Ontario Securities Commission Bulletin

Issue 47/50 - December 12, 2024

Ont. Sec. Bull. Issue 47/50

• Nova Tech Ltd and Cynthia Petion

• Nova Tech Ltd and Cynthia Petion -- ss. 127(1), 127.1

• CSA Staff Notice 11-312 (Revised) National Numbering System

• Ontario Securities Commission Staff Notice 51-736 -- Corporate Finance Division 2024 Annual Report

• Place Montfort Apartment Project

• A&W Revenue Royalties Income Fund

• S Split Corp. -- s. 1(6) of the OBCA

• Brandes Investment Partners & Co.

• Florence Wealth Management Inc. et al.

• Invesco Canada Ltd. and Invesco Balanced-Risk Allocation Pool

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Carta Capital Markets, LLC -- Revocation of Exemptive Relief -- Notice of Commission Decision

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Nova Tech Ltd and Cynthia Petion

FOR IMMEDIATE RELEASE

December 4, 2024

TORONTO -- The Tribunal issued its Reasons and Decision and an Order in the above-named matter.

A copy of the Reasons and Decision and Order both dated December 3, 2024 are available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Oasis World Trading Inc. et al.

FOR IMMEDIATE RELEASE

December 5, 2024

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated December 5, 2024 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

December 6, 2024

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated December 6, 2024 is available at capitalmarketstribunal.ca.

Subscribe to notices and other alerts from the Capital Markets Tribunal:

For Media Inquiries:

For General Inquiries:

Nova Tech Ltd and Cynthia Petion -- ss. 127(1), 127.1

File No. 2023-20

Adjudicator: |

M. Cecilia Williams (chair of the panel) |

Sandra Blake |

|

Jane Waechter |

December 3, 2024

(Subsection 127(1) and section 127.1 of theSecurities Act, RSO 1990, c S.5)

WHEREAS on October 2, 2024, the Capital Markets Tribunal held a hearing by videoconference, to consider the sanctions and costs that the Tribunal should impose on Nova Tech Ltd and Cynthia Petion as a result of the findings in the Reasons and Decision on the merits issued July 19, 2024;

ON READING the materials filed by the Ontario Securities Commission, and on hearing the submissions of the representative for the Commission and no one appearing on behalf of the respondents;

IT IS ORDERED THAT:

1. with respect to the respondents, Nova Tech and Petion:

a. pursuant to paragraph 2 of s. 127(1) of the Act, trading in any securities by the respondents shall cease permanently;

b. pursuant to paragraph 2.1 of s. 127(1) of the Act, the acquisition of any securities by the respondents is prohibited permanently;

c. pursuant to paragraph 3 of s. 127(1) of the Act, any exemptions contained in Ontario securities law do not apply permanently to the respondents;

d. pursuant to paragraph 8.5 of s. 127(1) of the Act, the respondents are permanently prohibited from becoming or acting as a registrant or a promoter;

e. pursuant to paragraph 9 of s. 127(1) of the Act, the respondents shall jointly and severally pay to the Commission an administrative penalty of $2,500,000;

f. pursuant to paragraph 10 of s. 127(1) of the Act, the respondents shall jointly and severally disgorge to the Commission $31,000; and

g. pursuant to s. 127.1 of the Act, the respondents shall jointly and severally pay $193,333.52 to the Commission for the costs of the investigation and hearing; and

2. with respect to Petion:

a. pursuant paragraph 7 of s. 127(1) of the Act, Petion shall resign any position that she holds as a director or officer of any issuer;

b. pursuant to paragraph 8 of s. 127(1) the Act, Petion is permanently prohibited from becoming or acting as a director or officer of any issuer;

c. pursuant to paragraph 8.1 of s. 127(1) of the Act, Petion shall resign any position that she holds as a director or officer of any registrant; and

d. pursuant to paragraph 8.2 of s. 127(1) of the Act, Petion shall be prohibited permanently from becoming or acting as a director or officer of any registrant.

Oasis World Trading Inc. et al.

File No. 2023-38

Adjudicator: |

Mary Condon |

December 5, 2024

WHEREAS on December 5, 2024, the Capital Markets Tribunal held a hearing by videoconference;

ON HEARING the submissions of the representatives for the Ontario Securities Commission and for the respondents;

IT IS ORDERED THAT:

1. each party shall serve the other parties with a book of documents containing copies of the documents, and identifying the other things that the party intends to produce or enter as evidence at the merits hearing by 4:30 p.m. on March 20, 2025;

2. each party shall advise all other parties of any issues about the authenticity or admissibility of documents contained in the books of documents by 4:30 p.m. on March 28, 2025;

3. each party shall provide to the Registrar a completed copy of the Hearing Participant Checklist by 4:30 p.m. on March 28, 2025;

4. a further case management hearing in this matter is scheduled for April 3, 2025, at 10:00 a.m., by videoconference, or as may be agreed to by the parties and set by the Governance & Tribunal Secretariat;

5. the Commission shall serve and file the affidavit of Yu Chen by 4:30 p.m. on April 8, 2025; and

6. each party shall provide to the Registrar electronic versions of their book of documents containing the documents that the party intends to rely on or enter as evidence at the merits hearing by 4:30 p.m. on April 29, 2025.

File No. 2022-9

Adjudicator: |

Russell Juriansz |

December 6, 2024

WHEREAS on December 6, 2024, the Capital Markets Tribunal held a hearing by videoconference to set a schedule for a sanctions and costs hearing in this proceeding;

ON HEARING the submissions of the representatives for the Ontario Securities Commission, Receiver for Bridging Finance Inc., Natasha Sharpe and Andrew Mushore, no one appearing for David Sharpe, and on considering that all parties in attendance agree to the schedule below;

IT IS ORDERED THAT:

1. The Commission shall serve and file written evidence, if any, and written submissions on sanctions and costs, by 4:30 p.m. on February 7,2025;

2. the respondents shall each serve and file written evidence, if any, and written submissions on sanctions and costs, by 4:30 p.m. on March 26, 2025;

3. the Commission shall serve and file reply written evidence, if any, and reply written submissions on sanctions and costs, if any, by 4:30 p.m. on April 16, 2025; and

4. the hearing with respect to sanctions and costs shall commence on April 28, 2025 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, and continue on April 29 and 30, 2025, commencing at 10:00 a.m. on each day, or as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Nova Tech Ltd and Cynthia Petion -- ss. 127(1), 127.1

Citation: Nova Tech Ltd (Re), 2024 ONCMT 28

Date: 2024-12-03

File No. 2023-20

(Subsection 127(1) and section 127.1 of the Securities Act, RSO 1990, c S.5)

Adjudicator: |

M. Cecilia Williams (chair of the panel) |

|

Sandra Blake |

||

Jane Waechter |

||

|

||

Hearing: |

October 2, 2024 |

|

|

||

Appearances: |

Brian Weingarten |

For the Ontario Securities Commission |

|

||

No one appearing for Nova Tech Ltd or Cynthia Petion |

||

[1] In a decision on the merits dated July 19, 2024 (the Merits Decision),{1} the Capital Markets Tribunal found that Nova Tech Ltd breached the Securities Act (theAct){2} through unregistered trading, illegal distribution of securities, and breaching the Tribunal's temporary cease trade order. The Tribunal also found that Cynthia Petion violated Ontario securities law by authorizing Nova Tech's violations of the Act.

[2] The Ontario Securities Commission asks the Tribunal to impose a broad range of sanctions against Nova Tech and Petion pursuant to s. 127(1) of the Act, and for an order requiring them to pay the Commission's costs of the investigation and this proceeding. The respondents did not respond or otherwise participate.

[3] For the reasons set out below, we conclude that it is in the public interest to order that Nova Tech and Petion be subject to permanent bans from participating in Ontario's capital markets, pay an administrative penalty of $2.5 million, disgorge $31,000 and pay costs of $193,333.52.

[4] Nova Tech told investors that it would earn three percent per week returns for them by trading in foreign exchange and crypto assets using pooled investor funds.{3} It promoted these returns over YouTube, its website, and a Telegram channel with 30,000 subscribers.{4}

[5] Ultimately, Nova Tech stopped allowing investors to make withdrawals and later stopped communicating with investors. Investors lost the money they continued to hold in accounts with Nova Tech.{5}

[6] In the Merits Decision, the Tribunal found that Nova Tech violated Ontario securities law because:

a. it did not file a prospectus with the Commission pertaining to the securities it was offering to investors;

b. it did not register with the Commission; and

c. it continued to accept new investments despite a Tribunal cease trade order prohibiting Nova Tech from doing so.

[7] Petion is the founder, sole director, and CEO of Nova Tech. She oversaw its operations and promoted its investments.{6} The Tribunal found that Petion authorized Nova Tech's breaches of Ontario securities law and, therefore, personally violated Ontario securities law.

[8] The Tribunal may impose sanctions under s. 127(1) of the Act where it is in the public interest to do so. The Tribunal's exercise of that jurisdiction must be consistent with the purposes of the Act, which include protecting investors from unfair, improper, and fraudulent practices, and fostering fair and efficient capital markets and confidence in the capital markets.

[9] Sanctions are protective and are intended to prevent future harm to investors and to the capital markets.{7}

[10] In this case, the Commission seeks the following sanctions and costs against Nova Tech and Petion:

a. permanent prohibitions on their participation in Ontario's capital markets;

b. an administrative penalty of $2,500,000, on a joint and several basis;

c. disgorgement of $31,000, on a joint and several basis; and

d. costs of $193,333,52, on a joint and several basis.

[11] We agree that the requested sanctions and costs are appropriate for the reasons below.

[12] The Tribunal has identified various sanctioning factors that may be relevant when assessing breaches of Ontario securities law.{8} We will focus on the seriousness of Nova Tech and Petion's misconduct and on specific and general deterrence.

[13] We find that the circumstances of this case weigh heavily in favour of significant sanctions. Furthermore, we find that there are no mitigating factors to consider for Nova Tech's and Petion's misconduct. Rather, we find that the broad-based solicitation of investors, the failure to provide required information to investors, and the blatant breach of the temporary cease trade order all served as aggravating factors in determining sanctions.

[14] The Commission submits that Nova Tech's and Petion's misconduct was egregious. We agree. It was far from the behaviour that Ontario investors have a right to expect when dealing with legitimate market participants. They:

a. accessed the Ontario capital markets virtually through a broad-based solicitation of investors through Nova Tech's website, a YouTube channel, an active Telegram channel, and a web-based investment platform;

b. promoted a security to investors without disclosure of the risks involved, securing at least 8,500 Ontario investors;

c. gave financial incentives to investors to bring other investors to Nova Tech;

d. stopped communicating with investors when faced with an influx of investor withdrawal requests; and

e. did not return either invested funds or promised returns to investors.

[15] All these activities were done outside Ontario's cornerstone framework of regulatory licensing and prospectus disclosure. This denied Ontario investors access to a prospectus that they were entitled to receive under Ontario securities law. A prospectus could have provided sufficient information to help them realistically assess their investments.

[16] Nova Tech's investors also did not receive the protections that are available to investors who use investment professionals authorized by the Commission to act on behalf of investors. Those protections include proficiency, integrity, and financial solvency requirements, all of which could have shielded investors from financial loss.

[17] We find that, by denying investors these critical protections of Ontario securities law, Nova Tech and Petion engaged in serious misconduct deserving significant sanctions.

[18] Additionally, we find that Nova Tech and Petion were flagrant in their disregard for the Tribunal's temporary cease trade order. The Tribunal found that Nova Tech made an illusory change to its website to remove Canada from a list of jurisdictions where eligible investors could reside. The change was illusory because:

a. Nova Tech told investors in a YouTube video how to circumvent jurisdictional restrictions that applied to them by simply choosing another jurisdiction listed on Nova Tech's website;{9}

b. a Commission investigator demonstrated that following those instructions allowed him to invest from Ontario while the Tribunal's cease trade order was in effect;{10} and

c. Investor C also testified about learning this evasive strategy from a Nova Tech YouTube video.{11}

[19] The Commission also urged us to consider as an aggravating factor the fact that Nova Tech solicited investors by promising astonishing returns or extraordinary wealth. We have not taken these facts into account in determining sanctions, since the Commission did not allege in the Statement of Allegations any statutory breach or raise any other addressable concern related to the purported returns.

[20] Nova Tech's and Petion's flagrant disregard for a Tribunal order warrants significant sanctions.

[21] Sanctions play a key role in specific deterrence, which involves discouraging future misconduct by the respondents to an enforcement proceeding -- in this case, Nova Tech and Petion. Sanctions are also designed for general deterrence, that is to dissuade other like-minded individuals or companies from carrying out similar activities. Both specific and general deterrence are designed to protect Ontario investors from future misconduct.

[22] We find that, given their serious wrongdoing, Nova Tech and Petion should be subject to substantial sanctions to promote specific deterrence. Those sanctions should also speak to others who consider preying on Ontario investors and, as a result, promotes general deterrence as well.

[23] The Commission requests that the respondents be ordered to disgorge $31,000 on a joint and several basis. Such an order is authorized by paragraph 10 of s. 127(1) of the Act, which refers to disgorgement of "any amounts obtained" because of non-compliance with Ontario securities law. A disgorgement order also may be made joint and several between a corporation and the directing minds of that corporation when the corporation receives funds through a contravention of the Act.{12}

[24] Although there was not an explicit finding in the Merits Decision that Petion was a directing mind of Nova Tech, that does not preclude such a finding now.{13} The Merits Decision found that as the founder, sole director and CEO of Nova Tech, Petion was credited with "creating, planning, implementing and integrating the strategic direction" of Nova Tech and for overseeing the operations of the company.{14} Therefore, we find that Petion was the directing mind of Nova Tech and should be joint and severally liable for the disgorgement order.

[25] The Tribunal has developed a non-exhaustive list of factors to determine both whether disgorgement is appropriate and what amount should be disgorged:

a. whether an amount was obtained by a respondent because of non-compliance with Ontario securities law;

b. the seriousness of the misconduct and whether that misconduct caused serious harm, whether directly to investors or otherwise;

c. whether the amount obtained because of the non-compliance is reasonably ascertainable;

d. whether those who suffered losses are likely to obtain redress; and

e. the deterrent effect of a disgorgement order on the respondents and other market participants.{15}

[26] The Commission bears the onus of proving on a balance of probabilities the amounts obtained by a respondent because of their non-compliance with Ontario securities law. Once a disgorgement figure has been established, the onus shifts to the respondent to disprove the reasonableness of that number. Any risk of uncertainty in calculating disgorgement falls on the respondent whose breach of the Act is the basis of that uncertainty.{16}

[27] The Commission was unable to present a comprehensive disgorgement amount pertaining to all Ontario Nova Tech investors. Nova Tech and Petion caused the Commission's inability to demonstrate a comprehensive disgorgement amount by not participating in the investigation or proceeding.

[28] The Commission's requested disgorgement order relates to the $31,000 invested by the three Ontario residents who testified in this proceeding. Those proven investments were obtained by Nova Tech because of the respondents' non-compliance with Ontario securities law. During the sanctions hearing, we asked about the $2,250 that Investor B was able to withdraw from their Nova Tech account after Nova Tech started restricting withdrawals. The Commission argued that we should apply the principle in Mughal where the Tribunal found that in the context of a Ponzi scheme, it may not be appropriate to reduce a disgorgement order by amounts returned to investors.{17} The Tribunal's rationale in Mughal was that "[t]he payments to investors in a Ponzi scheme are not intended to make investors whole or to repair harm done by the fraud; rather, they are a necessary element of the Ponzi scheme to allow it to continue."{18} While we agree with that approach for a proven Ponzi scheme, Nova Tech and Petion were not alleged to operate a Ponzi scheme. As such, the rationale that applied in Mughal does not apply to these facts.

[29] While it was not alleged that Nova Tech and Petion operated a Ponzi scheme, we read the Act broadly and purposively and find that $31,000 represents amounts obtained by the respondents because of their non-compliance. Considering all the factors in making an order for disgorgement, and in particular the seriousness of the misconduct, the fact that one investor received a small return on investment does not weigh in favour of reducing the disgorgement order sought in these circumstances. We find that it is more likely than not that the respondents obtained significantly more than the requested disgorgement amount, given that there were at least 8,500 Nova Tech investors in Ontario and that Nova Tech was entitled to a $25 monthly fee from each investor's account.

[30] For those reasons, we exercise our discretion to order $31,000 in disgorgement against the respondents, jointly and severally. In doing so, we rely on our earlier conclusion about the seriousness of the respondents' misconduct, together with specific and general deterrence.

[31] The Commission seeks an administrative penalty of $2.5 million, to be paid jointly and severally by Nova Tech and Petion.

[32] Paragraph 9 of s. 127(1) of the Act provides that if a person or company has not complied with Ontario securities law, the Tribunal may require the person or company to pay an administrative penalty of not more than $1,000,000 for each failure to comply.

[33] The requested administrative penalty is broken down by the Commission as follows:

a. $1,000,000 for the breach of s. 25(1);

b. $1,000,000 for the breach of s. 53(1); and

c. $500,000 for the breach of the cease trade order.

[34] The Commission asks for a total administrative penalty of $2 million for Nova Tech's breaches of s. 25(1) and s. 53(1), together with joint and several liability for Petion because she authorized Nova Tech's breaches. The Commission submits that this was not merely a technical breach of s. 25(1) and s. 53(1), but serious misconduct circumventing the gatekeeper provisions of the Act. We agree.

[35] The Commission has drawn our attention to recent decisions involving unregistered trading and illegal distributions through online trading platforms. In Mek Global Limited (Re),{19} the respondents, like Nova Tech, engaged in unregistered trading and illegal distributions of securities through a crypto asset trading platform. The Mek Global respondents and Nova Tech both operated global platforms and their misconduct was recurring. The Tribunal imposed a $2 million administrative penalty.

[36] In Mek Global, the Tribunal held that when determining the appropriate administrative penalty, it was appropriate to consider the fact that disgorgement was not possible since the respondents did not cooperate with the Commission and because of their offshore character. This prevented the collection of information about the fees or other amounts received through the respondents' operations in Ontario.{20}

[37] Polo Digital Assets, Ltd (Re){21} involved unregistered trading and an illegal distribution of securities through the operation of an online crypto asset trading program.{22} It had approximately 9,300 Ontario accounts,{23} which is similar in scope to Nova Tech's Ontario presence of approximately 8,500 accounts. The Tribunal imposed a $1.5 million administrative penalty.

[38] In Polo Digital, the Tribunal explained that "there is a need for regulatory sanctions to create economic incentives to foster compliance or alternatively, remove economic incentives for non-compliance."{24} In other words, sanctions were necessary to create an economic disincentive for future misconduct by Polo Digital. In Polo Digital, an ascertainable amount was proven in support of a disgorgement order for more than $1.8 million.{25} Even with this sizeable disgorgement amount, the Tribunal ordered an administrative penalty of $1.5 million.{26}

[39] Unlike this case, neither Mek Global nor Polo Digital involved a breach of a Tribunal temporary cease trade order.

[40] The economic incentives seen in Mek Global and PoloDigital are equally applicable in this case. The Commission submits, and we agree, that because a comprehensive disgorgement order is unavailable, we should promote specific and general deterrence by ordering an administrative penalty against Nova Tech of $1 million for unregistered trading plus $1 million for illegal distribution of securities to Ontario investors. The same economic incentives apply to Petion, who we order is jointly and severally liable with Nova Tech to pay administrative penalties. This aspect of the sanctions will prevent the respondents from reaping a windfall from their illegal conduct in Ontario.

[41] The Commission is seeking a joint and several administrative penalty of $500,000 for Nova Tech's breach of the cease trade order and Petion authorizing this breach.

[42] The Commission referred us to MOAG Gold Resources Inc (Re), a case where the only allegation was that the respondents breached a cease trade order. In Moag, the individual respondents were ordered to pay administrative monetary penalties of $200,000 and $400,000 for misconduct involving trading in debentures while a Tribunal cease trade order was in effect. The Tribunal found that the conduct was serious and recurring and affected many investors.{27}

[43] The Commission asks us to find that the misconduct in this case was more egregious than that in MOAG because of Nova Tech's illusory compliance efforts. As stated above, we find flagrant misconduct in Nova Tech's breach of the Tribunal's temporary cease trade order and Petion's authorization of that breach. Their efforts to circumvent the Tribunal's order should attract a substantial penalty, and we find that an administrative penalty of $500,000, joint and several as against Nova Tech and Petion, is appropriate in the circumstances.

[44] The Commission asks that we impose permanent restrictions on the respondents' participation in Ontario's capital markets. Specifically, the Commission asks for an order that:

a. trading in any securities by the respondents cease permanently;

b. the acquisition of any securities by the respondents cease permanently;

c. any exemptions in Ontario securities laws do not apply to the respondents permanently; and

d. the respondents be prohibited permanently from becoming or acting as a registrant or a promoter.

[45] The Commission submits, and we agree, that participation in the capital markets is a privilege and not a right.

[46] The Commission relies on Mek Global and Polo Digital, where the Tribunal imposed permanent market participation bans on the corporate respondents. In those cases, no individuals were named as respondents.

[47] We agree that the proposed permanent bans from participating in Ontario's capital markets are necessary. Mek Global and Polo Digital involved similar violations of registration and prospectus requirements. Permanent bans are needed to reflect the serious nature of the respondents' violations of cornerstone provisions of Ontario securities law and to guard against potential harm that the respondents may cause to Ontario investors in future.

[48] The respondents have misused Ontario's capital markets and should not be permitted to do so again. Anything less than a permanent ban would result in a loss of confidence in the integrity of Ontario's capital markets and expose investors to the elevated risks that Nova Tech, Petion, and like-minded persons pose.

[49] With respect to Petion, the Commissions asks for an order that:

a. Petion resigns any positions as a director and/or officer of any issuer or registrant; and

b. Petion be prohibited permanently from becoming or acting as a director or officer of any issuer or registrant.

[50] We agree that these sanctions are appropriate for Petion. She was the sole director, chief executive officer and public face of Nova Tech, was responsible for the serious and repeated breaches of the Act, and bears responsibility for the illusory jurisdictional restrictions used in the face of the Tribunal's temporary cease trade order.

[51] We find that Petion cannot be trusted to engage in corporate governance appropriately or lawfully. It is important that Ontario investors are permanently protected against any future venture involving Petion.

[52] Section 127.1 of the Act authorizes the Tribunal to order a respondent to pay the costs of an investigation or a hearing if the Tribunal is satisfied that the person or company has not complied with Ontario securities law or has not acted in the public interest. Costs are not a sanction, but rather a tool for recovery of costs incurred in an investigation and enforcement proceeding.

[53] The Commission seeks costs of $193,333.52 against the respondents jointly and severally. This amount is comprised of $189,647.50 for fees and $3,686.02 for disbursements.

[54] We have reviewed the Commission's bill of costs and have considered the reductions that the Commission has made to its bill of costs. The investigation involved multi-jurisdictional cooperation by regulators, and a significant volume of social media material and YouTube videos to review. The Commission received no cooperation from Nova Tech and Petion, who are not entitled to further reductions in the Commissions costs. We find that the costs requested were fairly and reasonably incurred to investigate Nova Tech and Petion, and to prove the Commission's allegations against them. We order that the respondents jointly and severally pay the Commission $193,333.52 in costs.

[55] For the above reasons, we order that:

a. with respect to the respondents, Nova Tech and Petion:

i. pursuant to paragraph 2 of s. 127(1) of the Act, trading in any securities by the respondents shall cease permanently;

ii. pursuant to paragraph 2.1 of s. 127(1) of the Act, the acquisition of any securities by the respondents is prohibited permanently;

iii. pursuant to paragraph 3 of s. 127(1) of the Act, any exemptions contained in Ontario securities law do not apply permanently to the respondents;

iv. pursuant to paragraph 8.5 of s. 127(1) of the Act, the respondents are permanently prohibited from becoming or acting as a registrant or a promoter;

v. pursuant to paragraph 9 of s. 127(1) of the Act, the respondents shall jointly and severally pay to the Commission an administrative penalty of $2,500,000;

vi. pursuant to paragraph 10 of s. 127(1) of the Act, the respondents shall jointly and severally disgorge to the Commission $31,000; and

vii. pursuant to s. 127.1 of the Act, the respondents shall jointly and severally pay $193,333.52 to the Commission for the costs of the investigation and hearing.

b. with respect to Petion:

i. pursuant paragraph 7 of s. 127(1) of the Act, Petion shall resign any position that she holds as a director or officer of any issuer;

ii. pursuant to paragraph 8 of s. 127(1) the Act, Petion is permanently prohibited from becoming or acting as a director or officer of any issuer;

iii. pursuant to paragraph 8.1 of s. 127(1) of the Act, Petion shall resign any position that she holds as a director or officer of any registrant; and

iv. pursuant to paragraph 8.2 of s. 127(1) of the Act, Petion shall be prohibited permanently from becoming or acting as a director or officer of any registrant.

Dated at Toronto this 3rd day of December, 2024

{1} Nova Tech Ltd (Re), 2024 ONCMT 18 (Merits Decision)

{2} RSO 1990, c S.5

{3} Mertis Decision at para 5

{4} Mertis Decision at para 9

{5} Merits Decision at paras 57-60

{6} Merits Decision at para 52

{7} Bradon Technologies Ltd (Re), 2016 ONSEC 19 at para 27 citing Committee for the Equal Treatment of Asbestos Minority Shareholders v Ontario (Securities Commission), 2001 SCC 37

{8} Norshield Asset Management (Canada) Ltd (Re), 2010 ONSEC 16 at para 73; Mughal Asset Management Corporation (Re), 2024 ONCMT 14 (Mughal) at para 33

{9} Merits Decision at para 44

{10} Merits Decision at para 43

{11} Merits Decision at para 44

{12} Quadrexx Hedge Capital Management Ltd (Re), 2018 ONSEC 3 at para 46

{13} MOAG Copper Gold Resources Inc (Re), 2020 ONSEC 29 (MOAG) at para 57

{14} Merits Decision at para 52

{15} First Globa Data Ltd (Re), 2023 ONCMT 25 at para 86, citing Pro-Financial Asset Management Inc (Re), 2018 ONSEC 18 at para 56; Limelight Entertainment Inc (Re), 2008 ONSEC 28 at para 52

{16} Polo Digital at para 118

{17} Mughal at para 91

{18} Mughal at para 87

{19} 2022 ONCMT 15 (Mek Global) at para 125

{20} Mek Global at para 122

{21} 2022 ONCMT 32 (Polo Digital) at para 134

{22} Polo Digital at para 10

{23} Polo Digital at para 15

{24} Polo Digital at para 132

{25} Polo Digital at para 131

{26} Polo Digital at para 134

{27} MOAG at para 86

CSA Staff Notice 11-312 (Revised) National Numbering System

December 12, 2024{1}

The Canadian Securities Administrators (CSA) follows a system in which securities regulatory instruments are assigned numbers that indicate the type and subject matter of the instrument.

The numbering system was designed so as to:

(i) convey as much information as possible about the particular instrument so that a user knows what type of instrument it is, whether the instrument is national, multilateral or local and what subject matter it relates to;

(ii) permit all National{2} Instruments/Multilateral Instruments, National Policies/Multilateral Policies and CSA Notices to have the same numbers in all jurisdictions (as is currently the case); and

(iii) be flexible enough to permit Local Rules, Policies, Notices and implementing instruments of all jurisdictions to be numbered in accordance with the numbering system without affecting the numbering of National Instruments/Multilateral Instruments, National Policies/Multilateral Policies and CSA Notices{3}.

Under the numbering system, each instrument is assigned a five-digit number, with a hyphen appearing between the second and third digit. There are four components to the number assigned to a document:

• The first digit represents the broad subject area.

• The second digit represents a sub-category of the broad subject area.

• The third digit represents the type of the document.

• The last two digits represent the number of the document within its document type in its sub-category (in sequential order starting at 01).

More specifically, these four components may be described as follows:

• The first digit relates to the subject matter category into which the instrument has been classified. The nine subject matter categories are:

1. Procedures and Related Matters

2. Certain Capital Market Participants (Self-Regulatory Organizations, Exchanges and Market Operations)

3. Registration Requirements and Related Matters (Dealers, Advisers and other Registrants)

4. Distribution Requirements (Prospectus Requirements and Prospectus Exemptions)

5. Ongoing Requirements for Issuers and Insiders (Continuous Disclosure)

6. Take-over Bids and Special Transactions

7. Securities Transactions Outside the Jurisdiction

8. Investment Funds

9. Derivatives

For example, in the context of 54-101, the number "5" indicates that the instrument relates to Ongoing Requirements for Issuers and Insiders.

• The second digit relates to the sub-category of the subject matter category into which the instrument has been classified (see the "sub-category" column of the table below).

Using the 54-101 example, within the Ongoing Requirements for Issuers and Insiders category, a sub-category for instruments dealing with Proxy Solicitation is denoted by the number "4". Accordingly, all instruments dealing with this matter commence with the numbers "54".

• The third digit classifies the document as one of nine types of documents:

1. National Instrument/Multilateral Instrument and any related Companion Policy or Form(s)

2. National Policy/Multilateral Policy

3. CSA Notice

4. CSA Concept Proposal or Discussion Paper

5. Local Rule, Regulation or Blanket Order or Ruling and any related Companion Policy or Form(s), except an Implementing Instrument described below.

6. Local Policy

7. Local Notice

8. Implementing Instrument{4}

9. Miscellaneous

Using the same example, the third digit in 54-101 indicates that the type of instrument is a National Instrument or Multilateral Instrument (or a related Companion Policy or Form).

• The fourth and fifth digits represent a number assigned to instruments of the same type in consecutive order from 01 to 99 within a particular sub-category.

Again, using the example 54-101, the number "01" indicates that the instrument is the first document of its type in the sub-category "Proxy Solicitation".

A Companion Policy or Form that is related to an Instrument or Local Rule will have the same number as the Instrument or Local Rule to which it relates, followed by "F" in the case of a Form. If there is more than one Form related to a particular instrument, the Forms will be numbered consecutively (F1, F2, F3, etc.).

In 2023, the CSA introduced a Coordinated Blanket Order format, which is used to reflect the fact that all or several CSA members are issuing the same (or similar) exemptive relief. The coordinated CSA blanket orders are designated by the third digit (document type) 9, for example, Coordinated Blanket Order 13-932, Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval +. In this number, the first two digits represent the subject matter category and sub-category, the third digit represents the document type (coordinated blanket order), and the last two digits represent the consecutive number assigned to this instrument in this category and document type. Generally, CSA coordinated blanket order numbers will start with xx-930 because the document type number 9 could have been previously used for miscellaneous documents.

Category, Sub-Category and Document Type Numbers

Category |

Sub-Category |

Document Type |

(1st digit) |

(2nd digit) |

(3rd digit) |

|

||

1 -- Procedure and Related Matters |

1 -- General |

1 -- National or Multilateral Instrument (Rule) and any related Companion Policy and Form |

|

2 -- Applications |

|

|

3 -- Filings with Securities Regulatory Authority |

|

|

4 -- Definitions |

|

|

|

2 -- National or Multilateral Policy |

|

5 -- Hearings and Enforcement |

|

|

||

2 -- Certain Capital Market Participants |

1 -- Stock Exchanges |

3 -- CSA Notice or CSA Staff Notice |

|

2 -- Other Markets |

|

|

3 -- Trading Rules |

4 -- CSA Concept Proposal or Discussion Paper |

|

4 -- Clearing and Settlement |

|

|

5 -- Other Participants |

|

|

||

3 -- Registration and Related Matters |

1 -- Registration Requirements |

5 -- Local Rule, Regulation or Blanket Order or Ruling and any related Companion Policy or Form |

|

2 -- Registration Exemptions |

|

|

3 -- Ongoing Requirements Affecting Registrants |

|

|

4 -- Fitness for Registration |

6 -- Local Policy |

|

5 -- Non-Resident Registrants |

|

|

||

4 -- Distribution Requirements |

1 -- Prospectus Contents -- Non-Financial Matters |

7 -- Local Notice |

|

2 -- Prospectus Contents -- Financial Matters |

8 -- Implementing Instrument (Local Rule that gives effect to a National or Multilateral Instrument) |

|

3 -- Prospectus Filing Matters |

|

|

4 -- Alternative Forms of Prospectus |

|

|

|

9 -- A CSA Coordinated Blanket Order or Miscellaneous item (e.g., a Form that does not relate to another Instrument or Policy) |

|

5 -- Prospectus Exempt Distributions |

|

|

6 -- Requirements Affecting Distributions by Certain Issuers |

|

|

7 -- Advertising and Marketing |

|

|

8 -- Distribution Restrictions |

|

|

||

5 -- Ongoing Requirements for Issuers and Insiders |

1 -- Disclosure -- General |

|

|

2 -- Financial Disclosure |

|

|

3 -- Timely Disclosure |

|

|

4 -- Proxy Solicitation |

|

|

5 -- Insider Reporting |

|

|

6 -- Restricted Shares |

|

|

7 -- Cease Trading Orders |

|

|

8 -- Corporate Governance |

|

|

||

6 -- Take-Over Bids and Special Transactions |

1 -- Special Transactions |

|

|

2 -- Take-over Bids |

|

|

||

7 -- Securities Transactions Outside the Jurisdictions |

1 -- International Issuers |

|

|

2 -- Distributions Outside the Jurisdiction |

|

|

||

8 -- Investment Funds |

1 -- Investment Fund Distributions |

|

|

||

9 -- Derivatives{5} |

1 -- General |

|

|

2 -- Trading |

|

|

3 -- Registration and Regulation of OTC Derivatives Market Participants |

|

|

4 -- Clearing and Cleared Derivatives |

|

|

5 -- Uncleared Derivatives |

|

|

6 -- Data Reporting |

|

Questions

Please refer your questions to any of the following people:

Katrina Prokopy |

Sylvia Pateras |

Alberta Securities Commission |

Autorité des marchés financiers |

katrina.prokopy@asc.ca |

sylvia.pateras@lautorite.qc.ca |

|

|

Liliana Ripandelli |

Noreen Bent |

Ontario Securities Commission |

British Columbia Securities Commission |

lripandelli@osc.gov.on.ca |

nbent@bcsc.bc.ca |

|

|

Sonne Udemgba |

Leigh-Anne Mercier |

Financial and Consumer Affairs Authority of Saskatchewan |

Manitoba Securities Commission |

sonne.udemgba@gov.sk.ca |

Leigh-Anne.Mercier@gov.mb.ca |

|

|

Moira Goodfellow |

Doug Harris |

Financial and Consumer Services Commission (New Brunswick) |

Nova Scotia Securities Commission |

Moira.Goodfellow@fcnb.ca |

doug.harris@novascotia.ca |

|

|

Steven Dowling |

Mohammad Bin Mannan Atik |

Government of Prince Edward Island, Superintendent of Securities |

Office of the Superintendent of Securities, Service NL |

sddowling@gov.pe.ca |

MohammadAtik@gov.nl.ca |

|

|

Rhonda Horte |

Matthew Yap |

Office of the Yukon Superintendent of Securities |

Office of the Superintendent of Securities, Northwest Territories |

Rhonda.Horte@yukon.ca |

Matthew_Yap@gov.nt.ca |

|

|

Debora Bissou |

|

Department of Justice, Government of Nunavut |

|

dbissou@gov.nu.ca |

|

{1} This Notice adds information on the numbering of CSA coordinated blanket orders and is a revised version of CSA Staff Notice 11-312, as published on February 6, 2009 and revised on February 19, 2010 and on January 29, 2015.

{2} A National Instrument or Policy is an instrument or policy that has been adopted by all CSA jurisdictions, whereas a Multilateral Instrument or Policy is an instrument or policy that has not been adopted by one or more CSA jurisdictions.

{3} In Québec, all National Instruments, Multilateral Instruments and Rules are referred to as Regulations and all National Policies and Companion Policies are referred to as Policy Statements.

{4} For this purpose, an Implementing Instrument is a local rule making consequential changes relating to the implementation of a National Instrument/Multilateral Instrument.

{5} Please note that in Québec, derivatives regulations are made under the Derivatives Act (Québec) and not the Securities Act (Québec).

OSC Staff Notice 33-757 -- Review of Restricted Dealer Crypto Asset Trading Platforms' Compliance with the Account Appropriateness, Investment Limits and Client Limits Requirements

December 10, 2024

Staff of the Ontario Securities Commission (Staff orwe) conducted a focused compliance review (theSweep) of the know-your-client (KYC), account appropriateness assessment, and Client Limit (defined below) practices of crypto asset trading platforms (CTPs) based in Ontario and registered as restricted dealers. This notice summarizes our findings from the Sweep and provides guidance (including Staff's views as to practices that may be considered to be "suggested practices") to CTPs to assist them in meeting their regulatory obligations (the Notice).

We strongly encourage CTPs to use this Notice to improve their understanding of, and compliance with, their KYC, account appropriateness assessment, and Client Limit obligations. We also suggest that CTPs use this Notice as a self-assessment tool to strengthen their compliance with Ontario securities law.

We expect CTPs to comply with the letter and spirit of the conditions set out in the exemptive relief decisions (Decisions){1} granting them relief from certain securities law requirements, including those conditions related to account appropriateness assessments, investment limits and Client Limits for clients.{2} Among other areas, CTPs are expected to:

• ensure that the maximum amount of crypto assets, excluding Specified Crypto Assets (defined below), that a client, except those clients resident in Alberta, British Columbia, Manitoba, and Quebec, may purchase and sell (calculated on a net basis and is an amount not less than $0) in the preceding 12 months does not exceed the investment limit.

• conduct a meaningful account appropriateness assessment that takes into account the Account Appropriateness Factors (defined below) specific for each client, as described in the Decision.

• assign a Client Limit to each client which considers all the Account Appropriateness Factors and is used to monitor the client's ongoing trading activity.

• ensure actions taken when a client meets or exceeds their Client Limit are timely, meaningful, and proportional to the client's activity to ensure that the client is made aware that their activity is likely subjecting their investments to excessive risk given their individual circumstances.

The following is an outline of this Notice:

• Background

• Purpose of the Sweep

• Account Appropriateness Assessments

• Investment Limits

• Client Limits

• What are Client Limits?

• Determination of Client Limits

• Monitoring & Application of the Client Limits

KYC and suitability determination obligations are fundamental obligations owed by registrants to their clients and are cornerstones of our investor protection regime. As outlined in CSA Staff Notice: 31-336 Guidance for Portfolio Managers, Exempt Market Dealers and Other Registrants on the Know-Your-Client, Know-Your-Product and Suitability Obligations, we expect registrants to comply not only with the letter of the requirements themselves, but also with the spirit of the requirements.

As set out in CSA Staff Notice 21-327 Guidance on the Application of Securities Legislation to Entities Facilitating the Trading of Crypto Assets (Staff Notice 21-327) and Joint Canadian Securities Administrators (CSA) / Investment Industry Regulatory Organization of Canada Staff Notice 21-329 Guidance for Crypto-Asset Trading Platforms: Compliance with Regulatory Requirements (Staff Notice 21-329), securities legislation applies to CTPs that facilitate or propose to facilitate the trading of instruments or contracts involving crypto assets because the user's contractual right to the crypto asset may itself constitute a security and/or a derivative (Crypto Contract).

Exemptive relief from the prospectus requirement has been granted to allow registered CTPs to purchase, hold, stake, deposit, withdraw and sell crypto assets for clients through Crypto Contracts. In addition, certain registered CTPs that do not provide recommendations or advice to clients, or do not conduct trade-by-trade suitability determination for clients, have been granted exemptive relief from the trade-by-trade suitability determination requirements under section 13.3 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103). As a condition of the relief, among others, CTPs are required to perform account appropriateness assessments (see Account Appropriateness Assessments below), and apply investment limits (see Investment Limits below) and Client Limits (see Client Limits below).

Staff conducted a Sweep of six registered CTPs whose principal regulator is the Ontario Securities Commission, to assess their compliance with the terms and conditions of their Decisions. These terms and conditions included obligations in the following areas:

• custody arrangements over clients' crypto assets,

• account appropriateness of client accounts, or suitability determination, for trading in Crypto Contracts,

• corporate governance structures,

• insurance bonding policies, and

• management of material conflicts of interest.

Four of the six registered CTPs obtained relief from the trade-by-trade suitability determination requirement in section 13.3 of NI 31-103 and were conducting account appropriateness assessments (account appropriateness model). The remaining two CTPs did not obtain relief from the suitability determination requirements and were subject to the trade-by-trade suitability determination for clients, including the enhanced suitability requirements as a result of the client-focused reforms in respect of s. 13.3 of NI 31-103 (suitability model).

The purpose of the Sweep was to:

• review and assess the CTPs' compliance with KYC and account appropriateness or suitability determination obligations (as applicable),

• enhance Staff's knowledge regarding CTPs' compliance with KYC, account appropriateness assessments or suitability determination obligations, and to determine whether there is a need for additional guidance, and

• highlight to registered CTPs and those applying for registration, the importance of these obligations and improve the level of compliance and investor protection.

This Notice will focus on our findings from the Sweep and provide guidance to CTPs to assist them in meeting their regulatory obligations in the areas of account appropriateness assessments, investment limits, and Client Limits.

For guidance on our findings from the other areas reviewed as part of the Sweep, please refer to our Summary Report for Dealers, Advisers and Investment Fund Managers under OSC Staff Notice 33-755 and OSC Staff Notice 33-756.

CTPs operating under the account appropriateness model are required to consider all the following factors (the Account Appropriateness Factors) in conducting the account appropriateness assessment:

(i) the client's experience and knowledge in investing in crypto assets

(ii) the client's financial circumstances

(iii) the client's risk tolerance

(iv) the crypto assets approved to be made available to a client on the platform

Pursuant to the conditions of their exemptive relief, CTPs must perform an account appropriateness assessment prior to opening a client account, on an ongoing basis, and at least every twelve months. The account appropriateness assessment should be performed more frequently than every twelve months if there is a significant change in a client's circumstances or a significant change in market conditions.

To meet the account appropriateness assessment obligation, CTPs are expected to take reasonable steps to collect information and establish the Account Appropriateness Factors for each prospective client. CTPs may use an onboarding questionnaire and any such questionnaire should be developed and designed with this in mind. CTPs should use the collected information to conduct a meaningful account appropriateness assessment using all the Account Appropriateness Factors for each client and determine whether it is appropriate for the CTP to enter into a Crypto Contract with the client.

During the Sweep, Staff found instances where a CTP took a mechanical "tick box" approach to collecting Account Appropriateness Factors without following up on any inconsistencies or otherwise conducting a meaningful assessment of the Account Appropriateness Factors. In addition, Staff observed that some CTPs did not update clients' Account Appropriateness Factors on an ongoing basis, thereby assessing account appropriateness on outdated information. These failures sometimes resulted in accounts being opened or maintained for clients where the account was not appropriate for the client.

In circumstances where the CTP has determined that entering into a Crypto Contract with and opening an account for the client is not appropriate, this should be clearly communicated to the client and the CTP should not open an account for the client at that time. In addition, CTPs should establish policies and procedures for handling situations where the CTP has determined that it is not appropriate for the prospective client to open an account, including preventing a client from gaming the onboarding process.

In reference to record keeping, CTPs must maintain books and records that evidence any changes in a client's information (or a confirmation that there are no changes). In addition, CTPs should establish policies and procedures for collecting, documenting, and reviewing information necessary to conduct a meaningful account appropriateness assessment.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Suggested practices for conducting the account appropriateness assessment:

• Develop and design any onboarding questions to meaningfully capture the Account Appropriateness Factors for each prospective client. CTPs should follow up with the client where any inconsistencies are identified in the information collected.

• Conduct a meaningful account appropriateness assessment, rather than a mechanical "tick box" approach, that considers all the Account Appropriateness Factors for each client at the onboarding stage and on an ongoing basis.

• Update their account appropriateness assessment for each client at least annually or more frequently if there is a significant change in a client's circumstances or a significant change in market conditions.

• Maintain books and records that evidence any changes in a client's information (or a confirmation that there are no changes).

• Establish policies and procedures for collecting, documenting, and reviewing information necessary to conduct a meaningful account appropriateness assessment.

• Establish policies and procedures for handling situations where the CTP has determined that it is not appropriate for the prospective client to open an account, including preventing a client from gaming the onboarding process

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Except for clients resident in Alberta, British Columbia, Manitoba and Québec, and permitted clients (as defined under NI 31-103), CTPs must limit a client's purchases of crypto assets (that are not Specified Crypto Assets{3}) to a maximum amount on the CTP's platform. This is referred to as the investment limit.

For CTPs operating under the account appropriateness model, the maximum amount of crypto assets that a client may purchase and sell (calculated on a net basis) in the preceding 12 months must not exceed a net acquisition cost of $30,000.

For CTPs operating under the suitability model, the maximum amount of crypto assets that a client may purchase and sell (calculated on a net basis) in the preceding 12 months must not exceed:

• $30,000 for a client that does not meet the definition of an eligible crypto investor,

• $100,000 for a client that meets the definition of an eligible crypto investor, and

• no investment limit for a client that meets the definition of an accredited crypto investor.

The investment limit cannot be less than $0 and excludes purchases and sales of Specified Crypto Assets.

During the Sweep, Staff did not identify any instances where CTPs failed to discharge their obligation to limit a client's purchases of crypto assets (that are not Specified Crypto Assets) to the applicable maximum amount on the CTP's platform.

CTPs operating under the account appropriateness model are required to establish Client Limits as a condition of their Decision{4}:

...[t]he Filer has adopted and will apply policies and procedures to conduct an assessment to establish appropriate limits on the losses that a Client can incur, what limits will apply to such Client based on the Account Appropriateness Factors (the Client Limit), and what steps the Filer will take when the Client approaches or exceeds their Client Limit. This assessment of the Client Limit takes into consideration the Account Appropriateness Factors. After completion of the assessment, the Filer will implement controls to monitor and apply the Client Limits.

Referred to as the loss limit in some earlier Decisions, the purpose of the Client Limit is to mitigate the risk of clients incurring significant realized and unrealized losses while trading in Crypto Contracts on CTPs (the Client Limit). It is meant to:

• be an appropriate and tailored limit on the losses that a client can incur,

• help clients understand the losses they have incurred to date on their investments in Crypto Contracts, and

• initiate meaningful action to help limit further losses the client can incur.

It is also used to help deter "gambling-like" or excessively risky actions taken by clients when losses are experienced, such as "doubling down" on existing crypto asset positions.

When assigning a Client Limit for each client, the CTP is required to consider all Account Appropriateness Factors of the respective client and determine a Client Limit that is appropriate for the client in light of their individual circumstances.

During the Sweep, however, Staff noted numerous instances where CTPs assigned Client Limits that were not meaningfully tailored to each client's individual circumstances. For example:

• Client Limit was determined based on consideration of only one or a few Account Appropriateness Factors. For example, Staff noted that some firms used risk tolerance as the sole Account Appropriateness Factor in determining a tailored Client Limit, which does not provide a complete picture of the client's circumstances.

• Client Limit was based on arbitrary and dynamic factors such as (a) a specific change in the trailing price of each crypto asset offered by the CTP (e.g., 20% drop in the price of Bitcoin over a trailing 60-day period), (b) a specific change in the market value of a client's portfolio, or (c) a specific change in the market value of a client's portfolio relative to the adjusted book value of a client's crypto asset holdings (e.g., market drop causing a 20% (un)realized loss calculated using a client's adjusted book value).

In Staff's view, such approaches do not appropriately consider and reflect the client's ability to tolerate losses and are not meaningfully tailored to each client's individual circumstances.

To comply with the conditions of the Decisions, CTPs should assign Client Limits that are tailored to each client based on the respective client's Account Appropriateness Factors (e.g., setting a dollar amount that reflects what the client can afford to lose, which may be expressed as a percentage of the client's net financial assets).

During the Sweep, Staff also found instances where CTPs did not effectively monitor the Client Limits or perform any meaningful action once a Client Limit was met or exceeded. In those instances, clients were able to freely pursue further transactions after exceeding their Client Limit, without any meaningful action taken by the CTPs to deter further losses.

As a condition of the Decisions, CTPs are required to monitor clients' accounts against their Client Limit. As the client begins to incur losses, this should trigger progressive layers of intervention by the CTP to help warn the client that they are approaching their Client Limit and notify the client of their accumulated losses to date. Staff do not expect trading activity for the client to be immediately blocked or limited as they approach their Client Limit.

If the Client Limit is reached, the CTP should inform the client and provide them with appropriate tools to mitigate further losses. Staff expect this deterrence to be proportionate to the losses incurred by the client with the expectation that the CTP would inform the client that further trading activity may be detrimental and provide steps the client should consider. Part of this deterrence may include temporarily limiting activities related to pursuing further transactions in Crypto Contracts given the losses incurred to date. CTPs should also conduct a reassessment on whether the account remains appropriate for the client.

Client notifications should be timely to ensure that clients are made aware of the losses they have incurred to date relative to their Client Limit. Clients that continue to exceed their Client Limit should continue to receive notifications intermittently to meaningfully make clients aware of their losses. However, CTPs should ensure the notifications are not so frequent (e.g., daily) that the clients disregard the persistent notifications.

As a condition of the Decisions, CTPs cannot provide recommendations or advice to any client or prospective client. Thus, CTPs should refrain from using language in the notifications that may be construed as advice. Notifications should be used to point to the losses accumulated to date at the time of the notification and educate clients on how they can reduce further losses.

The design of an appropriate Client Limit system should ensure that the outcomes taken as a client approaches, meets, or exceeds their Client Limit makes the client aware of their accumulated losses and reassesses the client's appropriateness for continued trading in Crypto Contracts. CTPs are expected to demonstrate on a reasonable efforts basis that meaningful interventions have been added to protect clients in situations where their losses on the platform appear to be disproportionately detrimental relative to their individual circumstances.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Suggested practices for a Client Limit system:

• Develop an onboarding process to collect sufficient information to allow the CTP to develop an appropriate Client Limit for each client.

• Consider all Account Appropriateness Factors to understand the client's individual situation and assign an appropriate Client Limit during the onboarding process and on an ongoing basis. One factor alone is not sufficient to obtaining an understanding of the client's individual situation and properly evaluating an individual Client Limit as required under the Decision.

• Establish a Client Limit that considers the client's individual situation and is based on a dollar value which can be used in monitoring the client's ongoing trading activity. Using a value or calculation for the Client Limit that does not consider all the client's Account Appropriateness Factors and is based on elements that dynamically change does not result in a meaningful consideration of the client's individual situation.

• Make sure language contained in the Client Limit notifications makes the client aware that their current trading activity is approaching their Client Limit and direct them to educational materials on the risks of excessive trading. Refrain from using language in Client Limit notifications that conveys any messaging that could be construed as advice.

• Monitor the Client Limit based on the trading activity of the client and take appropriate actions when a client meets or exceeds their Client Limit, including:

• issuing timely and meaningful notifications to the client, and

• making sure any action taken is proportional to the client's activity and that the client is aware their activity to date is putting the client at excessive risk.

• Ensure adequate policies and procedures are in place to evaluate, monitor and apply the Client Limit to individual clients as required by the terms of their Decision.

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

The suggested practices identified in this Notice are intended to provide additional Staff guidance on how we expect CTPs to comply with the conditions related to account appropriateness, investment limits and Client Limits in the Decisions. CTPs are encouraged to use this Notice as a self-assessment tool to assess their compliance with these obligations and make any appropriate adjustments to their compliance program.

Staff will continue to monitor CTPs' compliance with the conditions of their respective Decisions alongside compliance with other fundamental registrant obligations in securities legislation. Where instances of non-compliance are noted, we will take appropriate action.

If you have any questions regarding this Notice, please refer them to any of the following:

Vincent Chow |

George Rodin |

Senior Accountant |

Senior Accountant |

Registration, Inspections and Examinations |

Registration, Inspections and Examinations |

vchow@osc.gov.on.ca |

grodin@osc.gov.on.ca |

|

|

Michael Man |

Namrata Bhagia |

Senior Accountant |

Legal Counsel |

Trading and Markets |

Trading and Markets |

mman@osc.gov.on.ca |

nbhagia@osc.gov.on.ca |

|

|

Jennifer Lee-Michaels |

|

Senior Legal Counsel |

|

Trading and Markets |

|

jleemichaels@osc.gov.on.ca |

|

{1} Available at https://www.osc.ca/en/industry/registration-and-compliance/registered-crypto-asset-trading-platforms.

{2} See Joint Canadian Securities Administrators/Investment Industry Regulatory Organization of Canada Staff Notice 21-329 Guidance for Crypto-Asset Trading Platforms: Compliance with Regulatory Requirements https://www.osc.ca/sites/default/files/2021-03/csa_20210329_21-329_compliance-regulatory-requirements.pdf.

{3} As of the date of this Notice, these assets include Bitcoin, Ether, Bitcoin Cash, Litecoin, and Value-Referenced Crypto Assets that comply with the conditions as set out in the CTP's Decision (the Specified Crypto Assets).

{4} While the wording presented may have slight variations between Decisions, the general premise and context have not changed as of the writing of this Staff Notice.

Ontario Securities Commission Staff Notice 51-736 -- Corporate Finance Division 2024 Annual Report

Ontario Securities Commission Staff Notice 51-736 Corporate Finance Division 2024 Annual Report is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

OSC Staff Notice 51-736

Corporate Finance Division

2024 Annual Report

December 6, 2024

Message from the Senior Vice President

We are pleased to share our first annual report as the Corporate Finance Division (Division). The Report provides an overview of our operational and policy work for the 2023-2024 fiscal year and guidance about our expectations and interpretation of regulatory requirements in certain areas.

In May 2024, the OSC released its six-year Strategic Plan setting out its vision of working together to make Ontario's capital markets inviting, thriving and secure. This vision is underpinned by six strategic goals that set out a robust response to changes in today's capital markets including rapid technological innovation, changing investor demographics, and shifting preferences in how investors interact with our market. The OSC is taking important steps to become a more agile, responsive and proactive regulator.

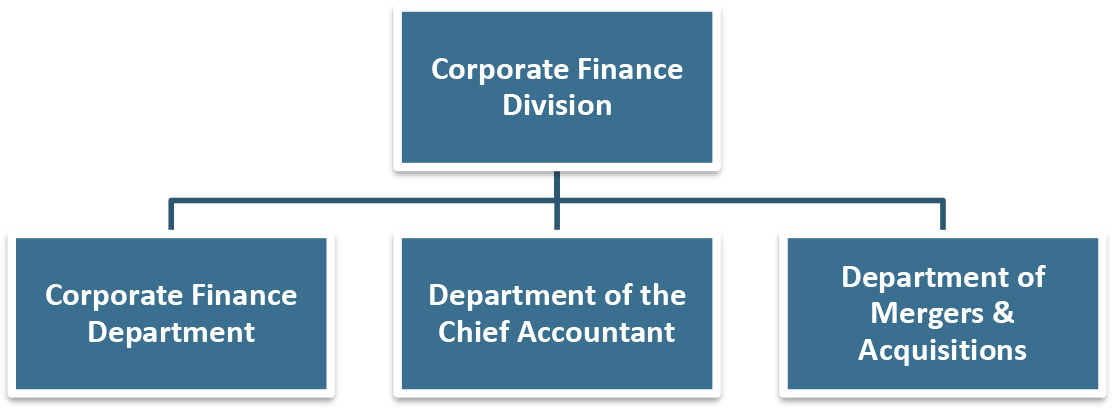

With the plan's strategic goals in mind, three operating departments -- Corporate Finance, the Chief Accountant (led by Cameron McInnis, Chief Accountant) and Mergers & Acquisitions (led by Jason Koskela, Vice President) -- now form the Division. The Division remains focused on improving the transparency, trustworthiness and efficiency of capital markets through our regulatory oversight of Ontario's reporting issuers and other important market participants.

Throughout fiscal 2023-2024, the Division, with its partners in the Canadian Securities Administrators, continued to advance its policy work, including projects related to climate disclosures, prospectus exemptions to promote capital formation and reducing regulatory burden.

These initiatives continue to be part of the Division's main policy focus in fiscal 2025. In addition, we continue to monitor and consider new market trends and potential areas of concern that may warrant a regulatory response.

We hope that this report provides insight into our work during the past year and the work we will conduct under our newly implemented structure. Further, we hope that the report serves as a guide to better understand disclosure and other regulatory obligations under applicable Ontario securities law. We welcome any questions or feedback that you may have.

Best regards,

Table of Contents

Fiscal 2024 Snapshot |

4 |

||

|

|||

Introduction |

5 |

||

|

|||

Corporate Finance Division: Who We Are & What We Do |

5 |

||

|

|||

Part A: Corporate Finance Department |

8 |

||

1. |

Continuous Disclosure Review Program |

9 |

|

|

A) |

CDR Program outcomes for Fiscal 2024 |

10 |

|

B) |

Trends and Guidance |

13 |

2. |

Other Ongoing Regulatory Oversight |

27 |

|

|

A) |

Financial Benchmarks and Designated Rating Organizations |

27 |

|

B) |

Exempt Market Reviews |

27 |

3. |

Public Offerings |

29 |

|

|

A) |

Trends and Guidance |

29 |

4. |

Exemptive Relief Applications |

36 |

|

|

A) |

Trends and Guidance |

36 |

5. |

Insider Reporting |

38 |

|

|

|||

Part B: Department of the Chief Accountant |

39 |

||

|

|||

Part C: Department of Mergers & Acquisitions |

44 |

||

|

|||

Part D: Responsive Regulation |

52 |

||

|

|||

Part E: Resources |

57 |

||

|

|||

Appendix A -- Glossary |

60 |

||

* Note: all figures are as at / for Fiscal 2024 and are approximate or rounded.

** Includes public offerings and private placements of equity and convertible debentures.

This Corporate Finance Division 2024 Annual Report (Report) provides an overview of the Division's operational and policy work during the fiscal year ended March 31, 2024 (Fiscal 2024), including a summary of key findings and outcomes from our regulatory oversight programs and a status report of ongoing Issuer-related policy initiatives. The report is intended for entities and individuals we regulate, their advisors, as well as investors.

In publishing this report we aim to

• REINFORCE the importance of complying with regulatory obligations;

• PROVIDE GUIDANCE to improve compliance;

• HIGHLIGHT trends in the capital markets; and

• INFORM AND UPDATE stakeholders on new and ongoing policy initiatives.

Corporate Finance Division: Who We Are & What We Do

Through our oversight role, we support the OSC's goal to improve transparency, trustworthiness,

and efficiency in Ontario's capital markets.

The Corporate Finance Division comprises the following three departments:

The Corporate Finance Department focuses on the oversight of Reporting Issuers in Ontario. To do this, our operational work includes:

• assessing, using risk-based criteria, whether Reporting Issuers in Ontario are providing the required level of disclosure of material information to investors so they can make informed investment decisions, including through the review of

• public offerings of securities;

• capital raising activities in the exempt market;

• continuous disclosure (CD) filed by Reporting Issuers;

• reviewing and considering applications for exemptive relief from regulatory requirements;

• responding to inquiries and complaints;

• reviewing insider reporting;

• reviewing credit rating agencies that are designated rating organizations;

• overseeing designated benchmarks and benchmark administrators;

• overseeing the listed Issuer function for OSC-recognized exchanges;

• engaging with stakeholders, including external advisory committees;

• providing guidance to stakeholders through staff notices that communicate expectations and interpretations of regulatory requirements in certain areas; and

• delivering Issuer education and outreach programs.

The Department of the Chief Accountant (DCA) provides advisory services relating to accounting and assurance for all divisions in the OSC and is involved with policy initiatives focussed on financial reporting. The DCA also engages with various external stakeholders that are involved with financial reporting, including standard setters, audit regulators, and professional accounting firms.

Its operational work includes:

• overseeing securities rules and regulations related to financial reporting frameworks (e.g., IFRS Accounting Standards);

• providing advisory services to the OSC for complex accounting or assurance issues;

• advising the OSC on the impact of new financial reporting developments; and

• engaging with external stakeholders on significant financial reporting matters.

The Department of Mergers and Acquisitions (DM&A) is responsible for the regulation of mergers and acquisition (M&A) transactions and the unique risks faced by shareholders in evolving capital markets. The department focuses on take-over bid requirements, issuer bid requirements, early warning requirements, conflict of interest transactions, defensive tactics and minority shareholder rights.

Its operational work includes:

• real-time monitoring and supervising M&A transactions;

• responding to complaints regarding M&A transactions;

• responding to inquiries;

• reviewing and considering exemptive relief applications;

• participating in M&A hearings, including making submissions and working with parties to narrow issues and navigate procedural matters; and

• engaging with stakeholders on emerging trends and policy issues.

1. Continuous Disclosure Review Program

2. Other Ongoing Regulatory Oversight

3. Public Offerings

4. Exemptive Relief Applications

5. Insider Reporting

This section provides an overview of the key findings and outcomes from our Fiscal 2024 continuous disclosure review program (CDR Program). We discuss key or novel issues, suggest best practices, and specify applicable legislation and relevant guidance to assist Issuers in addressing each of the topic areas.

Under Ontario securities law, a Reporting Issuer must provide timely and periodic CD about its business and affairs. The CDR Program seeks to assess whether Reporting Issuers are complying with disclosure obligations and to identify material deficiencies that may affect the reliability and accuracy of a Reporting Issuer's disclosure record. For further information about the CDR Program, refer to CSA Staff Notice 51-312 and our website.

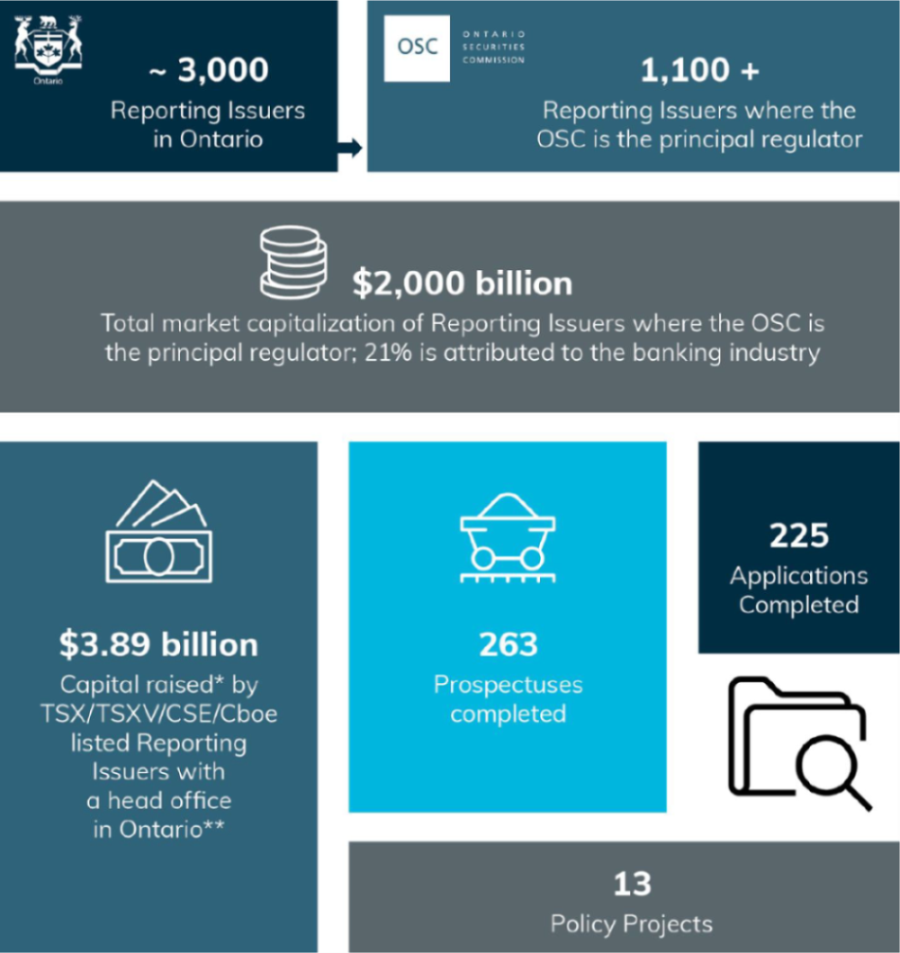

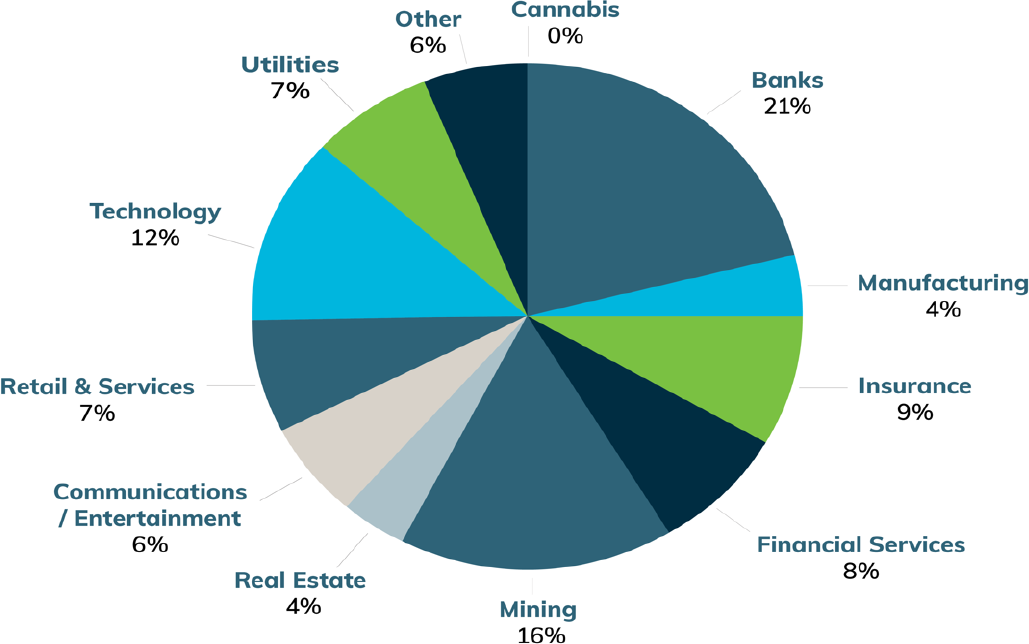

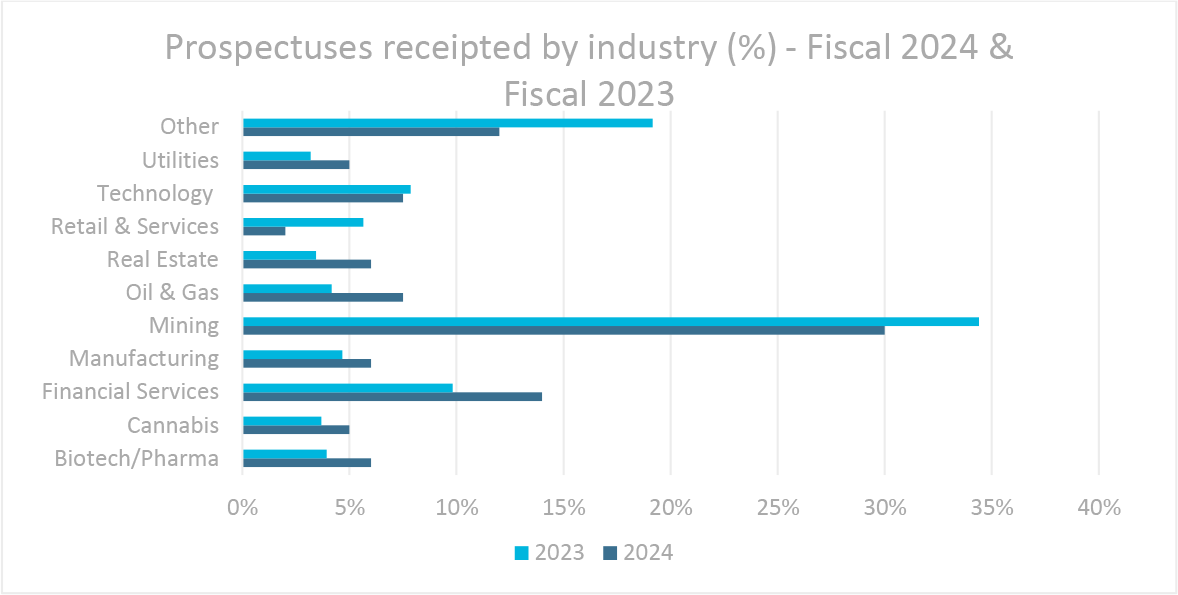

The Division has primary responsibility as principal regulator{1} over approximately 1,100 Reporting Issuers with an aggregate market capitalization of approximately $2,000 billion as at March 31, 2024. The three largest industries by market capitalization were banking, mining, and technology.

Market capitalization of Ontario Reporting Issuers by industry as at March 31, 2024

Our CDR Program is risk-based and outcome-focused. It includes planned full reviews and issue- oriented reviews (IORs) based on risk criteria as well as ongoing monitoring through news releases, media articles, complaints, and other sources. The CDR Program is conducted pursuant to the powers in subsection 20.1(1) of the Securities Act (Ontario) (Act) and is part of a harmonized CDR Program conducted by the CSA.{2}

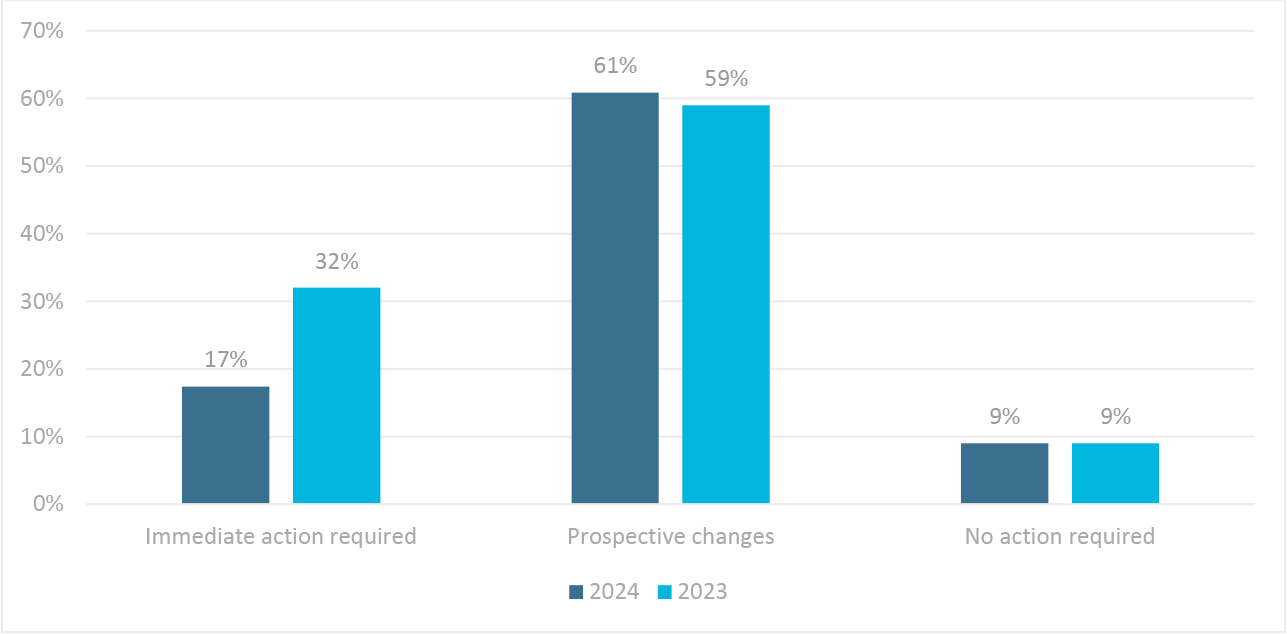

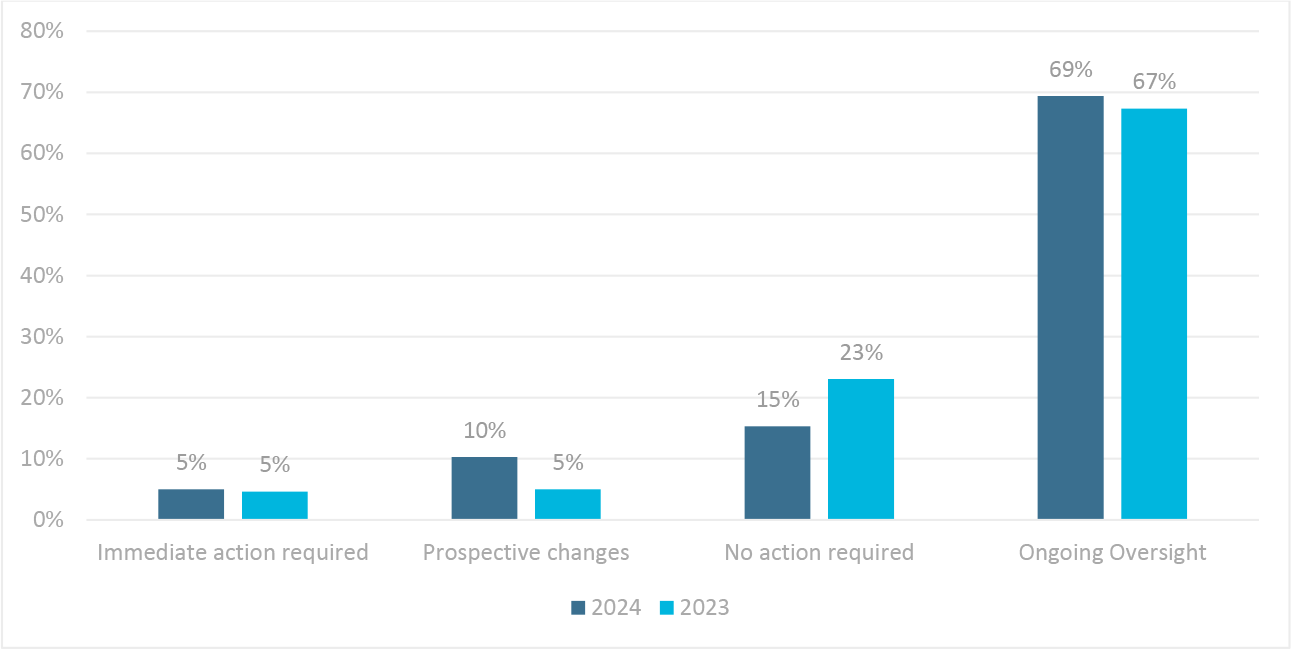

We track several categories of outcomes of the CDR Program:

• Immediate corrective action is required

• Includes the refiling of a previously filed CD document or the filing of a document that should have been previously filed, a referral to the Enforcement division or the issuance of a cease trade order.

• Prospective enhancements are required

• Changes or enhancements are required in the next filing as a result of deficiencies identified but they do not rise to the level of immediate action.

• No action is required

• Instances where the Issuer does not need to make any corrective changes or additional filings as a result of our review.

• Ongoing Oversight

• This type of outcome is specific to IORs where we conduct an initial high-level review of a Reporting Issuer's disclosure to determine whether direct engagement with the Reporting Issuer is required or conclude that no further action is required. Examples of this type of IOR include our ongoing monitoring of Reporting Issuers and the regular high-level reviews of technical reports filed on SEDAR+ which are intended to monitor disclosure compliance in real-time with the requirements of NI 43-101 and Form 43-101F1. Similarly, reviews triggered by significant industry developments fall into this category of IORs. If potentially significant disclosure deficiencies are identified, a formal IOR file will be opened, and we will engage with the Reporting Issuer.

• These types of IORs enable us to take a staged approach to CD reviews and more efficiently allocate staff resources in a timely manner.