3. Documentation:

(a) Final Order

(b) Reason for decision (Motion)

(c) Interim Orders

(d) Reply to MFDA

(e) Submission of staff of CIRO

(f) Hearing of the Merits

Ontario Securities Commission Bulletin

Issue 47/13 - March 28, 2024

Ont. Sec. Bull. Issue 47/13

• Cormark Securities Inc. et al.

• Latitude Uranium Inc. -- s. 1(6) of the OBCA

• YTM Capital Asset Management Ltd. and YTM Capital Fixed Income Alternative Fund

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Consolidation of ATS Protocol Orders -- Notice

• EquiLend Canada Corp. -- Cessation of ATS Business -- Notice

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Leszek Dziadecki et al. -- ss. 8, 21.7

FILE NO.: 2024-4

PROCEEDING TYPE: Application for Review

HEARING DATE AND TIME: April 2, 2024 at 10:00 a.m.

LOCATION: By videoconference

The purpose of this proceeding is to consider the application dated February 29, 2024 made by Leszek Dziadecki to review a decision of the Canadian Investment Regulatory Organization dated January 30, 2024.

The hearing set for the date and time indicated above is the first case management hearing in this proceeding, as described in subsection 17(6) of the Capital Markets Tribunal Rules of Procedure.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT ATTEND, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

Dated at Toronto this 22nd day of March, 2024.

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@capitalmarketstribunal.ca.

The Applicant, Leszek Dziadecki, request(s) that the Tribunal make the following order(s):

1. For hearing and review of a decision CIRO file #202230

The grounds for the request and the reasons for seeking a hearing and review are:

2. I do not agree with the decision of CIRO because:

During my professional career as a Financial Advisor and Certified Financial Planner I have recommended to the clients many investment opportunities. These recommendations have been based on my opinion and I trusted they would be beneficial for the clients. If I was not licensed to offer recommended investments, I referred the clients to qualified professionals. According to CFP Rules of Conduct for CFP Professionals "a CFP Professional shall offer advice to clients only in those areas in which he or she is competent. In areas where the CFP professional is not competent, the CFP professional shall seek the counsel of, and/or refer clients to, qualified professionals". (CFP Rules of Conduct #12)

The accusations of selling syndicated mortgage investments to the clients are false. Oxford definition of selling is "to give something to somebody in exchange for money".

According to Investopedia, selling is "a transaction that involves an exchange of goods or services for money" and I have not received any compensation for these transactions.

Advantage Group was approved as an outside business activity with Global Maxfin Investments. The disclosure form always stated that "MORTGAGE -- PROVIDED BY ANOTHER ASSOCIATE OF ADVANTAGE -- NO MONETARY BENEFIT". My associates who had licenses to sell insurance products also owned licenses to sell mortgages or been a tax accountant, but that doesn't mean that I was selling these products or that I was having a monetary benefit as well. Investments that I had been licensed to sell were processed either through my office or Global Maxfin Investments.

Let's state the facts:

- I did not sell SMI to the clients.

- I did not sign any documents relating to the sale of SMI.

- I did not process any of those transactions.

- I did not receive any compensation.

I met Edward Tsang a long time ago and yes, I had previous business dealings with him which didn't end well for me and for which I paid a high price. When Edward Tsang approached me with Bionorth business opportunity, based on previous experiences I told Edward Tsang that I cannot be involved in selling Bionorth SMI. However, I told him that I can put him in front of mortgage brokers from my office and let them decide if it would be an interesting product for them to sell.

Previously when I delt with Edward Tsang, I unfortunately decided to sell convertible debentures of his company prior to the approval of GMII. The fundamental difference is that at that time I DID sell debentures, sign all documents, and receive commission for it. When I was questioned by the OSC, I agreed with the allegations instantly and fully cooperated with OSC.

This is clearly not the case with Bionorth SMI!

I have never SOLD it!

My CFP registration allowed me to recommend products or services which in my opinion were valuable to clients. If you want to judge me for that, then I probably broke that rule 50 times a year by recommending services of my trusted accountant, real estate agent, mortgage broker, car mechanic etc., without written approval of GMII.

I was fully aware that I was not allowed to sell SMIs, so I never did.

During my radio programs I was talking about various investment products, not necessarily offered by my company or GMII. When I was talking about Bionorth SMI I expressed my positive opinion simply because it was secured by first mortgage with very low loan to value ratio of 40%.

I have built the trust and reputation within clients for running my company Advantage Group of Finance Inc. for the last 30 years. That was the first time my recommendation failed. However, I should not be responsible for wrong business decisions made by the management of Bionorth.

I want to correct some facts:

- I did not pray on the investors to have them invest in the Bionorth SMI or actively persuade them to do so,

- I did not say that the investment is 100% safe or guaranteed (I simply stated that is safer than other SMI because it is secured with first mortgage)

- I did not tell any of the clients I was leaving the Member

- I did not recommend clients to redeem mutual funds from their GMII accounts in order to invest in the Bionorth SMI. Clients who had accounts with ROI Capital (company moving out of Canada) received letters that Global Retirement Fund was closing, and money needs to be transfer somewhere else.

The Applicant intend(s) to rely on the following documents and evidence at the hearing:

3. Documentation:

(a) Final Order

(b) Reason for decision (Motion)

(c) Interim Orders

(d) Reply to MFDA

(e) Submission of staff of CIRO

(f) Hearing of the Merits

DATED this 29 day of February, 2024. |

Leszek Dziadecki |

800 -- 10 Kingsbridge Garden Cir. |

|

Mississauga, On L5R 3K |

|

905-206-9820; ext.225 |

|

Leszek.d@advantagegroup.org |

FOR IMMEDIATE RELEASE

March 21, 2024

TORONTO -- The Tribunal issued its Reasons and Decision in the above-named matter.

A copy of the Reasons and Decision dated March 20, 2024 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

March 22, 2024

TORONTO -- The Tribunal issued a Notice of Hearing to consider the application dated February 29, 2024 made by Leszek Dziadecki to review a decision of the Canadian Investment Regulatory Organization dated January 30, 2024.

A first case management hearing will be held on April 2, 2024 at 10:00 a.m. by videoconference.

Members of the public may observe the hearing by videoconference, by selecting the "Register to attend" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

A copy of the Notice of Hearing dated March 22, 2024 and the Application for Review dated February 29, 2024 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Cormark Securities Inc. et al.

FOR IMMEDIATE RELEASE

March 26, 2024

TORONTO -- The following merits hearing dates have changed in the above-named matter:

(1) the previously scheduled day of March 27, 2024 will not be used for the merits hearing; and

(2) the hearing will continue on April 11, 12, 15, 16, 17 and 30, 2024, May 1, 2, 3, 21, 22, 28, 29, 30, and 31, 2024, and June 3, 4, 5, 6, 10, 11, 12, 13, and 14, 2024 at 10:00 a.m. on each day.

The hearing will be held at the offices of the Tribunal at 20 Queen Street West, 17th floor, Toronto. Members of the public may observe the hearing by videoconference, by selecting the "Register to attend" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

For Media Inquiries:

For General Inquiries:

Phemex Limited and Phemex Technology Pte. Ltd.

FOR IMMEDIATE RELEASE

March 26, 2024

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated March 26, 2024 is available at capitalmarketstribunal.ca.

Members of the public may observe the hearing by videoconference, by selecting the "Register to attend" link on the Tribunal's hearing schedule, at capitalmarketstribunal.ca/en/hearing-schedule.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

March 26, 2024

TORONTO -- The Tribunal issued an Order in the above named matter.

A copy of the Order dated March 26, 2024 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

March 26, 2024

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated March 26, 2024 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Fawad Ul Haq Khan carrying on business as Forex Plus

FOR IMMEDIATE RELEASE

March 26, 2024

TORONTO -- The first case management hearing in the above-named matter scheduled to be heard on March 26, 2024 at 10:00 a.m. was adjourned due to technology issues.

The first case management hearing will be rescheduled on a date to be determined.

For Media Inquiries:

For General Inquiries:

Phemex Limited and Phemex Technology Pte. Ltd.

File No. 2023-22

Adjudicator: |

Cathy Singer |

March 26, 2024

WHEREAS on March 25, 2024, the Capital Markets Tribunal held a hearing by videoconference;

ON HEARING the submissions of the representatives for the Ontario Securities Commission (the Commission) and for the respondents, and on considering that the parties consent to the making of this order;

IT IS ORDERED THAT:

1. by no later than 4:30 p.m. on April 8, 2024, the respondents shall serve on the Commission a further and better summary of the expected evidence of Jifeng Ye (Ye) that complies with the requirements of Rule 28(3) of the Tribunal's Rules of Procedure and Forms, which witness summary shall include:

a. for each of the topic areas the respondents list in the witness summary dated February 28, 2024, the substance of Ye's expected evidence; and

b. the identification of the specific documents Ye is expected to refer to in his evidence;

2. the Commission shall serve and file a final sworn version of the affidavit of Cosmin Cazan by 4:30 p.m. on September 23, 2024;

3. the respondents shall serve and file a final sworn version of the affidavit of Ye by 4:30 p.m. on September 23, 2024;

4. each party shall serve the other party with a book of documents containing copies of the documents, and identifying the other things, that the party intends to produce or enter as evidence at the merits hearing, by 4:30 p.m. on August 20, 2024;

5. each party shall advise all other parties of any issues about the authenticity or admissibility of documents contained in the books of documents by 4:30 p.m. on August 27, 2024;

6. each party shall provide to the Registrar a completed copy of the Hearing Participant Checklist by 4:30 p.m. on August 27, 2024;

7. a further attendance in this matter is scheduled for September 4, 2024 at 10:00 a.m., by videoconference, or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat; and

8. the merits hearing shall take place on October 7, 2024 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, and continue on October 8, 9 and 10, 2024, commencing at 10:00 a.m. on each day, or on such other dates and times as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

File No. 2022-14

Adjudicator: |

Russell Juriansz |

March 26, 2024

WHEREAS on March 19, 2024, the Capital Markets Tribunal held a hearing by videoconference to schedule the hearing of a motion by the respondent Xiao Hua (Edward) Gong for a permanent stay of the proceeding;

ON HEARING the submissions of the representatives of the Ontario Securities Commission (the Commission) and of the respondent;

IT IS ORDERED THAT:

1. the motion is scheduled for October 15 and 16, 2024 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, or on such other date or time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat;

2. the parties shall adhere to the following timeline for the delivery of materials for the motion:

a. by 4:30 p.m. on June 20, 2024, the Commission shall serve and file any responding materials;

b. by 4:30 p.m. on August 1, 2024, Gong shall serve and file his written submissions;

c. by 4:30 p.m. on September 19, 2024, the Commission shall serve and file its responding written submissions; and

d. by 4:30 p.m. on September 26, 2024, Gong shall serve and file his reply written submissions.

File No. 2023-12

Adjudicator: |

James Douglas |

March 26, 2024

WHEREAS on March 21, 2024, the Capital Markets Tribunal held a hearing by videoconference;

ON HEARING the submissions of the representatives of the Ontario Securities Commission (the Commission) and for the respondents;

IT IS ORDERED THAT:

1. Pyo's motion to strike the statement of allegations and dismiss the proceeding against him (the Motion to Strike) is scheduled for April 25, 2024 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, or on such other date or time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat;

2. the parties shall adhere to the following timeline for the delivery of materials for the Motion to Strike:

a. by 4:30 p.m. on April 8, 2024, Pyo shall serve and file his submissions;

b. by 4:30 p.m. on April 15, 2024, the Commission shall serve and file its responding motion record, if any;

c. by 4:30 p.m. on April 17, 2024, the Commission shall serve and file its responding submissions;

d. by 4:30 p.m. on April 19, 2024, the parties shall complete cross-examinations, if necessary; and

e. by 4:30 p.m. on April 23, 2024, Pyo shall serve and file reply submissions, if any;

3. the Commission's motion for further and better witness summaries, filed on January 17, 2024 shall continue on April 25, 2024 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, or on such other date or time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat;

4. the parties shall deliver any expert reports in accordance with the following schedule:

a. the respondents shall serve their expert report(s), if any, on every other party by 4:30 p.m. on July 15, 2024;

b. the Commission shall serve their responding expert report(s), if any, on every other party by 4:30 p.m. on September 13, 2024;

5. the Commission shall serve on the respondents by 4:30 p.m. on May 31, 2024, a sworn version of an affidavit of its witness Bruce Meng; and shall serve and file a further or supplementary sworn version of Meng's affidavit by 4:30 p.m. on September 13, 2024;

6. the Commission shall serve and file final sworn versions of the affidavits of Anna Dunaevsky and Ria Sharma by 4:30 p.m. on September 13, 2024;

7. each party shall serve the other parties with a book of documents containing copies of the documents, and identifying the other things, that the party intends to produce or enter as evidence at the merits hearing, by 4:30 p.m. on August 14, 2024;

8. each party shall advise all other parties of any issues about the authenticity or admissibility of documents contained in the books of documents by 4:30 p.m. on August 23, 2024;

9. each party shall provide to the Registrar a completed copy of the Hearing Participant Checklist by 4:30 p.m. on August 23, 2024;

10. a further attendance in this matter is scheduled for August 29, 2024 at 10:00 a.m., by videoconference, or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat; and

11. the merits hearing shall commence on October 8, 2024 at 10:00 a.m., at the Capital Markets Tribunal located at 20 Queen Street West, 17th Floor, Toronto, Ontario, and continue on October 9, 10, 22, 23, 24, 29, 30, and 31, 2024, November 28, and 29, 2024, and December 2, 3, 12, 13, 16, 17, and 18, 2024, starting at 10:00 a.m. on each day, or on such other dates and times as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Mark Edward Valentine -- s. 127(1)

Citation: Valentine (Re), 2024 ONCMT 11

Date: 2024-03-20

File No. 2022-7

Adjudicators: |

Cathy Singer (chair of the panel) |

|

Dale R. Ponder |

||

Geoffrey D. Creighton |

||

|

||

Hearing: |

By videoconference, September 29, October 2, 3, 4, 10, 12 and December 21, 2023 |

|

|

||

Appearances: |

Andrew Faith |

For Staff of the Ontario Securities Commission |

Ryan Lapensee |

||

Sean Grouhi |

||

|

||

Janice Wright |

For Mark Edward Valentine |

|

Greg Temelini |

||

[1] In 2004, Mark Edward Valentine was banned by the Ontario Securities Commission from participating in Ontario's capital markets. Valentine was permanently banned from acting as a director or officer of an issuer (the D&O Ban) and banned from trading in securities for 15 years (the Trading Ban).

[2] Staff of the Commission alleges that Valentine breached these bans by:

a. acting as a director and officer of many Ontario corporations;

b. participating in the sale of over 5 million shares in a corporation called Flyp Technologies Inc. (the Flyp Sale); and

c. participating in several "Stock Secured Financings" or "Equity Loans";

and as a result, violated Ontario securities law.

[3] Valentine admits to the first two allegations and disputes the third.

[4] Staff also alleges that by engaging in the above conduct, Valentine engaged in conduct contrary to the public interest.

[5] For the reasons set out below, we find that Valentine:

a. breached the D&O Ban by acting as a director and/or officer of 38 Ontario corporations;

b. breached the Trading Ban by participating in the Flyp Sale; and

c. breached the Trading Ban by participating in Stock Secured Financings.

[6] Valentine is an Ontario resident with extensive experience in Ontario's capital markets. Valentine was a director, Chairman and the largest shareholder of the now defunct Thomson Kernaghan & Co. Ltd (TK).

[7] In 2002, following an internal investigation into its trading activity while under Valentine's stewardship, TK found that the "propriety of certain trades" was "questionable", that Valentine had "failed to provide any documents to support still other trades", and that an entire series of trades had no supportable rationale. TK took disciplinary action against Valentine and the firm subsequently declared bankruptcy.

[8] On December 16, 2004, Valentine entered into a settlement agreement with Staff of the Commission based on his breaches of Ontario securities law. On December 23, 2004, the Commission issued an order against Valentine imposing the following terms:

a. Valentine shall "resign all positions that he holds as a director or officer of an issuer";

b. Valentine is "permanently prohibited from becoming or acting as a director or officer of any issuer" (a. and b. collectively being the D&O Ban); and

c. the exemptions in Ontario securities law shall not apply to Valentine, and he shall "cease trading in securities for a period of 15 years", with limited carve-outs for personal trading of securities on defined exchanges (the Trading Ban).

[9] In 2020, Staff started an investigation into Valentine for potential breaches of the above settlement order and subsequently commenced this enforcement proceeding against Valentine in March 2022.

[10] Staff called three witnesses at the merits hearing in this proceeding:

a. Michael Ho, a senior forensic accountant in the Enforcement Branch of the Commission;

b. a former employee of Valentine (AP); and

c. a former business associate and friend of Valentine (SP).

[11] Part way through the hearing, the parties also jointly filed an agreed statement of facts for a fourth witness, a business associate and friend of Valentine (MS), which was marked as an exhibit at the hearing on consent.

[12] Though he made several admissions at the merits hearing, Valentine did not testify, and Staff filed transcript excerpts of his compelled interview with Staff.

[13] Valentine admits that he breached the D&O Ban. He does not, however, admit to any of the facts relating to that breach as set out in the Statement of Allegations. Therefore, Staff was required to prove this allegation with evidence.

[14] We are satisfied that Staff met its burden and find that Valentine breached the D&O Ban.

[15] Staff led its evidence of this breach through Ho's testimony. He detailed 38 corporations of which Valentine remained, or became, a director and/or officer over the period beginning on the date of the D&O Ban in 2004, up to the date this merits hearing began. Ho was cross-examined at some length to establish the "context of the breach" in respect of the specific corporations.

[16] In summary, Valentine was a director and officer of two corporations as of the date of the D&O Ban and failed to resign from those roles. Thereafter, over subsequent years, he became a director and/or officer of 36 corporations for various periods of time and continued to hold several of those roles up to the date this merits hearing began.

[17] Ho's evidence, together with the evidence that Staff read in from Valentine's compelled interview, established that the 38 corporations had a variety of purposes and degrees of activity. Some were largely inactive, and some were active. Some existed primarily to hold certain assets (such as an airplane, or pieces of real estate) and others were used in various business activities undertaken by Valentine.

[18] All of the corporations in issue were incorporated in Ontario. None of them were reporting issuers.

[19] Ho testified that his review of banking records disclosed that 13 of the corporations in issue had significant banking activity, which he defined as at least one transaction of $100,000 or more, or at least 10 transactions in a month for three different months in the period he reviewed.

[20] Two of the 13 corporations are notable due to the sheer size of transactions in their bank accounts: Thalerventures Ltd. (Thalerventures) and Pinnacle Global Partners Ltd. (PGP).

[21] Thalerventures was in the venture capital business. AP, Valentine's former employee, testified that the corporation had employees and an office in Toronto. Its banking activity was more significant than many of the corporations about which we heard testimony. For example, in 2015, it received a single transfer into its bank account of over $2 million. In 2015 and 2016, millions of dollars flowed through its bank accounts. Much of this financial activity related to the "stock secured financing" or "equity loan" transactions that are the subject of the third allegation in this proceeding.

[22] Similarly, PGP received in excess of US$11 million in 2015 and 2016. The parties dispute what those amounts were for, but it is enough to note the substantial dollar amount involved for purposes of fleshing out the context of the breach of the D&O Ban.

[23] Valentine took the position, in respect of three of the 38 corporations, that this proceeding is statute-barred by the six-year limitation period in s. 129.1 of the Securities Act (the Act).{1} He notes that his resignations from director and/or officer positions at Boomphones Inc., Lucky Air Ltd. And Premier Selling Technologies Inc. all occurred more than six years before the start of this proceeding.

[24] If the Statement of Allegations had laid out 38 separate alleged breaches of the D&O Ban, this submission might have had some weight. However, that is not what the Statement of Allegations does. It contains a single allegation in this regard, that "by remaining a director and officer of approximately two Ontario corporations and becoming a director or officer of approximately 36 Ontario corporations...Valentine breached the D&O Ban".

[25] The breach that is alleged is a single continuing course of conduct comprised of a series of contraventions from the moment the D&O Ban was issued until the date this proceeding was commenced (and which, in fact, continued up to the date this merits hearing began).

[26] Section 129.1 provides that no proceeding under the Act shall be commenced "later than six years from the date of the occurrence of the last event on which the proceeding is based." Staff submits that Heidary (Re) clarifies that this refers to the last event in the series of events which form the alleged course of conduct.{2} Boyle (Re), in turn, notes that a "course of conduct" includes three elements:

a. a pattern of conduct comprised of a series of acts;

b. over a period of time; and

c. evidencing a continuity of purpose.

A "continuity of purpose" requires that the subsequent acts be similar to the original act and in line with a person's original intent.{3}

[27] Staff argues, and we agree, that Valentine showed a pattern of conduct of acting as a director and/or officer of various Ontario corporations despite the D&O Ban. His conduct occurred over a period of time. The evidence also showed a "continuity of purpose" in that incorporating and managing the affairs of Ontario issuers was an integral part of Valentine's business activities throughout the period from the date of the D&O Ban to the date this proceeding was commenced, and beyond.

[28] In light of these findings, it is of no consequence that, for three out of 38 corporations, Valentine ceased to be a director or officer more than six years before the proceeding was commenced. The breach alleged in the Statement of Allegations has been established by the course of conduct, over a period of time, involving at one time or another each and every one of the 38 corporations.

[29] As noted above, because of Valentine's limited admission of the breach but not the underlying facts, Staff was required to lead evidence in respect of Valentine's impugned course of conduct.

[30] Valentine submits that the reason for the bare admission of the breach, but not the underlying facts, was that it was necessary to understand "the nature of the breach or the context of the breach in respect of the specific corporations that are in issue".

[31] When pressed, Valentine conceded that "there is going to be a mingling of facts germane to merits and facts germane to sanctions".

[32] As a result, Staff spent considerable time leading evidence to establish the activities of the corporations involved, their banking records, and the various activities in which they engaged.

[33] In closing submissions, however, Valentine urged the panel simply to find the admitted breach of the D&O Ban, and to go no further into the issue. Valentine submits that the evidence which Staff led as to the level of activity of the corporations, their banking records, and so forth is irrelevant in the merits stage. It can only have relevance to sanctions and this panel ought not to make findings only relevant to sanctions.

[34] We disagree. Merits panels, in the course of making findings as to the nature and extent of a respondent's conduct, will often make findings that are relevant to the subsequent sanctions phase. Indeed, in the ordinary course, sanctions panels typically ground their decisions on the factual findings of the merits panel without the need for extensive evidence at the sanctions stage.

[35] In this case, Valentine's decision not to admit any facts in the Statement of Allegations was explained by the desire to have the nature of the breach and the context of the breach put into evidence. That was done, and that is what our reasons are based upon. That there may be an intermingling of facts germane to merits and facts germane to sanctions is an expected and unremarkable result.

[36] Valentine also asserts that he has adduced mitigating evidence of his now admittedly incorrect interpretation of the D&O Ban. Staff counters that Valentine has adduced no direct evidence at all. Valentine chose not to testify and called no witnesses. All the evidence relied upon by Valentine was adduced in cross-examination of Staff's witnesses, or is based on exhibits introduced by Staff. Staff urges us to give no weight to self-serving hearsay statements allegedly made by Valentine to Ho, adduced through Ho's cross-examination.

[37] Generally, admissions against a party's interest should carry considerable weight. By contrast, self-serving statements by a party -- especially as to matters such as intention or state of mind -- should be approached with healthy skepticism. In this case, Valentine has declined to testify (as he is entitled to do), and in so doing has denied Staff the opportunity to cross-examine him on his understanding of the D&O Ban, and the source, plausibility and reasonableness of that understanding. The panel has not had the opportunity to assess Valentine's credibility as a witness. In these circumstances we give no weight to hearsay statements by Valentine concerning his misunderstanding of the D&O Ban.

[38] Based on the above, we are satisfied that Valentine breached the D&O Ban.

[39] Staff alleges that Valentine breached the Trading Ban by facilitating a transaction, described below, and referred to by the parties as the "Flyp Sale".

[40] Valentine admits that he breached the Trading Ban through his involvement in the Flyp Sale. However, just as with the first allegation, he did not initially admit any of the facts with respect to the Flyp Sale in the Statement of Allegations. Staff was again required to prove this allegation with evidence. We are satisfied that Staff met its burden and find that Valentine breached the Trading Ban.

[41] The Flyp Sale related to a sale of shareholdings in an Ontario corporation, Flyp Technologies Inc. (Flyp), for proceeds of approximately US$1.3 million. Despite that simple summary, Valentine's involvement in the transaction was somewhat convoluted, and he played an integral role in its completion.

[42] In the course of the hearing, the parties reached an agreement on one paragraph in the Statement of Allegations, and filed an Agreed Statement of Facts in respect of one of Staff's witnesses, MS.

[43] MS, a business associate and friend of Valentine, owned a British Virgin Islands corporation, Pecunia Holdings Limited (Pecunia BVI). It held shares in Flyp. In 2018, Flyp became involved in a financing transaction with a third party, and as a result, several existing shareholders of Flyp agreed to sell their shareholdings. Pecunia BVI was shown on the share register as one of those shareholders. However, by 2018 Pecunia BVI had been dissolved and no longer existed. This was a problem for MS, who asked Valentine to assist him in the sale of the Flyp shares.

[44] MS relied upon Valentine as an "agent" and "consultant" for the transaction. At MS's request, Valentine created a new Ontario corporation with an identical corporate name to Pecunia BVI -- Pecunia Holdings Limited (Pecunia Ontario). Valentine became Pecunia Ontario's sole director and officer.

[45] In that capacity, Valentine signed a Secondary Sale Share Purchase Agreement dated April 5, 2018, pursuant to which Pecunia Ontario purported to sell the 5,932,410 Flyp shares shown on Flyp's books as owned by Pecunia BVI, for US$1,364,454.30.

[46] Valentine also signed a Resolution of the Board of Directors and Shareholders, a Resolution of the Shareholders, a Waiver of Right of First Refusal, and a Release re the Secondary Sale Share Purchase Agreement.

[47] The proceeds of the sale, net of escrow and transaction fees, were approximately US$1.18 million. This amount was paid into Pecunia Ontario's US$ bank account on April 11, 2018. Thereafter, from April 16 through May 14, 2018, Pecunia Ontario transferred to Thalerventures and Dupont Family Office Ltd. (Dupont) about US$661,447 and US$178,390, respectively, for a total of US$839,837. These funds were some of the proceeds of the Flyp Sale.

[48] Valentine was president, secretary, treasurer and a director of Thalerventures. He was a director and 50% shareholder of Dupont. In his compelled interview, Valentine could not explain why these amounts were sent to Thalerventures and Dupont, and stated he "does not remember the purpose of the transfers".

[49] Ultimately, the proceeds of the Flyp Sale appear to have been distributed to MS and another individual who claimed entitlement. Staff did not allege, and did not attempt to establish, that Valentine received any compensation for his services in respect of the Flyp Sale.

[50] Staff alleges, and we find, that Valentine's involvement in the Flyp Sale was more than a casual favour to a friend. The motivation of Valentine throughout his participation in the Flyp Sale is not clear. What is clear is that he took an integral role in the sale of the Flyp shares, acting in furtherance of the trade, and thereby breached the Trading Ban.

[51] As with the breach of the D&O Ban, we give no weight to self-serving hearsay statements made by Valentine to Ho and adduced through Ho's cross-examination.

[52] Based on the above, we are satisfied that Valentine breached the Trading Ban by participating in the Flyp Sale.

[53] Staff alleges that Valentine also breached the Trading Ban by committing acts in furtherance of trades in the context of several transactions, referred to as "Stock Secured Financings" or "Equity Loans". We will refer to these transactions as the "Stock Secured Financings".

[54] As will become clear, the Stock Secured Financings were arrangements involving parties and transactions in various foreign jurisdictions. The allegations against Valentine, however, relate to his activities, and funds received, in Ontario. The allegations do not put in issue the propriety of any of the transactions themselves or the conduct of other parties under their local, or Ontario, laws. The allegations relate strictly to whether Valentine breached the Ontario Trading Ban. Neither Staff nor Valentine raised any issue concerning the offshore nature of some aspects of the transactions.

[55] Unlike the first two allegations, Valentine does not admit to this breach, nor did the parties reach any agreement on any of the alleged facts in the Statement of Allegations. Staff accordingly introduced evidence to establish the breach. In written closing submissions after the conclusion of the evidence, Valentine for the first time admitted and agreed to a number of facts alleged in the Statement of Allegations.

[56] We conclude that Valentine breached the Trading Ban through his involvement in the Stock Secured Financings for the following reasons.

[57] Though the parties varied, the Stock Secured Financings shared a general structure. An international lender would enter into an agreement with a borrower in Hong Kong. The borrower would pledge publicly-listed Hong Kong securities to the lender. The lenders themselves received funding from other international persons or entities.

[58] The borrowers were identified by an intermediary known as Great Wealth Asia (Great Wealth). The lenders to the borrowers were corporations known as Jendens Equity Finance Limited (Jendens) and Bretonnia Capital Corp. Ltd. (Bretonnia). Jendens and Bretonnia obtained their own funding from sources that included Pinnacle Global Partners I Fund Ltd. (PGP Fund), and a United Kingdom entity referred to in the evidence as GPP (the UK Financier). The principal of Jendens and PGP Fund was an individual we will refer to as SH.

[59] Valentine sat in the middle as an intermediary between PGP Fund and the UK Financier, on the one hand, and Great Wealth and the borrowers on the other.

[60] SP, a former business associate and friend of Valentine, was called as a witness by Staff. He was the only witness with direct involvement in these financings.

[61] SP testified that he acted as a consultant to Great Wealth. His role was to try to find lenders to fund borrowers sourced by Great Wealth. To do so, he would often approach Valentine, whom he testified "seemed to have the best handle on who would finance these types of things".

[62] Valentine gave similar evidence about his role in his compelled interview. He indicated he introduced SH to the principals of Great Wealth "for the purpose of financing and trading in stocks with respect to Asian equity loans". As will be described below, Valentine received compensation from Great Wealth for these introduction services.

[63] When asked what else he did in respect of the potential loans he would take to SH to consider funding, Valentine stated in his compelled interview that he would introduce his analysis of the corporation (meaning the Hong Kong corporations whose shares were being proposed to be pledged in return for loans). He described this as follows: "It would strictly be on the valuation, financial analysis, in terms of where the true potential value was".

[64] As summarized in the Statement of Allegations and admitted by Valentine in his written closing submissions, Valentine's roles in the Stock Secured Financings included sourcing financing from parties including PGP Fund and the UK Financier, analyzing pledged equities and assessing the parameters of the loans for the providers of funds, and facilitating communication among the parties.

[65] It is clear from the evidence that all the intermediaries and funding sources involved in the Stock Secured Financings (and perhaps many of the borrowers as well) anticipated that the loans would be satisfied by the sale of the pledged Hong Kong listed securities.

[66] SP, who represented Great Wealth on behalf of the borrowers, noted his understanding that the loans were "non-recourse". That meant the borrowers could "walk away whenever they want for whatever reasons they want". He indicated that the borrowers found this attractive.

[67] The parties funding the loans, ultimately PGP Fund and the UK Financier, understood that as well, and demonstrated it in their conduct.

[68] Two documents, a "Deal Summary" generated by Great Wealth, and a "Sales Spreadsheet", prepared by or for the UK Financier, summarize a number of the Stock Secured Financings and their administration.

[69] The Deal Summary sets out 16 different transactions. According to SP, Valentine was involved in most of those transactions. The document summarizes the transactions by reference not to the borrower, but to the ticker symbol of the pledged stock involved.

[70] The Deal Summary reveals that as of June 6, 2018, of the 16 transactions listed, all were in default. Of those, 11 had defaulted before the borrower ever made a single payment.

[71] This can be read in conjunction with the Sales Spreadsheet, dated March 2, 2016. Prepared by or for the UK Financier, it corresponds to six of the transactions listed in the Deal Summary, recording the sales of pledged shares. It was provided to Valentine by email from the UK Financier and sent on by him to SP. The email was entitled "Trades".

[72] The Sales Spreadsheet is identified not by borrower but by ticker symbol. It contains columns recording trade dates of the pledged shares, gross and net proceeds. At the bottom, the status for each stock is summarized in categories: "Bought", meaning the number of shares pledged, to which is ascribed the total amount advanced; "Sold", meaning the net proceeds of sale of the pledged shares; "Remaining", which notes whether any shares remain unsold; and finally, "Profit".

[73] In his compelled interview, Valentine explained his understanding that the "profit" on these transactions was "in essence...the net spread available after costs and agents from acquisition, disposition and funding". He confirmed that the "acquisition" and "disposition" referred to the pledged shares.

[74] Commenting on the Sales Spreadsheet, when asked why certain shares were being sold, Valentine explained "the lender would lend money with the understanding that they were going to be selling shares to pay down the loan". When then asked "are there other ways for the borrower to pay down the loan? Was it only in a default event where shares that were pledged were sold, or were there other circumstances that the shares can be sold?", Valentine replied "No, the shares could be sold at any time as per the lender's instructions".

[75] Far from being an unusual event, it is clear from the evidence that the expectation of Valentine, and those providing funding, was that the shares pledged under the Stock Secured Financings were being "acquired" and "disposed" of, to generate a profit.

[76] As now admitted by Valentine, his roles in the Stock Secured Financings included sourcing financing from parties including PGP Fund and the UK Financier; analyzing pledged equities and assessing the parameters of the loans for the providers of funds; and facilitating communication among the parties.

[77] In his compelled interview, Valentine described his analysis role as something he provided to the potential lenders as they considered a possible loan. "It would strictly be on the valuation, financial analysis, in terms of where the potential value was, if there were any research reports outstanding, to try and gather those reports and to understand if there was any institutional ownership in the underlying company." He confirmed he was analyzing the corporations of which shares were proposed to be pledged, not the proposed borrowers.

[78] His role, as Valentine described it, is entirely consistent with his understanding of the transactions (an understanding that he shared with the financiers): that the lender would be lending in the expectation that it was effectively acquiring the pledged shares for resale, to make a profit.

[79] Valentine received compensation for his involvement in the Stock Secured Financings. It was received through Thalerventures, and a new Ontario corporation he set up for the purpose of these transactions, called PGP.

[80] Valentine received compensation from Great Wealth, on the borrowers' side, and from PGP Fund on the lenders' side. At the time of his compelled interview, Valentine did not recall the details of his compensation in terms of the amounts paid to him or how it was structured.

[81] He did recall, however, that he was compensated by the lenders based on "a portion of the profitability of the transactions" (which he understood as the "net spread available after costs and agents, from acquisition, disposition and funding"). It was Valentine's expectation, and the fact, that he would be paid compensation if, as and when the lenders traded pledged shares for a profit. At no point did he, nor did any of evidence before us, suggest that his compensation was in any way tied to the interest received or fees paid in respect of the loan itself.

[82] He stated that he generally received a percentage amount of the profit, which he estimated to be in the range of 25% to 35%. He stressed, however, that there was no contractual obligation on which his compensation was based: it was "a fluid number", "not a fixed cost percentage". He stated it was "verbal for everybody". Accordingly, there was no documentary record of the basis or quantum of his compensation. He received compensation both from the financier side, and sometimes from Great Wealth as well.

[83] Valentine stated that he had little memory of the amounts he received as compensation from either PGP Fund or Great Wealth. In each case, when questioned, he was only willing to narrow it down to something greater than $1 million but less than $10 million.

[84] Staff led evidence of banking records of Thalerventures and PGP, Valentine's corporations, which showed receipt of funds from Great Wealth, and from PGP Fund. The evidence shows that Great Wealth paid $3,257,639.75 and US$807,696.00 to Valentine's corporations. Valentine did not challenge these amounts and confirmed that all amounts received from Great Wealth were related to the Stock Secured Financings.

[85] The banking records also show that Valentine's corporation, PGP, over the period of the Stock Secured Financings, received transfers from PGP Fund in the amount of US$11,294,805.00. Valentine disputes that all of this relates to Stock Secured Financings. He has conceded that four of the transfers, totaling US$2,549,940, were in respect of fees paid on those transactions, but challenges the rest.

[86] Valentine submits that the allegation that the full US$11,294,805 relates to Stock Secured Financings is "contrary to the Statement of Allegations". We disagree. The Statement of Allegations clearly alleges receipt by PGP of that precise amount, and notes the descriptions accompanying the transfers. It then states that "at least four" of the transfers, being those already conceded by Valentine at that point, were in respect of the loans. The amounts received, up to the US$11,294,805, were clearly in issue as a matter to be addressed by evidence.

[87] The payments from PGP Fund to PGP were affected by wire transfers, each of which included "details" inserted by the payor. There were 13 transfers over the period from December 2015 to December 2016, a period which corresponds to most of the Stock Secured Financings. The "details" in each case reference a specific Hong Kong listed security, by ticker number. All of those ticker numbers correspond to loans shown on the Deal Summary referred to above (with one exception, which was one of the payments Valentine conceded was related to the loans).

[88] The "details" are all some variant of "Acquisition of Stock HK[number]", "Purchase of HK[number]", "Funds Required for Purchase of HK[number] Security", or "Brokerage Fees Acquisition HK[number]". The four transfers conceded by Valentine comprise three referencing an acquisition and one referencing brokerage fees.

[89] These details were inserted by PGP Fund, a third party, and there is no evidence to question their accuracy. They are consistent with Valentine's description of the Stock Secured Financings as involving the acquisition and disposition of the Hong Kong stocks. They share the same ticker numbers as the Deal Summary and relate to the same time period.

[90] In response to undertakings given during his compelled interview, Valentine disavowed the "details" and gave his alternative description of what the transfers related to. In most cases, though, his notation is simply "fees" or "fees with a performance clause" -- and these are descriptions which applied equally to those amounts he conceded were in respect of payments for his role in Stock Secured Financings.

[91] The only exception is two transfers, in the amounts of US$1,013,985.00 and US$1,149,985.00, which he indicated were forwarded by PGP Fund as payment for the "purchase of real estate on 121 Scollard Avenue (back parking lot) from Terranatta". In further answers to undertakings, to provide back up for this stated use of the funds, Valentine referenced two cheques payable to Terranatta Corp in the aggregate amount of US$1,370,000, which is less than the aggregate of the two transfers in issue.

[92] Based on the evidence, we conclude that the transfers from PGP Fund to PGP, detailed in the banking records and summary tendered in evidence by Staff, were compensation paid to Valentine in respect of his involvement in the Stock Secured Financings. The only exception is the US$1,370,000 which Valentine asserts was for the purpose of purchasing property for PGP Fund.

[93] In the result, we conclude that Valentine received, in total, at least $3,257,639.75 and US$807,696.00 from Great Wealth, and US$9,924,805 from PGP Fund in respect of payments for his services in the Stock Secured Financings.

[94] We have described the structure of the Stock Secured Financings, how they operated in practice, Valentine's roles in them and his compensation for those roles. That leaves the question whether his involvement in those transactions was a breach of the Trading Ban. The answer depends on whether or not he acted "in furtherance of a trade". That in turn requires an analysis of both whether the transactions involved a "trade", and if his conduct was "in furtherance of" those trades.

[95] The definition of "trade" or "trading" in the Act is broad. It is defined, inclusively, in several detailed subsections. The first subsection includes "any sale or disposition of a security for valuable consideration...but does not include a purchase of a security, or, except as provided by clause (d), a transfer, pledge or encumbrance of securities for the purpose of giving collateral for a debt made in good faith".{4}

[96] Valentine relies upon the second portion of the definition, which carves out pledges for giving collateral for a debt made in good faith. In Valentine's submission, that carve-out in the definition provides a safe harbour for the Stock Secured Financings. He submits that "the language in the definition of 'trade' expressly limits its ambit so as not to catch secured lending agreements".

[97] In Valentine's submission, the carve-out in the definition extends to those transactions necessary to administer, and indeed contemplated in, the loan agreements themselves: namely, the issuance of the loan agreement itself, the pledge of securities to the lender, and the potential sale by the lender of pledged securities to satisfy indebtedness.

[98] As support, Valentine cites Taylor v OSC.{5} In Taylor, the Divisional Court considered an appeal from a Tribunal decision that determined that an issue of promissory notes was not a "good faith loan", but rather, a scheme to sell shares "in the guise of a loan". As a result, the Tribunal found that the shares pledged in connection with the promissory notes did not benefit from the carve-out in the definition of trading and violated the prospectus requirements of the Act. In dismissing the appeal, the Court stated:

Under the Act, good faith loans are exempt from the definition of trading. Specifically, s.1(1) of the Act defines 'trade' or 'trading' as including:

(a) any sale or disposition of a security for valuable consideration...but does not include...a transfer, pledge or encumbrance of securities for the purpose of giving collateral for a debt made in good faith.{6}

[99] Valentine stresses in particular the first sentence of this excerpt, for the general proposition that good faith loans are exempt from the definition of trading. As explained below, this is too broad a view of the carve-out in the definition of a "trade".

[100] Staff, on the other hand, urges us to find three ways in which the Stock Secured Financings were "trades":

a. First, it submits the loans were not loans made "in good faith", that they were in substance the purchase and sale of publicly traded shares.

b. Second, it submits that the anticipated, and actual, sales of the pledged shares by the lenders were separate trades.

c. Third, it submits that the loans themselves were securities in the Act's definition, as a "note or other evidence of indebtedness", and their initial issue was a 'trade' and also a 'distribution'.

[101] Valentine contests each of these submissions. He submits that it is far too late for Staff to take the position for the first time that the loans are not "loans in good faith", that such an allegation is not made in the Statement of Allegations, and that allowing it now would be a breach of natural justice.

[102] With respect to the third branch of Staff's submission, Valentine counters that interpreting the issuance of every secured loan to constitute a 'trade' or 'distribution' of a security would render the carve-out for pledges meaningless.

[103] The issues raised by Staff's first and third submissions, and Valentine's responses, are challenging, and both parties have addressed them ably in their submissions. We do not find it necessary, however, to resolve those issues to determine whether the Stock Secured Financings involved a 'trade'.

[104] Staff's second submission focuses on the sale of the pledged securities by the lender. In our view, that sale is a 'trade' in its own right. Each Stock Secured Financing in which the lender sold the listed Hong Kong securities, involved a trade.

[105] When pressed by the panel during oral submissions, Valentine reiterated that the sale of the pledged securities is part and parcel of the loan transaction. If the loan benefits from the carve-out in the definition of "trade", then no part of 'the legitimate loan activity' should be labelled a trade. Valentine went so far as to assert that the panel should "extrapolate the scope of the exemption to address all that could be required under a bona fide loan".

[106] This is, in our view, too expansive a view of the carve-out in the definition of "trade" in s. 1(1)(a) of the Act for pledges of securities The carve-out is specific to, and covers only, the pledge itself. It does not apply to the different ways in which a pledgee may deal with the pledged securities. Nor does it apply to the issuance of debt itself. Each of those dealings is a separate transaction which must be tested to determine if it is, itself, a trade within the Act's definition.

[107] Complex transactions typically involve many distinct transactional elements. Some elements may involve trades, others may not. Some may be trades but benefit from carve-outs or exemptions. It is important to examine each component of a transaction to test how it should be treated under the Act. Issuing a loan document, conveying securities by way of a pledge to secure debt, and disposing of securities held as collateral are each separate transactional elements to be analyzed independently.

[108] Valentine gives too broad an interpretation to the statement made by the Court in Taylor. First of all, the statement was made in a context where the "good faith" aspect of the loan, in its inception, was the key issue on which the matter turned, and on which the Court confirmed the ruling of the Tribunal. The facts in that case did not involve a sale of pledged shares. The issue in that case was whether the loan was made in good faith, so that therefore the pledge of shares could benefit from the carve-out. The persistence of the carve-out at a later stage was not in issue, because the entire transaction was challenged as not involving a good faith loan. Secondly, the sentence appears as a brief, perhaps overly paraphrased, introduction to the specific language of s.1(1)(a), immediately following. We do not interpret the case as establishing, in one sentence of obiter, that all transactions consequent on a good faith loan are themselves excluded from the definition of trade, given the absence of any words to that effect in the definition itself.

[109] In this case, each of the Stock Secured Financings involved at least one clear 'trade': the sale by the pledgee of the Hong Kong listed securities that were conveyed to the pledgee under the loan agreements. The pledge itself may have benefited from the carve-out in the definition of 'trade', in that the borrower was not "trading" when it pledged the shares. But that carve-out does not extend to the subsequent decision of the pledgee to sell the shares.

[110] Moreover, this trade was an integral aspect of the Stock Secured Financings as they operated in practice, and as Valentine and the lenders understood them to operate.

[111] The definition of "trading" under the Act includes "any act...directly or indirectly in furtherance of" any of the other definitions of "trading". This is commonly called, simply, acts in furtherance of a trade.

[112] The Tribunal has adopted a contextual approach when determining whether acts are in furtherance of a trade, examining "the totality of the conduct, including the surrounding circumstances, the impact of the conduct and the proximity of the acts to actual or potential trades in securities".{7}

[113] Acts in furtherance of a trade do not require a completed sale of a security.{8} The Tribunal has found that "there must be at a minimum something done for the purpose of furthering or promoting the sale or disposition". While not necessary, the "receipt of consideration or some other direct or indirect benefit" can be a "strong indication" of an act in furtherance of a trade.{9}

[114] We are satisfied that Valentine's admitted conduct through his involvement in the Stock Secured Financings meets the test for engaging in acts in furtherance of a trade. In particular, he acted in furtherance of the trades made (or anticipated to be made) by the pledgees of the Hong Kong securities that were pledged under the loan agreements.

[115] He was frank that his compensation was calculated based on the "profit" realized by the lenders when they proceeded to sell the pledged securities. He apparently did not receive any compensation from the lenders based on the entering into of the loan agreements, nor on the lenders' receipt of fees or any other metric grounded in the loan itself. Compensation was related to the sales of shares and any profits realized from them.

[116] Valentine described the analysis he provided at the time a lender was making a decision whether or not to fund a loan. As noted above, that analysis was a financial analysis of the underlying pledged securities, including what their potential value was on a sale. It was not an analysis of the borrowers, but rather of the shares which Valentine knew the lenders intended to sell. He said that "the lender would lend money with the understanding that they were going to be selling shares to pay down the loan" and that "the shares could be sold at any time as per the lender's instructions".

[117] Given his clear understanding of how the loans would work in practice, including that any compensation for himself would likely depend on a profitable sale of pledged shares, Valentine was clearly providing his introduction, facilitation and analytic services in furtherance of that intended trade. In doing so, he repeatedly breached the Trading Ban by his participation in the Stock Secured Financings.

[118] We conclude therefore that Valentine breached the Trading Ban through his participation in the Stock Secured Financings. The conduct which constitutes that breach was the basis on which he received millions of dollars in compensation as described in section 4.3.3.b above.

[119] Staff alleges that Valentine engaged in "conduct contrary to the public interest" by engaging in the misconduct we have outlined above.

[120] Valentine asks us to dismiss this allegation given the lack of particulars provided by Staff in support.

[121] As the Tribunal has previously noted,{10} the words "contrary to the public interest" do not appear in the Act. In this proceeding, Staff has proven breaches of the D&O Ban and Trading Ban, which are themselves contraventions of the Act. Staff has not identified any additional conduct that would warrant an order under s. 127 of the Act. As such, we dismiss this additional allegation against the respondent.

[122] For the reasons above, we find that Valentine breached both the D&O Ban and the Trading Ban.

[123] We therefore require that the parties contact the Registrar by 4:30 p.m. on April 5, 2024, to arrange an attendance, to schedule a hearing regarding sanctions and costs, and the delivery of materials in advance of that hearing. The attendance is to take place on a mutually convenient date that is fixed by the Governance & Tribunal Secretariat, and that is no later than April 19, 2024.

[124] If the parties are unable to present a mutually convenient date to the Registrar, each party may submit to the Registrar, for consideration by a panel of the Tribunal, a one-page written submission regarding a date for the attendance. Any such submission shall be submitted by 4:30 p.m. on April 5, 2024.

Dated at Toronto this 20th day of March, 2024

{1} RSO 1990, c S.5

{2} (2000) 23 OCSB 959 at para 22

{3} 2006 ONSEC 5 at para 48

{4} Act, s 1(1)(a)

{5} 2013 ONSC 6495 (Div Ct) (Taylor)

{6} Taylor at para 18

{7} VRK Forex & Investments Inc (Re), 2022 ONSEC 1 at para 42

{8} First Federal Capital (Canada) Corporation (Re), 2004 ONSEC 2 at paras 45-51

{9} Anderson (Re), 2004 ONSEC 13 at para 34

{10} Solar Income Fund Inc (Re), 2021 ONSEC 2 at paras 70-76

CSA Staff Notice 25-311 -- 2023 Annual Activities Report on the Oversight of Canadian Investment Regulatory Organization and Canadian Investment Protection Fund

CSA Staff Notice 25-311 2023 Annual Activities Report on the Oversight of Canadian Investment Regulatory Organization and Canadian Investment Protection Fund is reproduced on the following internally numbered pages. Bulletin formatting and pagination resumes at the end of the Staff Notice.

March 28, 2024

TABLE OF CONTENTS

1 |

2023 Highlights |

3 |

|

|

|||

2 |

Who We Are |

4 |

|

|

|||

3 |

Executive Summary |

6 |

|

|

|||

4 |

What We Do |

7 |

|

|

|||

5 |

Post-Close Initiatives |

9 |

|

|

|||

6 |

Who We Regulate |

|

|

|

(A) |

Canadian Investment Regulatory Organization |

11 |

|

(B) |

Canadian Investor Protection Fund |

16 |

|

|||

7 |

Composition of Oversight Committees |

19 |

|

|

|||

8 |

Rule/By-law/Policy and Procedures Amendments |

20 |

|

|

|||

9 |

Questions |

22 |

|

The Canadian Securities Administrators (CSA) is the council of Canada's provincial and territorial securities regulators. Its objective is to improve, coordinate and harmonize regulation of the Canadian capital markets to ensure the smooth operation of Canada's securities industry and protect investors.

Applicable legislation in each province and territory provides a securities regulator with the power to recognize a self-regulatory organization through a Recognition Order. There is currently one recognized self-regulatory organization responsible for investment dealers and mutual fund dealers (SRO), the Canadian Investment Regulatory Organization (CIRO), which operates as a successor to the Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA). IIROC and the MFDA amalgamated to continue as the New Self-Regulatory Organization of Canada (New SRO), effective January 1, 2023, which subsequently changed its name to CIRO on June 1, 2023.

There is currently one approved/accepted investor protection fund (IPF), the Canadian Investor Protection Fund (CIPF) formed through the amalgamation of two protection funds, the former Canadian Investor Protection Fund and the MFDA Investor Protection Corporation, on January 1, 2023. Analogous to the recognition of CIRO, CIPF has been approved/accepted{1} through Approval Orders.

CIRO is recognized and CIPF is approved/accepted by the securities regulatory authorities in all thirteen provinces and territories (the Recognizing Regulators or RRs).

Acronym |

Name of Recognizing Regulator |

BCSC |

British Columbia Securities Commission |

ASC |

Alberta Securities Commission |

FCAA |

Financial and Consumer Affairs Authority of Saskatchewan |

MSC |

Manitoba Securities Commission |

OSC |

Ontario Securities Commission |

AMF |

Autorité des marchés financiers |

FCNB |

Financial and Consumer Services Commission of New Brunswick |

NSSC |

Nova Scotia Securities Commission |

PEI |

Prince Edward Island Office of the Superintendent of Securities |

NL |

Office of the Superintendent of Securities, Digital Government and Service Newfoundland and Labrador |

YT |

Office of the Yukon Superintendent of Securities |

NT |

Office of the Superintendent of Securities, Northwest Territories |

NU |

Office of the Superintendent of Securities, Nunavut Office |

We are pleased to share CSA Staff Notice 25-311 2023 Annual Activities Report on the Oversight of Canadian Investment Regulatory Organization and Canadian Investor Protection Fund (Report), our Report which summarizes the key activities through which we conduct oversight of CIRO and CIPF.

This Report covers the period of January 1 -- December 31, 2023 (the Reporting Period).

The amalgamations to form CIRO and CIPF were the result of the CSA's in-depth review of the SRO framework and started in 2019. After extensive stakeholder consultations and the publication of a consultation paper, which sought public input on key issues identified, CSA Position Paper 25-404 New Self-Regulatory Organization Framework was published on August 3, 2021 (Position Paper). The CSA took the position that the establishment of a new single enhanced SRO and, separately, the consolidation of the two IPFs into a single protection fund, independent from the SRO, is the best solution to address the issues that had been identified and to provide a framework for efficient and effective regulation in the public interest at this point and, as the capital markets continue to evolve, into the foreseeable future.

Much of our focus during the Reporting Period has been to work on various solutions outlined in the Position Paper to be implemented after the close of the amalgamation transactions. The nine post-close initiatives are being conducted alongside of our continuing regular oversight, which includes our review of amendments to CIRO rules and CIPF policies and by-laws; review of required filings from CIRO and CIPF; and the CSA's 2023 Oversight Review of specific processes in three functional areas of CIRO. Post-close initiatives will continue to be an area of focus in 2024.

This Report is an important tool for engaging with our stakeholders. We hope that the Report in its new format will serve to: (i) improve transparency; (ii) foster public confidence in the regulatory framework; and (iii) explain our role in overseeing CIRO's and CIPF's compliance with securities regulation requirements. We welcome any questions or feedback that you may have.

The oversight of CIRO is coordinated through a Memorandum of Understanding (MOU) among the RRs. The MOU describes the oversight program used by the RRs to: (i) oversee CIRO's performance of its self-regulatory activities and services; and (ii) ensure that CIRO is acting in the public interest and complying with the terms and conditions of its Recognition Orders.

A similar MOU exists for the oversight of CIPF.

Each MOU sets out that two RRs are designated as coordinators, tasked with the role of coordinating, communicating and scheduling activities of the oversight program between the RRs, and between the RRs and CIRO or CIPF (Coordinators).

The Coordinators serve for four years on a staggered rotation basis among the two designated RRs. During the Reporting Period, BCSC and OSC were designated as the inaugural Coordinators by consensus of all the RRs. One of two Coordinators will be replaced and thereafter each Coordinator will have a four-year term.

As required by each MOU the following oversight committees have been established:

• The CSA Market Regulation Steering Committee (MRSC) is the forum for coordination and providing updates where issues relate to both CIRO and CIPF.

• Oversight committees for CIRO and CIPF (Oversight Committees) are operational committees under the oversight of MRSC. Each Oversight Committee acts as forum to discuss issues, concerns and proposals related to the oversight of their respective entities. The committees included representatives from RRs, with the Coordinators serving as the leads.

Components of the SRO and IPF oversight program are outlined below.

Oversight Function |

Activities During the Reporting Period |

|

|

||

Annual Risk Assessment |

• |

Evaluation of each entity's potential inherent risks and mitigating controls in each functional area of the entity. |

|

• |

Evaluation can become the basis of future oversight activities. |

|

||

Review of Proposed Rules |

• |

CIRO is required to seek approval from the RRs for proposed new rules, policies, and constating documents (collectively, the rules) and by-laws, and any changes to existing rules and by-laws. |

|

• |

CIPF is required to seek approval or non-objection of any changes to certain policies (e.g., coverage policy) and its by-laws. |

|

• |

A "housekeeping" rule change is one that has no material impact on investors, issuers, registrants, CIRO, CIPF, or the Canadian capital markets generally (e.g., changes of an editorial nature; changes necessary to conform to applicable securities legislation, statutory or legal requirements, accounting or auditing standards). |

|

• |

If a rule change is not classified as housekeeping, it is published for public comment. |

|

||

Review of Materials Filed |

• |

CIRO and CIPF are responsible for filing certain information (other than proposed rules or by-laws) with each RR. |

|

• |

This information includes, but is not limited to, reports on financial condition, regulatory self-assessment, risk management, systems integrity, market surveillance, internal audit, progress on compliance examination results, and enforcement matters. |

|

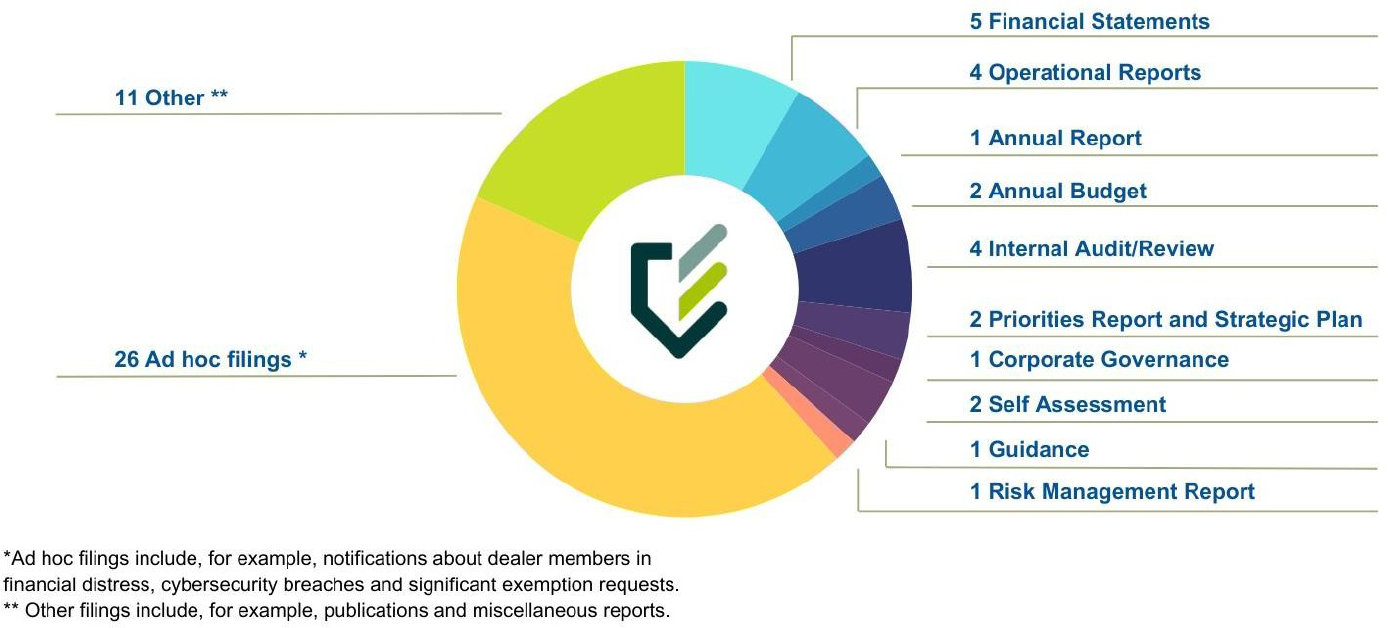

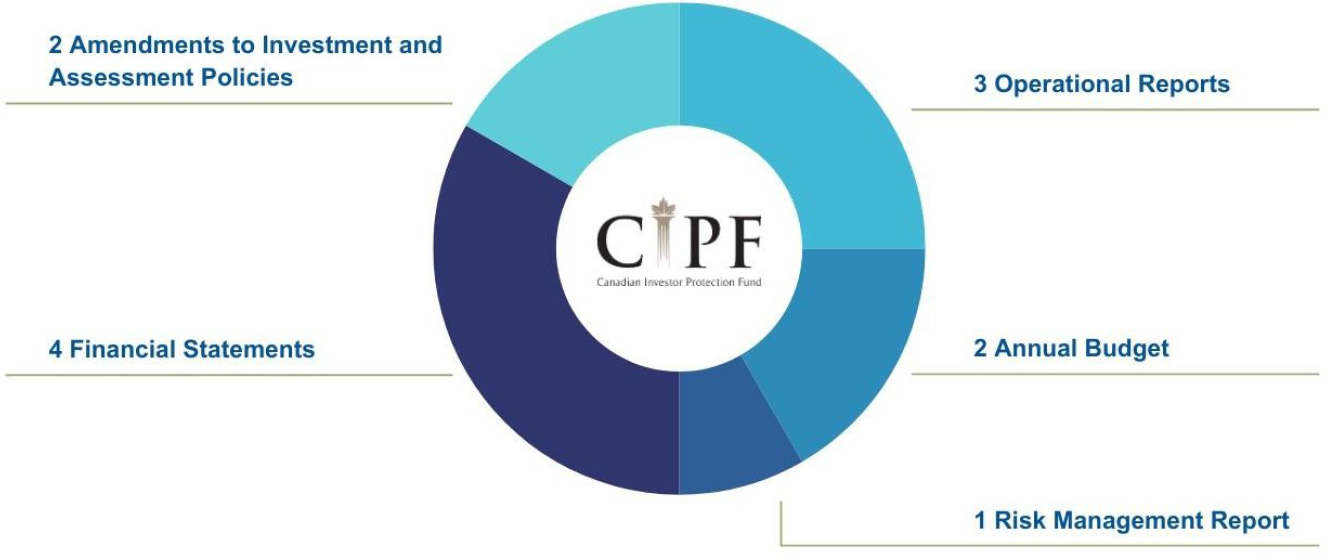

• |

During the Reporting Period, 72 filings were reviewed. |

|

• |

Staff of the RRs (Staff) reviewed issues and the materials filed, which informed the annual risk assessment. |

|

||

Meetings |

• |

During the Reporting Period, quarterly meetings were scheduled with CIRO and semi-annual meetings with CIPF to discuss the oversight process and to share information about emerging and/or ongoing regulatory issues and trends. |

|

• |

In addition to regularly scheduled bi-weekly meetings with CIRO and CIPF, numerous ad hoc meetings were held throughout the Reporting Period as part of the oversight of specific issues -- primarily relating to the integration of the predecessor SROs and, separately, the predecessor IPFs, as well as proposed rule amendments and filing requirements. |

|

||

Oversight Reviews |

• |

A more in-depth process for Staff to make an independent assessment of whether and how CIRO or CIPF have met their regulatory obligations. |

|

• |

The scope of an oversight review is determined by the results of the annual risk assessment and/or specific issues that arise on a periodic basis. |

|

• |

As part of an oversight review, Staff may interview CIRO or CIPF staff, review written policies and procedures to understand the systems and processes in place, and examine files on a sample basis. |

|

• |

During the Reporting Period, the RRs jointly completed a risk-based oversight review of CIRO that targeted specific processes within the areas of: (i) corporate governance; (ii) trading review and analysis; and (iii) financial compliance of investment dealers and mutual fund dealers. The results of the oversight review have been published in a separate report also on March 28, 2024. |

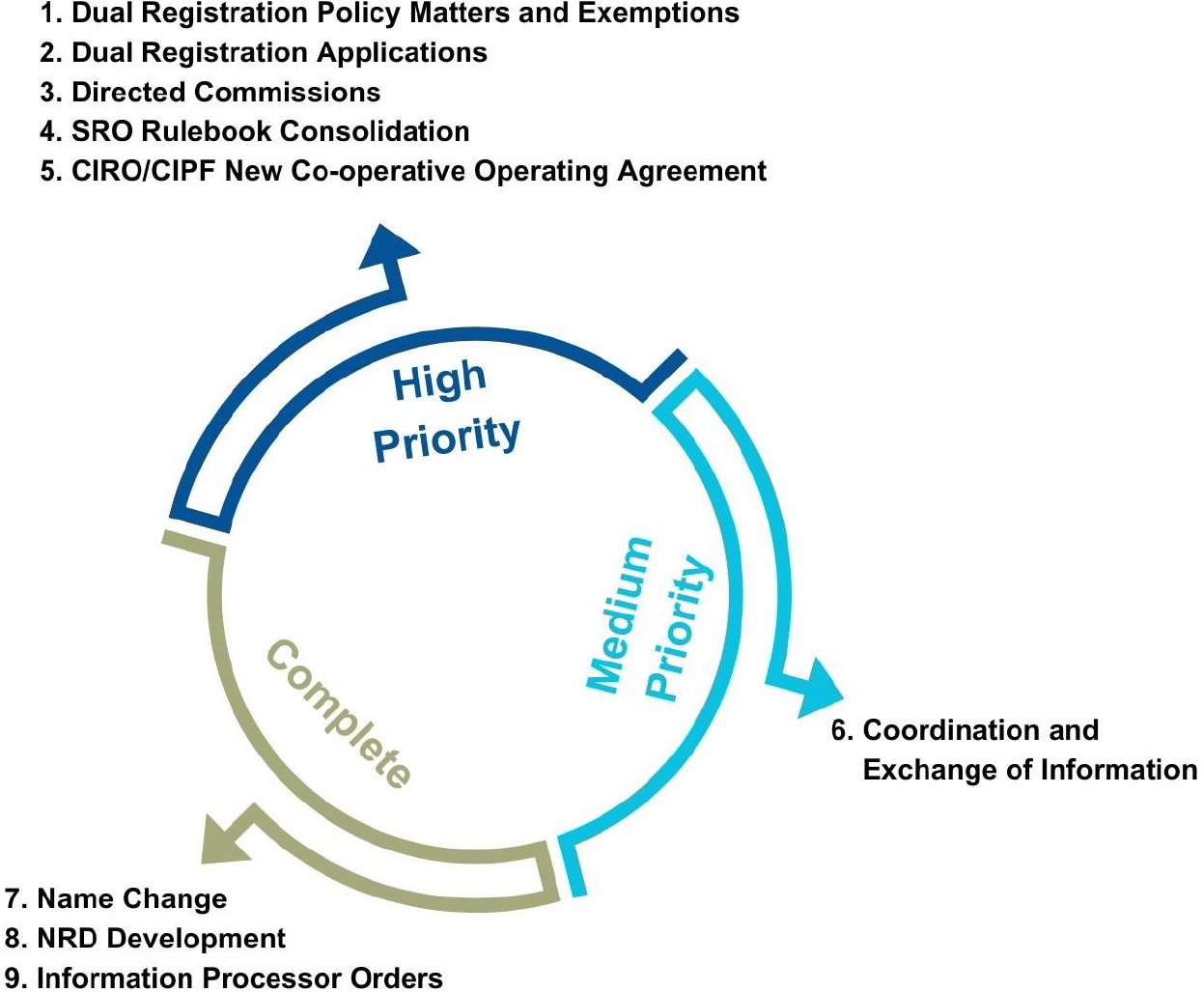

After the amalgamation of the predecessor SROs and IPFs, during the Reporting Period, the Oversight Committees continued to work on various solutions outlined in the Position Paper, published on August 3, 2021, to be implemented after the closing of the transactions. The Oversight Committees' work included monitoring post-close transition and implementation initiatives of varying priorities, as set out below.

|

Post-close Initiative |

Priority / Status |

Scope |

|

|

||||

1. |

Dual registration policy matters and exemptions |

High |

• |

CSA is considering dual registration matters and whether there are any potential challenges associated with these applications. Staff and CIRO staff are discussing novel issues related to the dual registration of investment dealers and mutual fund dealers. |

|

||||

2. |

Dual registration applications |

High |

• |

CSA and CIRO are working to complete an internal guide for reviewing dual registration applications. As policy issues are identified, they are being discussed among Staff working on Initiative #1 (dual registration policy matters and exemptions) and #2 (dual registration applications). |

|

||||

3. |

Directed commissions |

High |

• |

CSA is monitoring steps that CIRO is proposing relating to the compensation of investment dealing representatives and mutual fund dealing representatives, including the publication on January 25, 2024 of a position paper requesting public comments on CIRO's proposed approaches. |

|

||||

4. |

SRO rulebook consolidation |

High |

• |

Staff to review and recommend for approval CIRO proposals to consolidate and harmonize the rulebooks for investment dealers and mutual fund dealers over five phases, which commenced in late 2023. |

|

||||

5. |

CIRO/CIPF New Co-operative Operating Agreement |

High |

• |

In 2022, the predecessor SROs and IPFs entered into a Transitional Agreement, that came into effect on January 1, 2023, designed to ensure that existing arrangements between the predecessor entities would continue to govern the relationship between CIRO and CIPF. |

|

|

|

• |

CSA is monitoring the negotiation of the new Co-operative Operating Agreement, which will establish the respective responsibilities of CIPF and CIRO. |

|

||||

6. |

Coordination and exchange of information |

Medium |

• |

CSA continues to engage CIRO on the coordination and exchange of information, regarding the supervision of market related data and other information. |

|

||||

7. |

Name change |

Complete |

• |

The name change to CIRO was completed in July 2023, with changes made to the Recognition Orders, MOU, and SEDAR+.{2} |

|

||||

8. |

National Registration Database (NRD) development |

Complete |

• |

NRD development to automate the dual registration process and enhancements to improve clarity with regard to dual-registered dealer firms. |

|

||||

9. |

Information processor orders |

Complete |

• |

Variation and restatement of the information processor's Designation Order, effective June 1, 2023, to reflect the SRO amalgamation. |

The RRs have given CIRO, as an SRO, the responsibility to govern the operations and business conduct of investment dealers and mutual fund dealers and their representatives, and the trading activity on members of CIRO that are marketplaces. The authority of CIRO to carry out certain regulatory functions is set out in the Recognition Orders, along with the terms and conditions that CIRO is to comply with in carrying out its regulatory functions.

As of December 31 |

2023 |

2022 |

% Change |

|

|

||||

Assets Under Management |

$4.5 Trillion |

$4.1 Trillion |

9.8% |

|

|

||||

Approved Persons |

109,777 |

108,987 |

0.7% |

|

|

||||

Firms |

|

|

|

|

|

Investment Dealer |

169 |

173 |

|

|

Mutual Fund Dealer |

82 |

83 |

|

|

Dually Registered |

4 |

0 |

|

|

Total |

255 |

256 |

- 0.4% |

The increase in CIRO's assets under management was mainly attributable to an increase in equity markets during the Reporting Period.

The following diagram represents the distribution of member firms by head office location.