Ontario Securities Commission Bulletin

Issue 48/44 - November 06, 2025

Ont. Sec. Bull. Issue 48/44

• Ontario Securities Commission and Radhakrishna Namburi

• Ontario Securities Commission et al.

• Ontario Securities Commission and Andre Itwaru

• Ontario Securities Commission et al.

• Ontario Securities Commission and Radhakrishna Namburi

• Adam Joseph Arquette and Arquette Insurance and Wealth Management -- ss. 127(1), 127(5.1)

• Ontario Securities Commission and Andre Itwaru -- Rules 14, 14.1 of CMT Rules of Procedure

• OSC Staff Notice 81-739 -- Investment Management Division Annual Summary Report

• OSC Staff Notice 11-737 (Revised) -- Securities Advisory Committee -- Vacancies

• Russell Investments Canada Limited

• True Exposure Investments, Inc.

• True Exposure Investments, Inc. and TRU.X Exogenous Risk Pool

• CIBC Asset Management Inc. and Conservative Income Portfolio

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Mount Logan Capital Inc. -- s. 21(b) of Ont. Reg. 398/21 of the OBCA

• Global Copper Corp. -- s. 21(b) of Ont. Reg. 398/21 of the OBCA

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Ontario Securities Commission et al. -- s. 127(8)

FILE NO.: 2025-28

BETWEEN:

Subsection 127(8) of the Securities Act, RSO 1990, c S.5

PROCEEDING TYPE: Application for Extension of Temporary Order

HEARING DATE AND TIME: November 10, 2025 at 10:00 a.m.

LOCATION: By videoconference

The purpose of this proceeding is to consider whether the Capital Markets Tribunal should grant the application filed by the Commission to extend the temporary order issued by the Commission on October 27, 2025.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT ATTEND, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

Dated at Toronto this 30th day of October, 2025.

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@capitalmarketstribunal.ca.

BETWEEN:

(For Extension of a Temporary Order Under Subsections 127(1) and 127(7) of the Securities Act, RSO 1990 c S.5)

The Applicant, the Ontario Securities Commission (the Commission), requests that the Capital Markets Tribunal (the Tribunal) make the following orders:

1. An Order extending the Temporary Order of the Commission dated October 27, 2024 (Temporary Order) made with respect to Adam Joseph Arquette (Arquette) and Arquette Insurance and Wealth Management (AIWM) for six months, until April 27, 2025, or for such other period as the Tribunal considers necessary if satisfactory information is not provided to the Tribunal within the fifteen-day period pursuant to s. 127(8) of the Securities Act, RSO 1990, c S.5 (the Act); and

2. Such other Order as the Tribunal considers appropriate in the public interest.

The grounds for the request are:

1. The Commission's Enforcement Division (Enforcement) is investigating Arquette and AIWM for possible breaches of Ontario securities law.

2. In the course of the investigation, Enforcement has found evidence that:

(a) Arquette is an Ontario resident, and the principal of AIWM, a company incorporated under the laws of Canada and resident in Ontario;

(b) Neither Arquette nor AIWM has ever been registered with the Commission in any capacity;

(c) Arquette and AIWM have been soliciting investments from third parties (Clients) to be managed and invested by Arquette and AWIM, in exchange for a fee of approximately 2.5% of the Clients' investment;

(d) Arquette and AIWM may have executed direct or indirect control of more than 300 Client investment accounts, belonging to more than 100 unique Clients;

(e) Arquette and AIWM may have co-mingled funds received from Clients with Arquette's personal funds, including funds deposited into Arquette's personal trading accounts;

(f) Arquette and AIWM may have obscured their conduct, including trading losses in Client investment accounts, by ensuring that brokerage statements were not sent directly to Clients, and misrepresenting the value of Client investment accounts and losses;

(g) Arquette and AIWM may be continuing to receive fees from Clients for trading in securities on behalf of the Clients;

(h) Arquette and AIWM may be continuing to solicit persons for the purpose of trading in securities on their behalf for a fee;

3. It therefore appears to the Commission that Arquette and AIWM may be :

(a) engaging or participating in an act, practice or course of conduct relating to securities that the person or company knows or reasonably ought to know perpetrates a fraud on any person or company, contrary to section 126.1(1)(b) of the Act;

(b) engaging in or holding themselves out as engaging in the business of trading in securities without being registered and without an applicable exemption from the registration requirements, contrary to section 25 of the Act; and

(c) engaging in or holding themselves out as engaging in the business of advising in securities without being registered and without an applicable exemption from the registration requirements, contrary to section 25 of the Act;

4. On October 27, 2025, the Commission issued the Temporary Order.

5. The Temporary Order provided that:

(a) pursuant to clause 2 of subsection 127(1), trading in any securities by Arquette, AIWM, or by any person on their behalf, including but not limited to any act, advertisement, solicitation, conduct, or negotiation, directly or indirectly in furtherance of a trade, shall cease;

(b) pursuant to clause 3 of subsection 127(1), any exemptions contained in Ontario securities law do not apply to Arquette or AIWM; and

(c) pursuant to subsection 127(6) of the Act, this order shall take effect immediately and shall expire on the 15th day after its making unless extended by order of the Capital Markets Tribunal.

6. The investigation into the conduct described in the Temporary Order and this Application is continuing, and the time required to conclude a hearing could be prejudicial to the public interest;

7. The Order sought by the Commission is necessary to protect investors from serious and ongoing harm and is in the public interest;

8. Subsections 127(1) and 127(8) of the Act; and

9. Such further grounds as counsel may advise and the Tribunal may permit.

The Applicant intends to rely on the following evidence at the hearing:

1. The Temporary Cease Trade Order of the Commission signed October 27, 2025;

2. Affidavit of Jody Sikora, to be filed;

3. Such further evidence as counsel may advise and the Tribunal may permit.

Date: October 29, 2025

ONTARIO SECURITIES COMMISSION |

|

|

|

Johanna Braden |

|

Senior Litigation Counsel |

|

Tel: (416) 263-3763 |

|

Email: jbraden@osc.gov.on.ca |

|

Ontario Securities Commission and Radhakrishna Namburi

FOR IMMEDIATE RELEASE

October 29, 2025

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated October 29, 2025, is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission et al.

FOR IMMEDIATE RELEASE

October 30, 2025

TORONTO -- The Tribunal issued a Notice of Hearing on October 30, 2025 setting the matter down to be heard on November 10, 2025 at 10:00 a.m. to consider whether the Capital Markets Tribunal should grant the application filed by the Commission to extend the temporary order issued by the Commission on October 27, 2025.

A copy of the Notice of Hearing dated October 30, 2025, Application dated October 29, 2025 and Temporary Order dated October 27, 2025 are available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission and Andre Itwaru

FOR IMMEDIATE RELEASE

October 30, 2025

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated October 30, 2025 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission et al.

FOR IMMEDIATE RELEASE

October 31, 2025

TORONTO -- A case management hearing in the above-named matter is scheduled to be heard on November 6, 2025 at 9:00 a.m. by videoconference.

Members of the public may observe the hearing by videoconference, by selecting the "View by Zoom" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

November 4, 2025

TORONTO -- The Tribunal issued its Reasons for Decision in the above-named matter.

A copy of the Reasons for Decision dated November 3, 2025 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission and Benjamin Ward

FOR IMMEDIATE RELEASE

November 4, 2025

TORONTO -- A case management hearing in the above-named matter is scheduled to be heard on November 14, 2025, at 10:00 a.m. by videoconference.

Members of the public may observe the hearing by videoconference, by selecting the "View by Zoom" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission and Nayeem Alli

FOR IMMEDIATE RELEASE

November 4, 2025

TORONTO -- A case management hearing in the above-named matter is scheduled to be heard on November 18, 2025, at 10:00 a.m. by videoconference.

Members of the public may observe the hearing by videoconference, by selecting the "View by Zoom" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Ontario Securities Commission and Radhakrishna Namburi

BETWEEN:

File No. 2025-24

Adjudicator: |

Dale Ponder |

October 29, 2025

WHEREAS on October 29, 2025, the Capital Markets Tribunal held a hearing by videoconference;

ON READING the materials filed by the Ontario Securities Commission, and on hearing the submissions of the representative for the Commission, no one attending for the respondent, although properly served;

IT IS ORDERED THAT:

1. pursuant to rule 3 and subrule 14.1(1) of the Rules of Procedure (the Rules), the merits hearing and the sanctions and costs hearing in this proceeding shall be heard together;

2. pursuant to subrule 9(6) of the Rules, this proceeding shall be conducted in writing;

3. by 4:30 PM on December 4, 2025, the Commission shall serve and file its affidavit evidence, and written submissions on the merits, sanctions and costs;

4. by 4:30 PM on January 15, 2026, the respondent shall serve and file any affidavit evidence and written submissions on the merits, sanctions and costs; and

5. if applicable, by 4:30 PM on January 29, 2026, the Commission shall serve and file any reply affidavit evidence and any reply submissions on merits, sanctions and costs.

Adam Joseph Arquette and Arquette Insurance and Wealth Management -- ss. 127(1), 127(5.1)

(Subsections 127(1) and 127(5.1))

WHEREAS:

1. It appears to the Ontario Securities Commission (the Commission) that:

a. Adam Joseph Arquette (Arquette), an Ontario resident, is the principal of Arquette Insurance and Wealth Management (AIWM), a company incorporated under the laws of Canada and resident in Ontario; Neither Arquette nor AIWM has ever been registered with the Commission in any capacity;

b. Arquette and AIWM have been soliciting investments from third parties (Clients) to be managed and invested by Arquette and AWIM, in exchange for a fee of approximately 2.5% of the Clients' investment;

c. Arquette and AIWM may have executed direct or indirect control of more than 300 Client investment accounts, belonging to more than 100 unique Clients;

d. Arquette and AIWM may have co-mingled funds received from Clients with Arquette's personal funds, including funds deposited into Arquette's personal trading accounts;

e. Arquette and AIWM may have obscured their conduct, including trading losses in Client investment accounts, by ensuring that brokerage statements were not sent directly to Clients, and misrepresenting the value of Client investment accounts and losses;

f. Arquette and AIWM may be continuing to receive fees from Clients for trading in securities on behalf of the Clients;

g. Arquette and AIWM may be continuing to solicit persons for the purpose of trading in securities on their behalf for a fee;

h. Arquette and AIWM may have breached Ontario securities law and acted contrary to the public interest, including by:

i. engaging or participating in an act, practice or course of conduct relating to securities that the person or company knows or reasonably ought to know perpetrates a fraud on any person or company, contrary to section 126.1(1)(b) of the Securities Act, R.S.O. 1990, c. S.5, as amended (the Act);

ii. engaging in or holding themselves out as engaging in the business of trading in securities without being registered and without an applicable exemption from the registration requirements, contrary to section 25 of the Act; and

iii. engaging in or holding themselves out as engaging in the business of advising in securities without being registered and without an applicable exemption from the registration requirements, contrary to section 25 of the Act;

2. The Commission is conducting an investigation into the conduct described above;

3. The Commission is of the opinion that the time required to conclude a hearing could be prejudicial to the public interest; and

4. The Commission is of the opinion that it is in the public interest to make this Order.

IT IS ORDERED pursuant to section 127 of the Act that:

1. pursuant to clause 2 of subsection 127(1), trading in any securities by Arquette, AIWM, or by any person on their behalf, including but not limited to any act, advertisement, solicitation, conduct, or negotiation, directly or indirectly in furtherance of a trade, shall cease;

2. pursuant to clause 3 of subsection 127(1), any exemptions contained in Ontario securities law do not apply to Arquette or AIWM; and

3. pursuant to subsection 127(6) of the Act, this order shall take effect immediately and shall expire on the 15th day after its making unless extended by order of the Capital Markets Tribunal.

DATED at Toronto, this 27th day of October 2025.

Ontario Securities Commission and Andre Itwaru -- Rules 14, 14.1 of CMT Rules of Procedure

BETWEEN:

File No. 2025-22

Adjudicators: |

Jane Waechter |

October 30, 2025

(Rules 14 and 14.1 of the Capital Markets Tribunal Rules of Procedure)

WHEREAS on October 30, 2025, the Capital Markets Tribunal held a hearing by videoconference;

ON READING the materials filed by the Ontario Securities Commission, and on hearing the submissions of the representative for the Commission and Andre Itwaru for himself, and on being advised that all parties consent;

IT IS ORDERED THAT:

1. pursuant to rule 3 and subrule 14.1(1) of the Rules of Procedure the merits hearing and the sanctions and costs hearing in this proceeding shall be heard together;

2. by 4:30 PM on December 8, 2025, the Commission shall serve and file any affidavit evidence or witness summary, and written submissions on the merits, sanctions and costs;

3. by 4:30 p.m. on January 19, 2026, the respondent shall serve and file any affidavit evidence or witness summary, and written submissions on the merits, sanctions and costs;

4. if applicable, by 4:30 PM on February 2, 2026, the Commission shall serve and file any reply affidavit evidence and any reply submissions on merits, sanctions and costs; and

5. the hearing on the merits, sanctions and costs shall take place on March 26, 2026, at 10:00 AM, by videoconference, or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Harry Stinson et al. -- s. 144.1

Citation: Stinson v Ontario Securities Commission, 2025 ONCMT 14

Date: 2025-11-03

File No. 2025-13

BETWEEN:

(Section 144.1 of the Securities Act, RSO 1990, c S.5)

Adjudicators: |

Russell Juriansz (chair of the panel) |

|

Jane Waechter |

||

M. Cecilia Williams |

||

|

||

Hearing: |

In-person, October 21, 2025 |

|

|

||

Appearances: |

Kirsten Thoreson |

For the Ontario Securities Commission |

|

||

Richard A. Wellenreiter |

For Harry Stinson and Buffalo Grand Hotel |

|

|

||

No one appearing on behalf of Stinson Hospitality Management Inc., Stinson Hospitality Corp., Restoration Funding Corporation, Buffalo Central LLC, and Stephen Kelley |

||

|

||

Simon Parry |

For himself, as intervenor |

|

|

||

Henry Wemekamp |

For himself, as intervenor |

|

[1] Harry Stinson and Buffalo Grand Hotel Inc. (together, the Applicants) applied to vary an enforcement order made against them on December 15, 2023.{1} They asked the Tribunal to remove the following financial sanctions (the Financial Sanctions) that were ordered jointly and severally against them:

a. a disgorgement order for approximately $13.5 million;

b. a $600,000 administrative penalty; and

c. a $166,000 cost award.

[2] The Applicants presented a financing plan to renovate and refurbish the Buffalo Grand Hotel (the Hotel), which has been closed since December 30, 2021, after a fire caused extensive damage. The Applicants submitted that this financing plan is the only way that investors in the Hotel will recover any of their investments and that the Financial Sanctions are the only thing standing in the way of the financing plan. The Applicants presented a draft order that would reinstate the Financial Sanctions if several ongoing conditions were not satisfied relating to the financing.

[3] In its sanctions decision, the Tribunal stated:

We are sympathetic to the idea of investors obtaining redress through the sale of the assets. However, there is insufficient evidence in this case that such an outcome is on the horizon...{2}

[4] We came to the same conclusion about the Applicants' financing proposal. There was insufficient evidence that it was a real option for investor recovery. Moreover, the Applicants failed to meet the statutory requirement to show, on a balance of probabilities, that removing the Financial Sanctions would not be prejudicial to the public interest.

[5] On October 21, 2025, we dismissed the application, with reasons to follow.{3}

[6] In June 2023, the Tribunal found that the Applicants breached the Securities Act{4} by conducting an illegal distribution of securities and by breaching a cease trade order. The Tribunal ordered various sanctions against them on December 15, 2023, including the Financial Sanctions.

[7] By Notice of Application dated August 20, 2025, the Applicants applied to vary the Financial Sanctions on the ground that that the Financial Sanctions prevent the Applicants from getting financing to repair and reopen the Hotel. The Applicants said that this, in turn, prevents investors from recovering their investments in the Hotel.

[8] The Applicants submitted evidence including:

a. a Term Sheet dated May 23, 2025, from a lender which, if carried through to a binding lending agreement, would result in approximately US$19 million in funding;

b. an "as is" appraisal for the Hotel of US$3 million;

c. an "as complete" appraisal for the Hotel of US$31.7 million in 2028 and US$36.6 million in 2029, based on what it termed the "extraordinary assumption" that US$27 million will be spent to renovate, remediate and rebrand the Hotel;

d. a signed Franchise Agreement with a major hotel chain;

e. a Subordination Agreement between the Applicants and two trustees for the investors; and

f. an Investor Security Agreement.

[9] The Applicants also submitted evidence intended to demonstrate their impecuniosity.

[10] We permitted a redacted version of the exhibits to Stinson's September 16, 2025, affidavit to be filed and available to the public to protect the identity and personal information of individual investors and sensitive commercial information.

3.1 Intervenors

[11] Shortly before the commencement of the hearing, Simon Parry and Henry Wemekamp each applied to intervene in this application. They are trustees representing investors comprising 84 percent of the capital invested. They attended the hearing in person. They did not satisfy the procedural and substantive requirements to intervene and we were skeptical about whether they would make a unique contribution to our understanding of the issues. However, we exercised our discretion to permit Mr. Parry and Mr. Wemekamp to address the Tribunal for five minutes because of the unique nature of this variation request, the perspective they might bring as trustees for the investors, and because the parties consented. They offered some context and stated that approximately 80% of the investors were in favour of the Applicants' plan.

[12] Subsection 144.1(1) of the Act grants the Tribunal authority to vary its orders if satisfied that doing so would not be prejudicial to the public interest.

[13] The Tribunal's authority under s. 144.1 is an extraordinary remedy to be used only in the "rarest of circumstances."{5}The Tribunal has previously exercised its discretion to vary orders when:

a. new and material facts came to light after the initial order, or there were changes in the material circumstances underlying the order, including where terms of the initial order were duplicative or no longer necessary;{6}

b. the prior order was later found to be manifestly unfair to the respondent;{7} and

c. the Commission supported and consented to the requested relief.{8}

[14] In addition, the Tribunal has held that relief may be warranted where there has been a misrepresentation, where material facts were not disclosed during the original hearing, where new and previously undiscoverable facts came to light after the original hearing, where legislative changes made it appropriate to revisit the original decision, or where a binding authority was not brought to the attention of the Tribunal.{9}

[15] We focused our analysis on whether there were changes in the material circumstances underlying the Financial Sanctions, including whether the terms of the initial order are no longer necessary. None of the other circumstances that might justify revisiting an order were present in this application.

[16] The Applicants have the onus of proving on a balance of probabilities that the variation sought is justified and not prejudicial to the public interest.{10}

4.1 Material Change in Circumstances

[17] The Applicants submitted that circumstances have materially changed since the Tribunal imposed the Financial Sanctions in December 2023. The purported material change is that they now have a viable plan that would permit investors to recover their investments if the Financial Sanctions were removed.

[18] We were not persuaded. The evidence the Applicants filed was incomplete and largely speculative. They failed to provide sufficient specific and definitive information to meet their onus of proof. Their evidence indicated that a great deal of uncertainty remains. In particular:

a. The Term Sheet from the lender expired on May 23, 2025, and the Applicants did not provide a signed extension from the lender. Email evidence from the financial broker in March 2025, which could pertain to the same lender, said that "We do not have long to clear this issue as our current lender has us on a time frame in order to solve this with the OSC before our terms become void..."{11} This created uncertainty about whether the Term Sheet, which is not a binding loan commitment, will evolve into one.

b. The Term Sheet states: "There is currently an open matter with the Ontario Securities Commission which will be fully resolved prior to closing."{12} The Applicants submitted that this refers to this variation application, although this application was not an open matter when the Term Sheet was completed. We also did not know what "fully resolved" meant. This created uncertainty about the lender's requirements.

c. The financial broker wrote to the Applicants in March 2025 that:

It is imperative that we clear any clouds pertaining to the Ontario Securities Commission and any judgements against the Buffalo Grand Hotel and yourself for a lender to close on a loan to fund the re-opening of the hotel and convention center.{13}

There are US$3.5 million in liens and judgments registered against the Hotel. The Applicants said these amounts would be paid from the proceeds of the US$19 million loan (which was originally proposed to be a US$22 million in Term Sheet but was revised to US$19 million after a property appraisal was obtained). The documentation, however, did not clarify whether the lender would require the other judgments to be satisfied before advancing the loan. The March 2025 email from the broker suggested that prepayment may be required. This created further uncertainty about the lender's requirements and whether they can be satisfied by the Applicants.

d. The Term Sheet contemplated personal guarantees from Stinson and any investors holding more than a 10 percent interest in the Hotel. No investors hold more than 10 percent and, therefore, the only guarantor would be Stinson. In our view, a guarantee from Stinson would not be valuable to a lender, since the evidence filed showed that he is impecunious. This created uncertainty about whether the lender will proceed to a binding commitment when there are no guarantors.

e. The "as complete" appraisal for the Hotel relied on representations from management including the "extraordinary assumption" that US$27 million will be spent to remediate, renovate, rebrand and reposition the Hotel. The appraiser explained that if this assumption proves false, it would directly impact their value conclusions. We had no basis to regard the appraiser's "extraordinary assumption" to be reasonable. We note there was no evidence to show how the additional US$11.5 million contemplated by the appraisal would be raised (over and above the US$19 million covered by the Term Sheet and the US$3.5 million in judgments to be paid from the financing rather than spent on renovation).

f. The signed Franchise Agreement for the Hotel provided that renovations must begin no later than 30 days after the effective date of June 30, 2025. There was no evidence that renovations had begun; on the contrary, the Applicants' whole point was that the renovations could not begin until the Financial Sanctions are removed and the financing completed. This created uncertainty about whether the franchisor would be bound by the Franchise Agreement.

g. The City of Buffalo placed a certificate of abandonment on the property on June 19, 2025, and has threatened proceedings against the Hotel to seize it. There was no evidence that the City of Buffalo gave any assurance that it will change its position if the Financial Sanctions are removed. This created uncertainty as to whether the Hotel will be available to renovate and refurbish.

[19] There was also some evidence that weighs against the Financial Sanctions being an impediment to financing:

a. the Applicants said that the Franchise Agreement was contingent on the Financial Sanctions being lifted but we did not see that in any document or from the Franchisor; and

b. the OSC has not registered the order containing the Financial Sanctions against the Hotel and, as such, it is not a registered lien that directly impedes financing of the Hotel.

[20] In addition, there was no evidence about:

a. whether any further steps contemplated by the Term Sheet have been taken, other than payment of a due diligence deposit of $100,000; and

b. the substance of any communications between the Applicants and the proposed lender after July 7, 2025.

[21] The Applicants submitted that the Financial Sanctions are the primary remaining obstacle to developing the Hotel. We saw many more obstacles than the Financial Sanctions, as described above. Furthermore, the evidence did not suggest to us that the Financial Sanctions are no longer necessary. As such, we found that the Applicants have not demonstrated that a material change in circumstances has occurred to support varying the Financial Sanctions.

4.2 The Public Interest

[22] The Commission identified three precedent cases where an applicant sought to vary sanctions orders after contested sanctions and costs hearings, Freisen (Re),{14}Bergen (Re){15} and Spaetgens (Re),{16} and submitted that a common thread in these authorities is the requirement for substantial and satisfactory evidence, with adequate, specific and verifiable supporting information. For the purpose of our analysis, we focused on Spaetgens. Freisen and Bergen were less applicable to this case because they involved the need for current, corroborating evidence of character for individuals asking to be reinstated in a regulated industry.

[23] In Spaetgens (Re),{17} the Alberta Securities Commission refused to grant the requested order because the variation application was speculative, premature and unsupported by sufficient detail to permit any assessment of whether it would be prejudicial to the public interest to grant relief.

[24] Like in Spaetgens, the evidence filed by the Applicants was speculative, premature and unsupported by sufficient detail to permit an assessment of the public interest. We explained above that there are too many uncertainties, and we found that the evidence fell well short of "substantial and satisfactory."

[25] We would expect to, but did not, see evidence on the following topics relevant to the public interest:

a. whether the Applicants made any effort to pay the Financial Sanctions;

b. what was done with the funds initially raised from investors; and

c. whether other potentially viable options have been pursued, as the Commission referred to a few potentially viable options, including obtaining a forbearance agreement from the Commission on terms acceptable to the Commission, or obtaining a receivership order.

[26] In summary, other than a weakly supported assertion that their financing plan was the only viable option available to investors, the Applicants did not provide essential evidence to support a conclusion that removing the Financial Sanctions would not be prejudicial to the public interest.

[27] In addition, we were mindful of two of the important factors that assist the Tribunal in determining the appropriate sanctions in any case: specific and general deterrence. The order Stinson seeks to vary stems from the second instance where he has breached Ontario securities law. In the sanctions and costs decision in this matter, the Tribunal commented on Stinson's "failure to appreciate the importance of complying with Ontario securities law, especially in light of Stinson's previous settlement in 2006" with the Commission.{18} Exercising our discretion to grant the requested variation on the basis of such incomplete and speculative evidence would, in our view, undermine the specific deterrence intended by the Tribunal's sanctions order.

[28] We were also concerned that to grant the variation in this instance would send a message to like-minded individuals that financial sanctions from the Tribunal may be avoided on speculative, premature or unsupported evidence, thereby undermining the general deterrent effect of Tribunal sanctions decisions.

[29] While we understood and were sympathetic to the plight of the investors, we made two observations.

[30] First, the Tribunal's sanctions are protective and preventative, not compensatory. They have the purpose of protecting all investors by maintaining public confidence in the capital markets. The Tribunal has no jurisdiction to redress harm caused to private investors by making orders for restitution. The Tribunal's order of disgorgement is not the same as damages and is not intended to compensate individual investors.{19}

[31] Second, we did not accept the investors had no alternative but to rely on the Applicants to manage the refinancing, renovating and reopening the Hotel to attempt to recoup their investments as there was no evidence of any other options having been explored, as suggested by the Commission.

[32] For the above reasons, we found that the Applicants had not met their burden of demonstrating, on a balance of probabilities, that removing the Financial Sanctions was justified and would not be prejudicial to the public interest and we dismissed their application.

Dated at Toronto this 3rd day of November, 2025.

{1} Stinson (Re), 2023 ONCMT 50 (Stinson)

{2} Stinson at para 73

{3} (2025), 48 OSCB 8754

{4} RSO 1990, c S.5 (Act)

{5} X Inc. (Re), 2010 ONSEC 26 at para 35

{6} Cheng (Re), 2019 ONSEC 35; Macquarie Capital Markets Canada Ltd (Re), 2018 ONSEC 12 at paras 11-14; Friesen (Re), (1999) 22 OSCB 2427 (Friesen)

{7} AiT Advanced Information Technologies Corporation (Re), 2008 ONSEC 23

{8} Katanga Mining Limited (Re), 2021 ONSEC 11 at paras 5-9

{9} Pro-Financial Asset Management Inc (Re), 2017 ONSEC 39 at para 16

{10} Rankin (Re), 2011 ONSEC 32 at para 84, aff'd 2023 ONSC 112 (Div Ct)

{11} Exhibit 4, Email from Luke Thompson to Harry Stinson, dated March 23, 2025, Exhibit I to the Affidavit of Harry Stinson, sworn on October 7, 2025 (Thompson Email March 23, 2025)

{12} Exhibit 3, Lender Term Sheet, dated May 23, 2025 at p 3, Exhibit N to the Affidavit of Harry Stinson, sworn on September 16, 2025

{13} Exhibit 4, Thompson Email March 23, 2025

{14} Friesen (Re) (1999), 22 OSCB 2427

{15} 2021 CanLII 142789 (SK FCAA)

{16} 2017 ABASC 163

{17} 2017 ABASC 163

{18} Stinson at para 48

{19} Cartaway Resources Corp (Re), 2004 SCC 26 at paras 58-62, citing Committee for the Equal Treatment of Asbestos Minority Shareholders v Ontario (Securities Commission), 2001 SCC 37 at paras 41-45

OSC Staff Notice 81-739 -- Investment Management Division Annual Summary Report

OSC Staff Notice 81-739 Investment Management Division Annual Summary Report is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

November 5, 2025

Contents

Senior Vice President's Message |

5 |

|||

Introduction |

7 |

|||

|

Responsibilities and structure of the IM division |

7 |

||

|

Types of investment funds |

10 |

||

|

Investment funds market landscape |

12 |

||

|

|

Investment fund population |

13 |

|

Part A: Operational highlights |

14 |

|||

|

I. |

Prospectus filings |

14 |

|

|

Pre-filing process for novel products |

15 |

||

|

Late changes to final prospectus document |

15 |

||

|

Data on prospectus reviews |

15 |

||

|

Noteworthy prospectus filings or trends |

17 |

||

|

|

Collateralized loan obligation ETFs |

17 |

|

|

|

Solana crypto funds |

18 |

|

|

|

High interest savings account (HISA) ETFs |

18 |

|

|

II. |

Exemptive relief applications |

19 |

|

|

Data on exemptive relief applications |

19 |

||

|

Noteworthy exemptive relief applications or trends |

20 |

||

|

|

Relief to borrow up to 10% of NAV on a short-term basis to facilitate purchases and redemptions on a T+1 settlement cycle |

20 |

|

|

|

Financial statements filing and delivery requirements for pooled funds |

21 |

|

|

|

Related party debt relief |

21 |

|

|

|

Lapse date extensions |

22 |

|

|

|

Underlying fund relief |

22 |

|

|

|

Bulk transfer applications |

23 |

|

|

III. |

Continuous disclosure reviews |

24 |

|

|

Summary of completed reviews |

24 |

||

|

Artificial intelligence washing |

24 |

||

|

Small issuer review |

25 |

||

|

Outlier analysis of investment fund survey data |

25 |

||

|

Fund risk rating |

26 |

||

|

Sales communications |

27 |

||

|

Monitoring of crypto asset funds |

28 |

||

|

Standard continuous disclosure reviews |

29 |

||

|

IV. |

Section 11.9 and 11.10 notices |

29 |

|

Part B: Regulatory policy |

31 |

|||

|

Completed policy initiatives |

31 |

||

|

|

Investment fund settlement cycle |

31 |

|

|

|

Modernization of the prospectus filing model for investment funds |

31 |

|

|

|

OSC Rule 81-510 Dealer Rebates of Trailing Commissions |

32 |

|

|

Ongoing policy initiatives |

33 |

||

|

|

Access based model for investment fund reporting issuers |

33 |

|

|

|

Modernization of continuous disclosure documents |

33 |

|

|

|

Review of principal distributor practices |

34 |

|

|

|

Use of chargeback model |

34 |

|

|

|

Investment funds investing in crypto assets |

35 |

|

|

|

Review of exchange traded funds |

35 |

|

Part C: Emerging issues and initiatives |

36 |

|||

|

Retail investor access to long-term assets through investment fund product structures |

36 |

||

|

Use of AI systems in capital markets |

36 |

||

|

Foreign issuer reports of exempt distribution |

38 |

||

|

Investment fund survey |

38 |

||

|

Financial sector assessment program |

39 |

||

Part D: Stakeholder outreach and resources |

40 |

|||

|

Landing page on OSC website |

40 |

||

|

Investment management brief |

40 |

||

|

SEDAR+ resources |

41 |

||

|

Publication of staff notices |

41 |

||

|

|

OSC Staff Notice 81-735 Cash Collateral Use for Delayed Basket Securities in ETF Subscriptions |

41 |

|

|

|

CSA Staff Notice 81-338 Guidance on the Use of Discretion Under the CSA Investment Risk Classification Methodology |

41 |

|

|

Investment Funds Technical Advisory Committee |

42 |

||

Appendix A -- Glossary and description of rules |

43 |

|||

I am pleased to share this annual Summary Report (Report) which provides an overview of the activities of the newly formed Investment Management division (IM division) for the fiscal year ended March 31, 2025 (Fiscal 2025).

Effective April 1, 2024, the Ontario Securities Commission (OSC) implemented changes to streamline its organizational structure to better deliver our six-year Strategic Plan and enable us to be responsive to market trends while continuing to provide balanced, flexible and responsive regulation. The scope of the IM division (previously the Investment Funds and Structured Products Branch) was broadened to include regulatory policy matters related to investment fund managers (IFMs) and portfolio advisers. This Report reflects the first operational year of the IM division, and I am proud of our efforts to move forward in a seamless manner.

Operationally, our Product Offerings team continued to improve efficiency by streamlining work processes and focusing on high-impact issues. These efforts helped to enhance the way we perform our regulatory functions. The Risk and Analytics team remained proactive in identifying emerging risks. Their outlier analysis using data from the Investment Fund Survey (IFS) has been especially useful in flagging unusual activities that may require further review.

On the policy side, the Regulatory Policy team undertook several key initiatives this year, with a strong emphasis on engaging stakeholders. We recognize the importance of thoughtful planning and careful consideration before publishing any proposed rules for public comment. Our newly formed Portfolio Advisers team brought valuable expertise in the regulation of IFMs and portfolio advisers. Their in- depth knowledge is instrumental in helping the IM division adapt our regulatory approach to reflect the evolving services offered by registrants.

Moving forward, we know the industry will continue to face changes and challenges that impact both investors and firms. We are committed to working closely with stakeholders and interested parties to ensure the IM division remains responsive and agile, to enhance the investor experience while keeping regulation aligned with shifting risks, needs and practices in Ontario and globally.

We hope this Report provides insight into our work and is useful to stakeholders. We welcome any questions or comments.

This Report provides an overview of the key operational and policy initiatives of the IM division that impact investment fund issuers and advisers during Fiscal 2025.

The Report can be used as a resource for IFMs and advisers, entities who perform services on their behalf and other stakeholders, including investors.

The Report is organized into four key areas:

Part A -- Operational highlights

• Summarizes our key activities, including

• prospectus reviews

• applications for exemptive relief,

• continuous disclosure reviews, and

• review notices relating to proposed ownership changes in, or asset acquisitions of, registered firms.

Part B -- Regulatory policy initiatives

• Identifies ongoing policy initiatives affecting investment funds and portfolio advisers with detail on their status.

Part C -- Emerging issues and initiatives

• Summarizes recent or upcoming changes in the industry that affect investment funds and portfolio advisers.

Part D -- Stakeholder outreach and resources

• Provides detail on our outreach initiatives and resources for issuers of investment funds and other stakeholders.

The OSC's mandate is to provide protection to investors from unfair, improper or fraudulent practices, to foster fair, efficient and competitive capital markets and confidence in the capital markets, to foster capital formation, and to contribute to the stability of the financial system and the reduction of systemic risk.

In May 2024, the OSC released its Strategic Plan detailing how it will approach its work over the next six years. The plan outlines six strategic goals aimed at making Ontario's capital markets inviting, thriving and secure, while aligning with the OSC's modernization efforts and supporting our mandate.

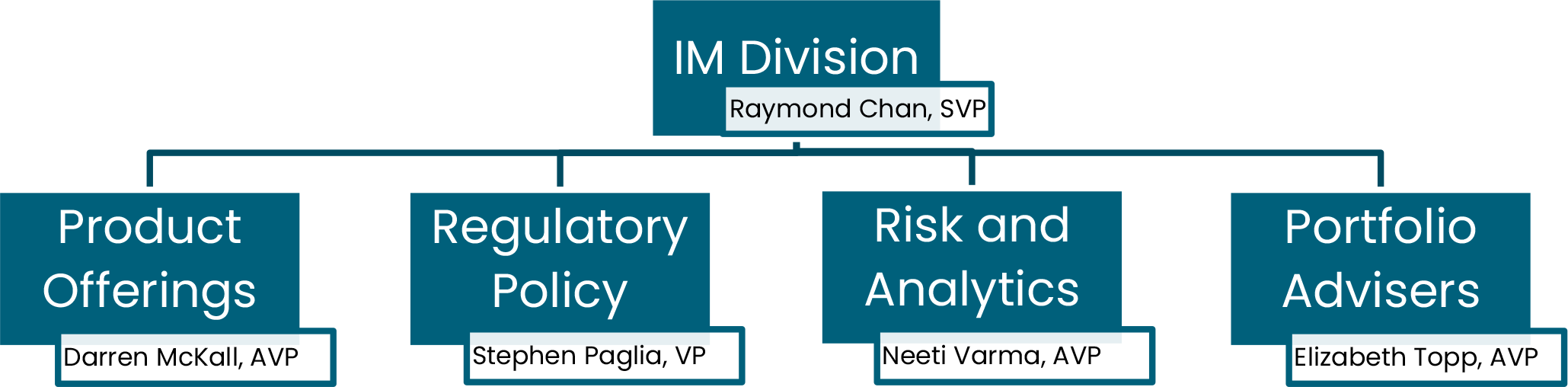

In support of the OSC's mandate and strategic plan, the IM division is responsible for administering the regulatory framework for investment funds, IFMs and portfolio management services that are offered to Ontario investors. The IM division is comprised of four teams, each with its own dedicated staff and key responsibilities.

Product Offerings Team

[x] reviews and assesses disclosure for all types of publicly offered investment funds, including prospectus filings and amendments,

[x] considers applications for discretionary relief from securities legislation, and

[x] engages with the Canadian Securities Administrators (CSA) on issues raised related to novel filings.

Regulatory Policy Team

[x] responsible for policy initiatives affecting investment funds and often collaborates with CSA counterparts to work on rule proposals and amendments aimed at adapting to changes in the capital markets,

[x] monitors, reviews and assesses regulatory proposals and product developments in Canada and abroad to determine possible impacts on our regulatory regime, and

[x] monitors and participates in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO), and other financial regulators.

Risk and Analytics Team

[x] monitors the investment funds industry using risk and data analytics, using tools such as our continuous disclosure reviews, the IFS, and other resources,

[x] monitors and responds to emerging capital markets and investor protection risks more effectively, using a risk-based approach, and

[x] shares data with CSA and international regulators for systemic risk monitoring purposes.

Portfolio Advisers Team

[x] responsible for oversight of policy and operational matters, such as exemptive relief applications, relating to IFMs and portfolio management,

[x] reviews notices of proposed ownership changes in, or asset acquisitions of, registered firms, and

[x] liaises with the Registration, Inspection and Examination division (RIE) on novel and complex registration issues related to IFMs, portfolio management and advice.

In addition, staff across all teams in the IM division regularly

[x] engage with industry participants, including on advisory committees and consultation papers, and

[x] communicate our expectations on process or policy matters with stakeholders through regulatory updates in the Investment Management Brief (formerly known as eNews articles) and provide guidance in staff notices.

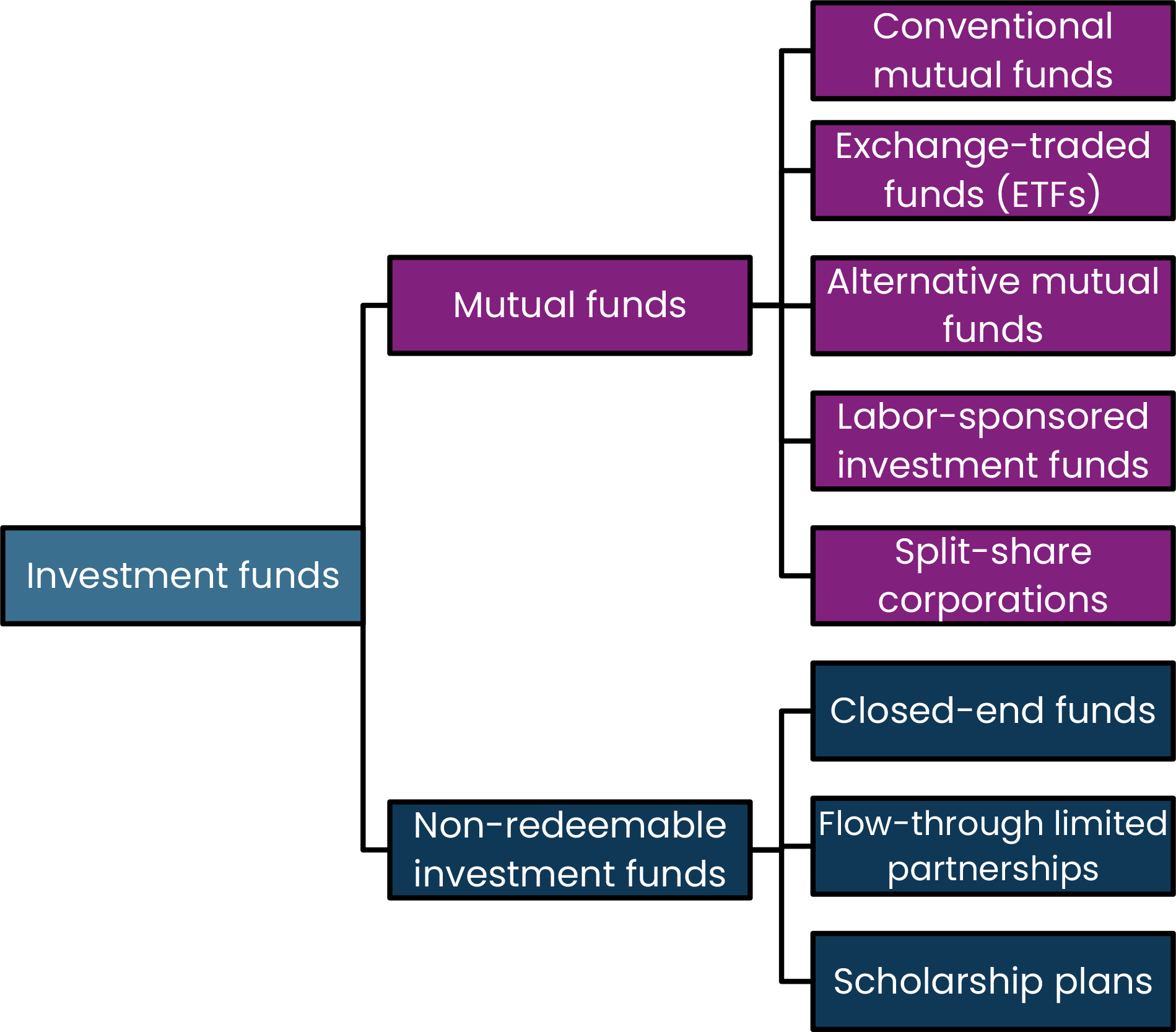

Guidance on whether an issuer is an investment fund was provided in the 2023 Report. Publicly offered investment fund assets in Canada are comprised broadly of mutual funds and non-redeemable investment funds:

Refer to Appendix A for a glossary and description of the rules that the IM division considers as part of its oversight of investment funds, IFMs and firms and individuals who are in the business of advising on securities in Ontario.

Canada's public investment funds have shown a slight growth since the prior year based on assets under management (AUM){1}:

Investment fund products |

AUM as of March 31, 2024 |

AUM as of March 31, 2025 |

% of Investment fund AUM as of March 31, 2025 |

|

|||

Conventional mutual funds |

$2.1 trillion |

$2.3 trillion |

79% |

|

|||

ETFs |

$417.1 billion |

$546.9 billion |

19% |

|

|||

Closed-end funds |

$41.6 billion |

$48.7 billion |

2% |

|

|||

TOTAL |

$2.6 trillion |

$2.9 trillion |

|

While conventional mutual funds still make up the bulk of the total investment fund AUM, ETF assets continue to grow at a faster rate than other investment fund products. Since the prior year, ETFs experienced the highest rate of growth in AUM (31%), as compared to conventional mutual funds (10%) and closed end funds (17%) and the value of ETF assets has almost doubled since fiscal 2021. The market share of ETFs also rose slightly to 19% from 16% in the prior year, with the shift coming entirely from conventional mutual funds which are at 79% as compared to 82% in the prior year. ETFs' continued popularity was evident with $95 billion of positive net sales during the period, which exceeds the combined total from the previous two periods. After two years of net redemptions, there were also positive net sales of $26 billion for conventional mutual funds during the period.

Globally, the Canadian investment funds industry remains significant and Canadian data on hedge funds, open-ended and closed-end funds can be compared to data from foreign jurisdictions on the IOSCO Investment Funds Statistics Dashboard. The IOSCO dashboard uses data from the IFS and aggregates public and private investment fund data from all its reporting jurisdictions, as well as showing information from individual jurisdictions.

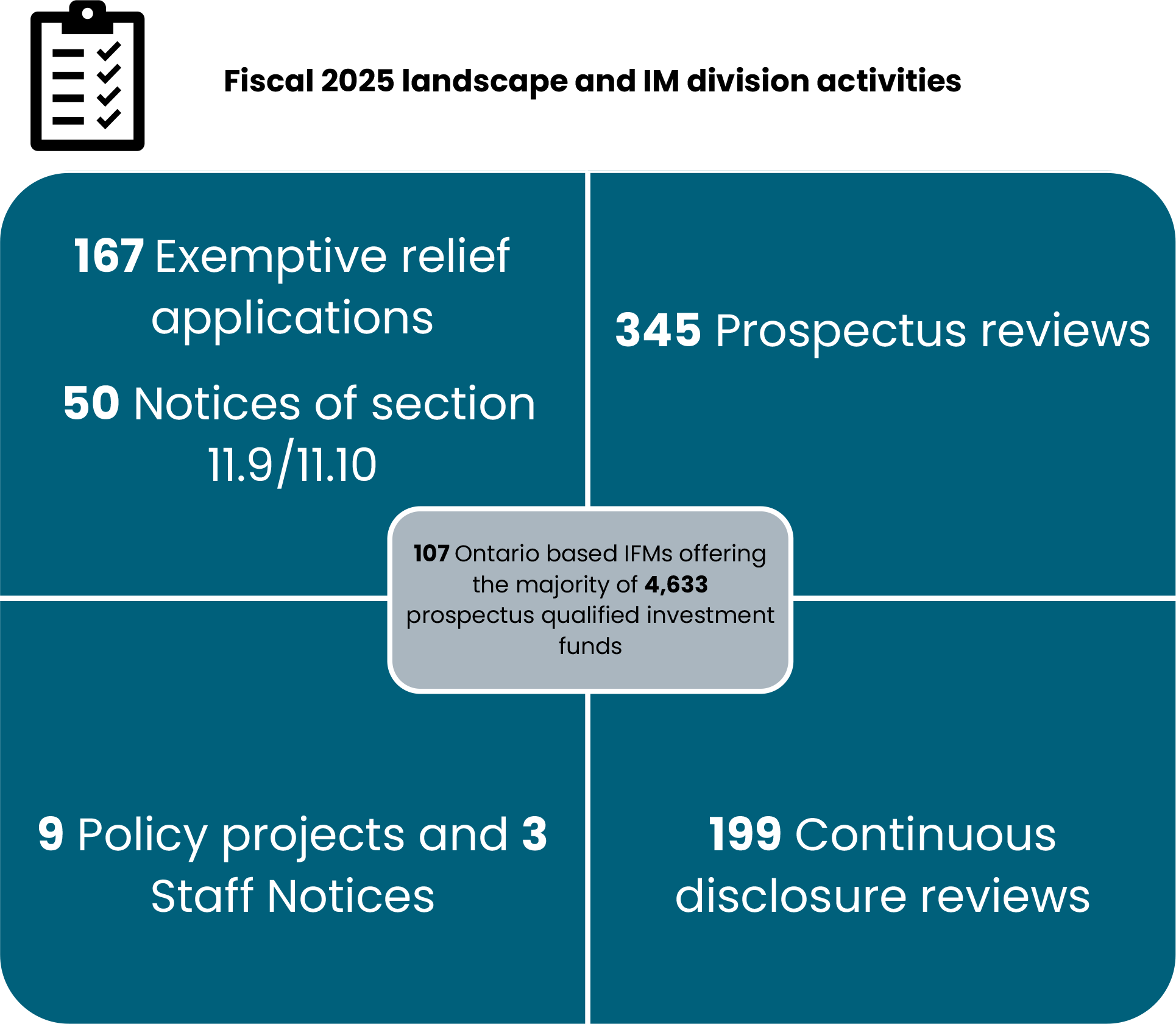

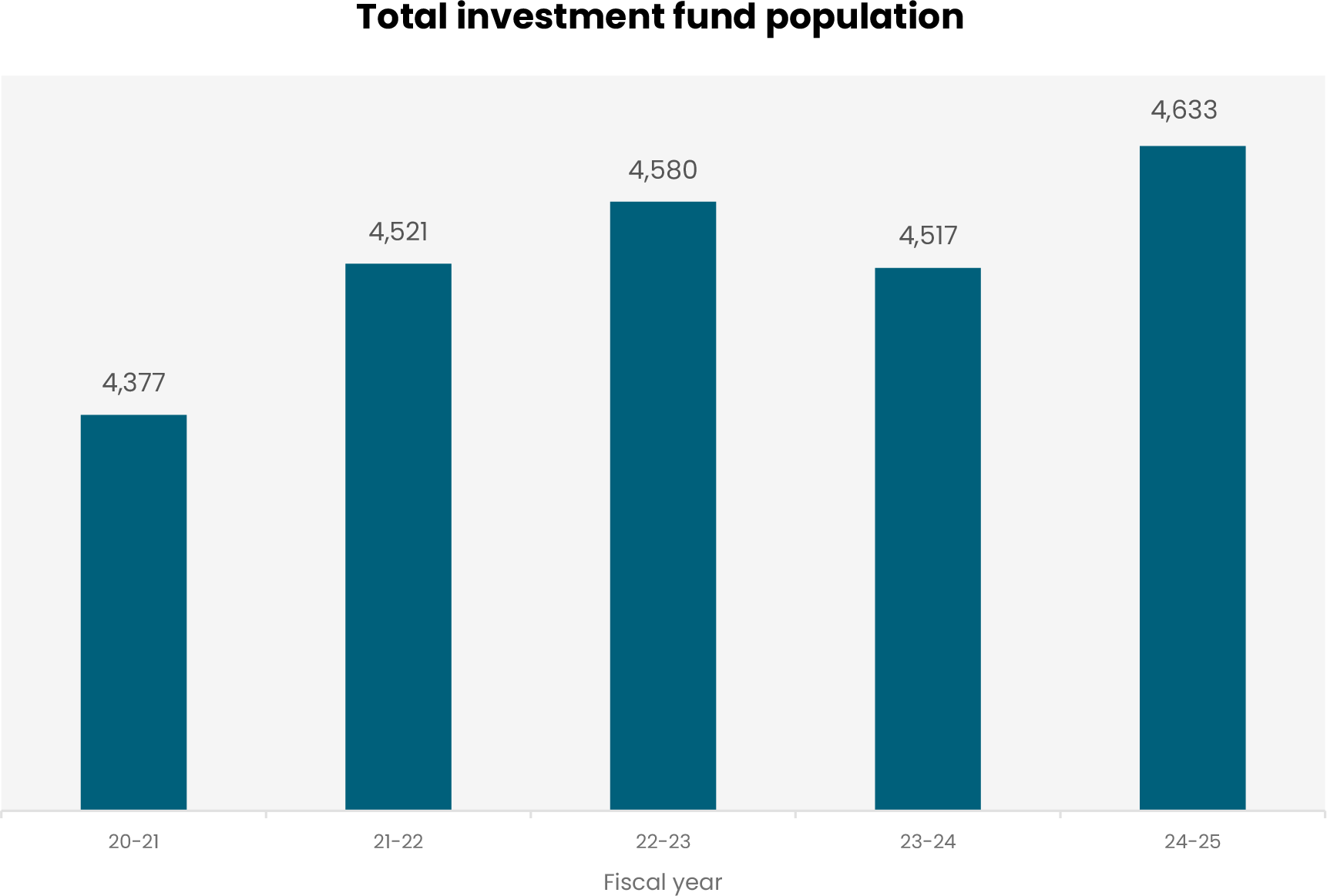

The OSC is the principal regulator to more than 80% of all Canadian investment funds, based on the head office location of the IFM. As of March 31, 2025, there were 107 Ontario-based IFMs offering the majority of the over 4,600 publicly offered investment funds, as compared to 119 IFMs in the prior year.{2} While the number of IFMs decreased during Fiscal 2025, there was a slight net increase of 116 funds in the total investment funds population.

The OSC is committed to transparency, accountability and timeliness in its regulatory functions and has set service standards and timelines which stakeholders can rely on when interacting with OSC staff. The OSC's most recent service commitment was published in March 31, 2025, and includes timelines for prospectus filings and amendments, review of exemptive relief applications, and continuous disclosure reviews. The IM division prides itself on ensuring that services are delivered efficiently and effectively. Sections I to IV below will highlight each of our main operational functions in more detail.

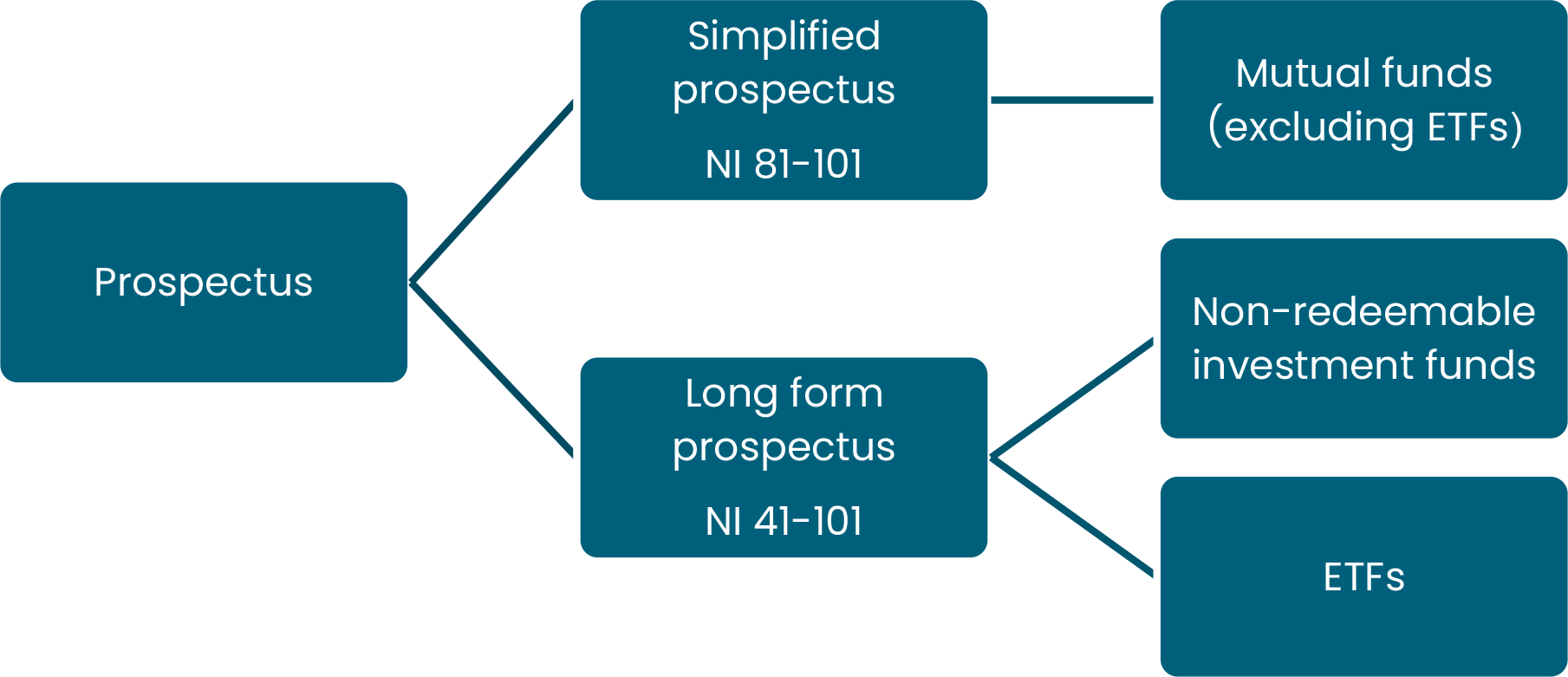

The review of preliminary and pro forma prospectuses is one of our key operational functions in regulating the sale of investment funds to retail investors. A preliminary prospectus is filed for new investment funds offerings, and a pro forma prospectus is filed to renew a prospectus that has lapsed (expired). Under Canadian securities law, an issuer must file a prospectus and obtain a receipt to "distribute" securities to the public. The type of prospectus required to be filed depends on the type of investment fund (e.g., conventional mutual fund or ETF) that is offering securities.{3}

For unique or novel products, we recommend that filers use the confidential pre-file process for prospectus and exemptive relief applications. Many filers who wish to launch a novel type of product in the market have used this process as it maintains the confidentiality of the product offering as the regulatory issues are resolved. While we understand the competitive aspect of being first to market with a novel product, we note that these types of files often require an in depth and thorough review as well as coordination with the other Canadian regulators in the CSA.

For more information on the pre-file process click here.

Staff remind IFMs that substantive changes to prospectus disclosure made after a preliminary or pro forma prospectus has been filed, or cleared for final, may cause delays in receiving a receipt for the final prospectus. More information on the review process when there have been substantive changes can be found here.

Prospectus filings are categorized by the IM division into one of three review types: standard, issue-oriented or full review. Most prospectus filings are subject to standard review, as these generally relate to investment funds that are already in distribution and have been previously reviewed. An issue-oriented review targets specific issues with the filing, while a full review is a more comprehensive and thorough review of the filing, which may occur when the prospectus is for a new manager, for a new type of fund or for a product that has features or characteristics that could raise novel issues. These filings are sometimes also accompanied by a related application for exemptive relief.

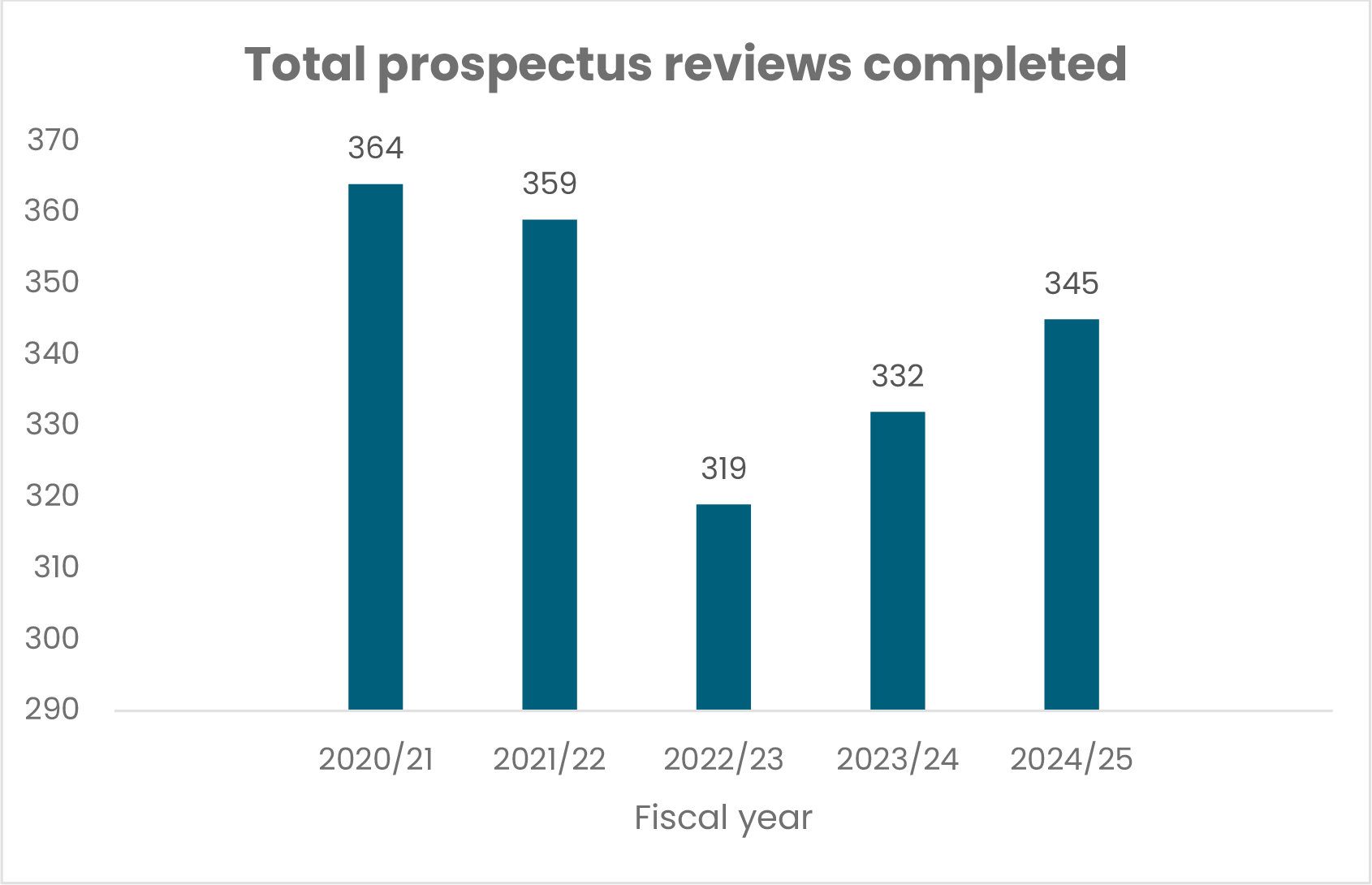

During Fiscal 2025, 86% of the prospectus reviews were standard, 12% were issue- oriented and 2% were full reviews.

For Fiscal 2025, the following trends were noted:

• There was a 4% increase in the total number of prospectus filings this fiscal year compared to last year. Over a third of the total filings were received in the first quarter (April 1 to June 30th) when markets were generally experiencing growth and IFMs may have seen this as an opportunity to launch new products. This large number of filings slowed down in the last three quarters when there was greater economic and political uncertainty in the markets.

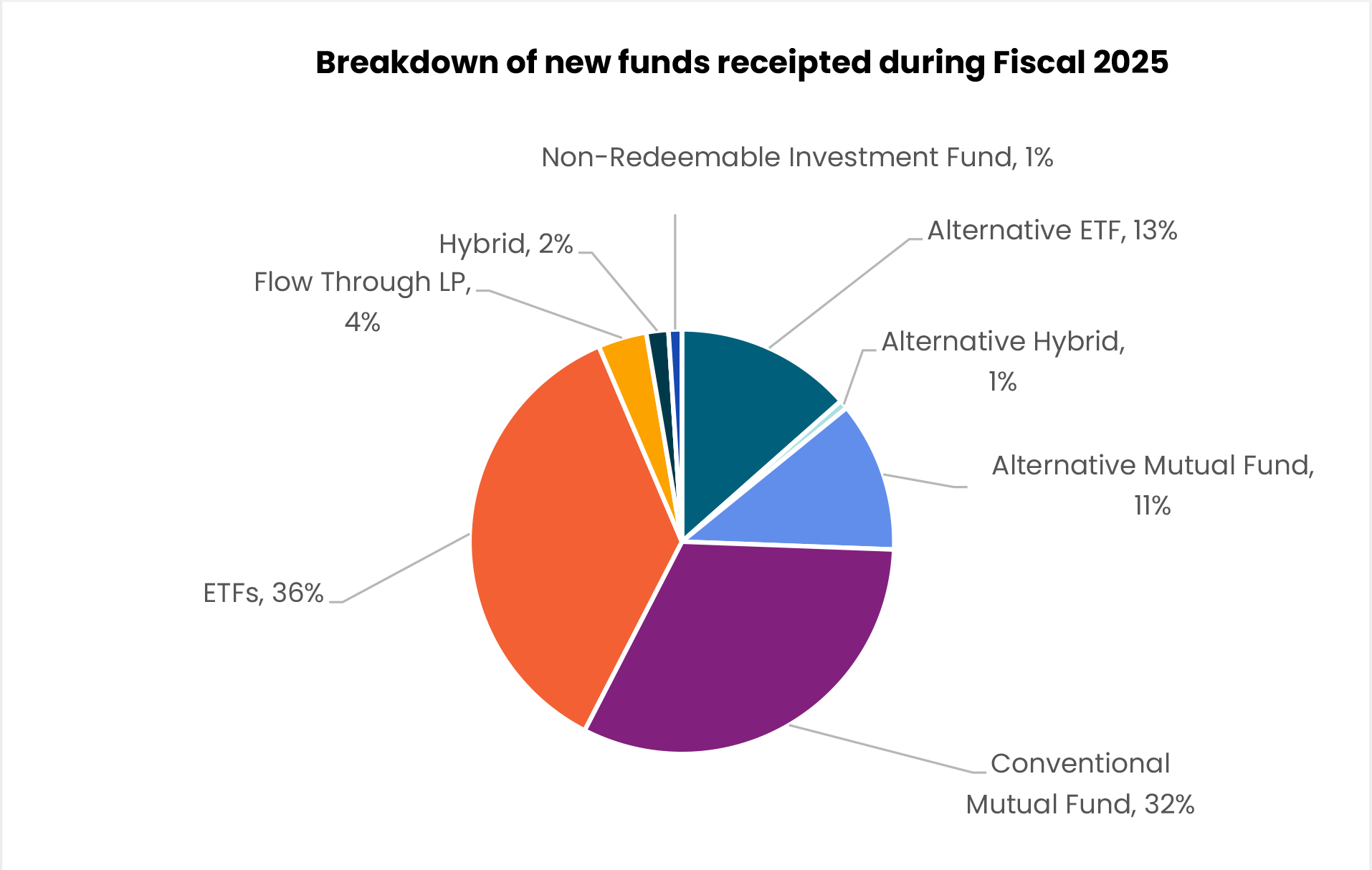

• Total new funds receipted were relatively stable with 297 in Fiscal 2025, compared to 301 in the prior year.

• For the second consecutive year, newly launched ETFs exceeded those for conventional mutual funds at 49% vs 43%, respectively, compared to 48% vs 39% in the prior year. Factors contributing to this trend are the continued strength of ETF sales and its use to launch fund products, lower fees than conventional mutual funds and new managers (non-Canadian financial institutions) expanding into the Canadian ETF market.

• Of new funds receipted this year, new launches of alternative investment funds increased from 10% (31 funds) last year to 25% (76 funds) in Fiscal 2025, with most of the increase attributable to alternative ETFs. An "alternative mutual fund" is defined under NI 81-102 as a fund that can invest primarily in physical commodities, borrow cash or engage in short selling in a manner not permitted for other mutual funds under NI 81-102. Such funds can also create leverage through derivatives up to a maximum of 300% of net asset value. Within the alternative bucket, there are a variety of types of funds including crypto asset funds, leveraged strategies, long/short strategies and single U.S issuer ETFs, providing investors with more investment options and alternative strategies.

Some of the noteworthy prospectus filings that were receipted during the fiscal period (or shortly thereafter) are summarized below, along with details on any related exemptive relief.

An emerging trend this year was the launch of several ETFs that invest in collateralized loan obligations (CLOs), primarily rated AAA. During the last quarter of Fiscal 2025, five preliminary prospectuses were filed.

CLOs are investment vehicles that hold an underlying portfolio of corporate loans that are then put into a pool, securitized and managed like a fund. Each CLO is structured as a series of tranches that are interest-paying bonds, along with a small portion of equity. As the senior tranches have first claim on the cash flows produced by the loan pool, they are commonly granted AAA-ratings by credit rating agencies.

Institutional investors have been the traditional investor for CLOs. The CLO ETFs now provide a means for retail investors to obtain exposure to this asset class. CLOs are purported to provide higher yields than similarly rated corporate bonds, while having a lower correlation to equities and reduced correlation to traditional fixed income assets.

We note that CLO ETFs have been offered to U.S. investors for several years. OSC staff will continue to monitor this trend.

Shortly after the launch of Solana futures on the Chicago Mercantile Exchange in March 2025, we receipted the first Solana ETFs in North America that provide direct spot exposure to Solana. These ETFs began trading on the Toronto Stock Exchange on April 16, 2025. Four IFMs were issued final prospectus receipts for their respective Solana ETFs. The Solana ETFs, like the Ether ETFs, are also permitted to stake Solana held to earn staking rewards for the benefit of investors. Up to half of the fund's holding can be staked.

The launch of the Solana ETFs is consistent with the CSA's final rule amendments to NI 81-102 that provide for greater regulatory clarity for public investment funds investing in crypto assets and further the CSA's commitment to financial innovation and competition while maintaining investor protection.

On October 31, 2023, the Office of the Superintendent of Financial Institutions (OSFI) announced that it was raising liquidity requirements for HISA ETFs of deposit taking institutions, as these are considered unsecured wholesale funding and require a 100% run-off, compared to the previous rate of 40%. Banks that hold deposits for HISA funds must hold sufficient high-quality liquid assets, such as government bonds, to support all HISA ETF balances that can be withdrawn within 30 days. With the new stricter rules effective January 31, 2024, staff performed a review of HISA ETFs in the previous fiscal year to monitor their activities as part of the OSFI announcement, and to ensure the policy impact was managed. As part of that review, staff communicated expectations for disclosure in future renewal prospectuses.

Staff noted that HISA ETF renewal prospectuses filed in Fiscal 2025 have enhanced prospectus disclosure that describes the existence of terms in the ETF manager's contractual agreements with deposit taking institutions that may limit the ability of the ETF manager to make timely withdrawals without sufficient notice to the deposit taking institution, for example to reinvest assets of the ETF elsewhere. The ETFs are generally permitted to make withdrawals without prior notice to satisfy unitholder redemptions. There is no impact on retail investors to purchase/sell units in the secondary market.

The IM division also reviews applications for exemptive relief, some of which are novel in nature. Novel applications generally consist of requests for relief that have not previously been granted or that deviate substantially from the fact patterns underlying any prior decisions. These applications generally take longer to review because of their nature and complexity, and we consult with the CSA on all novel applications. The test for granting the relief is whether the relief would not be prejudicial to the public interest.

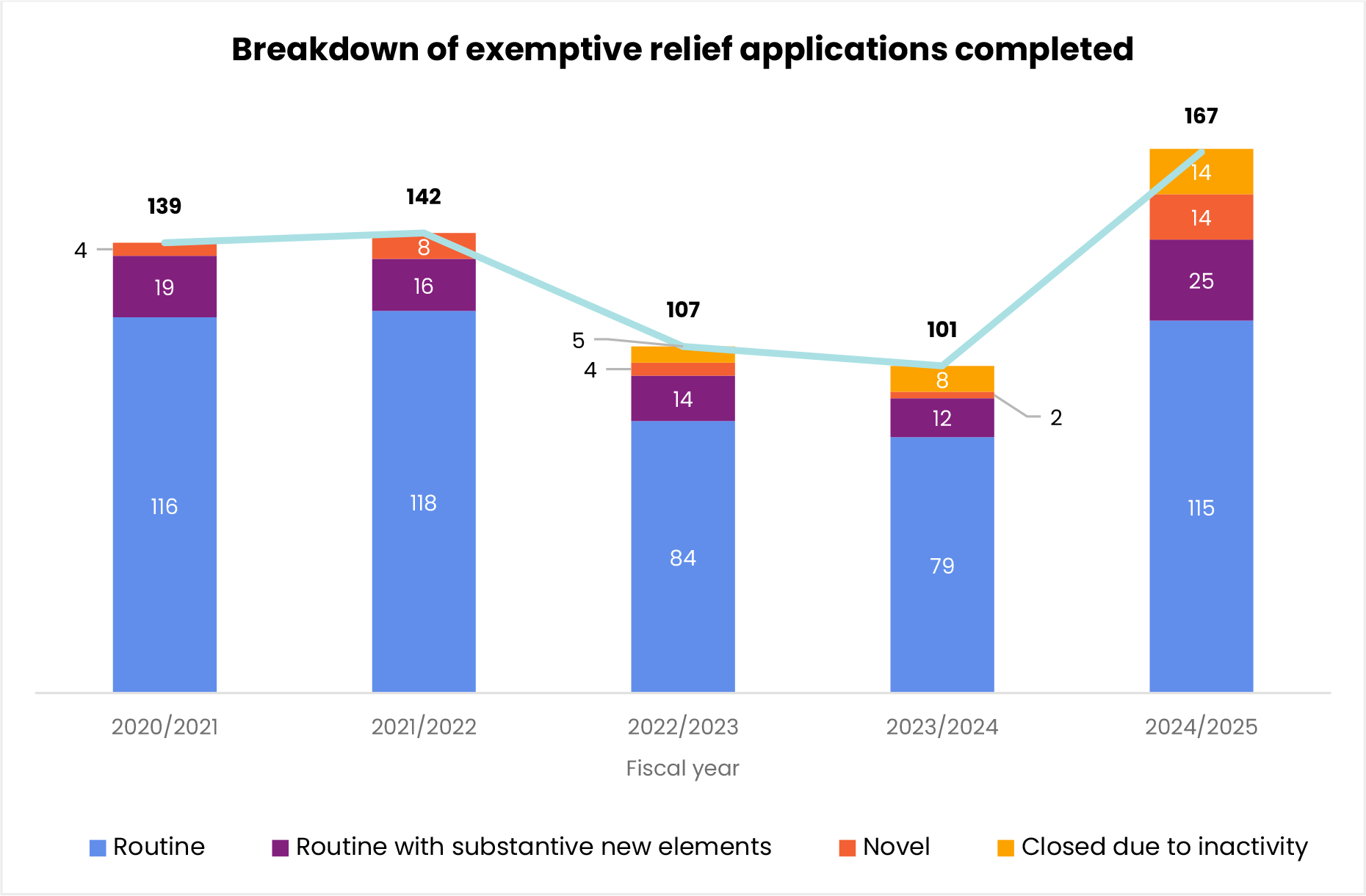

The volume of exemptive relief applications received in Fiscal 2025 increased almost 30% from the prior year. Much of this increase is due to the addition of the Portfolio Advisers team and the accompanying applications related to relief from NI 31-103. While codifying routine relief as part of our burden reduction efforts led to a decline in the number of applications in the previous two years, many of the investment fund-related applications received in Fiscal 2025 have been more novel or have unique elements. Routine applications still made up the bulk of the exemptive relief applications completed. The general increase in the volume of filing submissions early in the fiscal year as compared to the latter half is consistent with favorable market conditions early in the year and more economic uncertainty towards the end of the fiscal period.

Relief was granted in May 2024 to allow certain mutual funds managed by 11 IFMs to borrow cash on a temporary basis in an amount that does not exceed 10% of the mutual fund's net asset value at the time of borrowing to (i) accommodate requests for redemption of securities of the fund while the fund settles portfolio transactions initiated to satisfy such redemption requests, and to (ii) permit the fund to settle a purchase of portfolio securities that is executed in anticipation of the settlement of an investor's purchase of securities of the fund. Subsequent to this relief, additional IFMs applied and received similar relief.

The relief is aimed at addressing operational hurdles for those funds with exposure to non-T+1 markets, because of the implementation of T+1 settlement for securities traded in North American markets as of May 27, 2024, while certain foreign markets will continue to maintain T+2 settlement. Such markets include, but are not limited to, the European Union, the United Kingdom, Japan, Brazil, Australia, and New Zealand. The relief expires in three years.

Staff have periodically received applications on behalf of investment funds that are not reporting issuers (Pooled Funds), seeking exemptive relief from the deadline for financial statement filing and delivery requirements. These applications are typically sought by Pooled Funds that invest a significant portion of their assets in other underlying investment funds (Underlying Funds), that are established or domiciled in a foreign jurisdiction.

Relief is granted primarily to account for the additional time needed to incorporate the financial statements of the Underlying Funds into the Pooled Funds' financial statements so that they may be properly audited by the Pooled Fund's auditor.

We are reminding filers seeking this relief to, at a minimum, address the following:

• A description of the Pooled Fund's investment objectives and strategies, and how those objectives are met by investing in the Underlying Funds.

• The proportion of the Pooled Fund's net assets invested in the Underlying Funds.

• Where the Underlying Funds are domiciled.

• Why the relief is being requested (e.g. confirmation from the auditor that the Pooled Fund is unable to complete the audit of the financial statements without Underlying Fund information).

• The basis for the specific amount of additional time requested.

• What alternatives were considered (such as, for example, altering its financial year-end) to address the timing issues and why those options are impractical or unfeasible such that seeking exemptive relief is the better option.

• How the filer will inform the Pooled Fund's securityholders of the relief and give securityholders the opportunity to exit the fund on reasonable terms, within a certain window of time after being informed of the relief.

We note that the need to provide submissions unique to the situation being considered makes it unlikely that staff would be prepared to recommend this relief on a future oriented basis.

OSC and Autorité des marchés financiers staff worked collaboratively on novel relief granted in February 2025 to permit dealer-managed investment funds managed by five bank-owned investment IFMs, to invest in offerings of non-reporting issuer debt securities underwritten by a related party or a syndicate including a related party. This relief: (i) revokes prior similar relief granted to the funds, (ii) establishes revised conditions requiring the IFM's consideration of three substantive key elements relevant to the mitigation of conflicts of interest inherent in transactions contemplated by the relief, and (iii) mandates increased interaction between the IFM and the funds' Independent Review Committee (IRC) where any exceptions to the three substantive key elements are pursued.

During the period, we worked with several IFMs to accommodate extensions to their prospectus filing timelines to facilitate the consolidation of fund prospectuses for funds under common management. The lapse date requirement ensures the currency and accuracy of a prospectus to protect investors from relying on out-of- date information when purchasing securities. The lapse date extension relief enables IFMs to:

• combine the renewal of different prospectuses under the same document to streamline fund disclosure across the IFM's fund platform, allowing investors to compare their features more easily, and

• save on additional costs and expenses associated with preparing two separate renewal prospectuses, given how close in proximity the lapse dates of the different funds are to one another.

Filers are still obligated to disclose material changes, and staff are satisfied that the conditions of the relief ensure that investors are receiving current information related to their investments.

In the past year, the OSC has granted a decision, and opted into a decision of the BCSC, that provide relief from the fund-of-fund restrictions in NI 81-102, to permit certain investment funds to invest all, or substantially all of their assets in securities of an underlying U.S.-listed ETF or exchange-traded product. Five decisions of this nature were issued in Fiscal 2025, with the relief being granted to four different IFMs on behalf of six investment funds.

While relief had been granted previously to permit an investment fund to invest substantially all of its assets in an underlying U.S.-listed ETF, some of the decisions granting this relief over the past year contained substantive new elements. The facts surrounding these applications differed from one another, as did certain conditions contained in the decisions. However, there were several common elements. In each case, the underlying U.S.-listed ETF or exchange-traded product was (i) listed and traded on a recognized exchange in the U.S., (ii) managed in a manner consistent with the investment restrictions in NI 81-102, (iii) subject to disclosure requirements which were substantially similar to the disclosure requirements under NI 41-101, Form 41-101F2, Form 41-101F4, and NI 81-106, (iv) in good standing with the U.S. Securities and Exchange Commission (SEC), and (v) either an investment company subject to the Investment Company Act of 1940 or regulated by the SEC as a reporting issuer under the Securities Act of 1933.

Staff were satisfied that permitting these investment funds to invest their assets in these underlying U.S. funds could increase diversification opportunities that are otherwise not available and represent an efficient and cost-effective alternative to obtaining exposure to securities held by or strategies of the U.S. fund, without causing prejudice to investors.

When a large number of registered individuals move from one firm to another as the result of a business transaction, the acquiring firm may file an application for exemptive relief with the regulator from the individual form filing requirements, so that the transfer of registered or permitted individuals and business locations can be done on a 'bulk transfer' basis instead of an individual basis. Appendix D of 33-109CP lists the circumstances in which regulators will consider granting this relief as well as the information generally required to be submitted with an application.

Prior bulk transfer applications have typically involved a minimum of 25 individuals who must transfer their registration. Where the number of individuals moving is lower than 25, we would be unlikely to consider an application for bulk transfer relief and may ask filers to withdraw an application.

Finally, another factor impacting bulk transfer applications is timing. Bulk transfers cannot be processed through NRD from December 15 to the third week of January and therefore, the transfer will only be processed through NRD once this blackout period has expired. It is recommended that firms seeking bulk transfer relief apply at least 30 days before the effective date and include all the information in their application as set out in Appendix D to 33-109CP.

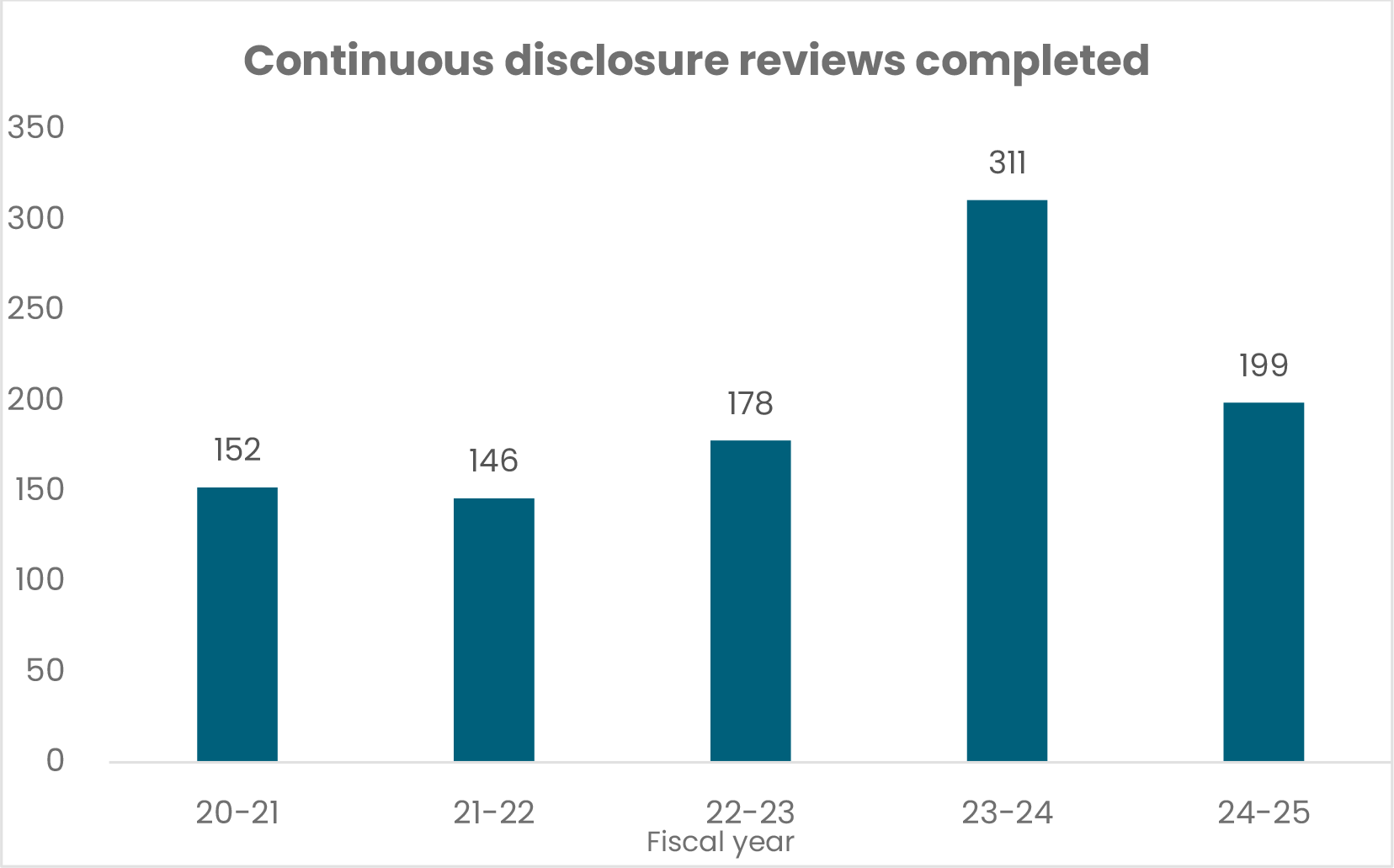

The IM division conducts standard and targeted reviews of the continuous disclosure (CD) filings of Ontario-based investment funds. Risk-based criteria are used to select investment funds to ensure compliance with disclosure requirements and to identify trends. We may also choose to conduct targeted reviews of a particular segment, on a particular issue or based on complaints received.

Although the overall number of completed CD reviews decreased in Fiscal 2025, there was a 58% increase in the number of targeted CD reviews performed compared to the prior year. These reviews take longer to complete and require more time and resources than standard reviews. The targeted reviews completed are described in more detail below.

Outlined below are the major reviews completed during the fiscal period:

We conducted an issue-oriented desk review of investment funds to determine if issuers were exaggerating their investment products' use of artificial intelligence (AI).

The review identified approximately 15 issuers that use the term AI or other related terminology (Generative AI, Large Language Model, Machine Learning, etc.) The vast majority of the 15 issuers use the term AI to indicate investments in large companies that are at the forefront of research and development of AI. There was no evidence noted of issuers using the term AI or related terminology in a misleading manner to attract investors, or of AI being used to perform portfolio management services.

Staff will continue to review the funds' disclosure around AI washing to ensure there are no misleading or inaccurate claims.

Staff conducted a review of small issuers with a focus on IFMs with total AUM of less than $100 million as well as small funds with less than $10 million in net assets. Staff reviewed documents for compliance with filing and disclosure requirements and clear presentation, such as the various compliance reports under NI 81-102, financial statements, the Management Report of Fund Performance (MRFP), prospectuses, and the IFM's website and other marketing materials for any misleading or egregious presentation. Staff noted that some smaller issuers have disclosure in the MRFP which is inconsistent with regulatory requirements or is not fulsome in nature, as well as other minor issues in the other disclosure documents or compliance reports. With regards to compliance reports that are required to be filed, issuers are reminded to submit the documents by the filing deadline in SEDAR+ under the appropriate SEDAR+ profile number. The review of small issuers is ongoing, and staff will determine whether guidance is needed in this area upon completion of the review and in conjunction with the ongoing policy initiative related to the modernization of continuous disclosure documents, including the MRFP, which is described in more detail in Part B.

Staff conducted detailed analysis on the data collected through the IFS for the year ended December 31, 2023, focusing on key risk areas including portfolio liquidity and financial leverage of investment funds.

Staff selected several key performance indicators (KPIs) or regulatory markers to compare and identify funds which were outliers compared to their peers or offside any regulatory restrictions for that particular type of investment fund. During Fiscal 2025, the analysis focused on the following areas:

• Portfolio liquidity -- the percentage of a fund's assets that require more than 365 days to liquidate.

• Cash borrowing -- the percentage of a fund's cash borrowing relative to its net asset value.

• Total borrowing and short sales -- the percentage of a fund's cash and securities borrowing relative to its net asset value.

• Aggregate exposure to borrowing, short selling and specified derivatives.

The majority of the funds complied with the applicable regulatory requirements for the KPIs selected based on the IFS data. Where outliers were identified, staff examined prospectuses, continuous disclosure documents and portfolio holdings to ensure that the funds were not offside regulatory requirements and to understand why the funds differed from their peers.

In some cases, the funds were outliers for valid reasons, for example due to receiving exemptive relief or erroneously identifying themselves as mutual funds in the IFS when they were in fact, alternative mutual funds and subject to different requirements. Some funds experienced transitory fluctuations in their borrowing or liquidity and staff will monitor these funds going forward using data from the most recent IFS.

Staff will continue to monitor outliers and incorporate data from the latest IFS to look for trends or issues that require further action.

Fund managers must use the CSA risk classification methodology to determine the investment risk level of conventional mutual funds and ETFs for use in the Fund Facts document and in the ETF Facts document, respectively. Under the CSA methodology, a mutual fund must calculate its standard deviation for the most recent 10 years to determine its investment risk level on the 5-category risk scale in the Fund Facts or ETF Facts, as applicable. IFMs are permitted to use discretion to classify a mutual fund at a higher investment risk level than that indicated by the standard deviation calculation, if it is reasonable to do so in the circumstances.

During the period, staff conducted a CD review to better understand the IFMs' use of discretion to increase the investment risk level of a mutual fund, including the circumstances under which discretion has or has not been used, and the related policies and procedures. CD review letters were sent to 45 IFMs of varying ranges of assets under management that manage mutual funds.

The review found that over 64% of IFMs have used discretion to increase a fund's risk rating. Among the reasons cited were the following:

• to avoid unnecessary disruption and confusion to investors by maintaining a previous risk rating,

• when a fund is on the cusp of two standard deviation ranges,

• to have the same investment risk level as comparable funds, and

• when higher volatility is anticipated.

Of note, in 2019, some IFMs reportedly used discretion to maintain a fund's investment risk level as disclosed in the most recently filed Fund Facts or ETF Facts when the 10-year standard deviation calculation under the CSA methodology no longer included the performance returns of the 2008 financial crisis.

The results of the review are summarized in OSC Staff Notice 81-338 Guidance on the Use of Discretion Under the CSA Investment Risk Classification Methodology. The staff notice also encourages all IFMs to adopt policies and procedures to determine the appropriateness of using discretion to increase a fund's investment risk level under the CSA methodology.

During the past fiscal year, staff continued to review sales communications of investment funds in accordance with the disclosure requirements in Part 15 of NI 81-102. Part 15 outlines how mutual funds can communicate and advertise their products to potential investors, including limitations on what information can be disclosed and what types of claims can be made in sales materials.

Through this review, staff noted that instances of non-compliance continue to occur in certain sales communications that are widely distributed through an IFM's website and social media (e.g., YouTube and LinkedIn). Instances of non-compliance through these sources included sales communications that:

• referred to a performance rating or ranking and included investment fund performance data without satisfying certain disclosure requirements,

• referenced non-compliant yield disclosure for certain investment funds that had not distributed securities under a prospectus for at least 12 consecutive months,

• included attention-grabbing high yield or high distribution rate information without also including standard performance data or ensuring that both data points were equally prominently displayed.

Where issues were identified that did not comply with the disclosure requirements, the sales communications were amended or removed as needed. Where there was continued non-compliance, staff referred the matter to the Registrant Conduct Team of the RIE division for further regulatory action.

To provide transparency to the market on amendments made to an investment fund's continuous disclosure record, website or social media during a staff review, staff may request the issuance of a news release by the IFM in relation to such corrections and place the affected investment fund issuers on the Refilings and Errors List for a period of three years.

We encourage IFMs to review the November 2023 article outlining staff's concerns around high yield figures being prominently displayed and emphasized over all other aspects of a fund's sales communication and marketing materials. Staff will continue to monitor investment fund sales communications to ensure compliance with disclosure requirements.

In Ontario, crypto asset funds are offered by seven IFMs and data on the crypto asset landscape is shown below:

Fiscal year |

# of Ontario public crypto asset funds |

AUM of crypto asset funds |

# crypto asset funds receipted |

# crypto asset funds terminated |

|

||||

2025 |

25 |

$7.35 billion |

44 |

0 |

|

||||

2024 |

21 |

$7.45 billion |

0 |

3 |

|

||||

2023 |

24 |

$2.85 billion |

2 |

1 |

|

||||

2022 |

23 |

$6.89 billion |

17 |

0 |