 3 of subsection 127(1) of the Act, any exemptions contained in Ontario securities law shall not apply to Hew permanently;

4. pursuant to paragraphs 7 and 8.1 of subsection 127(1) of the Act, Hew shall resign any positions that he holds as a director or officer of an issuer or registrant;

5. pursuant to paragraphs 8 and 8.2 of subsection 127(1) of the Act, Hew is permanently prohibited from becoming or acting as a director or officer of any issuer or registrant;

6. pursuant to paragraph 8.5 of subsection 127(1) of the Act, Hew is permanently prohibited from becoming or acting as a registrant or as a promoter;

7. pursuant to paragraph 9 of subsection 127(1) of the Act, Hew shall pay an administrative penalty of $100,000.00; and

8. pursuant to section 127.1 of the Act Hew shall pay $38,282.87 for costs of the Commission's investigation and hearing.

Katanga Mining Limited and Ontario Securities Commission -- s. 17 of OSA, s. 2(2) of Tribunal Adjudicative Records Act, 2019, and Rule 8(4) of CMT Rules of Procedure

BETWEEN:

File No. 2024-16

Adjudicators: |

Jane Waechter (chair of the panel) |

Russell Juriansz |

|

Dale R. Ponder |

January 27, 2026

(Section 17 of the Securities Act, RSO 1990, c S.5, subsection 2(2) of the Tribunal Adjudicative Records Act, 2019, SO 2019, c 7, Sched 60, and Rule 8(4) of the Rules of Procedure)

WHEREAS the Capital Markets Tribunal held a confidential hearing by videoconference on February 13, 2025, to consider an Application made by Katanga Mining Limited pursuant to section 17 of the Securities Act for an order permitting Katanga to disclose certain information received from the Ontario Securities Commission in connection with the Commission's confidential investigation of Katanga to internal and external counsel of Katanga's parent company, Glencore International AG and Glencore plc;

AND WHEREAS on March 15, 2025, the Tribunal issued an order whereby the adjudicative records in this application were marked as confidential, with certain exceptions, and requested submissions from the parties on whether any of those adjudicative records should remain confidential;

ON READING the written joint submission of Katanga and the Commission and on considering that the parties consent to this order;

IT IS ORDERED THAT:

1. pursuant to subsection 2(2) of the Tribunal Adjudicative Records Act, 2019 and rule 8(4) of the Tribunal's Rules of Procedure, only the filed redacted versions of the following materials shall be made available to the public:

a. Katanga's Application Record, dated December 27, 2024;

b. Katanga's Written Submissions, dated December 27, 2024;

c. Katanga's Supplementary Application Record, dated February 4, 2025;

d. the Commission's Written Submissions, dated February 7, 2025; and

e. the transcript of the February 13, 2025, oral hearing.

Katanga Mining Limited and Ontario Securities Commission -- s. 17 of OSA, s. 2(2) of Tribunal Adjudicative Records Act, 2019, and Rule 8(4) of CMT Rules of Procedure

BETWEEN:

File No. 2025-12

Adjudicators: |

Jane Waechter (chair of the panel) |

Russell Juriansz |

|

Dale R. Ponder |

January 27, 2026

(Section 17 of the Securities Act, RSO 1990, c S.5, subsection 2(2) of the Tribunal Adjudicative Records Act, 2019, SO 2019, c 7, Sched 60, and Rule 8(4) of the Rules of Procedure)

WHEREAS the Capital Markets Tribunal held a confidential hearing by videoconference on November 11, 2025, to consider an Application made by Katanga Mining Limited pursuant to section 17 of the Securities Act for an order permitting Katanga to disclose certain information received from the Ontario Securities Commission in connection with the Commission's confidential investigation of Katanga to its parent company, Glencore plc for disclosure in a civil proceeding in the United Kingdom;

AND WHEREAS on November 20, 2025, the Tribunal dismissed Katanga's application and on November 25, 2025 the Tribunal issued an order whereby the adjudicative records in this application were marked as confidential, with certain exceptions, and requested submissions from the parties on whether any of those adjudicative records should remain confidential;

ON READING the written joint submission of Katanga and the Commission and on considering that the parties consent to this order;

IT IS ORDERED THAT:

1. pursuant to subsection 2(2) of the Tribunal Adjudicative Records Act, 2019 and rule 8(4) of the Tribunal's Rules of Procedure, only the filed redacted versions of the following materials shall be made available to the public:

a. Katanga's Application Record, dated August 6, 2025;

b. the Commission's Application Record, dated September 2, 2025;

c. Katanga's Written Submissions, dated September 12, 2025;

d. Katanga's Supplementary Application Record, dated September 17, 2025;

e. the Commission's Written Submissions, dated October 10, 2025;

f. Katanga's Second Supplementary Application Record, dated November 4, 2025; and

g. the transcript of the November 11, 2025 oral hearing.

Ontario Securities Commission and Ahmed Kaiser Akbar -- ss. 126.1(1)(b), 126.2(1)

Citation: Ontario Securities Commission v Akbar, 2026 ONCMT 3

Date: 2026-01-21

File No. 2024-7

(Subsections 126.1(1)(b) and 126.2(1) of the Securities Act, RSO 1990, c S.5)

Adjudicators: |

James Douglas (chair of the Panel) |

|

Sandra Blake |

||

M. Cecilia Williams |

||

|

||

Hearing: |

June 20, 23, 24, 25, and 26, 2025 |

|

|

||

Appearances: |

Stacy Reisman |

For the Ontario Securities Commission |

Hansen Wong |

||

|

||

Mitchell Fournie For Ahmed Kaiser Akbar |

||

[1] The Ontario Securities Commission brought this application for enforcement proceeding pursuant to s. 127 of the Securities Act{1} (Act) against the respondent, Ahmed Kaiser Akbar. The Commission alleges that Akbar perpetrated a fraud and made misleading or untrue statements contrary to ss. 126.1(1)(b) and 126.2(1) of the Act in relation to two press releases issued by SoLVBL Solutions Inc. and other public filings made by SoLVBL. For the reasons following, and despite the able submissions of counsel for the Commission, we conclude that the Commission failed to prove that Akbar's conduct was a breach of either s. 126.1(1)(b) or s. 126.2(1).

[2] Akbar is a lawyer with considerable experience in securities law and the workings of the capital markets. In December 2021, Akbar's licence to practise law was suspended by the Law Society of Ontario. It remains suspended.

[3] Akbar was instrumental in the formation, financing and operation of Agile Blockchain Inc., a predecessor company of SoLVBL. Akbar, Rahim Allani and Gad Caro were, directly or indirectly through Akbar's spouse and Allani's and Caro's corporations, the initial investors in and principal lenders to Agile.

[4] On February 10, 2021, SoLVBL was formed through a reverse takeover of Agile and continued to carry on the business of Agile. Its common shares were listed for trading on the Canadian Stock Exchange.

[5] Following the reverse takeover, SoLVBL's officers and directors were replaced with nominees of Agile and included Agile's CEO, Raymond Pomroy, and Agile's CFO, Khurram Qureshi.

[6] From the outset, SoLVBL experienced serious financial problems. It had no revenue, was operating at a loss and had a working capital deficiency. Its MD&A for the three months ended March 31, 2021, included a going concern statement. SoLVBL's share price declined steadily through the winter and spring of 2021, and it continued to rely on loans from Akbar, Allani and Caro to fund its ongoing operations.

[7] Regardless of whatever formal titles he may or may not have held, the evidence is clear that, during the relevant period, Akbar was legal counsel to SoLVBL. He performed all the functions one might expect to be performed by in-house counsel of a small publicly traded company, despite not being technically employed in that capacity.

[8] In late April 2021, Akbar, Allani and Caro discussed forming a new company to use SoLVBL's technology to produce non-fungible tokens. On April 27, 2021, Akbar incorporated New Foundation Technologies Corp. Akbar has been the sole director and officer of New Foundation since its incorporation.

[9] On April 29, 2021, SoLVBL entered into a technology licensing agreement with New Foundation pursuant to which New Foundation was granted an exclusive, worldwide licence to use SoLVBL's technology to develop non-fungible token products. The licence agreement called for payment of a one-time fee of $120,000 to SoLVBL. New Foundation's source of funding for the licence fee was, directly or indirectly, Akbar, Allani and Caro. No work was ever performed under the licence agreement and New Foundation never had any business, employees, revenue, products or customers.

[10] On May 13, 2021, and June 3, 2021, SoLVBL issued separate press releases (the Press Releases) that dealt with the licence agreement between SoLVBL and New Foundation and which the Commission alleges contained misrepresentations, either overtly or by omission. Akbar prepared the initial drafts of the Press Releases and sent them for review to Allani, Caro, Pomroy, and, for the May press release, Qureshi.

[11] In each of June and July, 2021, SoLVBL filed a Form 7-Monthly Progress Report with the CSE. SoLVBL also filed a Form 10-Notice of Proposed Significant Transaction with the CSE in June 2021. The Commission submits that these filings contained the same or similar misrepresentations as the Press Releases. Akbar prepared the initial drafts of the filings before they were sent to Pomroy and thereafter filed by SoLVBL.

[12] In July 2021, SoLVBL completed two private placements. Research Capital was the investment adviser to SoLVBL for both financings. The initial financing proposal from Research Capital was made in April 2021. As legal counsel to SoLVBL, Akbar was intimately involved in the efforts associated with shepherding the private placements to successful completion.

[13] SoLVBL raised a total of $4 million through the two private placements. Some of the proceeds were used to repay the loans that had been made, directly or indirectly, by Akbar, Allani and Caro to SoLVBL. Other amounts of the proceeds were used to pay operating expenses, including fees payable to Akbar under an independent contractor agreement he entered into with SoLVBL in July 2021.

[14] On June 18, 2025, the respondent brought a motion seeking to admit into evidence the transcript from the voluntary investigative interview of Stephen Metcalfe, a representative of Research Capital.

[15] During the merits hearing, the parties advised that they had resolved the motion and the Commission was consenting to entering certain redacted excerpts of the Metcalfe transcript as evidence. The Tribunal issued an order reflecting the agreement reached by the parties.{2}

[16] The Commission alleges that:

a. Akbar engaged or participated in acts, practices, or a course of conduct relating to securities that he knew or reasonably ought to have known perpetrated a fraud on persons or companies, contrary to s. 126.1(1)(b) of the Act; and

b. Akbar made statements and omissions that he knew, or reasonably ought to have known, were misleading or untrue and would reasonably be expected to have a material impact on the price or value of a security, contrary to s. 126.2(1) of the Act.

[17] The Commission asks us to find that Akbar was not a credible witness. It submits that Akbar's testimony was frequently self-serving and inconsistent with documentary evidence and testimony from other witnesses. In addition, the Commission cites numerous examples where it argues that Akbar was successfully impeached during cross-examination using the transcript from a prior compelled examination.

[18] Akbar disputes that he was not a credible witness. He points to instances where, in his submission, the Commission has mischaracterized the evidence or is asking us to draw unsupportable inferences from the evidence. On the issue of impeachment more generally, Akbar submits that the alleged instances of impeachment do not pertain to any relevant and material facts and, moreover, cannot be used to support an inference of liability.

[19] We agree with the Commission's submission that Akbar's testimony was, on occasion, inconsistent with the documentary record and the testimony of other witnesses. For example, his attempt to explain a statement in a SoLVBL public filing drafted by him concerning New Foundation's approaching "a few other technology companies with capabilities to develop NFT products" as meaning New Foundation looked at their websites can only be described as fatuous. Similarly, his testimony concerning the role played or to be played by Allani's company in the business of New Foundation was neither consistent with anything in the documentary record nor with Allani's testimony.

[20] We also agree that there were numerous instances in which Akbar was impeached in cross-examination using the transcript from his prior compelled examination. For example, his testimony in chief on the issue of who comprised New Foundation's "mission-driven team" referenced in the June press release was shown to be inconsistent with his testimony on his compelled examination.

[21] More generally, we find Akbar to have been an evasive, and at times argumentative, witness in cross-examination. Coupled with the testimonial inconsistencies and instances of impeachment described above, we find that Akbar was not a generally credible and reliable witness. That said, we agree with Akbar's submission that we cannot infer a breach of Ontario securities law from testimonial impeachment alone, nor does our finding that Akbar was not a credible witness necessarily lead to a conclusion that Akbar committed the alleged breaches referred to above.

[22] The May press release made statements of fact about:

a. a request for proposal from New Foundation which was won by SoLVBL;

b. New Foundation being an international company; and

c. the upcoming signing of the License Agreement.

[23] The June press release made statements of fact about:

a. Vicky Arora, the Director of Licensing for New Foundation;

b. New Foundation's customers in the USA, Europe and Asia;

c. New Foundation being a US-based company with offices in Los Angeles and London, UK; and

d. New Foundation's mission-driven teams.

[24] The Press Releases omitted, among other information, the facts that:

a. New Foundation was incorporated on April 27, 2021, in Ontario by Akbar who was the sole officer and director;

b. New Foundation shared common shareholders and office space with SoLVBL; and

c. those shareholders had outstanding loans to SoLVBL.

[25] The evidence establishes, and we find that:

a. there was no request for proposal in writing or otherwise;

b. New Foundation was an Ontario company with no international ties;

c. New Foundation had no employees, including a Director of Licensing, and no teams;

d. New Foundation had no customers; and

e. the License Agreement was signed prior to the publication of the May press release.

[26] As indicated above, Akbar prepared the initial drafts of the Press Releases. This is clear from the documentary record and was not disputed by Akbar. Despite some changes being made by others, we find that the substance of the statements at issue in the Press Releases remained the same from Akbar's first draft. Similarly, no attempt was made following the first drafts to address the factual misrepresentations in and omissions from the Press Releases referred to above.

[27] Akbar attempted to characterize the impugned statements as aspirational. On their face, the statements purport to be factual, with no qualifying contingencies and no language to suggest they are forward-looking. They are presented as statements of fact.

[28] We find that the statements made in the Press Releases are false and misleading. They created the misleading impression that SoLVBL won a competitive request for proposal and was entering into a transaction with an established international company, with multiple offices, previous business activity and established customers. The evidence clearly demonstrates that none of this was true.

[29] We agree with the Commission's submission that the Forms 7 and Form 10 referred to above contain the same or similar misrepresentations and omissions as found in the Press Releases. However, Akbar submits that it would be an error of law, and procedurally unfair, for the Tribunal to make findings of liability based on allegations that are not anchored in the Application for Enforcement Proceeding (AEP), particularly where the allegations involve fraud. In support of his position, Akbar cites the Court of Appeal for Ontario's decisions in Rodaro v Royal Bank of Canada{3} and Marketology Media Inc. v DGA North American Inc.{4}

[30] The underpinning for Akbar's submission lies in the language of the AEP. After extensively detailing the alleged misrepresentations in the Press Releases, the AEP briefly references allegations of misrepresentations in SoLVBL's Management Discussion and Analyses from May 31, 2021, to May 1, 2022, which the Commission says were "primarily" drafted by Akbar. It also alleges a failure to correct an entry in SoLVBL's financial statements. The AEP later returns to the issue of SoLVBL's failure to correct public filings, but again specifically refers only to the company's MD&A and financial statements. Nowhere in the AEP is there any reference to the Forms 7 or the Form 10. Importantly, the Commission did not pursue any issue of misrepresentations in SoLVBL's MD&A or financial statements at the hearing.

[31] The Commission relies on a paragraph in the AEP that uses the term "other public filings" but makes no specific reference to what those are. The Commission cites the Divisional Court's decision in Phillips v Ontario (Securities Commission){5} in support of its position. Relying on the Court's decision in that case, the Commission argues that the fact that the Forms 7 and Form 10 were drafted by Akbar and produced by SoLVBL, were contained in the Commission's disclosure, were never the subject of a particulars motion by Akbar, were discussed in the investigator's affidavit filed at the hearing and were discussed in the opening statement and again during the hearing without objection, is a full answer to Akbar's position on point.

[32] None of the cases cited by the parties were directly on point. Rodaro holds that it is an error on the part of a trial judge in a civil action to find liability on a theory never pleaded and upon which the parties did not join issue at the trial.{6} Marketology reinforces the principle that it is not open to a trial judge to decide a civil case on a basis that was neither pleaded nor explored in evidence.{7}

[33] In Phillips, the Divisional Court held that the Commission's Statement of Allegations (now an AEP) should not be treated in the same manner as a criminal information or indictment but should rather be viewed through the lens of the Tribunal's public interest jurisdiction where "fairness requires sufficient particularization of the allegations to define the issues, prevent surprise and to enable the parties to prepare for the hearing".{8} The Court went on to find that the Statement of Allegations in the case, which clearly alleged that the individual respondents made misrepresentations contrary to s. 44(1) of the Act but did not refer to the specific evidence relied upon to establish that breach, did not, on the facts of the case, constitute a denial of procedural fairness.

[34] Unlike the facts in our case, Phillips did not address the question of procedural fairness in the context of an AEP that did provide particulars which were later abandoned at the hearing and replaced by new and different particulars. In our view, it is understandable that Akbar did not seek particulars of the allegations in the AEP because particulars of the impugned statements in the MD&A and financial statements were provided. Similarly, while the Forms 7 and Form 10 were in the Commission's disclosure and referenced in the Ferguson affidavit, so were the MD&A and the financial statements. The Commission's opening statement made no specific reference to the Forms 7 and Form 10. When the Chair questioned the purpose of putting the Forms 7 and Form 10 to Pomroy during his examination in chief, Commission counsel described the documents as going to "Mr. Akbar's role" at SoLVBL and part of the "factual matrix". Lastly, when questioned during closing submissions as to whether, in respect of this issue, the Commission had met the requirements of s. 8 of the Statutory Powers Procedure Act (SPPA), {9} which requires that "reasonable information" regarding allegations against the good character of a respondent be provided, Commission counsel simply referred us back to Phillips, a decision that does not specifically address s. 8 of the SPPA.

[35] Viewing this issue through the lens of our public interest jurisdiction and relying upon the principles articulated in Phillips, we conclude that there was insufficient particularization of the allegations relating to the Forms 7 and Form 10 to define the issues, prevent surprise and allow the respondent to prepare for the hearing. Accordingly, we decline to make any determination of liability related to alleged misrepresentations or omissions in those documents.

[36] The Commission alleges that Akbar directly engaged in acts or a course of conduct that constituted a fraud contrary to s. 126.1(1)(b) of the Act. We disagree. We have concluded that the statements and omissions at issue were false or misleading. We have also concluded that Akbar initially drafted the Press Releases which contained the false or misleading statements and omissions and provided his drafts to SoLVBL. However, it was SoLVBL, not Akbar, that made the false or misleading statements and omissions to the investing public when it issued the Press Releases.

[37] Importantly, the Commission did not allege that Akbar participated in a fraud perpetrated on the investing public by SoLVBL, nor did it allege that Akbar perpetrated a fraud on SoLVBL. The gravamen of the Commission's case against Akbar was that, in drafting press releases that contained false statements and omissions, Akbar was the direct perpetrator of a fraud on the investing public contrary to s. 126.1(1)(b) of the Act, a proposition which we find unsupportable in both fact and law.

[38] Subsection 126.1(1)(b) of the Act provides, in part:

A person or company shall not, directly or indirectly, engage or participate in any act, practice or course of conduct relating to securities, ... that the person or company knows or reasonably ought to know,

...

(b) perpetrates a fraud on any person or company.

[39] A fraud analysis under this subsection has two steps, as set out by the Tribunal in Bridging Finance Inc. (Re):{10}

a. determining whether a fraud has occurred, and

b. assessing whether the respondent, directly or indirectly, participated in an act or conduct, related to securities, that they knew (or reasonably ought to have known) perpetrated the fraud.{11}

[40] The term "fraud" is not defined in the Act. Previous Tribunal decisions have consistently applied the test for fraud as set out by the Supreme Court of Canada in R v Théroux.{12} A finding of fraud requires proof of:

a. Objective element:

i. A prohibited act, which can be an act of deceit, falsehood or other fraudulent means, and

ii. Deprivation caused by that act, which includes detriment, prejudice, or risk of prejudice to the financial interests of the victims.

b. Subjective element:

i. Knowledge of the prohibited act, and

ii. Knowledge that the act could have as a consequence the deprivation of another.

[41] If the conduct of a person or company, whether or not a respondent, meets both elements of the test, the first step of the fraud analysis under the Act, namely a finding that there was a fraud, is satisfied.

[42] Once the Tribunal has found that there was a fraud, the second step in the analysis is to consider whether those named as respondents have, as s. 126.1(1)(b) requires, directly or indirectly, participated in any act or conduct, related to securities, that they knew or reasonably ought to have known perpetrated the fraud.{13}

[43] For the second step of the analysis, where the respondent is the alleged perpetrator of the fraud, as is the case with Akbar, the "knows or reasonably ought to know" requirement in s. 126.1(1)(b) is already satisfied by the initial finding of fraud, it being an included or lower standard of subjective mental element than as required under the Théroux test to make that initial finding as against the perpetrator.{14} Therefore, the Commission need show only that the fraudulent conduct was related to securities. That requirement is satisfied if the conduct is directed at investors or other capital markets participants, so as to bring it within the broad protective jurisdiction of the Act.{15} The result for the purposes of the analysis of the alleged breach by Akbar, the sole alleged perpetrator of the fraud at issue, is that steps one and two can effectively be combined.

[44] The Commission failed to establish that Akbar's conduct in drafting the Press Releases containing false statements and omissions and providing them to SoLVBL breached s. 126.1(1)(b) of the Act. Viewed in isolation, the false statements and omissions would arguably satisfy the need to find a prohibited act in accordance with the first branch of the objective element of the Théroux test. However, the statements and omissions were not made to investors, as alleged by the Commission, and therefore were not related to securities as required under the second step of the Bridging framework and by the language of s. 126.1(1)(b) itself. Moreover, providing the draft Press Releases to SoLVBL did not itself cause any loss or risk of loss to investors as required to satisfy the second branch of the objective element of the Théroux test. Considering these conclusions, it is not necessary for us to consider the remaining subjective elements of the fraud test.

[45] The first step of the objective element of the Théroux test is to determine if there was a prohibited act. An act of deceit or falsehood is established by demonstrating that the respondent represented a situation as being of a certain character when it was not{16} and includes situations where misrepresentations were made to induce others to act.{17} Fraud by "other fraudulent means" includes any act that a reasonable person would consider to be dishonest{18} and can encompass omissions or non-disclosure of important facts.{19}

[46] The Commission alleges that Akbar directly perpetrated the fraud at issue. The Commission does not allege that Akbar perpetrated the fraud against SoLVBL. Nor does the Commission allege that Akbar was a participant in a fraud perpetrated by SoLVBL. Regarding the latter, when the Panel asked the Commission during oral argument whether it intended to make submissions about whether Akbar had participated in a fraud perpetrated by SoLVBL, the Commission responded in the negative and confirmed that their sole argument was that Akbar directly perpetrated the fraud at issue.

[47] Akbar's alleged act of fraud was drafting the Press Releases containing the false and misleading information and omissions. Akbar, the Commission alleges, drafted the false statements knowingly to craft a false narrative of a success story for SoLVBL and further concealed the truth with the omissions.

[48] In oral argument, the Commission took the position that it was Akbar's entire course of conduct leading up to the publication of the Press Releases that constitutes the fraud. That course of conduct includes Akbar's:

a. involvement with SoLVBL's predecessor company and the reverse take-over that created SoLVBL;

b. significant loans to SoLVBL;

c. introduction of members of SoLVBL's board to the company;

d. intimate involvement with New Foundation;

e. drafting the Press Releases containing the false statements and omissions; and

f. exploitation of Pomroy's trust.

[49] The Commission further submits that Akbar caused the publication because he knew that Pomroy:

a. had no experience as a Chief Executive Officer of a public company;

b. relied on Akbar as SoLVBL's company counsel; and

c. trusted Akbar entirely.

[50] The Commission argues that Akbar exploited Pomroy's trust by providing him with the Press Releases containing the false statements, while not telling Pomroy that the statements were false.

[51] Pomroy's evidence was that there were things about being an officer of a public company that he did not know much about, including press releases, so he relied on Akbar to help him. He also testified that Akbar regularly drafted SoLVBL's press releases. Pomroy stated that he had known Akbar for a long time, he trusted what Akbar presented to him and there was no indication that his trust was misplaced. He, therefore, did not double check documents Akbar gave him.

[52] Pomroy testified that he reviewed and approved the Press Releases. Pomroy also confirmed in testimony that it was his practice with press releases to circulate them to management, including the Chief Financial Officer, for comment after receiving the drafts from Akbar.

[53] Akbar submits that the Commission cannot use Pomroy's alleged reliance on him to hold Akbar liable for alleged misstatements to the investing public which were made by SoLVBL, following authorization and approval by Pomroy.

[54] Akbar submits that the Commission has not identified any acts or course of conduct carried out by him in his individual capacity that would amount to a contravention of s. 126.1(1)(b) of the Act. At no point did Akbar, in his personal capacity, do anything to represent to the investing public a situation to be of a certain character when it was not. SoLVBL, the public issuer and corporate entity, made the statements in the Press Releases which were published by it on the authority and approval of its management.

[55] We are not persuaded by the Commission's submissions that Akbar's preparation of the initial drafts of the Press Releases and their delivery to Pomroy constituted a breach of s. 126.1(1)(b) of the Act. While, as we previously found, the draft Press Releases contained misrepresentations and misleading omissions of fact, the draft Press Releases and the statements made therein are not, in isolation, an "act, practice or course of conduct relating to securities" such as to bring them within the proscriptive language of s. 126.1(1)(b) of the Act. The Press Releases arguably become acts relating to securities only when they are issued or published by SoLVBL. Before that, they are simply documents internal to SoLVBL, which are unavailable to investors or the capital markets more generally.

[56] Nor do we accept that Akbar's overall course of conduct contravenes the proscriptive language of s. 126.1(1)(b) of the Act. The Commission submits that we should not focus on the fact that SoLVBL issued or published the Press Releases. Rather, the Commission argues that we should do as the Supreme Court of Canada did in R v Zlatic{20} and look to the substance of the matter which, as argued by the Commission, extends to Akbar's entire course of conduct as outlined above.

[57] We are of course bound by Zlatic. However, that case involved the general fraud provisions of s. 380 of the Criminal Code.{21} Subsection 126.1(1)(b) of the Act, in contrast to those general provisions, contains specific proscriptive requirements that have been developed through decisions interpreting and applying the language of the subsection.{22} We decline to ignore those specific requirements and look to a concept of broad substance when we are tasked with determining what constitutes securities fraud under that subsection of the Act.

[58] A fraud contrary to s. 126.1(1)(b) of the Act must both be related to securities and directed against a person(s) or company. The Commission has not alleged that Akbar committed a fraud against SoLVBL, the person that received Akbar's false statements and omissions. The alleged fraud is against the investing public, who were the recipients of the Press Releases. However, Akbar did not make the statements at issue to the investing public; SoLVBL did. If SoLVBL had declined to issue the Press Releases as drafted there would be no act or conduct relating to securities and directed to the investing public such as to engage our jurisdiction under s. 126.1(1)(b).

[59] Moreover, there is insufficient evidence for us to conclude that Akbar caused SoLVBL to issue the Press Releases. Pomroy's evidence that he trusted and relied on Akbar is, in this instance, insufficient. While SoLVBL was in serious financial straits, there was no evidence that it was not an operating company. It had a Chief Executive, albeit inexperienced, a Chief Financial Officer and an independent board. Although Akbar knew members of the board and introduced them to SOLVBL, there was no evidence that he controlled them. While Akbar was a significant shareholder and debtholder of SoLVBL, we saw no evidence that he controlled SoLVBL's activities. Pomroy admitted to circulating the draft Press Releases to SoLVBL's management and to reviewing and approving the documents himself.

[60] The Commission's sole argument in this regard is that Pomroy trusted and relied on Akbar. This does not, in our view, amount to evidence that Akbar "caused" SoLVBL to make the public statements that give rise to the alleged fraud. While Pomroy's trust may have been misplaced, there was no evidence that Akbar deceived Pomroy or otherwise duped him or SoLVBL into issuing the Press Releases.

[61] Accordingly, in the circumstances and having regard to the restrictive manner in which the Commission pled and argued its case, we cannot find that Akbar's drafting of the Press Releases and/or his other impugned conduct constituted a breach of s. 126.1(1)(b) of the Act.

4.5 Did Akbar make misleading or untrue statements contrary to s. 126.2(1) of the Act?

4.5.1 Introduction

[62] The Commission further alleges that Akbar, as the maker of the false or misleading statements in the Press Releases, breached s. 126.2(1) of the Act. Again, we disagree. Our earlier finding that it was SoLVBL, not Akbar, that made the false or misleading statements and omissions in the Press Releases is wholly dispositive of the issue of Akbar's liability under s. 126.2(1). Importantly, the subsection does not allow for liability of persons or companies other than those who make the impugned statement or statements. Accordingly, any liability for corporate actors involved in the making of such impugned statement or statements by a corporation would have to be addressed under s. 129.2 of the Act, an issue which was not before us in this case.

[63] Subsection 126.2(1) of the Act provides:

A person or company shall not make a statement that the person or company knows or reasonably ought to know,

(a) in a material respect and at the time and in the light of the circumstances under which it is made, is misleading or untrue or does not state a fact that is required to be stated or that is necessary to make the statement not misleading; and

(b) would reasonably be expected to have a significant effect on the market price or value of a security, ...

[64] There are four elements that must be satisfied to give rise to liability under the subsection:

(i) a person or company must make a statement that is misleading or untrue;

(ii) the person or company must know, or reasonably ought to know, that the statement is misleading or untrue;

(iii) the statement must be material; and

(iv) the statement must reasonably be expected to have a significant effect on the market price or value of a security.

[65] It is tautological that the proscription applies only to statements made to investors or the investing public, otherwise the materiality and market impact requirements of elements (iii) and (iv) could not be satisfied. In other words, the subsection does not purport to regulate the internal communications of corporations or their communications with external advisors.

[66] The Tribunal's recent decision in TeknoScan Systems Inc. (Re){23} clarified that a misleading statement made by a corporation in a notice to investors was not a statement of the individual corporate managers or directors who prepared and approved the statement. In that case, the notice in question was from the corporation to its shareholders, was signed by the President and CEO of the corporation and was prepared and approved by the individual respondents in their capacities as officers and/or directors of the corporation. In reaching the conclusion that the individual respondents were not personally liable under s. 126.2(1) of the Act for the misleading statements in the notice, the Tribunal held, "As a factual matter, the Notice was issued on behalf of TeknoScan, which was a fully functioning corporate entity, and the Notice was not a statement made by each of the Individual respondents."{24}

[67] The Commission's argument in support of its position that Akbar was the maker of the impugned misleading or untrue statements in the Press Releases was identical for the purposes of his alleged liability under s. 126.2(1) of the Act as it was for the purposes of his alleged liability under s. 126.1(1)(b). Namely, the Commission argues that, although SoLVBL issued or published the Press Releases containing the misleading or untrue statements, it did so only because Pomroy relied upon Akbar to have provided accurate and truthful drafts. Our reasons for rejecting this argument as a basis for finding Akbar to have perpetrated the alleged fraud under s. 126.1(1)(b) apply equally to the Commission's submission that Akbar made the impugned statements for the purposes of establishing the first element of liability necessary to prove a breach of s. 126.2(1).

[68] Accordingly, the Tribunal's reasoning in TeknoScan would appear to apply with equal force to the facts of this case and to lead to a dismissal of the allegation that Akbar breached s. 126.2(1) of the Act. However, the Commission argues that: (i) past jurisprudence of the Tribunal confirms that an individual can be responsible for making misleading statements published by a corporation contrary to s. 126.2(1); (ii) the facts in our case are distinguishable from those in TeknoScan; and (iii) a finding that Akbar "made" the misleading or untrue statements in the Press Releases in breach of s. 126.2(1) is consistent with a purposive and contextual interpretation of the subsection.

[69] In support of its first argument, the Commission cites three prior decisions of the Tribunal. Two are settlement approvals{25} which, in our view, are distinguishable and of limited precedential value, in particular because in both cases the individual respondents admitted to making the impugned statements and, in one case, the individual respondent was actually quoted in the press releases in issue. The third case cited by the Commission is Sulja Bros. Building Supplies, Ltd. et al.,{26} where the Tribunal provided no rationale for concluding that the CEO of a company was liable for a breach of s. 126.2(1) of the Act for failing to stop the issuance by the company of press releases containing misleading or untrue statements or to correct those statements before the press releases were issued.{27} As we explain below, we do not find Sulja to be helpful in deciding the case before us.

[70] The Commission's attempt to distinguish the facts of this case from those of TeknoScan is again predicated on its argument that the trust that Pomroy reposed in Akbar caused Akbar to become the maker of the impugned statements which he, in turn, caused SoLVBL to publish. In support of this argument, the Commission offered no additional evidence that Akbar either personally published the Press Releases or duped Pomroy or SoLVBL into publishing them. Nevertheless, the Commission says the facts of its case are different from those in TeknoScan where the corporate officers and directors drafted and approved the offending notice which was subsequently sent by the corporation to its shareholders.

[71] In support of its third argument, the Commission submits that the Act does not provide that only corporations can be liable for the statements published by a corporation, a rather broad negative proposition with which we do not disagree in the abstract. The Commission goes on to submit that it is open to us to find that a person or company is the maker of misleading or untrue statements for the purposes of finding liability under s. 126.2(1) of the Act, regardless of who published those statements, and that such an interpretation would be consistent with the investor protection purposes of the Act.

[72] Akbar responds to the Commission's arguments by referring to the panel's reasons in TeknoScan and specifically to the language from those reasons quoted above. He also refers us to two decisions from capital markets tribunals in other jurisdictions that dealt with similar misrepresentation proscriptions. The first was the decision of the British Columbia Securities Commission (the BCSC) in Re Cerisse,{28} which dealt with corporate misrepresentations in press releases drafted by an individual who was neither an officer nor a director of the corporation. In dismissing the allegations of misrepresentation against the individual, the BCSC reached the following conclusion: "We find that the mere drafting of press releases combined with attending to the mechanics of dissemination of those releases cannot be said to constitute a respondent 'making' a statement for the purposes of section 50(1)(d)."{29}

[73] The BCSC also held in Cerisse that, while the misrepresentation proscription at issue did not extend to individual corporate actors, the appropriate remedy against officers and directors who authorize, permit or acquiesce in corporate misrepresentations was under s. 168.2 of the British Columbia Securities Act,{30} which is similar to s. 129.2 of the Act.{31}

[74] The second decision Akbar refers to is Re Bluforest Inc.,{32} a decision of the Alberta Securities Commission (the ASC). In that case, the ASC was dealing with a preliminary issue concerning the liability of individuals for corporate misrepresentations where it was unclear whether the notice of hearing adequately alleged that the individual respondents authorized, permitted or acquiesced in the misrepresentations, thereby engaging the deemed liability provision in s. 194(3) of the Alberta Securities Act,{33} which is similar to s. 129.2 of the Act. Before concluding that the notice of hearing in the case did not give adequate notice to the individual respondents of liability exposure under the aforesaid Alberta provision, the ASC quoted extensively from the decision of the Court of Appeal of Alberta in Alberta (Securities Commission) v Workum.{34} The following excerpt from that quote is apposite:

A fundamental principle of corporate law is that a registered corporation is an entity separate and distinct from its officers and members. The concept is one of limited liability. A corporation acts through its officers and directors, but they are not personally liable. The corporate veil will only be pierced if a statute clearly imposes personal liability, or in certain other situations, such as a sham company -- neither alleged nor applicable in this case. Here, the Act, through [what was then] section 194(4) as well as other provisions, provides a means of imposing personal liability for corporate acts. The corporate veil otherwise remains in place.{35}

[75] Akbar responds to the Commission's statutory interpretation argument by submitting that its adoption would result in an unlimited expansion of potential liability under s. 126.2(1) of the Act, reaching beyond corporate officers and directors to anyone who participated in drafting corporate communications. He argues that such an interpretation would be inconsistent with the intent of the Legislature as expressed in s. 129.2 of the Act which limits the extension of liability to corporate officers and directors who authorize, permit or acquiesce in the offending misrepresentation.

[76] In our view, the reasoning of the decisions in TeknoScan, Cerisse and Bluforest is to be preferred to the bald conclusion in Sulja. Unlike the panels in TeknoScan, Cerisse and Bluforest, the panel in Sulja provided no interpretive analysis of how they arrived at their decision to find the respondent corporate officer in breach of s. 126.2(1). Importantly, the decision makes no reference to s. 129.2 of the Act.

[77] We disagree with the Commission's submission that the facts in our case are distinguishable in any material respect from the facts in TeknoScan. Both cases involved allegations of breach of s. 126.2(1) of the Act against individuals who drafted corporate communications which were later disseminated to investors by the corporation. The only factual distinction is that the individuals in TeknoScan were officers and directors of the corporation, whereas Akbar was neither an officer nor a director of SoLVBL at the relevant time.

[78] As to the Commission's statutory interpretation argument, we again adopt the reasoning in TeknoScan, Cerisse and Bluforest. To the extent that the Legislature intended individual respondents to be liable for corporate misrepresentations under s. 126.2(1) of the Act, its intent is expressed in, and limited by, the language of s. 129.2 of the Act, which extends liability to officers and directors who authorize, permit or acquiesce in the misrepresentations of the corporation but not to others such as employees or external consultants.

[79] Accordingly, we are unable to find that the Commission has satisfied the first element required to establish liability under s. 126.2(1) of the Act on the part of Akbar for the impugned statements in the Press Releases. As a result of this conclusion, it is unnecessary for us to consider whether the Commission has satisfied the other required elements through the evidence it led in this case.

[80] In conclusion, we dismiss the application for enforcement proceeding brought by the Commission against Akbar in its entirety. That said, we find Akbar's conduct in this matter to have been reprehensible and unworthy of a lawyer and trusted advisor in the capital markets context. Had the Commission framed its allegations against Akbar differently, we might properly have concluded that it would have been in the public interest to impose sanctions on Akbar under s. 127 of the Act, even absent a contravention of Ontario securities law.

Dated at Toronto this 21st day of January, 2026

{1} RSO 1990, c S.5 (Act)

{2} (2025), 48 OSCB 6083

{3} 2002 CanLII 41834 (ONCA) (Rodaro) at paras 60-63

{4} 2024 ONCA 799 (Marketology) at para 29

{5} 2016 ONSC 7901 (Div Ct) (Phillips)

{6} Rodaro at paras 60-63

{7} Marketology at para 29

{8} Phillips at para 54, quoting YBM Magnex International Inc (Re) (2000), 23 OSCB 1171 at para 6

{9} RSO 1990, c S.22

{10} 2024 ONCMT 23 (Bridging)

{11} Bridging at paras 34-35

{12} 1993 CanLII 134 (SCC) (Théroux) at para 27; Meharchand (Re), 2018 ONSEC 51 (Meharchand) at para 119, citing Théroux at para 20; First Global Data Ltd. (Re), 2022 ONCMT 25 (First Global) at para 346; Feng (Re), 2023 ONCMT 12 at para 37; Bridging at para 34

{13} Bridging at para 35

{14} Bridging at para 36

{15} Act, s 1.1; Committee for the Equal Treatment of Asbestos Minority Shareholders v Ontario (Securities Commission), 2001 SCC 37 at paras 39-45; Pezim v British Columbia (Superintendent of Brokers), 1994 CanLII 103 (SCC) at p 589

{16} Théroux at para 18

{17} Bradon Technologies Ltd (Re), 2015 ONSEC 26 at para 157, citing Théroux at paras 26-27

{18} R v Zlatic, [1993] 2 SCR 29 at 44-45; Solar Income Fund (Re), 2022 ONSEC 2 at para 85, aff'd Kadonoff v OSC, 2023 ONSC 6027; Meharchand at para 120; Quadrexx Hedge Capital Management (Re), 2017 ONSEC 3 at para 20, aff'd Quadrexx Hedge Capital Management Ltd. v Ontario Securities Commission, 2020 ONSC 4392 [Quadrexx]

{19} Hogg (Re), 2024 ONCMT 15 (Hogg), aff'd Hogg v Chief Executive Officer, 2025 ONSC 6214 (Div Ct), at para 136; Money Gate Mortgage Investment Corporation (Re), 2019 ONSEC 40 at para 223

{20} 1993 CanLII 135 (SCC)

{21} RSC 1985, c C-46, s 380

{22} Bridging at paras 30-37; Hogg at paras 131-147

{23} 2024 ONCMT 32 (TeknoScan)

{24} TeknoScan at para 237

{25} Kallo (Re), 2024 ONCMT 29; Pomroy (Re), 2024 ONCMT 10

{26} 2010 ONSEC 27 (Sulja)

{27} Sulja at para 32

{28} 2017 BCSECCOM 27 (Cerisse)

{29} Cerisse at para 103 [emphasis in original]

{30} RSBC 1996, c 418

{31} Cerisse at para 102

{32} 2020 ABASC 138 (Bluforest) [https://www.asc.ca/-/media/ASC-Documents-part-1/Notices-Decisions-Orders-Rulings/Enforcement/2020/08/Bluforest-Inc-DECISION-20200824-5896410.pdf]

{33} RSA 2000, c s-4

{34} 2010 ABCA 405 (Workum)

{35} Workum at para 206

Oasis World Trading Inc. et al.

Citation: Oasis World Trading Inc (Re), 2026 ONCMT 4

Date: 2026-01-22

File No. 2023-38

Adjudicators: |

Mary Condon (chair of the panel) |

|

Andrea Burke |

||

Sandra Blake |

||

|

||

Hearing: |

June 2 and July 4, 2025 |

|

|

||

Appearances: |

Johanna Braden |

For the Ontario Securities Commission |

Hanchu Chen |

||

|

||

Janice Wright |

For Oasis World Trading Inc., Zhen (Steven) Pang and Rikesh Modi |

|

Greg Temelini |

||

[1] The respondents brought a motion to permanently stay this enforcement proceeding against them on the ground of abuse of process. The respondents say that the Commission withheld unquestionably relevant documents and information from them that ought to have been disclosed throughout the proceeding and has demonstrated a fundamental misunderstanding of its disclosure obligations.

[2] We dismissed the respondents' motion on July 9, 2025.{1} These are our reasons for dismissing the respondents' motion and instead granting alternative relief requiring the Commission to conduct a further review of its disclosure and make additional disclosure as applicable, in accordance with its obligations under the Capital Markets Tribunal Rules of Procedure (Rules of Procedure).

[3] These reasons also address our preliminary decision to hear the stay motion when it was brought in the middle of the merits hearing, rather than at the end of the evidentiary portion of the hearing.

[4] This proceeding involves allegations of market manipulation, unregistered trading and failure to establish and maintain systems of control and supervision, against Oasis World Trading Inc., an Ontario company, and two individual respondents associated with Oasis. The alleged market manipulation involves traders in China trading on the Toronto Stock Exchange (TSX) and the Australian Securities Exchange (ASX).

[5] The respondents allege that the Commission has repeatedly withheld relevant documents and information that ought to have been disclosed to them, has sought ways to limit disclosure and has taken positions throughout this proceeding that are contrary to the Commission's disclosure obligations. They further allege that the issue is not simply about late disclosure of certain relevant documents in one proceeding, nor is it about one Commission team's approach to disclosure, but it is instead about the Commission itself not accepting its disclosure obligations.

[6] The respondents assert that at virtually every turn in this proceeding, the Commission has demonstrated its unwillingness to adhere to well-established disclosure obligations, thereby acting in a manner contrary to its responsibilities in the exercise of enforcement powers.

[7] The respondents rely on numerous instances of alleged disclosure deficiencies, as well as the Commission's asserted positions in respect of the same, as grounds for their motion. They say that these instances (particularly when considered together) are offensive to society's notions of fair play and decency. We summarize these instances in chronological order below.

[8] In June 2024, prior to the commencement of the merits hearing, the respondents brought a motion seeking wide-ranging relief related to disclosure, primarily focused on the Commission's witness summaries. On August 27, 2024, the Tribunal issued an order granting some of the requested relief.{2} The Tribunal's Reasons for Decision{3} explained why the Tribunal found the Commission's witness summaries deficient in some respects and ordered the Commission to serve revised witness summaries.

[9] The respondents allege that the 2024 motion is one example of numerous disclosure failures by the Commission, including its failure to disclose the substance of its witnesses' anticipated evidence in accordance with the Rules of Procedure. They emphasize that the Tribunal disagreed with the Commission's position that it need not disclose all of the substance of a witness's anticipated testimony, finding it inconsistent with the principles behind, and the plain words of, rule 28(3) of the Rules of Procedure.{4}

[10] On March 20, 2025, less than six weeks before the start of the merits hearing and well after the deadline set for the Commission to complete its disclosure of relevant documents, the Commission disclosed over 150 English translations of Chinese "QQ chats" as part of the book of documents it intended to rely on at the merits hearing. The Commission obtained many of these English translations years prior, during the investigation leading up to this enforcement proceeding. At the April 3, 2025, case management hearing, the final case management hearing before the start of the merits hearing, the respondents sought production of other English translations prepared by outside translators of relevant Chinese documents in the Commission's possession.