Ontario Securities Commission Bulletin

Issue 47/17 - April 25, 2024

Ont. Sec. Bull. Issue 47/17

• Trilogy International Partners Inc.

• Polaris Financial Inc. and Quintessence Wealth

• Ninepoint Partners LP and Canadian Large Cap Leaders Split Corp.

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

FOR IMMEDIATE RELEASE

April 22, 2024

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated April 22, 2024 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

April 23, 2024

TORONTO -- A case management hearing in the above-named matter is scheduled to be heard on April 23, 2024 at 4:30 p.m. by videoconference.

Members of the public may observe the hearing by videoconference, by selecting the "Register to attend" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

For Media Inquiries:

For General Inquiries:

File No. 2022-19

Adjudicators: |

Andrea Burke (chair of the panel) |

James Douglas |

|

Cathy Singer |

April 22, 2024

WHEREAS on April 19, 2024, the Capital Markets Tribunal concluded the evidentiary portion of the merits hearing in this proceeding;

ON HEARING the submissions of the representatives for the Ontario Securities Commission, TeknoScan Systems Inc., Philip Kai-Hing Kung and Soon Foo (Martin) Tam, and of H. Samuel Hyams, appearing on his own behalf;

IT IS ORDERED THAT:

1. the Commission shall serve and file written closing submissions on the merits by 4:30 p.m. on May 14, 2024;

2. each of the respondents shall serve and file written closing submissions on the merits by 4:30 p.m. on May 28, 2024; and

3. oral closing submissions on the merits shall be heard on May 31, 2024, at 10:00 a.m. at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, or as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

A Post-Implementation Review of the Impacts of the CRM2 Annual Costs and Performance Reports on Investment Fund Fees and Performance

The Executive Summary, A Post-Implementation Review of The Impacts of The CRM2 Annual Costs and Performance Reports on Investment Fund Fees, and A Post-Implementation Review of the Impacts of the CRM2 Annual Costs and Performance Reports on Investment Fund Performance, are reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the reports.

The CSA has undertaken research to examine the post-implementation impacts of the final phase of the Client Relationship Model (CRM2) amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (herein after the CRM2 annual costs and performance reports) on industry and investor behaviour.

The final amendments, which came into effect on July 15, 2016, were designed to ensure investors receive clear and complete annual disclosure of both the performance of their investments and of all fees associated with their accounts, including registrant compensation. The detailed findings of this research are presented in the following reports{1}:

• A Post-Implementation Review of The Impacts of The CRM2 Annual Costs and Performance Reports on Investment Fund Fees (Fees Report)

• A Post-Implementation Review of the Impacts of the CRM2 Annual Costs and Performance Reports on Investment Fund Performance (Performance Report)

This document provides a high-level summary of the research findings. The findings presented in this executive summary and the research reports are the views of CSA staff and are for informational purposes only. As such, statements made in these documents do not represent the CSA's views of any official policy position.

The increased disclosure of fees and performance brought about by the CRM2 amendments is expected to have enabled retail investors to make better investment decisions and promoted efficient markets. As a result, we hypothesize that this greater transparency has led to more competitive fund pricing and higher performance by investment funds.

To test our hypothesis, we undertook a study to examine whether the enhanced reporting of investment cost and performance led to changes in mutual fund and exchange-traded fund (ETF) fees{2}, product creation, product distribution, and fund performance.

In particular, we asked:

1. Have investment fund managers (IFMs) lowered fees, specifically management expense ratios (MER) and management fees, and what is the extent of these changes?

2. Have product manufacturers and product distributors been shifting to products that are not captured by the new account costs and performance disclosures?

3. What have been the changes in product creation and distribution trends?

4. Has greater transparency about investment returns led to IFMs improving the risk-adjusted performance of their mutual funds and ETFs?

The research covers January 2013 to December 2020. This time period begins about 18 months before the first set of CRM2 amendments came into effect on July 15, 2014 (cost disclosures related to pre-trade disclosure of charges, and trade confirmation for debt securities). The 2013 start date gives us a baseline for the investment fund industry before the first set of CRM2 amendments were implemented. We hypothesize that the changes we are seeking to measure took place several years after the CRM2 annual costs and performance reports were fully implemented. Considering this, the study timeline extends to 2020 to account for this time lag, enabling us to more fully observe the extent of any changes. Our analysis groups the findings into three time periods: 2013 to 2020, which is the overall duration of our study period, the pre-implementation period of 2013 to 2016 and the post-implementation period of 2017 to 2020.

The research findings suggest that overall industry behaviour has been shifting in directions that are consistent with our hypothesis on the impact of the CRM2 regulations. This helps provide evidence that disclosure-based regulations may be an effective tool in changing industry and investor behaviour.

Our findings provide important directional trends (i.e., correlation rather than cause and effect outcomes). It is possible that other factors, which we could not practically account for in our analysis, also contributed to the changes we are highlighting.

We caution readers from drawing conclusions that the changes presented in this report were caused solely by the CRM2 annual costs and performance reports.

Research question 1: Have investment fund managers (IFMs) lowered fees, specifically MERs and management fees, and what are the extent of these changes? |

There were declines in the asset-weighted average MERs and management fees, for both mutual funds and ETFs, during our study period, and the extent of these changes varied by investment fund type and fund characteristics.{3},{4}

Overall, the asset-weighted average MER declined by 38 basis points (or 19%) over 2013-2020 for our study sample, and between 13 and 49 basis points, or between 6% and 30%, across the main fund characteristics examined.{5} The size of the asset-weighted average management fee declines was smaller, at 29 basis points for the overall study sample and ranged from 6 to 39 basis points across the main fund characteristics, or between 4% and 32%.

Changes in the asset-weighted average MERs and management fees were generally greater during the post-implementation period than the pre-implementation period. Declines in the asset-weighted average MERs and management fees across the fund characteristics examined ranged from 3 to 19 basis points, or 2% to 15%, for both time periods.

Both shifts in the distribution of assets towards mutual fund series with lower fees, and reductions in series' MERs and management fee rates, contributed to lowering the asset-weighted average MERs and management fees.{6}

However, shifts in the distribution of assets had a larger effect than reductions in MER/management fee rates in lowering the aggregate asset-weighted average MERs/management fees for both time periods.

ETFs, compared to mutual funds, had smaller declines in their asset-weighted average MERs and management fees during our study period. This finding was anticipated since the MERs and management fees for most ETFs started from a lower baseline level. This is primarily because the majority of ETF assets are invested in funds that employ a passively managed investing strategy.

By the end of our study period in 2020, the asset-weighted average MER for our study sample had declined by 8 basis points (or 21%) from 2013 levels, and between 6 and 11 basis points or between 12% and 34%, depending on the fund characteristic examined. The decrease in the overall asset-weighted average management fee was 7 basis points (22%) between 2013 and 2020. Across the main fund characteristics, the declines in asset-weighted averages ranged from 3 to 10 basis points, or 5% to 34%.

Changes in the asset-weighted average MERs and management fees during both the pre- and post-implementation periods ranged from +1 to -8 basis points or +1% to -19% across the fund characteristics examined. There were no strong directional trends in the asset-weighted average MER/management fee declines by fund characteristics. Both changes in the distribution of assets and reductions in MERs and management fee rates had a broadly similar contribution to lowering the asset-weighted average fees, in both the pre- and post-implementation periods.{7}

Research question 2: Have product manufacturers and product distributors been shifting to products that are not captured by the new account costs and performance disclosures? |

Our analysis of Canadian household discretionary financial assets did not show a trend of discretionary financial assets moving towards products not captured by the CRM2 annual costs and performance report requirements.{8}

Between 2013 and 2020, the share of discretionary financial assets held in deposits remained stable at 27%. Meanwhile, the share of assets in non-investment fund securities increased slightly, from 25% to 26%, and the share of assets in investment funds increased from 28% to 32%. For investment funds, the 4 percentage point share increase was the result of growing market shares for mutual funds and ETFs.

Research question 3: What have been the changes in product creation and distribution trends, generally? |

Five notable changes in product creation and distribution occurred during our study period. Unless otherwise noted, the findings and figures discussed below are for the overall industry and are not only for our study sample.

The continued popularity of fund wrap programs contributed to a rise in the number of fund-of-funds products, for both mutual funds and ETFs{9}. This was evident in the shift of assets away from stand-alone funds to fund-of-funds products. In 2013, 26% of mutual fund assets were in fund-of-funds products and by 2020 this figure had increased to 37%. One of the largest ETF manufacturers introduced ETF-of-ETFs products in early 2018. By December 2020, ETF-of-ETFs products accounted for $6 billion or 2% of the total industry ETF assets.

Growth of the ETF market was evident during our study period, and the growth rate for ETFs substantially surpassed the growth rate for mutual funds. Between 2013 and 2020, the annual growth in the number of ETFs was 17% while it was 2% for mutual funds.

Within ETF creation, one of the most significant changes that occurred during our study period was the rise of actively managed and strategic beta ETFs.{10} Near the start of our study period, actively managed and strategic beta ETFs accounted for 23% and 17% of the number of ETFs according to data from Investor Economics. By December 2020, their respective share rose to 43% and 21%. The rise in the number of strategic beta ETFs did not lead to a corresponding rise in ETF assets in that category of funds. In contrast, the share of ETF assets in actively managed ETFs increased from 9% at the start of our study period, to 24% by the end of our study period.

Within the mutual fund market, the shift from commission-based to fee-based series was pronounced during our study period. Between 2013 and 2020, the number of fee-based series increased by 186%, from 2,592 to 7,404. In comparison, the number of commission-based "A-series," which is the "core" mutual fund series, increased by 103% from 2,887, in 2013, to 5,880, in 2020.

Looking at our study sample, we found that 6% of mutual fund assets were in fee-based series at the start of our study period in 2013. This figure increased to 27% by the end of our study period in 2020. The growth and shift of assets into fee-based series corresponded with declining assets in commission-based A-series. In 2013, 75% of our study sample assets were in A-series and by 2020 this figure had declined to 58%.

A product creation trend that occurred towards the end of our study period was the rise of and demand for funds with an environmental, social, and governance (ESG) mandate. There were 49 mutual funds with an ESG mandate in 2013 and these funds had assets of $5.1 billion. By 2020, the number of mutual funds with an ESG mandate almost doubled to 97 funds. The number of ETFs with an ESG mandate grew from 10 in 2018, to 50 by 2020. Despite the significant increase in the number of funds with an ESG mandate, their share of total industry assets is small. In 2020, funds with an ESG mandate accounted for around 1% of total industry assets within the mutual fund and ETF markets, respectively.

A new direct to investor/consumer distribution channel emerged in 2014 with the launch of four online advice platforms -- Wealthsimple, Wealth Bar, NestWealth, and Questwealth Portfolios. These platforms provide retail investors with access to discretionary asset management services with no or low account size minimum requirements. These platforms invest client assets primarily in ETFs, and to a lesser extent in mutual funds, other redeemable investment funds, cash, and cash equivalents.{11} By the end of 2020, 22 online advisers operated in Canada. These firms had an estimated $10 billion in assets under management, which is equivalent to about 4% of the industry total assets for ETFs.

Research question 4: Has greater transparency about investment returns led to investment fund managers improving the risk-adjusted performance of their mutual funds and ETFs? |

On balance, we find that the risk-adjusted performance relative to our model's benchmark for both mutual funds and ETFs, while remaining negative for the whole study period, improved in the years after the client statements, annual costs and performance reports were implemented.{12}

Our research findings are based on a fund sample representing approximately 62% of mutual funds and ETFs in the Canadian market, as measured by assets under management (AUM) in December 2020.

We use total return and risk-adjusted return, also known as alpha, as measures of fund performance, and report results based on gross returns (i.e., returns before fees and expenses).{13}

The annualized average gross total returns between 2013 and 2020, for our study sample, were 7.1% for mutual funds and 7.9% for ETFs. Accounting for fund risks, we found that the mean gross alphas relative to our model benchmarks were -3.5% for mutual funds and -2% for ETFs. These negative alphas imply that, on average, the total returns are lower than what would be implied by our chosen benchmark used to account for fund risks.{14}

Comparing the performance findings for the pre- and post-implementation periods, we found that the risk-adjusted returns relative to our model benchmarks improved during the post-implementation period, even though they continued to remain negative. For mutual funds, the annualized average gross alpha was -5%, between 2013 and 2016, and -2.2% between 2017 to 2020. The ETF findings were -4.8% for the pre-implementation period and -0.6% for the post-implementation period.

Our research also analyzed whether there were differences in fund performance by the following fund characteristics: asset class, investing strategy, product type, and IFM type. The findings by fund characteristics directionally mirrored the overall findings but the annualized average gross total return and risk-adjusted return varied by fund characteristics.

There were no uniform directional trends for the gross total returns when we compared the pre- and post-implementation results. Between these two time periods, returns increased for some fund characteristics and decreased for others. The gross total returns ranged from 1% to 10.8% for mutual funds, and 1.4% to 11.2% for ETFs.

{1} The reports have benefited greatly from comments from internal and external peer reviewers. They include J. Ari Pandes, Haskayne School of Business, University of Calgary, and reviewers from The Investment Funds Institute of Canada (IFIC) and ISS MI Investor Economics. Any remaining errors of fact or interpretation are the sole responsibility of the authors.

{2} Our study is focused on the management expense ratio (MER) and management fees because the MER is an ongoing cost levied annually, and the components of the MER are relatively consistent across asset classes for the same (mutual fund) series type. The MER consists of the management fee paid to the fund's investment manager, trailing commissions paid investment advisors and/or dealers, operating expenses and taxes. For more information, see https://www.getsmarteraboutmoney.ca/learning-path/mutual-funds-segregated-funds/mutual-fund-fees/

{3} Asset-weighting the average MER or management fee is a way to calculate the average fee paid by investors which gives more weight to the fees charged by investment funds that manage more assets. We use this measure as it better reflects the average fees paid by investors than a simple average.

{4} Our analysis of fees examined the changes in MER and management fees across the following fund characteristics: asset class, fund product type (mutual funds only), fund investment strategy, IFM firm type, and series/class type.

{5} The analysis in the body of the report focuses on fund characteristics that account for the majority of mutual fund and ETF assets.

{6} Series with all levels MER/management fee rates saw both increases and decreases in their asset shares during our study period. However, on average, asset shares of series with lower MER/management fee rates grew more than asset shares of series with higher MER/management fee rates, and this contributed to lowering the asset-weighted average fees.

{7} Ibid.

{8} Investor Economics defines discretionary financial assets as financial assets where households hold the decision-making power with regards to the deployment of these monies into specific investment vehicles.

{9} Investor Economics defines fund wrap programs as those that use investment funds as building blocks. These can include segregated funds of funds, mutual funds of funds, packaged fund wraps and high-end fund wraps.

{10} Strategic beta ETFs are funds that apply rules to a basket of securities (often represented by an index) to target companies that demonstrate specific "factors" such as value, momentum, or growth. Strategic beta ETFs are also known by other names such as smart beta or alternative beta. There is no universally accepted view as to whether strategic beta ETFs are passively managed investment funds or actively managed investment funds. For the purpose of our research, we have classified strategic beta ETFs as passively managed funds because they focus on a specific basket of securities often represented by indices.

{11} Redeemable investment funds generally allow investors to purchase or redeem securities of mutual funds on demand for a price representing a proportionate interest of the fund's net assets. Mutual funds are the main type of redeemable investment fund.

{12} Note that risk-adjusted performance is measured relative to our chosen benchmarks based on the Fama and French (2015) model. Negative risk-adjusted performance of a fund indicates that the fund underperformed the benchmarks used to account for the fund risks in the model we have applied. It is important to highlight that a negative risk-adjusted return does not imply that investors incurred losses from investing in the fund during our sample period.

{13} Gross performance allows the analysis of funds' performance to be independent of their fees and expenses, which are analyzed separately in a companion report entitled A Post-Implementation Review of the Impacts of the CRM2 Annual Costs and Performance Reports on Investment Fund Fees. We have also assessed net performance and obtained qualitatively similar conclusions (results available upon request).

{14} See footnote 11 for some information on our chosen benchmark.

1. |

Introduction and a Summary of Research Findings |

3 |

|

|

1.1 |

Purpose and Background of Research |

3 |

|

1.2 |

Summary of Research Findings |

4 |

|

|||

2 |

Organization of Research Findings |

9 |

|

|

|||

3 |

Overview of Canadian Household Discretionary Financial Assets |

10 |

|

|

|||

4 |

Overview of Investment Fund Industry in Canada |

12 |

|

|

|||

5 |

Mutual Fund Fees Research Findings |

19 |

|

|

5.1 |

Overview of Mutual Fund Study Sample -- Assets, Returns and Fees |

19 |

|

5.2 |

Changes in the Overall Asset-Weighted Average MERs and Management Fees by Study Period |

20 |

|

5.3 |

Mutual Fund Fees by Broad Asset Class |

25 |

|

5.4 |

Mutual Fund Fees by Series Type |

29 |

|

5.5 |

Mutual Fund Fees by Product Type |

32 |

|

5.6 |

Mutual Fund Fees by Investing Strategy |

35 |

|

5.7 |

Mutual Fund Fees by IFM Firm Type |

37 |

|

|||

6 |

ETF Fees Research Findings |

41 |

|

|

6.1 |

Introduction |

41 |

|

6.2 |

Overview of ETF Study Sample -- Assets, Returns, and Fees |

42 |

|

6.3 |

Changes in The Overall Asset-Weighted Average MERs and Management Fees by Study Periods |

43 |

|

6.4 |

ETF Fees by Broad Asset Class |

44 |

|

6.5 |

ETFs Fees by Investing Strategy |

47 |

|

6.6 |

ETF Fees by IFM Firm Type |

50 |

|

|||

7 |

Conclusion |

53 |

|

|

|||

Appendix A -- Research Design and Fees Methodology |

55 |

||

|

1. |

Research Design |

55 |

|

2. |

Fees Methodology |

58 |

|

|||

Appendix B -- Explanation and Interpretation of the Fund Asset Weight Effect, the Price Effect, and the Interaction Effect |

60 |

||

|

|||

Appendix C -- Supplemental Data Tables by Report Sections |

66 |

||

Policy evaluation is crucial in the policy development cycle because it allows regulators to understand whether a newly introduced policy has been implemented as intended and is having the desired impacts and outcomes.

The purpose of this research is to examine the post implementation impacts of the final phase of the Client Relationship Model (CRM2) amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (herein after the CRM2 annual costs and performance reports) on industry behaviour.

The final amendments, which came into effect on July 15, 2016, were designed to ensure investors receive clear and complete disclosure of the performance of their investments and all fees associated with their accounts, including registrant compensation, on an annual basis.

With increased transparency of fees and performance in the CRM2 annual costs and performance reports, we expect that investors have paid closer attention to the total cost of investing and the services received over time. We hypothesize that this increase in cost and performance awareness has led to more competitive product pricing (e.g., investment fund managers may lower fees on existing mutual fund series/classes) with knock on effects for risk-adjusted performance.

To test our hypothesis, we undertook a study to examine whether greater transparency about investment cost and performance has led to changes in mutual fund and exchange-traded fund (ETF) fees{2}, product creation, and product distribution. In particular, we asked:

1. Have investment fund managers (IFMs) lowered fees, specifically the management expense ratio (MER) and management fee, and what is the extent of these changes?

2. Have product manufacturers and product distributors been shifting to products that are not captured by the new account costs and performance disclosures, and

3. What have been the changes in product creation and distribution trends?

An accompanying research report entitled A Post-Implementation Review of the Impacts of the CRM2 Annual Costs and Performance Reports on Investment Fund Performance provides insights into whether IFMs have improved the risk-adjusted performance of their products as a result of the CRM2 annual costs and performance reports. The performance research tests our hypothesis that greater transparency of fees and performance has led to an increased demand from both investors and their advisers for funds with better risk-adjusted performance.

Research suggests that we should anticipate this outcome as a corollary of any reduction in fund fees.{3}

This fees report is focused on mutual funds and ETFs, but where appropriate other types of investment products, such as segregated funds, are also examined.{4}

Our fees analysis examines changes in MERs and management fees for the following mutual fund/ETF fund characteristics:

• asset class

• fund product type (mutual funds only)

• fund investing strategy

• IFM firm type

• series/class type (mutual funds only).{5}

We focused our analysis on these fund characteristics as there is a large body of research conducted by academics, industry, and regulators showing that these characteristics are significant in influencing fund expenses.

The study period covers January 2013 to December 2020. This time period begins about 18 months before the first set of CRM2 amendments came into effect on July 15, 2014 (cost disclosures related to pre-trade disclosure of charges, and trade confirmation for debt securities). The 2013 start date gives us a baseline of the investment fund industry before the first set of CRM2 amendments were implemented. We hypothesize that the changes we are seeking to measure took place several years after the CRM2 annual costs and performance reports are fully implemented. In light of this, the study timeline extends to 2020 to account for this time lag, enabling us to more fully observe the extent of any changes. Our analysis groups the findings into three time periods: 2013 to 2020, which is the overall duration of our study period, the pre-implementation period of 2013 to 2016 and the post-implementation period of 2017 to 2020.

The findings presented in this report are the views of CSA staff and are for informational purposes only. As such, statements made in the report do not represent the CSA's views of any official policy position.

Our findings provide important directional trends, i.e., correlation rather than cause and effect outcomes. As such, we caution readers from drawing conclusions that the changes presented in this report were caused by the CRM2 annual costs and performance reports.

It is possible that other factors, which we could not practically account for in our analysis, also contributed to the changes we are highlighting.

These factors include: advertising by firms competing on fees; local and national news stories focused on fees, cost effective investments, and the best interest discussion in Canada; increasing investor interest in passive investment funds and online advisers; and improvements in market conditions.

Keeping these limitations in mind, our research found that after the introduction of the CRM2 requirements:

• MERs and management fees decreased, for both mutual funds and ETFs in our study sample{6}

• there is no evidence that IFMs and product distributors have been shifting to products not subject to the CRM2 requirements

• there were market shifting changes in product creation and distribution. Most notable were the growth of the ETF market and actively managed and strategic beta ETFs, growth in fee-based mutual fund series, and the emergence of online advisers.

These findings suggest that industry behaviour, overall, has been shifting in directions that are congruent with our hypothesis on the impact of the CRM2 regulations, and help provide evidence that disclosure-based regulations may be an effective tool in changing industry and investor behaviour.

We further discuss the three generalized findings for each of our research questions by the study's three time periods, in the latter half of this section of the report. Sections 4, 5, and 6 of the report break down our research findings in greater detail, specifically by investment fund type, fund characteristics, and time periods.

This section of the report further discusses the three generalized findings for each of our research questions by the study's three time periods.

Research question 1: Have investment fund managers (IFMs) lowered fees, specifically MERs and management fees, and what are the extent of these changes? |

There were declines in the asset-weighted average MERs and management fees, for both mutual funds and ETFs, during our study period, and the extent of these changes varied by investment fund type and fund characteristics.

Overall, the asset-weighted average MER declined by 38 basis points (or 19%) over 2013-2020 for our study sample, and between 13 and 49 basis points, or between 6% and 30%, across the main fund characteristics examined.{7} The size of the asset-weighted average management fee declines was smaller, at 29 basis points for the overall study sample and ranged from 6 to 39 basis points across the main fund characteristics, or between 4% and 32%.

Changes in the asset-weighted average MERs and management fees were generally greater during the post-implementation period than the pre-implementation period. Declines in the asset-weighted average MERs and management fees across the fund characteristics examined ranged from 3 to 19 basis points, or 2% to 15%, for both time periods.

Both shifts in the distribution of assets towards mutual fund series with lower fees, and reductions in series' MERs and management fee rates, contributed to lowering the asset-weighted average MERs and management fees.{8}

However, shifts in the distribution of assets had a larger effect than reductions in MER/management fee rates in lowering the aggregate asset-weighted average MERs/management fees for both time periods.

ETFs, compared to mutual funds, had smaller declines in their asset-weighted average MERs and management fees during our study period. This finding was anticipated since the MERs and management fees for most ETFs started from a lower baseline level. This is primarily because the majority of ETF assets are invested in funds that employ a passively managed investing strategy.

By the end of our study period in 2020, the asset-weighted average MER for our study sample had declined by 8 basis points (or 21%) from 2013 levels, and between 6 and 11 basis points or between 12% and 34%, depending on the fund characteristic examined. The decrease in the overall asset-weighted average management fee was 7 basis points (22%) between 2013 and 2020. Across the main fund characteristics, the declines in asset-weighted averages ranged from 3 to 10 basis points, or 5% to 34%.

Changes in the asset-weighted average MERs and management fees during both the pre- and post-implementation periods ranged from +1 to --8 basis points or +1% to --19% across the fund characteristics examined. There were no strong directional trends in the asset-weighted average MER/management fee declines by fund characteristics. Both changes in the distribution of assets and reductions in MERs and management fee rates had a broadly similar contribution to lowering the asset-weighted average fees, in both the pre- and post-implementation periods.{9}

Research question 2: Have product manufacturers and product distributors been shifting to products that are not captured by the new account costs and performance disclosures? |

Our analysis of Canadian household discretionary financial assets did not show a trend of discretionary financial assets moving towards products not captured by the CRM2 annual costs and performance report requirements.

Between 2013 and 2020, the share of discretionary financial assets held in deposits remained stable at 27%. Meanwhile, the share of assets in non-investment fund securities increased slightly, from 25% to 26%, and the share of assets in investment funds increased from 28% to 32%. For investment funds, the 4 percentage point share increase was the result of growing market shares for mutual funds and ETFs.

Research question 3: What have been the changes in product creation and distribution trends, generally? |

Five notable changes in product creation and distribution occurred during our study period. Unless otherwise noted, the findings and figures discussed below are for the overall industry and are not only for our study sample.

The continued popularity of fund wrap programs contributed to a rise in the number of fund-of-funds products, for both mutual funds and ETFs; and, this was evident in the shift of assets away from stand-alone funds to fund-of-funds products. In 2013, 26% of mutual fund assets were in fund-of-funds products and by 2020 this figure had increased to 37%. One of the largest ETF manufacturers introduced ETF-of-ETFs products in early 2018. By December 2020, ETF-of-ETFs products accounted for $6 billion or 2% of the total industry ETF assets.

Growth of the ETF market was evident during our study period, and the growth rate for ETFs substantially surpassed the growth rate for mutual funds. Between 2013 and 2020, the annual growth in the number of ETFs was 17% while it was 2% for mutual funds.

Within ETF creation, one of the most significant changes that occurred during our study period was the rise of actively managed and strategic beta ETFs.{10} Near the start of our study period, actively managed and strategic beta ETFs accounted for 23% and 17% of the number of ETFs according to data from Investor Economics. By December 2020, their respective share rose to 43% and 21%. The rise in the number of strategic beta ETFs did not lead to a corresponding rise in ETF assets in that category of fund. In contrast, the share of ETF assets in actively managed ETFs increased from 9% at the start of our study period, to 24% by the end of our study period.

Within the mutual fund market, the shift from commission-based to fee-based series was pronounced during our study period. Between 2013 and 2020, the number of fee-based series increased by 186%, from 2,592 to 7,404. In comparison, the number of commission-based "A-series", which is the "core" mutual fund series, increased by 103% from 2,887, in 2013, to 5,880, in 2020.

Looking at our study sample, we found that 6% of mutual fund assets were in fee-based series at the start of our study period in 2013. This figure increased to 27% by the end of our study period in 2020. The growth and shift of assets into fee-based series corresponded with declining assets in commission-based A-series. In 2013, 75% of our study sample assets were in A-series and by 2020 this figure had declined to 58%.

A product creation trend that occurred towards the end of our study period was the rise of and demand for funds with an environmental, social, and governance (ESG) mandate. There were 49 mutual funds with an ESG mandate in 2013 and these funds had assets of $5.1 billion. By 2020, the number of mutual funds with an ESG mandate almost doubled to 97 funds. The number of ETFs with an ESG mandate grew from 10 in 2018, to 50 by 2020. Despite the significant increase in the number of funds with an ESG mandate, their share of total industry assets is small. In 2020, funds with an ESG mandate accounted for around 1% of total industry assets within the mutual fund and ETF markets, respectively.

A new direct to investor/consumer distribution channel emerged in 2014 with the launch of four online advice platforms -- Wealthsimple, Wealth Bar, NestWealth, and Questwealth Portfolios. These platforms provide retail investors with access to discretionary asset management services with a substantially lower, if any, account size minimum requirement. These platforms invest client assets primarily in ETFs, and to a lesser extent in mutual funds, other redeemable investment funds, cash and cash equivalents.{11} By the end of 2020, 22 online advisers operated in Canada. These firms had an estimated $10 billion in assets under management, which is equivalent to about 4% of the industry total assets for ETFs.

Our research findings are organized along the following structure.

Part 3 of the report provides a high-level overview of Canadian household discretionary financial wealth and how this wealth is allocated by investment products. This section of the report discusses whether product manufacturers and distributors are shifting to products not subject to the CRM2 requirements.

Part 4 provides a high-level overview of the investment fund industry in Canada. This section of the report discusses in detail changes in product creation and distribution. Parts 3 and 4 of the report provide useful information to readers that puts the research findings into context and aids readers in their interpretation of the research results.

Part 5 discusses the MER and management fee findings for mutual funds. The results are organized by the fund characteristics discussed in Appendix A of the report. A general overview is presented for each fund characteristic before we examine changes in MERs and management fees, before and after the full implementation of the CRM2 annual cost and performance reports.

Part 6 discusses the ETF fee findings. The format of the ETF research results mirrors the format for the mutual fund fees findings.

Part 7 summarizes our research findings by research question and CSA staff's view on whether disclosure-based regulations can shift industry behaviour in the desired policy direction.

Appendix A provides details of the study's research design and the formulas for calculating changes in MERs and management fees.

Appendix B explains and provides guidance on how to interpret the fees results for each of the effects we examined.

Appendix C provides supplemental data tables by report sections.

The purpose of this section of the report is to provide a high-level overview of Canadian household discretionary financial wealth and answer the question of whether product manufacturers and distributors are shifting to investment products not captured by the CRM2 annual costs and performance reports. Another intent of this overview is to provide useful information to readers that will assist them in contextualizing the research findings, interpreting, and understanding the research results.

Canadian households held an estimated $4.1 trillion in discretionary financial assets, in 2013.{12} Of this amount, approximately $1.1 trillion were held in investment funds.{13} Another $2.1 trillion were held in securities and deposits ($1.0 billion in securities; $1.1 trillion in deposits).

By the end of 2020, household discretionary financial assets increased to $6.5 trillion and, of this amount, $2.1 trillion were held in investment funds. Equities and deposits each amounted to $1.7 trillion in discretionary financial assets.

Table 3.1 below compares the asset size and share of discretionary financial assets for each investment product type, at the start and end of our study period. The share of assets held in investment funds increased during our study period while the share of assets in securities and deposits remained broadly stable.

At a high-level, an investment fund is an investment product that pools money from various investors and invests that money collectively through a portfolio of financial instruments, such as stocks and/or bonds, and the portfolio of investments is professionally managed by a fund manager.

For the purposes of our research, we collectively refer to mutual funds and ETFs, which are focus of our analysis, and segregated funds as investment funds.{14} Segregated funds are an insurance product and were not covered by the CRM2 annual costs and performance report requirements. We have looked at trends in the segregated fund market because they are often sold by dually registered/licensed advisers who are permitted to sell mutual funds and insurance products such as segregated funds.{15} Their inclusion enables us to assess whether product manufacturers and distributors were engaging in regulatory arbitrage by shifting to products not captured by the CRM2 annual costs and performance requirements.

Table 3.1 Estimated Canadian Discretionary Financial Assets, 2013 and 2020

|

Asset Size ($B) |

Share of discretionary financial assets |

|||

|

|||||

|

2013 |

2020 |

2013 |

2020 |

|

|

|||||

All discretionary financial assets |

4,091 |

6,517 |

- |

- |

|

|

|||||

|

Investment funds |

1,145 |

2,074 |

28% |

32% |

|

|||||

|

Securities |

1,031 |

1,686 |

25% |

26% |

|

|||||

|

Deposits |

1,102 |

1,742 |

27% |

27% |

Source: Investor Economics Household Balance Sheet 2021. Excludes group segregated funds, closed end funds and alternatives

Table 3.2 below compares the amount of financial assets that were in investment funds, and each investment fund type's share of the total investment fund assets and all discretionary financial assets, for 2013 and 2020.{16} Just below one-third (1/3) of all discretionary financial assets were held in investment funds, in both 2013 and 2020.

The most common type of investment fund held was mutual funds, which accounted for 26% of all discretionary financial assets, in 2020. Less widely held investment funds were ETFs and segregated funds. At the end of 2020, 4% of discretionary financial assets were held in ETFs and another 2% were held in segregated funds.

During our study period, the share of assets in ETFs increased by 2 percentage points and the share of assets in mutual funds increased by 4 percentage points. Segregated funds share of total financial assets remained stable (see Table 3.2).

Focusing solely on investment funds, ETFs gained market share during our study period. In 2013, their share of investment funds was 6%. By 2020, ETF market share increased to 12%, thus making it the second most widely held type of investment fund. The market share of mutual funds and segregated funds declined by 4 and 3 percentage points between 2013 and 2020. By the end of our study period, mutual funds accounted for 81% of investment fund assets and segregated funds accounted for another 6%.

Table 3.2 Estimated Canadian Discretionary Financial Assets Held in Investment Funds

|

Assets ($B) |

Share of Investment Funds (%) |

Share of discretionary financial assets (%) |

|||||

|

||||||||

|

2013 |

2020 |

2013 |

2020 |

2013 |

2020 |

||

|

||||||||

All discretionary financial assets |

$4,091 |

$6,517 |

- |

- |

- |

- |

||

|

||||||||

|

Investment funds |

$1,145 |

$2,074 |

- |

- |

28% |

32% |

|

|

||||||||

|

|

Canadian listed ETFs |

$63 |

$257 |

6% |

12% |

2% |

4% |

|

||||||||

|

|

Seg funds |

$101 |

$127 |

9% |

6% |

2% |

2% |

|

||||||||

|

|

Mutual funds excl. ETFs |

$981 |

$1,690 |

86% |

81% |

24% |

26% |

Source: Investor Economics Household Balance Sheet 2021. Excludes group segregated funds, closed end funds and alternatives

The findings presented in this section of the report suggest that product manufacturers and distributors were not shifting to products not subject to the CRM2 requirements.

This section of the report provides a high-level overview of the investment fund industry. The focus is on the number funds and assets by investment fund product types, specifically mutual funds, ETFs and (individual) segregated funds. The intent of this section of the report is to provide key background information that readers may need to understand and interpret the research findings. This section is not intended to provide a detailed overview of the investment fund industry in Canada. Readers interested in this topic can refer to the CSA's Mutual Fund Fees Discussion Paper published in December 2012.{17}

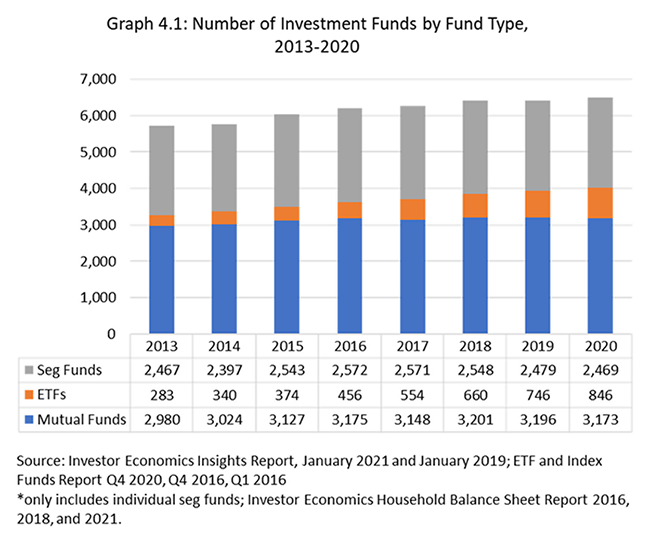

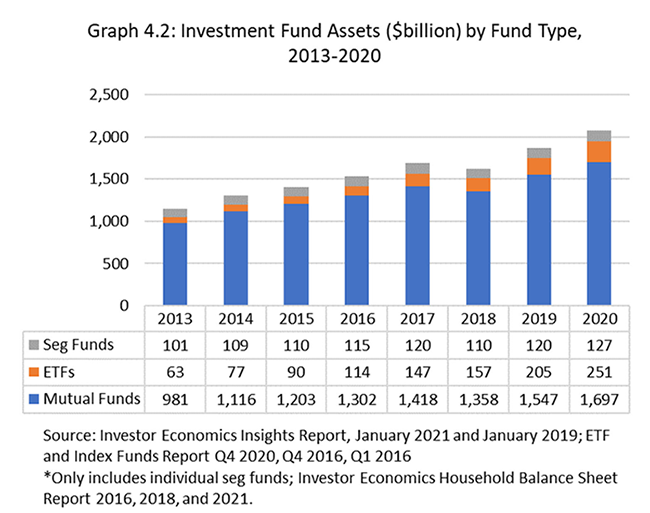

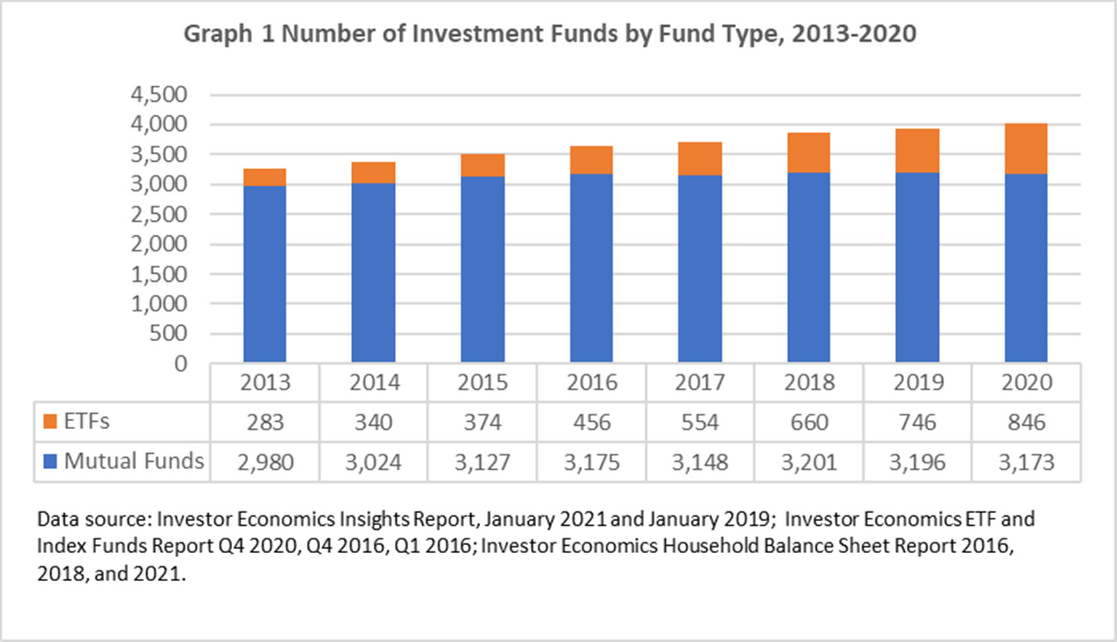

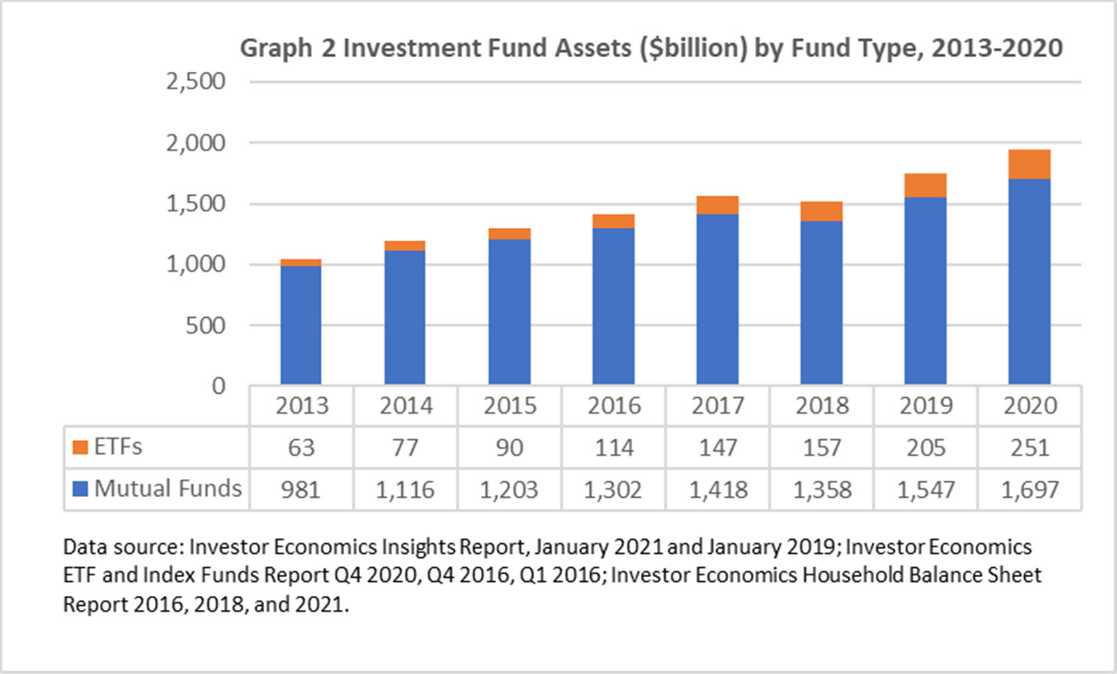

The graphs below show the number of funds and annual assets for each investment fund type.

During our study period, there was a steady rise in the number of ETFs and ETF assets (refer to Graphs 4.1 and 4.2). The average year-over-year increase in the number of ETFs was 17% during our study period. The average year-over-year increase was much lower for mutual funds and segregated funds, and the increases were 1% and 0.05%, respectively.

The number of segregated funds was not proportionate to its share of investment fund assets. Segregated funds accounted for 38% to 43% of investment funds throughout our study period, but only 6% to 9% of investment fund assets. The average annual growth in the number of funds and assets was 0.05% and 3%, respectively.

The number of mutual funds steadily increased during our study period, but they accounted for a declining share of the number of funds and investment fund assets, due to the rising share of ETFs. The average annual growth in the number of mutual funds and their assets were 1% and 8%, respectively.

The orange bars in Graphs 4.1 and 4.2 visualize the growing number of ETFs and their increasing share of investment fund assets, during our study period.

Trends in production creation and distribution were (and continues to be) driven by the need to differentiate product offerings and channels of access to investment funds.

The continued popularity of fund wrap programs has contributed to a rise in the number of fund-of-funds products, for both mutual funds and ETFs, and a corresponding rise in their fund assets (refer to Tables 4.1.1 and 4.1.2). The ratio of the number of stand-alone funds to fund-of-funds products remained constant throughout our study period. The share of assets, however, started to shift away from stand-alone funds to fund-of-fund products, as our study period progressed.{18}

The introduction of ETF-of-ETFs products, i.e., ETFs where the underlying portfolio of securities consists of other ETFs, by one of the larger ETF manufacturers occurred early in 2018.{19} By December 2020, ETF-of-ETF products, accounted for $6 billion or 2% of the total industry ETF assets.{20}

Table 4.1.1 Number of Mutual Funds by Product Type (Industry Total and for Long-Term Funds Only)

Product Type |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

|

||||||||

Stand-alone funds |

1,814 |

1,829 |

1,843 |

1,930 |

1,599 |

2,468 |

2,469 |

2,459 |

|

||||||||

Fund-of-funds |

485 |

495 |

481 |

564 |

501 |

687 |

689 |

678 |

|

||||||||

Total |

2,299 |

2,324 |

2,324 |

2,494 |

2,100 |

3,155 |

3,158 |

3,137 |

|

||||||||

Share of Industry Total |

||||||||

|

||||||||

Stand-alone funds |

79% |

79% |

79% |

77% |

76% |

78% |

78% |

78% |

|

||||||||

Fund-of-funds |

21% |

21% |

21% |

23% |

24% |

22% |

22% |

22% |

Source: IFIC; fund count is for December of each year

Table 4.1.2 Mutual Fund Assets ($B) and Share of Mutual Fund Assets by Product Type (Industry Total and for Long-Term Funds Only){*}

Product Type |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

|

||||||||

Stand-alone funds |

735 |

811 |

839 |

894 |

966 |

908 |

1,040 |

1,130 |

|

||||||||

Fund-of-funds |

264 |

330 |

392 |

445 |

511 |

515 |

591 |

654 |

|

||||||||

Industry Total |

999 |

1,141 |

1,231 |

1,339 |

1,477 |

1,423 |

1,630 |

1,784 |

|

||||||||

Share of Industry Assets |

||||||||

|

||||||||

Stand-alone funds |

74% |

71% |

68% |

67% |

65% |

64% |

64% |

63% |

|

||||||||

Fund-of-funds |

26% |

29% |

32% |

33% |

35% |

36% |

36% |

37% |

Source: IFIC

Another significant trend in the ETF market during our study period was the rise of actively managed and strategic beta ETFs.{21} In March 2014, actively managed and strategic beta ETFs accounted for 23% and 17% of the number of ETFs based on analysis of data from Investor Economics.{22} By December 2020, their respective shares rose to 43% and 21%.{23} The rise in the number of strategic beta ETFs did not lead to a corresponding rise in ETF assets. In contrast, the share of ETF assets in actively managed ETFs increased from 9% at the start of our study period, to 24% by the end of our study period.{24}

A third emerging trend that occurred towards the end of our study period was the rise of and demand for funds with an environmental, social, and governance (ESG) mandate. The number of ESG funds and the assets in these funds steadily increased during our study period, with the greatest year-over-year growth occurring between 2019 and 2020 (refer to Tables 4.1.3 and 4.1.4). By the end of our study period, there were an estimated 97 mutual funds and 50 ETFs with an ESG mandate, and their net assets accounted for 1% of total industry assets within the mutual fund and ETF markets, respectively.{25}

Table 4.1.3 Estimated Number of Funds, and Net Assets of Funds with an ESG Mandate

Fund Type |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

|

|

|||||||||

Number of Funds |

|||||||||

|

|||||||||

|

Mutual Fund |

49 |

46 |

46 |

52 |

61 |

67 |

73 |

97 |

|

|||||||||

|

ETFs |

- |

- |

- |

- |

- |

10 |

20 |

50 |

|

|||||||||

Net Assets ($B) |

|||||||||

|

|||||||||

|

Mutual Fund |

5.1 |

6.0 |

6.8 |

8.0 |

9.8 |

10.1 |

12.3 |

17.6 |

|

|||||||||

|

ETFs |

- |

- |

- |

- |

- |

0.1 |

0.3 |

2.8 |

Source: OSC analysis of IFIC data (sourced from fund prospectuses) . Analysis is limited to long-term mutual funds and ETFs. Fund count and fund assets are as at December of each year.

Table 4.1.4 Estimated Year-over-Year Change in the Number of Funds, and Net Assets of Funds with an ESG Mandate

Fund Type |

13-'14 |

14-'15 |

'15-'16 |

'16-'17 |

'17-'18 |

'18-'19 |

'19-'20{*} |

|

|

||||||||

Number of Funds |

||||||||

|

||||||||

|

Mutual Fund |

-6% |

0% |

13% |

17% |

10% |

9% |

33% |

|

||||||||

|

ETFs |

- |

- |

- |

- |

- |

100% |

150% |

|

||||||||

Net Assets ($B) |

||||||||

|

||||||||

|

Mutual Fund |

17% |

13% |

18% |

23% |

3% |

22% |

43% |

|

||||||||

|

ETFs |

|

|

|

|

|

162% |

954% |

Source: OSC analysis of IFIC data (sourced from fund prospectuses) . Analysis is limited to long-term mutual funds and ETFs.

A new direct to investor/consumer distribution channel emerged in 2014 with the launch of four online advice platforms -- Wealthsimple, Wealth Bar{26}, NestWealth, and Questwealth Portfolios. As noted in CSA Staff Notice 31-342.{27}

Unlike "robo-advisors" in the USA, these online advice platforms "offer hybrid services that utilize an online platform for efficiency, while registered advising representatives (ARs) remain actively involved. These platforms use online questionnaires as the basis for the know-your-client (KYC) information gathering process, but ARs are responsible for determining that sufficient KYC information has been gathered to support investment suitability determinations. Clients' managed accounts are invested in relatively simple products, including unleveraged exchange traded funds (ETFs), low cost mutual funds or other redeemable investment funds, cash and cash equivalents. Often, model portfolios are created using algorithmic software although, again, an AR has responsibility for the suitability of each client's investment."

By the end of 2020, 22 online advisers{28} operated in Canada. These firms had an estimated $10 billion in AUM.{29}

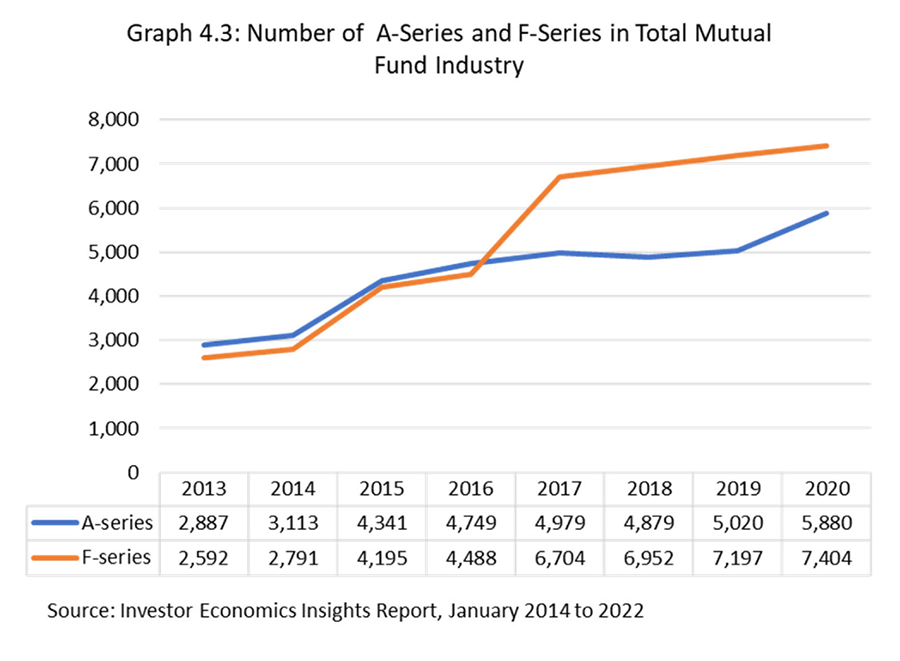

Another notable trend that emerged during our study period was the shift away from commission-based to fee-based products and/accounts. This was most pronounced in mutual funds, and the growth of fee-based "F-series".{30} In 2013, the number of funds with a F-series accounted for 23% of all mutual funds, and by 2020, this figure rose to 29% (refer to Graph 4.3). The number of F-series surpassed the number of A-series starting in 2017.{31} We hypothesize and have heard anecdotally that the proposed regulations related to embedded commissions in mutual funds and the Client Focused Reforms were important drivers behind this change, as IFMs started creating F-series, in response to a shift in adviser practice models.

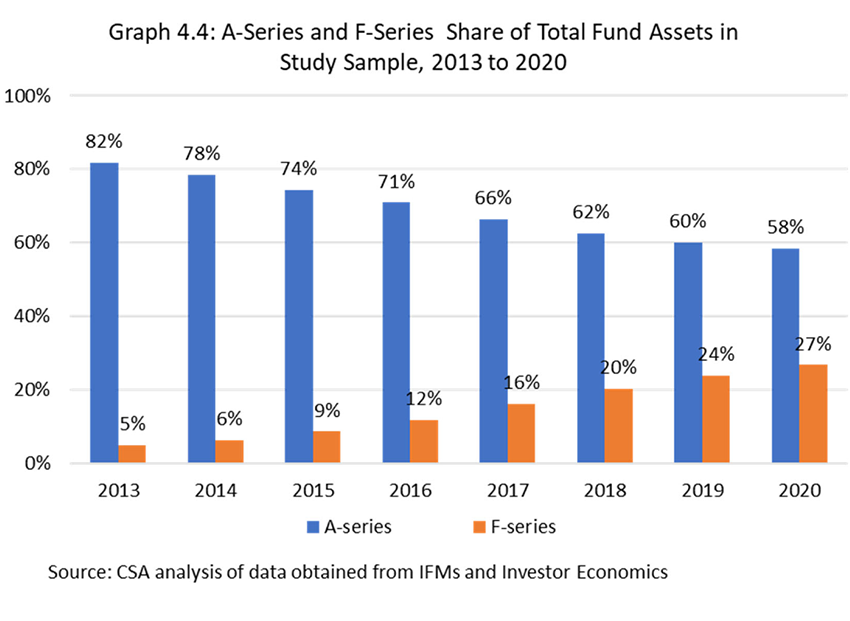

The shift in assets can be seen in our study sample. In 2013, 5% of assets were in F-series and, by 2020, this figure had increased to 27%. For the same time periods, the share of total fund assets in A-series decreased from 82% to 58% (refer to Graph 4.4).

Our analysis of mutual fund MERs and management fees consisted of 2,990 unique mutual funds, at the fund level, and 13,617 series. The total AUM of these funds was $781 billion in 2020, and these funds accounted for 44% of the total industry AUM of $1.78 trillion.{32} Table 5.1.1 breaks down the number of funds and their assets, returns, and fees for each year of our study period.

Fund assets steadily increased during our study period, from $545 billion in 2013 to $781 billion in 2020. Our study sample accounted for about 50% of total industry assets, on average.{33}

There were no clear overall directional trends in mutual fund returns during our study period. The asset-weighted annualized gross returns were positive for all but one year -- 2018 -- and returns ranged from -3.84% to 13.28%. While not a focus of our study, the fees and returns findings indicate that investors holding mutual funds, on average, realized positive net returns in 7 of the 8 years of our study period.

The simple average and asset-weighted average MERs and management fees steadily decreased for each year of our study period.

From 2013 to 2019 the simple average MER was lower than the asset-weighted average MER, and this relationship only reversed in 2020. This finding indicates that for seven years of our study, assets were concentrated in series with higher MERs and the asset shift to series with comparatively lower MERs only became evident in the final year of our study period.

Table 5.1.1 Mutual Fund Assets, Returns, and Fees, 2013-2020

|

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

|

||||||||

Net assets ($B) of series in study |

545 |

622 |

632 |

671 |

708 |

699 |

747 |

781 |

|

||||||||

Industry assets ($B) |

999 |

1,141 |

1,231 |

1,339 |

1,477 |

1,423 |

1,630 |

1,784 |

|

||||||||

Share of industry assets (series in study) |

55% |

54% |

51% |

50% |

48% |

49% |

46% |

44% |

|

||||||||

Number of funds in study (at the fund level) |

2,235 |

2,344 |

2,379 |

2,480 |

2,442 |

2,421 |

2,348 |

2,254 |

|

||||||||

Number of series in study |

7,497 |

8,382 |

9,120 |

10,175 |

10,549 |

11,067 |

10,539 |

10,011 |

|

||||||||

Number of series -- industry total |

8,652 |

9,356 |

15,175 |

18,813 |

20,644 |

21,232 |

21,784 |

22,066 |

|

||||||||

Share of industry total -- number of series in study |

87% |

90% |

60% |

54% |

51% |

52% |

48% |

45% |

|

||||||||

Asset-weighted annualized gross returns (%) |

13.05 |

8.21 |

3.08 |

7.26 |

7.22 |

-3.84 |

13.28 |

9.45 |

|

||||||||

Simple average MER |

1.96 |

1.93 |

1.88 |

1.82 |

1.77 |

1.71 |

1.69 |

1.69 |

|

||||||||

Asset-weighted average MER |

2.06 |

2.03 |

1.98 |

1.93 |

1.83 |

1.77 |

1.70 |

1.67 |

|

||||||||

Simple management fee |

1.49 |

1.47 |

1.44 |

1.40 |

1.36 |

1.33 |

1.32 |

1.31 |

|

||||||||

Asset-weighted average management fee |

1.65 |

1.64 |

1.61 |

1.56 |

1.48 |

1.43 |

1.38 |

1.36 |

CSA analysis of data obtained from investment fund managers and third-party data providers. Assets and expense data were obtained from Investor Economics. Gross monthly total returns data were obtained from Morningstar Direct. Assets are as at December. Funds in our study sample exclude institutional fund series.

This section of the report presents the research findings for all mutual funds, i.e., without grouping the mutual funds into different fund characteristics, for the pre- and post-implementation periods.

The asset-weighted average MER and management fee declined during both the pre- and post-implementation periods (refer to Tables 5.1.1 and 5.2.1). In 2013, the asset-weighted average MER was 206 basis points and by 2016 it had declined by 13 basis points (or 6%), to 193 basis points. In 2017, the asset-weighted average MER was 183 basis points, and by 2020 it had declined to 167 basis points, which was a 16 basis point (or 9%) decline. This trend was seen in the aggregate and, on average, at the individual fund level.

The asset-weighted average management fee declines were smaller than the MER declines. The pre-implementation decline was 9 basis points (5%), and the post-implementation decline was 13 basis points (8%). This finding was expected since, in general, the management fee accounts for most of an MER.

The negative fund asset-weight effects, for both the asset-weighted average MER and management fee, were larger than the negative price effects during the pre-implementation period (refer to the Fund Weight (FW) Effect and Price Effect rows in Table 5.2.1). This finding tells us two things. First, both the fund asset-weight and price effects contributed to lowering the asset-weighted fees.{34} Second, the fund asset-weight effect, i.e., changes in the distribution of assets across the different the series in our sample, however had a greater impact than the price effect in driving down the asset-weighted fees during the pre-implementation period. The relative impact between the fund asset weight and price effects in decreasing the asset-weighted average fees was broadly similar during the post-implementation period.

Table 5.2.1 Changes in AW Avg MERs/Mgmt Fees, All Mutual Funds, Pre- and Post-Implementation Periods

|

AW Avg MERs |

AW Avg Mgmt Fees |

||||

|

||||||

|

Chg '13-'16 |

Chg '17-'20 |

Chg '13-'16 |

Chg '17-'20 |

||

|

||||||

AW Avg MER Chg/Mgmt Fee Chg |

-0.13 |

-0.16 |

-0.09 |

-0.13 |

||

|

||||||

Fund Weight (FW) Effect |

-0.09 |

-0.12 |

-0.07 |

-0.10 |

||

|

||||||

|

of which... |

|

|

|

|

|

|

||||||

|

|

Sales Effect |

-0.11 |

-0.12 |

-0.08 |

-0.10 |

|

||||||

|

|

Returns Effect |

0.02 |

0.00 |

0.01 |

0.00 |

|

||||||

Price Effect |

-0.02 |

-0.01 |

-0.01 |

-0.01 |

||

|

||||||

FW + Price Effects |

-0.02 |

-0.02 |

-0.01 |

-0.01 |

||

|

||||||

Share of series with fund weight declines |

42% |

61% |

42% |

61% |

||

|

||||||

Share of series with price declines |

58% |

54% |

17% |

11% |

||

Fund Weight and Price Effects, and shares of series with fund weight and price declines, are calculated using series where both expense and asset data are available over the specific implementation period. CSA analysis of data obtained from investment fund managers and third-party data providers. Assets and expense data were directly obtained from Investor Economics. Returns data were obtained from Morningstar Direct.

The interaction effect (refer to the FW+Price Effects row in Table 5.2.1 also contributed to decreasing the asset-weighted fees. The size of the interaction effect ranged from 1 to 2 basis points.

An explanation and interpretation of these effects are provided below, using a subset of the research findings.

We caution readers that the size of the asset-weighted average MER/management fee changes discussed in this section of the report are not equal to the sum of the different fee changes by fund characteristic discussed in the proceeding sections of the report. This is because the asset-weighted averages reported above are calculated using all series in our sample, whereas the averages by fund characteristic discussed below are based on only the subset of series captured by each fund characteristic. |

As noted above, the asset-weighted average MER decreased by 13 and 16 basis points respectively during the pre- and post-implementation periods, and part of the decrease was driven by series with declines in their share of total assets covered by our sample. Specifically, 42% of series during the pre-implementation period and 61% of series during the post-implementation period experienced a decline in their assets and in turn their asset weights.{35} These declines would have lowered the aggregate asset-weighted average MERs by 9 and 12 basis points for the respective time periods if funds kept their fees constant over each period (refer to Table 5.2.1).

The findings pertaining to the share of series with declines in their assets and the size of the fund asset weight effect indicate that the relationship between these two variables is not linear; that is, a large numerical value for one variable does not correlate to a large numerical value for the other. Rather, the primary factor that dictates the size of the fund asset weight effect is the aggregate assets of the series with declines in their share of total assets covered by the sample, while the number of series is a secondary factor. A conclusion that can then be drawn from the MER findings is that larger funds contributed to the negative fund asset weight effect, particularly during the pre-implementation period.

Within the fund asset weight effect, we see that changes in assets arising from sales, in the aggregate, contributed to lowering the asset-weighted average MER and management fee, in both the pre- and post-implementation periods. A negative value for the sales effect does not indicate that in the aggregate there was negative sales for the series in our study sample. Rather, a negative value indicates that a sufficient number of series saw large enough declines in their asset shares due to sales, such that the asset share changes contributed to lowering the overall asset-weighted average MER/management fee.

Conversely, a positive return effect tells us that a sufficient number of series saw their asset shares increase because of asset growth arising from investment returns, such that the asset share changes contributed to increasing the aggregated asset-weighted average MER/management fee.

The purpose of the fund asset weight effect is to understand how changes in distribution of assets across series are contributing to changes in the asset-weighted average fee, while holding MERs/management fees constant. This metric is therefore not suitable for making inferences about whether assets were flowing into funds with lower or higher fees, overall. More appropriate metrics to use are the asset-weighted average MER and management fee findings, in Table 5.1.1, because these metrics consider changes in both a series' assets and MER/management fee rate. The conclusion that can be drawn from the findings in Table 5.1.1 is that assets generally flowed into funds with lower MER/management fee rates, and that MERs and management fees, on average, decreased.

The negative price effects indicate the following necessary and sufficient changes took place for series that operated over the entire given time periods:

i) a sufficient number of series lowered their MER or management fee rates

ii) the size of the fee reductions for these series was sufficiently large, and

iii) these series had sufficiently large assets

such that these three conditions contributed to lowering the aggregated asset-weighted average MER/management fee, for both the pre- and post- implementation periods by the amounts shown in Table 5.2.1.

The relationship between the share of series with declines in their fees and the price effect is not linear. A higher (lower) share of series with declines in their fees does not necessarily equate to a larger (smaller) price effect. The size of the price effect is determined by the interplay between the size of the fee reductions and whether these reductions occurred in series with relatively higher or lower fund asset weights.

Additionally, comparing the share of series with price declines and the corresponding price effect between fee types (and fund characteristics in proceeding sections of the report) or time periods is not meaningful due to differences in the sample size and population of series.{36} The only meaningful comparison that can be made for the price effect, across fee type, fund characteristics, and time periods is the size of the price effect and its contribution to the directional change in the aggregated asset-weighted average MER/management fees for the particular fee type, characteristic or time period. The price effect can also be compared to the fund asset weight effect for the same comparative analysis.

The interaction effect is more difficult to interpret than the individual price or fund asset weight effects because it is measuring the impacts of two variable changes at once rather than a single variable change, which is the procedure used to measure the fund asset weight and price effects.

The interaction effect can increase, decrease, or have no impact on the aggregated asset-weighted average MER/management fee. The size and direction of the interaction effect varied depending on the fund characteristics looked at in our study.

Two scenarios were responsible for the interaction effects observed in our study, as illustrated in Figure 1 in Appendix B of the report. The first scenario was due to the addition of new series or the deletion of existing series.{37} In general, the addition of new series occurred more often in our sample during the pre-implementation period than the post-implementation period. The second scenario was instances where series had simultaneous changes in their asset weights and MER or management fee rates.{38}

The distribution and number of mutual fund assets by broad asset class are shown below in Table 5.3.1. The dominant broad asset classes of funds throughout our study period were balanced funds, with 55% of mutual fund assets in our sample in 2020.{40} The other two dominant broad asset classes of funds were equity and fixed income funds. These funds accounted for 32% and 11% of total fund assets in our sample in 2020. Funds in the money market and other broad asset class categories accounted for the remaining 1% of assets in the final year of our study period. Balanced, equity, and fixed income funds' share of the total assets in our sample remained relatively constant throughout our study period.

Table 5.3.1 Mutual Fund Assets ($B) by Broad Asset Class

Broad Asset Class |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

No. of Series in Sample |

|

|||||||||

Balanced |

278 |

335 |

350 |

375 |

392 |

386 |

420 |

431 |

4,655 |

|

|||||||||

Equity |

200 |

220 |

214 |

224 |

237 |

234 |

238 |

252 |

6,890 |

|

|||||||||

Fixed Income |

59 |

59 |

61 |

65 |

71 |

70 |

81 |

89 |

1,692 |

|

|||||||||

Money Market |

6 |

5 |

5 |

4 |

4 |

4 |

5 |

5 |

110 |

|

|||||||||

Other |

2 |

3 |

3 |

3 |

4 |

4 |

4 |

3 |

270 |

|

|||||||||

Total |

545 |

622 |

632 |

671 |

708 |

699 |

747 |

781 |

13,617 |

CSA analysis of data obtained from investment fund managers and third-party data providers. Asset data were directly obtained from Investor Economics. Broad asset class data developed by the CSA using CIFSC data provided by investment fund managers. The "Other" broad asset class category represents funds that investment in so called alternative/non-traditional assets such as real estate or derivatives products.

The asset-weighted fees for funds of all three dominant broad asset classes steadily declined during our study period (refer to Tables 5.3.2 and 5.3.3).{41} The size of the decline was greater for the asset-weighted average MER than the asset-weighted average management fee. The size of the fee declines varied by asset classes, and it ranged from 32 to 48 basis points (15% to 30%) over 2013-2020 for the asset-weighted average MERs, and 24 to 38 basis points (14% to 32%) for the asset-weighted average management fees.

The asset-weighted average MERs and management fees for equity funds were, on average, slightly greater than the fees for balanced funds throughout our study period. Balanced and equity funds had asset-weighted average MERs that were above 200 basis points at the start of our study period, in 2013. The asset-weighted average MERs dropped below 180 basis points by the end of our study period, in 2020. Fixed income funds had the lowest asset-weighted average MERs and management fees of the three dominant asset classes. The cost difference between fixed income funds and equity/balanced funds was 64-78 basis points, for the asset-weighted average MER, and 49-63 basis points, for the asset-weighted average management fee, depending on the year of our study period.

Table 5.3.2 Asset-Weighted Average MERs by Broad Asset Class, 2013 to 2020

Broad Asset Class |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

Chg '13-'16 |

Chg '17-'20 |

|

||||||||||

Balanced |

2.10 |

2.07 |

2.03 |

1.98 |

1.90 |

1.85 |

1.79 |

1.78 |

-0.12 |

-0.12 |

|

||||||||||

Equity |

2.22 |

2.17 |

2.12 |

2.05 |

1.94 |

1.87 |

1.77 |

1.74 |

-0.17 |

-0.19 |

|

||||||||||

Fixed Income |

1.46 |

1.40 |

1.35 |

1.28 |

1.19 |

1.13 |

1.06 |

1.02 |

-0.18 |

-0.17 |

CSA analysis of data obtained from investment fund managers and third-party data providers. Asset and expense data were directly obtained from Investor Economics.

Table 5.3.3 Asset-Weighted Average Management Fees by Broad Asset Class, 2013 to 2020

Broad Asset Class |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

Chg '13-'16 |

Chg '17-'20 |

|

||||||||||

Balanced |

1.69 |

1.69 |

1.65 |

1.62 |

1.55 |

1.50 |

1.47 |

1.45 |

-0.08 |

-0.10 |

|

||||||||||

Equity |

1.75 |

1.73 |

1.70 |

1.63 |

1.55 |

1.49 |

1.44 |

1.41 |

-0.12 |

-0.14 |

|

||||||||||

Fixed Income |

1.20 |

1.16 |

1.11 |

1.04 |

0.97 |

0.91 |

0.85 |

0.82 |

-0.16 |

-0.15 |

CSA analysis of data obtained from investment fund managers and third party data providers. Asset and expense data were directly obtained from Investor Economics.

Declines in the asset-weighted average MERs and management fees were seen for funds of all three dominant broad asset classes, in both the pre- and post-implementation periods (refer to Tables 5.3.4 and 5.3.5). The asset-weighted average MER/management fee declines ranged from 8 to 18 basis points (or 5% to 13%) during the pre-implementation period, and 10 to 19 basis points during the post-implementation period (or 6% to 15%).

During both periods, changes in the distribution of assets across series played a larger role than reductions in MER/management fee rates in driving down the asset-weighted average MERs/management fees. Changes in the distribution of assets across series arising from sales contributed to lowering the asset-weighted average MERs/management fees. Conversely, changes in the distribution of assets attributable to investment returns had little impact on the asset-weighted average MERs/management fees.

The interaction effect for balanced series was close to zero in both the pre-and post-implementation periods. For equity and fixed income series, the interaction effect was negative. This was mainly attributable to the addition and termination of series over the period.

Table 5.3.4 Changes in the Asset-Weighted (AW) Average MERs by Select Broad Asset Classes

|

Balanced |

Equity |

Fixed Income |

|||||

|

||||||||

|

Chg '13-'16 |

Chg '17-'20 |

Chg '13-'16 |

Chg '17-'20 |

Chg '13-'16 |

Chg '17-'20 |

||

|

||||||||

AW Avg MER Chg |

-0.12 |

-0.12 |

-0.17 |

-0.19 |

-0.18 |

-0.17 |

||

|

||||||||

Fund Weight (FW) Effect |

-0.09 |

-0.11 |

-0.11 |

-0.14 |

-0.11 |

-0.08 |

||

|

||||||||

|

of which... |

|

|

|

|

|

|

|

|

||||||||

|

|

Sales Effect |

-0.09 |

-0.11 |

-0.11 |

-0.13 |

-0.11 |

-0.07 |

|

||||||||

|

|

Returns Effect |

0.00 |

-0.01 |

0.00 |

-0.01 |

0.00 |

-0.01 |

|

||||||||

Price Effect |

-0.02 |

-0.01 |

-0.03 |

-0.02 |

-0.02 |

-0.04 |

||

|

||||||||

FW + Price Effects |

-0.01 |

0.00 |

-0.03 |

-0.02 |

-0.04 |

-0.06 |

||

|

||||||||

Share of series with fund weight declines |

41% |

59% |

39% |

61% |

49% |

64% |

||

|

||||||||

Share of series with price declines |

53% |

50% |

63% |

56% |

55% |

58% |

||