Ontario Securities Commission Bulletin

Issue 48/49 - December 11, 2025

Ont. Sec. Bull. Issue 48/49

• Liquid Marketplace Inc. et al.

• OSC Staff Notice 51-737 -- Corporate Finance Division 2025 Annual Report

• Promino Nutritional Sciences Inc.

• Nodal Exchange, LLC -- s. 144 of the OSA; ss. 38, 78 of the CFA

• Starlight Western Canada Multi-Family (No. 2) Fund

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Nodal Exchange, LLC -- Application for Variation of Exemption Order -- Notice of Commission Order

• Cboe Canada Inc. -- Significant Change and Fee Change -- Dedicated Cores -- Notice of Approval

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Liquid Marketplace Inc. et al.

FOR IMMEDIATE RELEASE

December 4, 2025

TORONTO -- The previously scheduled days of December 15, 16 and 17, 2025 will not be used for the merits hearing in the above-named matter.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

John Cecil and Ontario Securities Commission

FOR IMMEDIATE RELEASE

December 5, 2025

TORONTO - The Tribunal issued an Order in the above-named matter.

A copy of the Order dated December 5, 2025 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Liquid Marketplace Inc. et al.

FOR IMMEDIATE RELEASE

December 8, 2025

TORONTO -- Additional merits hearing dates in the above-named matter is scheduled to be heard on June 18 and 19, 2026 at 10:00 a.m. on each day.

The hearing will be held at the offices of the Tribunal at 20 Queen Street West, 17th floor, Toronto.

Members of the public may observe the hearing by videoconference, by selecting the "Register to attend" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

Registrar, Governance & Tribunal Secretariat

Ontario Securities Commission

Subscribe to notices and other alerts from the Capital Markets Tribunal:

https://www.capitalmarketstribunal.ca/en/news/subscribe

For Media Inquiries:

For General Inquiries:

John Cecil and Ontario Securities Commission

BETWEEN:

File No. 2025-30

Adjudicator: |

Timothy Moseley |

December 5, 202

WHEREAS on December 5, 2025, the Capital Markets Tribunal held a hearing by videoconference regarding an application brought by John Cecil for an order varying a Tribunal order issued on December 11, 2024, in file number 2023-12;

ON READING the materials filed by the representatives for Cecil and on hearing the submissions of the representatives for Cecil and for the Ontario Securities Commission;

IT IS ORDERED that the hearing on the merits of the application is scheduled for February 20, 2026, at 10:00 a.m., at the Capital Markets Tribunal, located at 20 Queen Street West, 17th Floor, Toronto, Ontario, or as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Joint Canadian Securities Administrators and Canadian Investment Regulatory Organization -- Staff Notice 31-369 Guidance on the Application of Securities Legislation to Finfluencer Activity

December 11, 2025

This joint staff notice about finfluencers is published by staff of the Canadian Securities Administrators (CSA){1} and staff of the Canadian Investment Regulatory Organization (CIRO,{2} and together with the CSA, we or securities regulators). We are publishing this staff notice (the Notice) to provide guidance on how securities laws apply to the activities of social media financial influencers (finfluencers) and to registrants and issuers who work with them. We use "securities laws" as a general term to cover requirements which technically may be legislation, regulations, rules or by-laws.

Depending on exactly what you say and do, you may be engaged in activity regulated by securities laws. The context and whether people seeing a post might reasonably be influenced by what you say can matter. If you offer advice about investing you may be required to become registered with securities regulators. However, it is also important to be aware that there is a "general advice" exemption from this registration requirement that many finfluencers will be able to rely on. Finfluencers who rely on the "general advice" exemption must provide clear and timely disclosure when they have financial or other interests in securities that they talk about. Promoting securities for payment from an issuer is subject to securities laws, including disclosure requirements. Finfluencer activity may also be subject to other securities laws, particularly if the activities involve marketing investments or related services or providing a link to a trading platform for implementing copy trading. This notice discusses these laws and gives some examples of how they apply. Other legal requirements in addition to securities laws may sometimes also apply. Securities regulators monitor finfluencer activity. The consequences of acting outside of securities laws can be serious, including significant fines, disgorgement of profits or a ban on working in the securities industry. If you are uncertain where your activities fit after reading this Notice, we encourage you to get professional legal advice.

We consider a finfluencer to be someone who creates online content (such as through various social media platforms, online blogs, or message boards) to offer advice, tips, and guidance on how to manage money, invest, and achieve financial goals. They may not necessarily think of themselves as a finfluencer. They may create content on other topics as well as investing.

Finfluencers have the capacity to reach a wide and diverse audience. They raise awareness about the importance of investing, popularize financial topics, and provide retail investors with easily accessible and helpful information about investing. This is especially the case with young and new retail investors who rely on social media for information about investing.{3} Finfluencers can also play a role in raising awareness about common financial scams and offer practical advice on how to avoid them, among other preventative messages.

Unfortunately, some finfluencers' activities can introduce new risks to retail investors. These risks include the possibility of spreading misleading or biased information, promotion of higher-risk or complex products, inadequate disclosure of any conflicts of interest, and the potential for investors to be encouraged to invest in products that may be unsuitable for them.{4} The consequences for investors who act on bad advice from finfluencers can include poor returns or loss through scams.{5} Risks of these kinds are among the things that securities regulators seek to address as part of their investor protection mandate, including taking enforcement action where necessary to ensure securities laws are complied with.

Finfluencers may not always be aware of the potential application of securities laws to their activities. This Notice is primarily intended to create that awareness among finfluencers and encourage individual finfluencers to consider whether their particular activities may give rise to obligations under securities laws. To that end, this Notice discusses existing securities laws at a high level. It is not intended to present a comprehensive analysis of all possible situations involving finfluencer activity. More details about securities law requirements can be found in the instruments identified in this Notice and in information on the websites of securities regulators.{6} There may also be other relevant legal requirements that we have not identified.{7}

The purposes of securities laws include investor protection. This section describes at a high-level the securities laws most likely to apply to finfluencer activities. It is not an exhaustive inventory of all securities law requirements applicable to finfluencers.

Securities laws are, in many respects, principles-based, which makes them adaptable to new ways of delivering investment services, and they apply regardless of the technology being used to carry out a regulated activity. This means that securities laws can extend to finfluencer activity regardless of whether it is conducted through video, online postings, text messages, television, print or other means, and regardless of whether the finfluencer is a real person or is a computer-generated digital avatar (also referred to as a digital influencer). The same principles apply to the use of artificial intelligence (AI). If someone creates an AI agent or uses AI to provide advice about investing, to promote investments or anything else that is subject to securities laws, that person may be held responsible for what the AI does as if they themselves had done it directly.{8}

Requirement to Register

One of the principal ways securities laws seek to protect investors is by requiring the registration of individuals and firms who encourage others to rely on them for "advice" about investing in securities or for "trading" securities.

• "Advice" includes offering an opinion about the merits of investing in a business or its securities or making a recommendation about an investment in a business or its securities. Note that the use of certain emojis or promotional language such as "not to be missed" and "golden opportunity" could be perceived as investment recommendations. Advising does not include providing purely factual information (e.g., how securities markets work, investing basics, etc.). Finfluencers should consider whether their content could be interpreted as advice about investing in securities.

• "Trading" is defined broadly in securities law and captures the process of fulfilling a buy or sell order (i.e., trade execution services such as those offered by registered dealers), and also "any act, advertisement, solicitation, conduct or negotiation directly or indirectly in furtherance of" a sale of a security.{9} This could include activities such as facilitating "copy trading" by linking others who pay a subscription fee to replicate your trades to a self-directed /do-it-yourself (DIY) trading account.

If advice is given, or if trading activity is undertaken, for a "business purpose" registration is required. Whether an activity is undertaken for a business purpose is a matter of fact. These are some of the factors that are used to determine whether a person is in the business of advising or trading,

(a) Engaging in activities similar to a registrant: for example, by engaging in or representing to others that you are in the business of advising about investing in or buying and selling securities;

(b) Intermediating trades: for example, by connecting buyers and sellers of securities to arrange a trade, or acting as a market maker who buys securities not as an investment but only to sell them;

(c) Directly or indirectly carrying on the activity with repetition, regularity or continuity;

(d) Being, or expecting to be remunerated or compensated: it does not matter in what form or if compensation is actually received; and

(e) Directly or indirectly contacting anyone to solicit securities transactions or to offer advice.

An activity does not have to be the sole or even primary endeavour for it to be a factor. We do not automatically assume that any one factor on its own will determine whether an individual or firm is in the business of advising or trading.{10} It is important to note that the registration requirement cannot be avoided by simply making a disclaimer asserting you are not providing advice or trading securities.

General advice registration exemption

Securities legislation and regulations include certain exemptions from registration requirements. The exemption most likely to be available in respect of finfluencer activities is the "general advice" exemption.{11} It provides that if advice is not tailored to the needs of an individual receiving the advice, the person giving the advice is not required to register as an adviser, but they must disclose any financial or other interest that they have in a security mentioned in connection with the advice. "Financial or other interest" is broadly defined to capture any financial incentive that the party giving the advice might have to favour a particular investment. This includes indirect incentives and circumstances where certain associates have an interest (as described in the exemption's requirements). See below, "How to Make a Required Disclosure".

There is no equivalent exemption for trading activity or acts in furtherance of a trade or the other rules discussed below.

Becoming a Registrant

If someone would like to engage in advising or trading for a business purpose and does not qualify under an available exemption, they must register as an adviser or dealer. They must register with the securities regulator in each province and territory where the advice can be seen, heard or read, or trading services accessed (for internet-based communications, that likely means all of the provinces and territories). To become registered, individuals must be employed as a representative of a registered firm. Registered individuals must meet certain experience and education requirements. Individuals and firms are also subject to screening for integrity and solvency.{12} Registered firms and individuals are required to meet conduct requirements, including addressing material conflicts of interest in the client's best interest, maintaining regulatory capital, and paying fees, among other things.{13} Registered firms and individuals are also subject to an overarching standard of care which requires fairness, honesty, and good faith in dealing with clients.

Marketing, Promotion, and Similar Activities

If a finfluencer receives any form of payment to market the services of a registered dealer or registered adviser they may be entering into a "referral arrangement" subject to requirements set out in securities law. Before entering into arrangements of this kind, finfluencers should take care to ensure that they are dealing with someone who is registered and who has taken the appropriate steps to document the arrangement, as discussed below in the guidance for registered firms working with finfluencers.

If a finfluencer receives any form of payment to market or promote investing in particular securities, or undertake "investor relations" or similar activities, they may be found to be acting on behalf of an issuer or registrant. This will have legal implications for the finfluencer. For example, they may bring themselves into the scope of securities laws that govern the distribution of securities, some of which are referenced below in the guidance for issuers working with finfluencers. This can be a complex area of the law with serious penalties for violations. For example, finfluencers who are paid by issuers have been sanctioned for promoting stocks without complying with requirements that they disclose that they were acting on behalf of an issuer, and that such disclosure be clear and conspicuous.{14} We strongly encourage anyone contemplating undertaking these kinds of activity to consult with legal counsel.

Information about being retained to promote securities, or of a financial or other interest when relying on the "general advice" exemption, must be disclosed. It is important that disclosure be clear and conspicuous. Sufficient information is expected to be provided so that the audience is made aware of the specific nature of the retainer or financial interest, including the security, the nature of the compensation, the issuer or other payer, and the recipient of the payment or other incentive. A general disclosure such as "I may have a financial interest in some of the securities that I mention" will not be sufficient. Disclosure must be made at a point in a communication such as a video or post where the audience will connect it to the advice or promotion. Typically, this will be at the beginning of the communication. It should always be prominent, meaning hard-to-miss in the format of the communication. We would not consider disclosure to be adequate if the information is located at the end of a long video, document or post, or if the reader needs to make additional clicks to hear or see the information in full, or it is expressed in terms which are confusing or unclear.

Illegal Activity

If the general advice exemption is available, a finfluencer may not need to be registered as an adviser under securities law. However, this does not mean that other provisions and prohibitions in securities law will not apply to the finfluencer. For example, finfluencers should be wary that their activities could be considered misrepresentations, market manipulation, or conduct contrary to securities laws relating to marketing-type activity. CSA members also have the power to take action where conduct is deemed to be contrary to the public interest.

Misrepresentations

Securities laws prohibit misrepresentations, such as statements that the person or company making them knows or reasonably ought to know are untrue or misleading concerning a fact or omission that is likely to affect a decision of a reasonable investor or would reasonably be expected to have a significant effect on the market price or value of a security.{15}

Note that this means a statement may be a misrepresentation even if that was not your intention -- you should consider the actual impression your message might convey to a reasonable person receiving it. Precautions to avoid making misrepresentations include taking reasonable steps to ensure that any specific securities that you recommend are legitimate products offered in compliance with applicable laws (such as shares publicly traded on a stock market or a new offering coming to the market under a prospectus).

Market Manipulation

Securities laws prohibit manipulative or deceptive trading. This includes activities that may create misleading pricing or trading activity that is harmful to investors and the integrity of the markets. For example, "pump-and-dump" schemes, which involve buying shares at a low price and then taking action to artificially drive up the price, such as by making false or misleading statements about the security, in order to later sell at a profit. Finfluencers should be careful not to get tricked into working with fraudsters or others who might be engaging in market manipulation, even inadvertently.

The case studies below are designed to help you understand how securities laws apply to finfluencer activities. There are many other possible examples.

Scenario #1: Flora

Flora works at a flower shop and posts a series of short videos on social media called "How Investing is like Fashion". The series garners significant attention for its unconventional presentation of investment concepts.

• We would likely not consider Flora to be in the business of advising if her videos do not involve recommendations or advice about buying and selling securities.

Flora soon begins to offer one-hour fee-based courses on Fashionable Investing 101. There is strong demand for her course and Flora decides to offer a longer course that includes a section on stock buy and sell signals that will help attendees maximize their returns.

• As the one-hour course focuses on providing general information on investing, we would not consider her to be providing advice. However, once she expands the courses to include stock buy and sell signals, she would be advising on investing in securities. We would likely consider Flora to be in the business of advising if she undertakes these activities regularly and is compensated for them. However, so long as the recommendations and advice in the courses are not tailored to the needs of a specific individual receiving the advice, Flora could likely rely on the general advice exemption, but she will then be required to disclose any financial interest that she has in securities that she discusses.

Soon afterwards, Flora's followers start to ask personalized investment questions in the comments sections of her posts, in private server groups, in chat groups, or in direct messaging channels. Flora responds to these questions. Flora thinks these interactions go well so she starts inviting followers to direct message her for personalized advice. Gina contacts Flora. Flora begins to advise Gina on what stocks to buy for a fee. Gina is impressed and starts referring her friends to Flora, and those friends start referring their friends to her. Soon, Flora has over 1,000 followers that she provides tailored advice to.

• Flora is clearly advising others, and we would consider her to be in the business of advising others because she is soliciting followers to offer her services, regularly provides personalized recommendations and advice on securities, and is compensated for this advice. Flora would not be able to rely on the general advice exemption as her advice is tailored to the needs of Gina and the other followers that she provides the service to. Flora would be required to be registered to continue to engage in this activity or must stop providing such services.

Scenario #2: Ethan

Ethan is a self-proclaimed crypto enthusiast and regularly posts information on social media about initial token offerings of crypto asset projects that he believes in. Many of the tokens he likes appear to meet the definition of securities.{16} Ethan is not paid in any way by the founders of those crypto asset projects and has no personal or financial incentive to recommend those crypto assets.

• Depending on the circumstances, including the frequency with which Ethan engages in these activities, Ethan could be in the business of advising. However, since Ethan's recommendations are not tailored to the needs of a specific individual, he may be able to rely on the general advice exemption.

Ethan is excited about the initial token offering of LUCKY, a new crypto asset. The foundation's marketing strategy includes an airdrop. Ethan signs up to participate in the airdrop, in which he will be rewarded with LUCKY tokens if he carries out certain marketing tasks. Ethan starts immediately posting on social media "$LUCKY [x][x]. You should buy it!" and creating memes that are funny and shareable. He also creates a Telegram group and Discord channel to encourage others to join and "raise the $LUCKY".

• Ethan is recommending buying a security (i.e., the LUCKY token) and he would be in the business of advising in securities since he does so with regularity and is compensated for it. If he is careful not to tailor that advice to any one particular individual, he may be able to rely on the general advice exemption, but he would then be required to disclose his financial interest when he recommends investing in $LUCKY.

This catches the attention of UNOCoin, which is the issuer of securities and UNOCoin decides to retain Ethan as a "brand ambassador". In this role, Ethan receives monthly payments and performance bonuses in exchange for ongoing content creation about the project and its securities. He limits his content to general discussion and does not recommend UNOCoin to any one particular investor. In his postings related to UNOCoin Ethan provides the following disclosure: "I get monthly payments from UNOCoin for sharing posts like this, and if you use this affiliate link to purchase UNOCoins, I will receive a commission from UNOCoin at no additional cost to you."

• We would consider Ethan's activities for UNOCoin to be advising activities. Since the advice is not tailored to any particular person, Ethan can continue to rely on the general advice exemption, but Ethan must continue to disclose his financial interest each time he recommends UNOCoin's securities.

• It is important to note that the disclosure Ethan gives in this example is specific to the example and not an all-purpose disclosure. Ethan will need to tailor his disclosure if his compensation arrangements with UNOCoin should change.

• However, if Ethan goes on to share a link enabling his followers to buy and sell UNOCoin's securities on a trading platform and is paid by the followers or the platform, he would be undertaking acts in furtherance of a trade and be required to become registered.

Scenario #3: Jacob

Jacob follows some finfluencers on YouTube and X. He became inspired by these finfluencers and decided to build his own online following by posting about his personal investments. Jacob amassed a following of tens of thousands of subscribers across various platforms, including YouTube. Soon, companies took notice of his following and asked him to post content promoting the purchase of their securities in exchange for payment. Jacob agreed and started making videos on YouTube and posts on X promoting the purchase or sale of the companies' securities. For example, Jacob stated in one of his videos on YouTube "I own 1,000 shares of Company XYZ at a dollar. I wouldn't be surprised if the value tripled by this time next year." Few of Jacob's posts disclosed that they were made on behalf of a company. In fact, Jacob found that disclosing his sponsorship resulted in fewer views. Some of the videos included a disclaimer and sponsorship notice, but these were hidden unless the viewer scrolled down and clicked "Show More".

• Jacob was investigated and prosecuted. He was found to be contravening, among others, securities laws which require disclosure when statements are made by or on behalf of an issuer. Jacob's ignorance of the law was no defence to this contravention, and he was subject to sanctions.{17}

Registrants

Registered firms sometimes engage the services of finfluencers to assist them in widening their online presence in an effort to market the firms' products and services. Engagements of this kind may fall within the requirements and guidance regarding referral arrangements under NI 31-103 and CIRO rules. Securities laws and guidance related to conflicts of interest, marketing activities and advertising should also be considered. Registered firms are reminded that depending on the circumstances, they may be held responsible for statements made on their behalf. There is also the potential for risks to a firm's reputation depending on what is said or done by someone with whom it has a referral or marketing arrangement. The firm must also consider whether they could be facilitating registerable activity by unregistered parties, depending on the activities undertaken by finfluencers with whom they have arrangements.

We expect that registered firms will address these risks and regulatory requirements with appropriate policies, procedures and controls governing their arrangements with finfluencers and ensuring effective ongoing monitoring. These measures include, but are not limited to:

• Performing adequate due diligence on the finfluencer prior to engaging their services or entering into an agreement;

• Establishing written agreements, including referral agreements, that set out the purpose of the arrangement and each party's roles and responsibilities;

• Taking direct steps to ensure that the finfluencer is sufficiently well-informed to be able to discuss the firm and its products and services in a way that is fair, balanced, substantiated and not misleading (e.g., by containing untrue statements, unjustified promises of specific results, or failing to fairly present risks);

• Verifying on an ongoing basis that any claims or statements made by the finfluencer about the firm or the firm's products and services are fair, balanced, substantiated and not misleading, and taking corrective action if they do not;

• Ensuring that employees are adequately trained regarding any direct involvement with finfluencers and, through ongoing monitoring, identifying any unapproved involvement of employees with finfluencers on the firm's behalf; and

• Identifying, disclosing and addressing any material conflicts of interest in the best interest of the client.

Many investors who follow finfluencers are clients of order-execution-only (OEO) dealers. OEO dealers are prohibited from making recommendations to their clients. They should therefore ensure that they are not indirectly making such recommendations or facilitating registerable activity by unregistered others as a result of a referral arrangement with a finfluencer. OEO dealers should take these factors into consideration before they link to, host or provide third-party content, or facilitate copy-trading functionality.{18}

Securities Issuers

Securities issuers should always exercise caution when engaging third parties, including finfluencers, to create interest in buying their securities. Depending on the nature of the activities undertaken by a finfluencer, they may be considered a third-party engaged to generate investor interest in an issuer's securities, which may constitute investor relations activities, promotional activities, or similar communications{19} under securities laws. In those circumstances an issuer may be held responsible for statements made by a finfluencer on its behalf.

When engaging with a finfluencer, it is critical that high-quality disclosure practices are adhered to across all communication channels in order to prevent unbalanced, misleading or selective disclosure. Issuers are reminded of the guidance in CSA Staff Notice 51-348 Staff Review of Social Media used by Reporting Issuers, which emphasizes that content disseminated through social media or other channels should be consistent with the issuer's continuous disclosure record, including documents filed on SEDAR+, and should not be misleading or promotional in a manner that contravenes securities law obligations. Issuers are therefore encouraged to take a proactive approach when working with a finfluencer to promote their securities. They are expected to ensure the finfluencer is aware of the issuer's obligations under securities law regarding public communications. This may include providing appropriate training and guidance. We would also expect the issuer to implement appropriate controls to ensure that statements the finfluencer may make on its behalf comply with the issuer's obligations under securities laws. This includes taking appropriate steps to ensure that:

• the content is factual, balanced, does not contain any misrepresentations about the issuer's business or affairs, even if unintended, and does not create a misleading appearance of trading activity or contribute to an artificial price for a security;

• forward looking information is not selectively disclosed;

• payment for the promotional relationship is prominently disclosed; and

• the finfluencer does not engage in fraudulent or deceptive practices.

Securities regulators, in cooperation with domestic and international partners, monitor finfluencers' online activities for potential breaches of securities laws. Where concerns are identified, we will seek to protect the public interest by employing a range of tools to respond proportionately to non-compliance with securities laws. Among other potential consequences, this may lead to regulatory action, including enforcement proceedings before an administrative tribunal. This could lead to a finfluencer being required to pay significant fines, costs, disgorgement of any profits, or a prohibition from working in the securities industry.

Please refer any questions to the following staff:

Ontario Securities Commission

{1} The CSA is the council of the securities regulators of Canada's provinces and territories. It coordinates and harmonizes regulation for the Canadian capital markets.

{2} CIRO is the self-regulatory organization that oversees all investment dealers and mutual fund dealers, and trading activity on Canada's debt and equity marketplaces.

{3} See "Finfluencers. Final Report", Report of the Board of International Organization of Securities Commissions (IOSCO) (May 2025).

{4} See the IOSCO "Finfluencers. Final Report"

{5} OSC Research Report: Social Media and Retail Investing: The Rise of Finfluencers (2025), available at https://www.osc.ca/en/investors/investor-research-and-reports/social-media-and-retail-investing-rise-finfluencers; Kakhbod et al (2025) Finfluencers. Swiss Finance Institute Research Paper Series, No. 23 -- 30, 2. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4428232; Merkley et al (forthcoming) Crypto-Influencers. Review of Accounting Studies https://ssrn.com/abstract=4412017

{6} Although securities laws are made by the individual provinces and territories, they are harmonized in most regards and make extensive use of a system of national instruments. Additional rules applicable to investment dealers and mutual fund dealers are made by CIRO.

{7} Potentially including the Consumer Protection Act, or standards such as those applicable to advertisers and deceptive marketing practices, among others.

{8} For more information about the use of AI in capital markets, see CSA Staff Notice and Consultation 11-348 Applicability of Canadian Securities Laws and the use of Artificial Intelligence Systems in Capital Markets (December 5, 2024).

{9} See, for example, section 1(1) of the Ontario Securities Act; section 1(1) of the British Columbia Securities Act; section 1(jjj)(vi) of the Alberta Securities Act; definition of "dealer" in section 5 of the Québec Securities Act.

{10} For a more detailed discussion, see Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations (31-103CP).

{11} See section 8.25 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103) and section 34 of the Ontario Securities Act.

{12} The process for applying for registration is set out in National Instrument 33-109 Registration Information and related guidance is provided in Companion Policy 33-109CP Registration Information, as well as staff notices and other instruments issued by the CSA.

{13} NI 31-103 is the core requirement setting out proficiency and conduct requirements.

{14} Re Floreani, 2025 ABASC 41; and Re Stock Social Inc., 2023 BCSECCOM 52.

{15} Requirements in different provinces may vary in their details. See, for example, subsection 50(2) of the British Columbia Securities Act, subsection 92(4.1) of the Alberta Securities Act, subsection 112.3(1) of the Manitoba Securities Act, subsection 126.2(1) of the Ontario Securities Act and section 197 of the Québec Securities Act.

{16} For more about when crypto assets are securities and how trading in them is regulated see CSA Staff Notice 46-307 Cryptocurrency Offerings and CSA Staff Notice 46-308 Securities Law Implications for Offerings of Tokens.

{17} This example is based on a decision of the Alberta Securities Commission that James Domenic Floreani and Jayconomics Inc. breached the Securities Act (Alberta) by engaging in investor relations activities and failing to disclose that social media posts he shared as part of those activities were made on behalf of four Alberta issuers. See Re Floreani for more information. Alberta securities law, among others, requires disclosure about being retained to promote an issuer to be clear and conspicuous.

{18} OEO dealers should review CIRO guidance and any related guidance from other securities regulators for further information. They can contact CIRO with questions about the application of CIRO rules in different scenarios.

{19} "Investor relations activities, promotional activities, and similar communications" include social media posts, blogs, message boards, videos, or other online content and could constitute a form of public disclosure that may trigger securities law obligations, even if the content is not intended for investors.

OSC Staff Notice 51-737 -- Corporate Finance Division 2025 Annual Report

OSC Staff Notice 51-737 -- Corporate Finance Division 2025 Annual Report is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Notice.

December 9, 2025

Message from the Senior Vice President |

5 |

||

|

|||

Fiscal 2025 at a Glance |

6 |

||

|

|||

|

Right-Size Regulation |

6 |

|

|

|||

|

Regulatory Oversight |

6 |

|

|

|||

|

Emerging Trends |

7 |

|

|

|||

Fiscal 2025 Snapshot |

8 |

||

|

|||

Introduction |

9 |

||

|

|||

Corporate Finance Division: Who We Are & What We Do |

9 |

||

|

|||

|

Corporate Finance Department |

10 |

|

|

|||

|

Department of the Chief Accountant |

11 |

|

|

|||

|

Department of Mergers & Acquisitions |

11 |

|

|

|||

Part A -- Corporate Finance Department |

13 |

||

|

|||

|

Policy Initiatives |

13 |

|

|

|||

|

Policy Highlights |

13 |

|

|

|||

|

|

Access Model for Certain Continuous Disclosure Documents |

13 |

|

|||

|

|

Blanket Orders to Support Competitiveness of Canadian Markets |

13 |

|

|||

|

|

Climate-related Disclosures |

15 |

|

|||

|

|

Disclosure for Mineral Projects |

16 |

|

|||

|

|

Well-known Seasoned Issuers |

16 |

|

|||

|

|

Self-Certified Investor Prospectus Exemption |

17 |

|

|||

|

|

Semi-Annual Reporting Pilot (SAR Pilot) |

17 |

|

|||

|

Continuous Disclosure Oversight |

18 |

|

|

|||

|

|

CDR Program Outcomes for Fiscal 2025 |

19 |

|

|||

|

|

Trends and Guidance |

22 |

|

|||

|

Public Offerings |

30 |

|

|

|||

|

|

Prospectus Trends |

30 |

|

|||

|

|

Common Prospectus Issues |

31 |

|

|||

|

|

Crypto Asset Industry |

35 |

|

|||

|

Exempt Market |

38 |

|

|

|||

|

|

Oversight |

38 |

|

|||

|

|

Trends and Guidance |

39 |

|

|||

|

Financial Benchmarks and Designated Rating Organizations |

44 |

|

|

|||

|

|

Financial Benchmarks |

44 |

|

|||

|

|

Designated Rating Organizations |

44 |

|

|||

|

Exemptive Relief Applications |

45 |

|

|

|||

|

|

Trends and Guidance |

46 |

|

|||

|

Insider Reporting Oversight |

48 |

|

|

|||

Part B -- Department of the Chief Accountant |

49 |

||

|

|||

|

Introduction |

49 |

|

|

|||

|

Notable Topics |

49 |

|

|

|||

|

|

IFRS 18 Presentation and Disclosure in Financial Statements |

49 |

|

|||

|

|

Risk of Misleading Non-GAAP Financial Measures |

51 |

|

|||

|

|

Valuation in Financial Reporting |

52 |

|

|||

|

|

Unaudited Information in Audited Financial Statements |

53 |

|

|||

|

|

Issue-Oriented Review: Cash Flows and Liquidity Disclosures |

54 |

|

|||

Part C -- Department of Mergers and Acquisitions |

57 |

||

|

|||

|

Overview |

57 |

|

|

|||

|

Real-Time Review Program |

57 |

|

|

|||

|

Trends and Guidance |

58 |

|

|

|||

|

|

Financial Hardship Exemption for Related Party Transactions |

59 |

|

|||

|

|

Previously Agreed to and Generally Disclosed Transactions |

61 |

|

|||

|

|

Minority Approval Via Written Consent |

62 |

|

|||

|

M&A Hearings |

63 |

|

|

|||

|

|

Policy and Engagement |

64 |

|

|||

Part D -- Resources |

65 |

||

|

|||

|

OSC Website |

65 |

|

|

|||

|

Service Commitments |

66 |

|

|

|||

|

Administrative Matters |

66 |

|

|

|||

|

SME Institute |

66 |

|

|

|||

Appendix A -- Glossary |

67 |

||

|

|||

Appendix B -- Responsive Regulation |

71 |

||

|

|||

Contact Information |

81 |

||

Message from the Senior Vice President

We are proud to share our Corporate Finance Division 2025 Annual Report (Report). This Report reflects the first operational year of the Corporate Finance Division (the Division) since the Ontario Securities Commission (the OSC) was reorganized as part of its six-year Strategic Plan.

This Report provides an overview of our policy and operational work for the fiscal year ended March 31, 2025 (Fiscal 2025), including our observations and guidance on regulatory requirements in certain areas.

The rapidly evolving global political and economic environment is contributing to a dynamic landscape, where issuers, investors and other market participants have evolving needs. In response, the Division continues to prioritize our core regulatory operations, responding to emerging risks and trends with timeliness and agility, and taking measures to support Issuers at every stage of their development. For example, we collaborated with our partners in the Canadian Securities Administrators (CSA) to publish four co-ordinated blanket orders designed to reduce burden and increase opportunities for capital formation in both public and exempt markets.

Looking ahead, to support the OSC's vision of making Ontario's capital market's inviting, thriving and secure, we will remain focused on providing balanced, flexible and responsive regulation through our regulatory oversight of Ontario's Reporting Issuers and other market participants, without compromising investor protection.

Lastly, I want to thank staff in executing our regulatory role.

Best regards,

•

Published four harmonized blanket orders that foster capital formation while maintaining strong investor protection.

•

Proposed new prospectus exemptions to provide new sources of capital for eligible non-investment fund Issuers.

•

Proposed a multi-year pilot to allow eligible Venture Issuers to voluntarily adopt semi-annual financial reporting.

•

Further reduced the regulatory burden for well-known seasoned issuers (WKSIs) by introducing a permanent regime.

•

Reviewed approximately 300 prospectuses and 300 exemptive relief applications.

•

With the Economic Market and Analysis group, launched a dashboard that provides an overview of prospectus-exempt distributions by corporate issuers headquartered in Canada that raised capital from Ontario investors (the Dashboard).

•

Supported compliance with ongoing reporting obligations by completing over 350 continuous disclosure (CD) reviews.

•

Contributed to national harmonization efforts through various CSA committees.

•

Enhanced transparency regarding the use of the offering memorandum exemption by introducing the Annual Financial Statements Non-Delivery List.

•

Engaged with investors and market participants through educational and outreach programs through SME seminars and OSC Innovation Office.

•

Engaged with external stakeholders and other regulatory agencies on emerging, novel, or complex accounting, auditing, and related financial reporting issues.

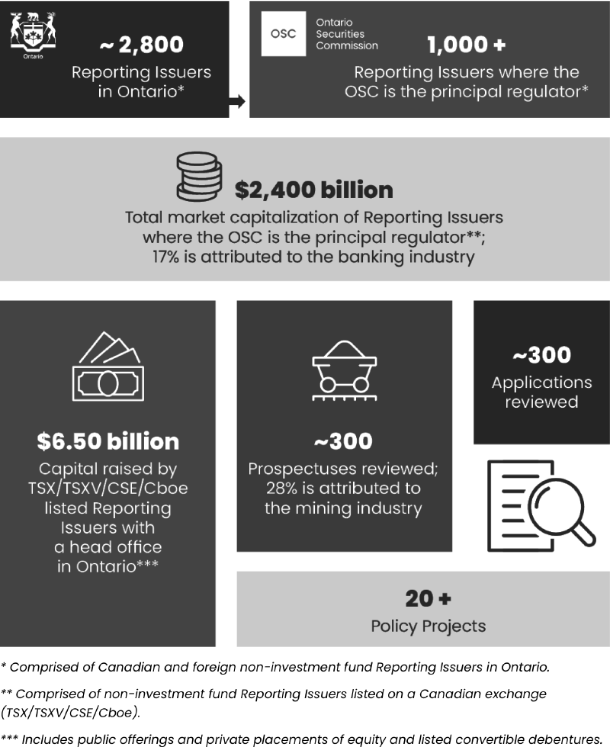

* Comprised of Canadian and foreign non-investment fund Reporting Issuers in Ontario.

** Comprised of non-investment fund Reporting Issuers listed on a Canadian exchange (TSX/TSXV/CSE/Cboe).

*** Includes public offerings and private placements of equity and listed convertible debentures.

This Report provides an overview of the Division's operational and policy work during Fiscal 2025, including a summary of key findings and outcomes from our regulatory oversight programs and a status report of ongoing Issuer-related policy initiatives. The Report is intended for entities and individuals we regulate, their advisors, as well as investors and other market participants.

Through this Report, we aim to:

• REINFORCE the importance of complying with regulatory obligations;

• PROVIDE GUIDANCE to support improved disclosure and compliance practices;

• HIGHLIGHT key trends in Ontario's capital markets; and

• INFORM AND UPDATE stakeholders on new and ongoing policy initiatives.

The Division supports the OSC's mandate and vision to make Ontario's capital markets inviting, thriving and secure. Through our oversight role, we support the OSC's goal to improve transparency, trustworthiness, and efficiency in Ontario's capital markets.

In addition to operational work, the Division is engaged in policymaking to update, enhance and streamline securities regulation in alignment with the OSC's mandate.

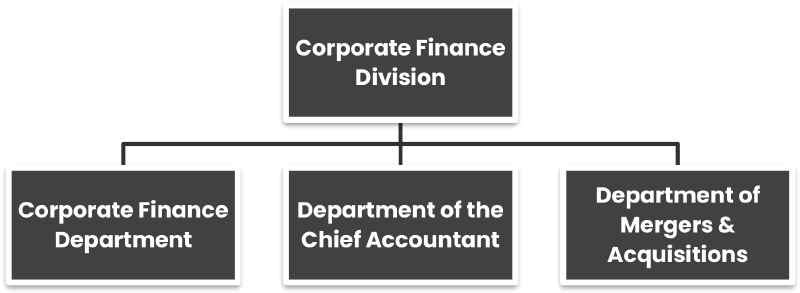

The Division's functions are organized among the following three departments:

The Corporate Finance Department (CFD) focuses on the oversight of Issuers in Ontario.

The CFD's operational work includes:

Disclosure Oversight (CD, Public Offerings and Exempt Market)

• assessing, using risk-based criteria, whether Issuers in Ontario are providing the required level of disclosure of material information to investors so they can make informed investment decisions, including through the review of

• CD filed by Reporting Issuers;

• public offerings of securities by Reporting Issuers;

• capital raising activities in the exempt market;

Exemptive Relief Applications

• reviewing and considering applications for exemptive relief from regulatory requirements;

Other Regulatory Oversight

• reviewing credit rating agencies that are designated rating organizations;

• overseeing designated benchmarks and benchmark administrators;

• overseeing the listed Reporting Issuer function for OSC-recognized exchanges;

• reviewing insider reporting;

Stakeholder Engagement, Guidance and Education

• responding to inquiries and complaints;

• engaging with stakeholders, including external advisory committees;

• providing guidance to stakeholders through staff notices that communicate expectations and interpretations of regulatory requirements in certain areas; and

• delivering education and outreach programs.

The Department of the Chief Accountant (DCA) provides advisory services relating to accounting and assurance for all divisions in the OSC and is involved with policy initiatives focused on financial reporting. The DCA also engages with various external stakeholders that are involved with financial reporting, including standard setters, audit regulators, and professional accounting firms.

The DCA's operational work includes:

• overseeing securities rules and regulations related to financial reporting frameworks (e.g., IFRS Accounting Standards);

• providing advisory services to the OSC for complex accounting or assurance issues;

• advising the OSC on the impact of new financial reporting developments; and

• engaging with external stakeholders on significant financial reporting matters.

The Department of Mergers and Acquisitions (DM&A) is responsible for the regulation of mergers and acquisition (M&A) transactions and the unique risks faced by shareholders in evolving capital markets. The DM&A focuses on matters relating to take-over bids, issuer bids, business combinations, related party transactions, early warning requirements, conflict of interest transactions, defensive tactics and minority shareholder rights.

The DM&A's operational work includes:

• real-time monitoring and supervising of M&A transactions;

• responding to complaints;

• responding to inquiries;

• reviewing and considering exemptive relief applications;

• participating in M&A hearings, including making submissions and working with parties to narrow issues and navigate procedural matters; and

• engaging with stakeholders on emerging trends and policy issues.

The CFD continues to play a leading role in several significant policy initiatives with other securities regulators in the CSA in addition to policy initiatives that are applicable only in Ontario.

Policy initiatives that were implemented or achieved significant milestones over the last year to the date of this Report are outlined below. A complete list of our current policy projects can be found in Appendix B.

Access Model for Certain Continuous Disclosure Documents

On November 19, 2024, the CSA published for a 90-day comment period revised proposals to introduce an access model for annual financial statements, interim financial reports and related management's discussion & analysis (collectively, CD documents) for non-investment fund Reporting Issuers. Implementing an access model for CD documents will modernize the way CD documents are made available to investors and provide a more timely and environmentally friendly way of communicating to investors than paper delivery. Generally, access will be provided once the CD document is filed on SEDAR+ and a news release is issued to advise that the CD document is accessible on SEDAR+, the SEDAR+ notification functionality is available, how to obtain an electronic or paper copy of the document and that standing instructions can be provided.

On April 17, 2025, the CSA introduced three blanket orders aimed at supporting the competitiveness of Canada's capital markets.

CBO 41-930 supports the competitiveness of Canada's public markets by making it more cost-effective for Issuers to go public in Canada through an initial public offering (IPO) prospectus and by streamlining other disclosure requirements. Key relief includes:

• allowing Issuers to exclude audited annual financial statements and operating statements for the third most recently completed financial year in their IPO prospectuses and, circulars or material change reports that are filed in relation to a restructuring transaction;

• allowing Issuers to include, subject to certain conditions, specified pricing information in marketing materials and standard term sheets distributed during the waiting period without first disclosing the information in a preliminary prospectus or an amendment to a preliminary prospectus; and

• allowing Issuers, in Ontario and certain other jurisdictions, to exclude promoter certificates from a prospectus where the promoter signs a certificate in the prospectus in another capacity, subject to the satisfaction of specified conditions.

CBO 45-930 provides a prospectus exemption for companies that will be going or have recently gone public in Canada through an underwritten IPO, giving them greater flexibility to raise additional capital following the IPO, provided certain conditions are met.

The key relief provides that, subject to certain conditions, within the 12-month period after a receipt is issued for a final long form IPO prospectus for an underwritten offering, a Reporting Issuer may, in total, distribute up to the lesser of $100,000,000 or 20% of the aggregate market value of the Reporting Issuer's listed equity securities on a specified date.

CBO 45-933 provides Issuers greater access to capital by providing an exemption from the $100,000 investment limit in NI 45-106, such that a re-investment of proceeds of disposition of an investment in the same Issuer does not count towards the investment limit, provided that the investor receives advice from a registered dealer or registered adviser that the re-investment of proceeds and any new investment under the offering memorandum exemption continues to be suitable for the investor.

In Ontario, all three blanket orders will expire on October 16, 2026, unless extended.

On May 14, 2025, the CSA published CBO 45-935, which increased the capital raising limit under the listed issuer financing exemption. Pursuant to CBO 45-935, listed Reporting Issuers can raise the greater of $25 million and 20% of the aggregate market value of their listed securities, up to a maximum of $50 million in a 12-month period, subject to certain conditions.

In Ontario, CBO 45-935 will expire on November 15, 2026, unless extended.

In response to increased uncertainty and rising competitiveness concerns for Issuers, on April 23, 2025, the CSA announced that it had paused its work on the development of a new mandatory climate-related disclosure rule.

We remind Issuers that existing securities legislation requires disclosure of material climate-related risks and related matters in an Issuer's regulatory filings. We also remind Issuers that misleading climate-related disclosures (often referred to as greenwashing) are not permitted under securities law. We refer Issuers to the following staff guidance, previously issued by the CSA, that may assist Issuers with climate-related disclosure:

• CSA Staff Notice 51-333 Environmental Reporting Guidance (2010) provides guidance on reporting of material environmental risks, including climate- related risks, and related matters.

• CSA Staff Notice 51-358 Reporting of Climate Change-rated Risks (2019) provides guidance on how Issuers might approach preparing disclosures about material climate-related risks.

• CSA Staff Notice 51-365 (2024) provides guidance on avoiding overly promotional claims by Issuers that could potentially be considered "greenwashing".

We continue to review disclosure of climate-related matters as part of our ongoing CD review program.

Following the CSA's publication of Consultation Paper 43-401 Consultation on National Instrument 43-101 Standards of Disclosure for Mineral Projects in 2022, on June 12, 2025, the CSA proposed amendments to NI 43-101, Form 43-101F1 and Companion Policy 43-101CP. The proposed amendments are intended to clarify, harmonize and streamline Canada's mining disclosure regime without introducing any new requirements. Specifically, the proposed amendments would update and enhance the standards for disclosing scientific and technical information about mineral projects to address evolving disclosure practices and policy considerations identified by CSA staff, and to reflect changing industry and investor expectations. The comment period for the proposed amendments ended on October 10, 2025.

On August 28, 2025, the CSA published final amendments to NI 44-102 to introduce a permanent expedited shelf prospectus regime for WKSIs in Canada. The amendments foster capital raising and support the competitiveness of Canadian markets by reducing regulatory burden for eligible WKSIs. The amendments came into force on November 28, 2025, and allow eligible WKSIs to:

• file a final base shelf prospectus and be deemed to receive a receipt for that prospectus without first filing a preliminary base shelf prospectus or undergoing any regulatory review;

• omit certain disclosure from the base shelf prospectus; and

• benefit from receipt effectiveness for a period of 37 months from the date of its deemed issuance, subject to the requirement for the Reporting Issuer to reassess its qualification to use the WKSI regime annually.

On September 25, 2025, the OSC published for comment new prospectus exemptions in CSA MI 45-111, which will provide new sources of capital for non-investment fund Issuers that have their head office in Canada and increased investment opportunities for investors who may not meet the financial thresholds or other criteria required to qualify as an accredited investor. In order to qualify, investors must meet other criteria intended to demonstrate financial knowledge, investment knowledge or relevant industry-specific experience, and acknowledge that they understand certain investment considerations and risks, among other conditions.

The OSC also published a new blanket order, OI 45-510, which came into effect on October 25, 2025, for an 18-month period. OI 45-510 provides time-limited prospectus exemptions, based on the self-certified investor prospectus exemptions in CSA MI 45-111 while the proposed multilateral instrument is being considered.

The OSC also published local amendments to section 2.4 of NI 45-106 to allow private issuers to distribute securities to self-certified investors under OI 45-510 and OI 45- 507 (collectively, the Class Orders) without losing their status as a private issuer and their ability to rely on the private issuer prospectus exemption in NI 45-106. The local amendments also amend section 2.4 of NI 45-106 to provide that the prohibition against paying a commission or finder's fee to any director, officer, founder or control person of an Issuer does not apply to a distribution to a self-certified investor in reliance on the Class Orders. The local amendments came into force on December 4, 2025.

On October 23, 2025, the CSA published for a 60-day comment period proposed CBO 51-933 to introduce a multi-year pilot project which would allow eligible Venture Issuers to voluntarily adopt semi-annual financial reporting, subject to certain terms and conditions. The SAR Pilot, which would include exemptions from certain CD requirements, aims to reduce administrative burden and costs associated with the preparation of the first and third quarter financial disclosures.

Upon adoption, Ontario's local blanket order will include an 18-month expiry date based on the statutory term limits for blanket orders. Therefore, the OSC concurrently published for a 60-day comment period proposed OSC Rule 51-507 to maintain the CD exemptions that will be in Ontario's local blanket order after its expiry.

The comment period for the SAR Pilot will end on December 22, 2025. The CSA anticipates the SAR Pilot will be in force prior to the end of March 2026.

This section provides an overview of the key findings and outcomes from our Fiscal 2025 CD review program (CDR Program). We highlight key or novel issues, discuss best practices, and reference relevant legislation and guidance to assist Issuers in addressing each topic.

Under Ontario securities law, a Reporting Issuer must provide timely and periodic CD about its business and affairs. The CDR Program seeks to assess whether Reporting Issuers are complying with disclosure obligations and to identify material deficiencies that may affect the reliability and accuracy of a Reporting Issuer's disclosure record. For further information about the CDR Program, refer to CSA Staff Notice 51-312, CSA Staff Notice 51-365 and our website.

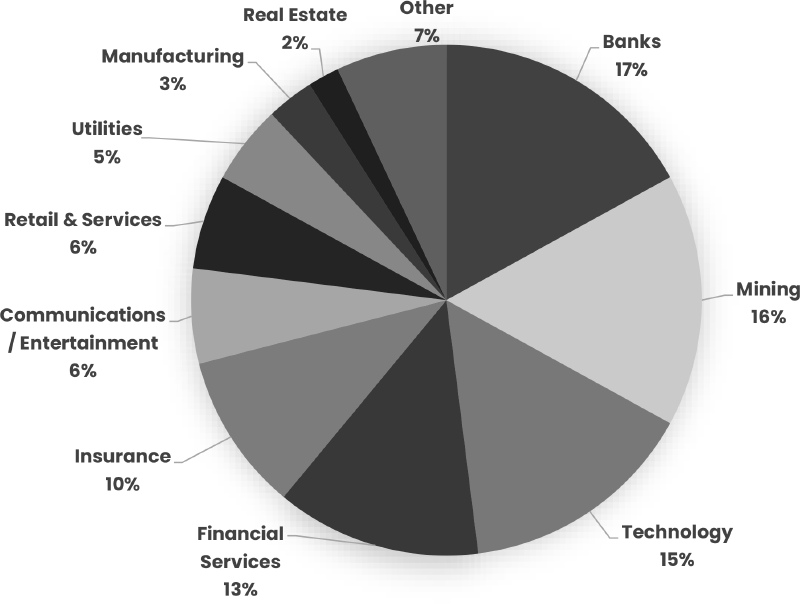

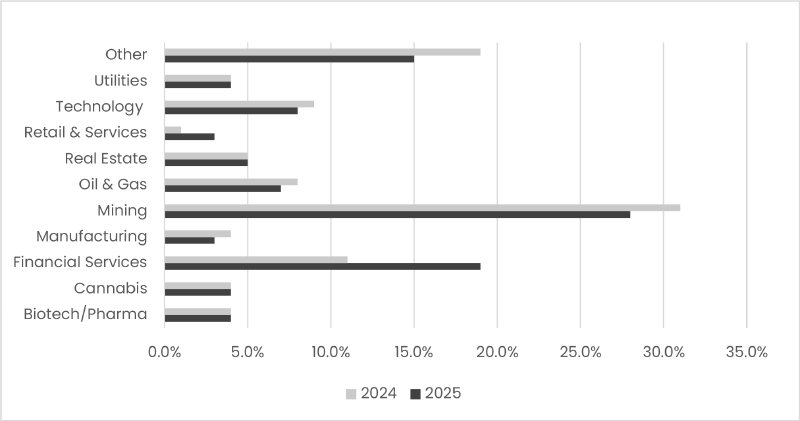

The Division has primary responsibility as principal regulator{2} over 1,000 Reporting Issuers with an aggregate market capitalization of approximately $2,400 billion as of March 31, 2025. The three largest industries by market capitalization were banking, mining, and technology.

The CDR Program is conducted pursuant to the powers in subsection 20.1(1) of the Act and is part of a harmonized CDR Program across the CSA.{4} Our CDR Program is risk-based and outcome-focused. It includes planned full reviews and issue- oriented reviews (IORs) based on risk criteria as well as ongoing monitoring through news releases, media articles, complaints, and other sources.

As public markets evolve over time, we see different industries and/or issues gain public prominence and attract significant amounts of investor capital. We reassess our selection criteria to reflect emerging risks and trends, which impacts file selection accordingly.

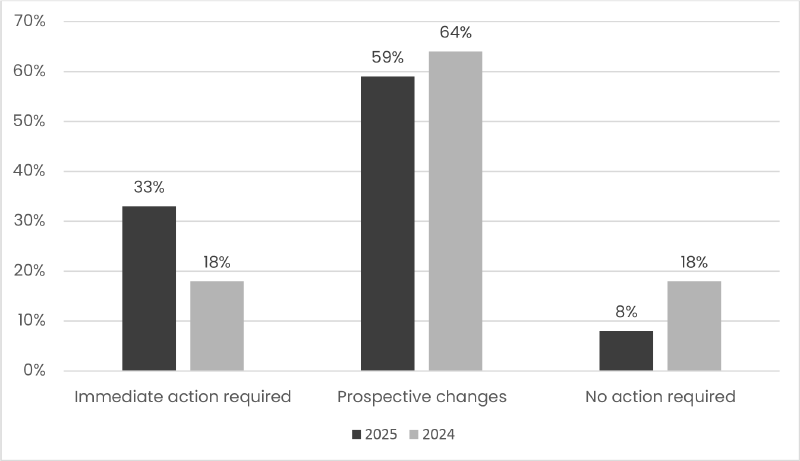

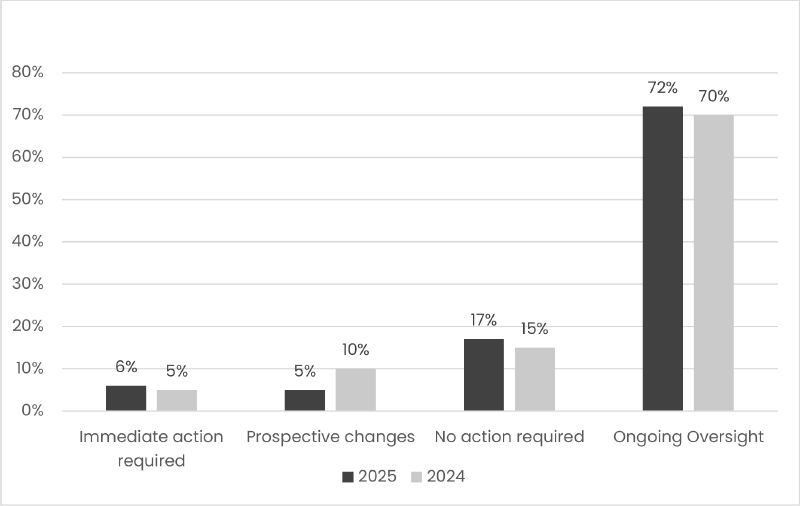

We track several categories of outcomes for the CDR Program:

• Immediate corrective action is required: includes the refiling of a previously filed CD document or the filing of a document that should have been previously filed, a referral to the Enforcement division of the OSC, or the issuance of a cease trade order (CTO).

• Prospective enhancements are required: includes changes or enhancements required to be incorporated in the next filing as a result of deficiencies identified.

• No action is required: instances where no corrective changes or additional filings are required.

• Ongoing Oversight: applies specifically to IORs and involves an initial high- level review of disclosure to determine whether direct engagement is required or to conclude that no further action is required. These reviews include ongoing monitoring of Reporting Issuers, high-level reviews of Technical Reports, and reviews triggered by significant industry developments. If we determine that direct engagement is required with the Reporting Issuer to address potentially significant disclosure deficiencies, a formal IOR file will be opened.

A CD review may result in more than one outcome. For example, a Reporting Issuer may be required to refile certain CD documents while also committing to prospective disclosure enhancements. Tracking these outcomes assists us in planning the CDR Program, including the re-evaluation of our existing risk-based selection criteria.

The outcomes on a year-over-year basis should not be interpreted as trends since the nature of the reviews, issues identified, and number of Reporting Issuers reviewed each year are generally different.

The following summarizes CD review outcomes for Fiscal 2025, and for the fiscal year ended March 31, 2024 (Fiscal 2024).{5}

The most common types of immediate action required from Reporting Issuers were amendments made to their CD record, including the following:

• refiling of financial statements to correct material misstatements;

• refiling of management's discussion and analysis (MD&A), where the form was materially deficient and did not meet the form requirements of Form 51- 102F1;

• refiling or filing (in instances when documents were not filed in the first place) of material contracts and material change reports;

• filing of executive compensation and corporate governance disclosure that was required to be filed at an earlier date; and

• refiling of a Technical Report where the report filed was not in compliance with NI 43-101.

Reporting Issuers that refile CD documents during our review are placed on the Refilings and Errors List found on our website.

This section highlights some of the common deficiencies and areas for improvement that were observed during our CD reviews in Fiscal 2025. It includes best practices and guidance to assist Reporting Issuers in meeting their regulatory obligations.

We direct readers to previously published Corporate Finance Annual Reports for further guidance, and in particular, the following topics from the Corporate Finance 2024 Annual Report:

• boilerplate discussion of operations (page 14);

• additional disclosure for Venture Issuers without revenue (page 17); and

• problematic promotional disclosures (page 18).

The rapidly evolving global political and economic environment is contributing to significant market uncertainty for Issuers. As a result, Issuers must continually assess the impacts of ongoing developments to determine whether their existing disclosure is sufficient. Issuers should provide timely, meaningful, transparent, and balanced

disclosures about related impacts and uncertainties to help investors make informed investment decisions.

Issuers should consider the broader impact of tariff policies when evaluating the impact of these policies on their business and operations, including disruption to supply-chains and access to raw materials and prices paid for such raw materials.

While this list is not exhaustive, disclosures that may be relevant to understanding the impact of the tariffs include:

• key risks to the Issuer;

• known and expected trends, demands, events or uncertainties related to tariffs that management reasonably believes will materially affect the Issuer's future revenue, expenses or projects;

• whether the Issuer has been impacted by counter tariffs imposed by the Canadian Federal government, or by other jurisdictions;

• operational changes and other measures taken by management in response to tariffs, including any plans to reallocate assets to another country, or divest of certain investments;

• the current and expected impact on the Issuer's operations and financial condition, including liquidity and capital resources; and

• other financial reporting considerations.

Reporting Issuers should also assess whether the impact of tariffs triggers the requirement to file a material change report. While Reporting Issuers may have provided detailed operational updates via news releases, we remind Reporting Issuers that such disclosure should also be included and updated in prospectuses and CD documents, such as MD&A and AIFs.

Depending on specific facts and circumstances, there could be numerous accounting implications across multiple areas such as going concern assessments, judgements and estimates, impairment of non-financial assets, etc. We remind Issuers that they must consider:

• all relevant events and information up to the authorisation date of the financial statements, particularly in relation to the going concern assessment; and

• as new information becomes available, whether their judgements and estimates need to be updated and reflected in their interim financial reports.

Forward-looking information (FLI) is an area of interest to many investors and can provide valuable insight about a Reporting Issuer's business and how it intends to attain its corporate objectives and targets.

Some Reporting Issuers present FLI that span multiple years, without providing reasonable and sufficient quantitative and qualitative assumptions to support the FLI. FLI should be limited to a time period that can be reasonably estimated, which generally will not go beyond the end of the Reporting Issuer's next fiscal year, unless supported by robust, specific, and verifiable assumptions.

However, in some industries (e.g., mining) longer term forecasts may be more common owing to more predictable quantitative forecast inputs. There may also be other scenarios where long-term FLI is relevant and supportable. Where long-term FLI is presented:

• all multi-year projections must be based on assumptions that are reasonable and supportable in the circumstances (not simply best estimates which cannot be supported); and

• the assumptions for financial projections must be specific and comprehensive, particularly with respect to quantitative details, such that an investor is able to clearly understand how each assumption was used to develop the FLI.

Where FLI is presented for multiple years without adequate support, staff may ask Issuers to limit the disclosure to cover a shorter period that can be more clearly supported (for example, one or two years, depending on facts and circumstances).

For more information on FLI, including multi-year FLI, please refer to the Corporate Finance 2022 Annual Report. Below is an example of disclosure that would not meet our expectations, followed by enhanced disclosure.

Disclosure Type |

Example |

|

|

Unsupported Long-Term FLI Disclosure |

During fiscal 20X5, we began construction of a second manufacturing facility. Facility construction will be completed in 2 years and will allow us to increase revenues by 50% in year 3, 60% in year 4 and 70% in year 5. |

|

|

Enhanced Disclosure |

During fiscal 20X5, we began construction of a second manufacturing facility. Facility construction will be completed in 2 years. The new facility will be approximately 100,000 square feet, which is approximately 50% of the square footage of our current facility. Given that manufacturing output is highly correlated to square footage available and given that our existing customers have already expressed interest in purchasing this increased throughput, we expect this will allow us to increase revenues by 50% in year 3. |

|

|

|

We also expect that new manufacturing processes will allow us to further enhance output levels on a per square foot basis, beginning in year 4, however the potential effectiveness of these new processes is not yet known, as they remain in development at this time. |

Pursuant to NI 52-110, audit committee members must not have a direct or indirect material relationship with the Reporting Issuer.{6} Similarly, section 1.2 of NI 58-101 prescribes that a director is "independent" if he or she would be independent within the meaning of section 1.4 of NI 52-110. A material relationship is defined as a relationship which could, in the view of the Reporting Issuer's board of directors, be reasonably expected to interfere with the exercise of a member's independent judgement. The purpose of the independence requirement is to support board members exercising independent judgment in performing their independent director or audit committee member duties.

What are the material relationships in NI 52-110?

NI 52-110 defines certain relationships as material relationships and thereby precludes some individuals from being considered independent. These material relationships are set out as bright line tests in sections 1.4 and 1.5 of NI 52-110, and they apply regardless of any determination of independence made by the board of directors. To be considered an independent director, an individual must not have a relationship captured by the bright line tests that are set out in section 1.4 of NI 52-110. To be considered an independent audit committee member, an individual must not have a relationship captured by the bright line tests that are set out in sections 1.4 and 1.5 of NI 52-110.

What are the bright line material relationship triggers in paragraphs 1.4(3)(a) and (f) of NI 52-110?

Staff have received inquiries as to whether, in certain fact patterns, subsection 1.4(7) of NI 52-110 provides for the non-application of the bright line test in subsection 1.4(3) of NI 52-110. Staff's position is that the material relationship triggers in subsection 1.4(3) of NI 52-110 are bright line tests, and once triggered, the bright line tests apply regardless. Below we consider the bright line material relationship triggers in paragraphs 1.4(3)(a) and (f) of NI 52-110.

Paragraphs 1.4(3)(a) and (f){7} respectively prescribe that an individual is considered to have a material relationship with the Reporting Issuer if such individual:

• is, or has been within the last three years, an employee or executive officer of the Reporting Issuer; or

• received more than $75,000 in direct compensation from the Reporting Issuer during any 12-month period within the last three years.

Guidance on subsections 1.4(3) and 1.4(7) of NI 52-110

Subsection 1.4(7){8} of NI 52-110 operates as a carve-out in certain limited factual circumstances to the bright line material relationship triggers in subsection 1.4(3) of NI 52-110. However, in circumstances where an individual also has a relationship captured by any of the bright line material relationship triggers contained in subsection 1.4(3) of NI 52-110, (as an example, the individual has previously acted as an interim CEO and received more than $75,000 in direct compensation for that interim role), this individual would not be considered independent for the purposes of NI 52-110 as the bright line tests apply regardless.

Subsection 1.4(7) of NI 52-110 prescribes that a material relationship is not imputed on an individual solely because the individual:

• has previously acted as an interim chief executive officer of the Reporting Issuer, or

• acts, or has previously acted, as a chair or vice-chair of the board of directors or of any board committee of the Reporting Issuer on a part-time basis.

If Issuers are unsure of a director's independence status, they should consult with their legal counsel.

"Trade" is defined broadly in the Act and includes "any act, advertisement, solicitation, conduct or negotiation directly or indirectly in furtherance of" a trade. While the definition of "trade" includes a carve-out for "a transfer, pledge or encumbrance of securities for the purpose of giving collateral for a debt made in good faith", a recent decision by the Capital Markets Tribunal (the Tribunal) that was subsequently affirmed by the Ontario Superior Court of Justice (Divisional Court) serves as an important reminder that this is a narrow exception and covers only the transfer, pledge, or encumbrance itself.

As noted by the Tribunal, "[the carve-out] does not apply to the different ways in which a pledgee may deal with the pledged securities. Nor does it apply to the issuance of debt itself. Each of those dealings is a separate transaction which must be tested to determine if it is, itself, a trade within the Act's definition."

We recommend that market participants seeking to rely on this carve-out to transfer, pledge or otherwise encumber securities of an Issuer that is subject to a CTO proceed with caution and, where appropriate, seek professional advice. While the specific transfer, pledge, or encumbrance of securities by the borrower to secure a bona fide debt may not be impacted by the CTO, such securities would remain subject to the CTO.

Where there is evidence to suggest that the transfer, pledge or encumbrance is made as part of a pre-arranged scheme and a trade related to the securities is expected, involvement in the conveyance may constitute acts in furtherance of a trade. Such acts may breach the CTO and may warrant compliance and/or enforcement action.

The determination of whether acts are in furtherance of a trade is a factual consideration examining the totality of conduct including, but not limited to, consideration of the surrounding circumstances, proximity of the acts to the potential trades, and the impact of the conduct. A strong indicator that actions further a trade is when benefits are directly or indirectly acquired as a result of the trade. There need not be a completed sale or disposition of a security for acts to be in furtherance of a trade; all that is required is acting for the purpose of doing so.

Reporting Issuers are reminded that entering into bankruptcy, insolvency, restructuring or receivership proceedings (collectively, the proceedings) does not relieve or exempt them from their securities filing requirements. If a Reporting Issuer is in default under securities laws, the principal regulator for the Reporting Issuer will generally issue a failure-to-file cease trade order (FFCTO) requiring all trading in the securities of the Reporting Issuer to cease. Where the OSC is the principal regulator for a Reporting Issuer, the proper forum to seek an exemption from securities filing requirements is the OSC.

When Reporting Issuers become the subject of a proceeding, they are generally expected to issue and file a news release disclosing the nature and circumstances of the proceeding. Reporting Issuers should also consider whether such proceedings trigger the timely disclosure requirement under section 75 of the Act.

We expect and encourage Reporting Issuers undergoing a proceeding to consider the regulatory implications of such proceeding in their court orders. For example, where a Reporting Issuer is subject to an FFCTO, any proposed sale, restructuring or other transaction arising out of a proceeding may require exemptive relief from the OSC to revoke or vary the FFCTO, even if the transaction is conducted under a court- supervised process. We encourage Reporting Issuers to seek legal advice from a qualified securities lawyer to determine whether specific provisions of their court order or other related relief sought within a proceeding is compliant with securities law requirements and any outstanding orders against the Reporting Issuer.

For further information on the regulatory implications for a Reporting Issuer undergoing a proceeding, refer to our website.

We continue to observe instances where Reporting Issuers do not file amended versions of a previously filed material contract. Pursuant to Companion Policy 51- 102CP, an amendment to a material contract or an amended material contract is treated as a "material contract" and must be filed on SEDAR+. The required timelines for filing material contracts are set out in NI 51-102 and summarized below.

Description |

Timeline for Filing |

|

|

If the Issuer is required to file an AIF |

|

|

|

A material contract for which a material change report is filed |

The material contract must be filed no later than the material change report |

|

|

All other material contracts |

Material contracts made or adopted before the date of the AIF must be filed no later than the time of filing the AIF |

|

|

If the Issuer is not required to file an AIF |

|

|

|

A material contract for which a material change report is filed |

The material contract must be filed no later than the material change report |

|

|

All other material contracts |

Material contracts must be filed within 120 days after the end of the financial year in which they were made or adopted |

Under Ontario securities law, to distribute securities, an Issuer must file and obtain a receipt for a prospectus or rely upon a prospectus exemption. A key component of our oversight of Issuers in Ontario's capital markets is the review of prospectuses in connection with public offerings. This section outlines data and trends with respect to public offerings and provides guidance on common issues that arise during our prospectus reviews.