Ontario Securities Commission Bulletin

Issue 46/37 - September 14, 2023

Ont. Sec. Bull. Issue 46/37

• Phemex Limited and Phemex Technology Pte. Ltd. -- ss. 127(1), 127.1

• Derek Scheinman -- ss. 127(1), 127(10)

• Traders Global Group Inc. and Muhammad Murtuza Kazmi -- ss. 127(1), 127(8)

• Phemex Limited and Phemex Technology Pte. Ltd.

• Traders Global Group Inc. and Muhammad Murtuza Kazmi

• Go-To Developments Holdings Inc. et al.

• Go-To Developments Holdings Inc. et al.

• Traders Global Group Inc. and Muhammad Murtuza Kazmi

• Traders Global Group Inc. and Muhammad Murtuza Kazmi -- ss. 127(1), 127(8)

• OSC Staff Notice 81-734 -- Summary Report for Investment Fund and Structured Product Issuers

• Absolute Software Corporation

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Amendments to Multilateral Instrument 25-102 Designated Benchmarks and Benchmark Administrators

• Changes to Companion Policy 25-102 Designated Benchmarks and Benchmark Administrators

• Amendments to National Instrument 14-101 Definitions

• Amendments to National Instrument 33-109 Registration Information

• Amendments to National Instrument 45-106 Prospectus Exemptions

• Changes to Companion Policy 52-107CP Acceptable Accounting Principles and Auditing Standards

• Amendments to National Instrument 81-102 Investment Funds

• Amendments to Ontario Securities Commission Rule 14-501 Definitions

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Phemex Limited and Phemex Technology Pte. Ltd. -- ss. 127(1), 127.1

FILE NO.: 2023-22

PROCEEDING TYPE: Enforcement Proceeding

HEARING DATE AND TIME: September 26, 2023 at 10:00 a.m.

LOCATION: By videoconference

The purpose of this proceeding is to consider whether it is in the public interest for the Capital Markets Tribunal to make the order(s) requested in the Statement of Allegations filed by Staff of the Commission on September 5, 2023.

The hearing set for the date and time indicated above is the first attendance in this proceeding, as described in subsection 5(1) of the Capital Markets Tribunal Practice Guideline.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT ATTEND, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

Dated at Toronto this 6th day of September, 2023

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@osc.gov.on.ca.

1. The Enforcement Branch of the Ontario Securities Commission brings this proceeding to hold Phemex Limited and Phemex Technology Pte. Ltd. (collectively, the Respondents) accountable for disregarding Ontario securities law and to signal that crypto asset trading platforms flouting Ontario securities law will face regulatory action.

2. The Respondents operated an online crypto asset trading platform under the trade name "Phemex" (the Phemex Platform) on which Ontario investors could trade in securities and derivatives based on exposure to underlying assets that included crypto assets. The Phemex Platform was available to Ontario residents at least during the period between November 25, 2019 and January 6, 2023 (Material Time). Since on or about January 7, 2023, the Phemex Platform is no longer accessible to investors using an Ontario internet protocol (IP) address.

3. The Respondents are subject to Ontario securities law because, prior to January 7, 2023, the Phemex Platform offered crypto asset products that are securities and derivatives to investors, including Ontario investors. They nonetheless failed to comply with the registration and prospectus requirements under Ontario securities law.

4. Registration and disclosure are cornerstones of Ontario securities law. The registration requirement serves an important gate-keeping function by ensuring that only properly qualified and suitable persons are permitted to engage in the business of trading. Prospectus requirements are fundamental to ensuring investors are provided with full, true and plain disclosure of all material facts relating to the securities being offered.

5. Entities such as the Respondents that do not comply with Ontario securities law expose investors to unacceptable risks and create an uneven playing field within the crypto asset trading platform sector.

Staff of the Enforcement Branch of the Ontario Securities Commission (Enforcement Staff) make the following allegations of fact:

6. The Phemex Platform went live on or around November 25, 2019.

7. During the Material Time, the Phemex Platform could be accessed through the website located at www.phemex.com and through mobile apps on the Google and Apple app stores.

8. Investors accessed the Phemex Platform by first creating an account on the platform using an online application process which does not require know-your-client information such as name, phone number and address.

9. After opening an account, an investor could deposit crypto assets into the account. Investors made crypto asset deposits by transferring crypto assets to a wallet controlled by the Respondents. Through third parties identified on the Phemex Platform, investors were also provided with the option to purchase crypto assets using fiat currency, including Canadian dollars.

10. During the Material Time, the Respondents maintained custody of crypto assets deposited and traded on the Phemex Platform in wallets they controlled. Investors did not have possession or control of crypto assets deposited or traded on the Phemex Platform. Rather, they saw a crypto asset balance displayed in their account on the Phemex Platform. In order to take possession of crypto assets reflected in their account balance, an investor was required to request a withdrawal and was dependent on the Respondents to satisfy that withdrawal request by delivering crypto assets to an investor-controlled wallet.

11. While the Respondents purported to facilitate trading of the crypto assets in its investors' accounts, in practice, they only provided their investors with instruments or contracts involving crypto assets. These instruments or contracts constitute securities and derivatives.

12. During the Material Time, investors were also able to trade crypto asset futures contracts on the Phemex Platform that constitute securities and derivatives. The Phemex Platform allowed investors to engage in leveraged trading of up to 100:1 on various futures contracts.

13. The Phemex Platform offered bonuses, fee discounts and other promotions to solicit trading by investors. The Phemex Platform also employed a multi-level recruiting strategy named the "Phemex All-Star Program" which encouraged existing investors to refer new investors to the Phemex Platform in exchange for commissions based on trading fees collected from those referrals.

14. The Phemex Platform charged fees for trades on the platform and for crypto asset withdrawals.

15. Phemex Limited and Phemex Technology Pte. Ltd. operated the Phemex Platform during the Material Time.

16. Phemex Limited is a company incorporated under the laws of the British Virgin Islands. An archived version of the Phemex Platform's Terms of Use dated March 18, 2020 states that "Phemex is a platform operated by Phemex Limited".

17. Phemex Technology Pte. Ltd. is a company incorporated under the laws of Singapore. It has been identified on the Google and Apple app stores as the developer of the mobile apps associated with the Phemex Platform.

18. Phemex Technology Pte. Ltd. is a wholly owned subsidiary of Phemex Limited.

19. The Respondents have never been registered with the Commission in any capacity or obtained an exemption from the registration requirement. The Respondents have also never filed a prospectus with the Commission or obtained an exemption from the prospectus requirement.

20. The Phemex Platform was accessible to Ontario residents during the Material Time. The Commission's investigation team was able to open an account on the Phemex Platform and conduct transactions.

21. On or about January 3, 2023, Phemex added Ontario to its list of restricted locations in the Phemex Platform's Terms of Use, after being contacted by the Commission's investigation team regarding its activities in Ontario. No notification about this change was sent to investors.

22. On or about January 7, 2023, the Respondents implemented a restriction based on IP addresses to purportedly restrict Ontario residents from accessing the Phemex Platform (IP Address Restriction).

23. Existing investors impacted by the IP Address Restriction were not notified of the reason for the IP Address Restriction. In particular, the Respondents did not notify existing investors that Ontario residents were prohibited from using the Phemex Platform.

24. In addition, the Respondents did not provide any guidance to existing investors impacted by the IP Address Restriction on how to withdraw their assets held on the Phemex Platform in light of the IP Address Restriction.

25. Prior to the implementation of the IP Address Restriction, as of January 6, 2023, the Phemex Platform had a total of 117 accounts for investors who: (a) self-identified as Ontario residents; and/or (b) primarily accessed their accounts using an Ontario IP address (Ontario Accounts). These investors traded the products offered on the Phemex Platform, as described above, in the Ontario Accounts.

26. In total, the Respondents obtained at least 39,712.43 USDT (a.k.a. Tether) in fees from the Ontario Accounts based on total trading volume in those accounts which exceeded 74 million USDT.

27. Enforcement Staff allege the following breaches of Ontario securities law and conduct contrary to the public interest:

(a) Phemex Limited and Phemex Technology Pte. Ltd. each engaged in, or held itself out as engaging in, the business of trading in securities without the necessary registration or an applicable exemption from the registration requirement, contrary to subsection 25(1) of the Securities Act, RSO 1990, c. S.5, as amended (the Act);

(b) Phemex Limited and Phemex Technology Pte. Ltd. each engaged in trading in securities which constitute distributions without complying with the prospectus requirements and without an applicable exemption from the prospectus requirements, contrary to section 53 of the Act; and

(c) In addition to breaching Ontario securities law as outlined above, Phemex Limited and Phemex Technology Pte. Ltd. each acted in a manner contrary to the fundamental purposes and principles of the Act as set out in sections 1.1 and 2.1 of the Act, and contrary to the public interest. Specifically, by engaging in the business of trading in securities through the Phemex Platform without the necessary registration, prospectus or exemptions from those requirements and by making the Phemex Platform available in Ontario, the Respondents undermined safeguards intended to protect investors from unfair, improper or fraudulent practices. Furthermore, by failing to comply with the registration and prospectus requirements before offering securities to Ontario residents, with which other crypto asset trading platforms are required to comply, at a cost, the Respondents undermined the fairness, efficiency, and confidence in the Ontario capital markets.

28. These allegations may be amended, and further and other allegations may be added as the Capital Markets Tribunal (the Tribunal) may permit.

29. Enforcement Staff request that the Tribunal make the following orders against the Respondents:

(a) that they cease trading in any securities or derivatives permanently or for such period as is specified by the Tribunal, pursuant to paragraph 2 of subsection 127(1) of the Act;

(b) that they be prohibited from acquiring any securities permanently or for such period as is specified by the Tribunal, pursuant to paragraph 2.1 of subsection 127(1) of the Act;

(c) that any exemptions contained in Ontario securities law do not apply to them permanently or for such period as is specified by the Tribunal, pursuant to paragraph 3 of subsection 127(1) of the Act;

(d) that they submit to a review of their practices and procedures and institute such changes as may be ordered by the Tribunal, pursuant to paragraph 4 of subsection 127(1) of the Act;

(e) that they be reprimanded, pursuant to paragraph 6 of subsection 127(1) of the Act;

(f) that they be prohibited from becoming or acting as a registrant, as an investment fund manager or as a promoter permanently or for such period as is specified by the Tribunal, pursuant to paragraph 8.5 of subsection 127(1) of the Act;

(g) that they pay an administrative penalty of not more than $1 million for each failure to comply with Ontario securities law, pursuant to paragraph 9 of subsection 127(1) of the Act;

(h) that they disgorge to the Commission any amounts obtained as a result of non-compliance with Ontario securities law, pursuant to paragraph 10 of subsection 127(1) of the Act;

(i) that they pay the costs of the Commission investigation and the hearing, pursuant to section 127.1 of the Act; and

(j) such other orders as the Tribunal considers appropriate in the public interest.

DATED this 5th day of September, 2023. |

ONTARIO SECURITIES COMMISSION |

20 Queen Street West, 22nd Floor |

|

Toronto, ON M5H 3S8 |

|

Alvin Qian |

|

Litigation Counsel |

|

Email: aqian@osc.gov.on.ca |

|

Tel: (416) 263-3784 |

Derek Scheinman -- ss. 127(1), 127(10)

FILE NO.: 2023-23

PROCEEDING TYPE: Inter-jurisdictional Enforcement Proceeding

HEARING DATE AND TIME: In writing

The purpose of this proceeding is to consider whether it is in the public interest for the Capital Markets Tribunal to make the order(s) requested in the Statement of Allegations filed by Staff of the Commission on September 6, 2023.

Take notice that Staff of the Commission has elected to proceed by way of the expedited procedure for a written hearing provided for by Rule 11(3) of the Capital Markets Tribunal Rules of Procedure and Forms.

Staff must serve on you this Notice of Hearing, the Statement of Allegations, Staff's hearing brief containing all documents Staff relies on, and Staff's written submissions.

You have 21 days from the date Staff serves these documents on you to file a request for an oral hearing, if you do not want to follow the expedited procedure for a written hearing.

Otherwise, you have 28 days from the date Staff served these documents on you to file your hearing brief and written submissions.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT PARTICIPATE, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

Dated at Toronto this 6th day of September, 2023

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@osc.gov.on.ca.

1. An inter-jurisdictional enforcement is sought based on a holding of the Ontario Court of Justice (the OCJ) that Derek Scheinman (Scheinman) engaged in a fraud where he defrauded his business partners and investors of approximately $23 million.

2. This order is sought using the expedited procedure for inter-jurisdictional proceedings set out in Rule 11(3) of the Capital Markets Tribunal's (the Tribunal) Rules of Procedure and Forms.

3. Scheinman is a resident of Thornhill, Ontario. He owned and operated a mortgage investment company called DMS Financial Management (DMS) from its offices in Richmond Hill, Ontario. He was previously registered with the OSC between April 12, 2000 and July 25, 2002.

4. Scheinman was charged for offenses taking place between August 2, 2006, to March 22, 2017 relating to transactions, business or a course of conduct related to securities.

5. On February 5, 2021, Scheinman pled guilty to two counts of fraud over $5,000 contrary to section 380(1)(a) of the Criminal Code of Canada (CCC) before the Honourable Justice P. Bourque of the Ontario Court of Justice.

6. On September 24, 2021, Justice Bourque sentenced Scheinman to a four-year sentence less four months credit for time served. Justice Bourque ordered Scheinman be prohibited for five years from seeking, obtaining or continuing any employment, or becoming or being a volunteer in any capacity, that involves having authority over the real property, money or valuable security of another person, pursuant to s. 380.2 of the CCC.

7. The Tribunal is requested to make an inter-jurisdictional enforcement order reciprocating Scheinman's conviction, pursuant to paragraph 1 of subsection 127(10) of the Ontario Securities Act, RSO 1990, c S.5, as amended (the Act).

8. Scheinman defrauded partners in Grossman Silver Horizon Limited Partnership (the Grossman Partnership) of approximately $13,000,000. He and his spouse funded a lavish lifestyle including gambling, luxury vacations, properties, and shopping sprees with this money.

9. In 2006, Scheinman formed the Grossman Partnership as an Ontario partnership. The limited partners were Pinecap Mortgage Corporation and 2106271 Ontario Inc. (the Limited Partners). DMS was the general partner. The Grossman Partnership's purpose was to invest in and manage mortgages.

10. The Limited Partners funded the Grossman Partnership while Scheinman managed the day-to-day operations of the Grossman Partnership. The Limited Partners had $33,000,000 invested into the Grossman Partnership at one point. In addition to compensation received for his services, DMS and the Limited Partners also entered into a profit-sharing agreement.

11. In 2015, the Limited Partners discovered a discrepancy of $800,000 including several unusual payments relating to a cottage and a condo in Florida both owned by Scheinman. The Limited Partners decided to dissolve the partnership and subsequently retained a lawyer and a forensic accountant.

12. 28 mortgages totaling more than $9,000,000 were revealed to be fictitious. Some real mortgages were discharged but Scheinman reported them to the Limited Partners as still outstanding. Unbeknownst to the Limited Partners, Scheinman opened additional bank accounts for the Grossman Partnership. He had sole signing authority for those accounts and monies meant to fund the mortgages flowed into these accounts.

13. Scheinman used the funds to (i) send money to companies controlled by Scheinman, his spouse, and unrelated third parties; (ii) pay for the expenses of three properties registered to relatives; (iii) pay for his credit card debt; and (iv) withdraw $600,000 in cash.

14. Separately, Scheinman also operated a Ponzi scheme, defrauding investors of $10,000,000 and diverted this money to his spouse and her business, and used it to purchase personal properties in Florida.

15. Scheinman operated another mortgage investment company called New Horizon Investment Management Corporation (New Horizon). New Horizon purportedly invested in mortgages as a security for loans for residential real estate and investment properties in Canada. Scheinman had promised New Horizon investors an unrealistic rate of return.

16. There are approximately 30 known investors in New Horizon. They received subscription agreements and share certificates in exchange for their investment. The investors believed that they were investing in mortgages backed by residential real estate.

17. In reality, Scheinman failed to make mortgage investments for years. Instead, he operated a Ponzi scheme where he paid older investors with funds provided by newer investors to maintain the façade of real investment returns. When Scheinman could not make interest payments from the contributions of new investors, he either failed to make the interest payments or he used funds from the Grossman Partnership. Between 2004 and 2017, Scheinman defrauded New Horizon and its investors of approximately $10,000,000.

18. Pursuant to paragraph 1 of subsection 127(10) of the Act, Scheinman's conviction for offences arising from transactions, business or a course of conduct related to securities or derivatives may form the basis for an order in the public interest made under subsection 127(1) of the Act.

19. It is in the public interest to make an order against Scheinman.

20. The Tribunal reserves the right to amend these allegations and to make such further and other allegations as the Tribunal deems fit and the Tribunal may permit.

21. The Tribunal is requested to make the following inter-jurisdictional enforcement order, pursuant to paragraph 1 of subsection 127(10) of the Act:

a. against Scheinman that:

i. pursuant to paragraph 2 of subsection 127(1) of the Act, trading in any securities or derivatives by Scheinman cease permanently;

ii. pursuant to paragraph 2.1 of subsection 127(1) of the Act, acquisition of any securities by Scheinman be prohibited permanently;

iii. pursuant to paragraph 3 of subsection 127(1) of the Act, any exemptions contained in Ontario securities law do not apply to Scheinman permanently;

iv. pursuant to paragraphs 7, 8.1 and 8.3 of subsection 127(1) of the Act, Scheinman resign any positions that he holds as a director or officer of any issuer or registrant;

v. pursuant to paragraphs 8, 8.2 and 8.4 of subsection 127(1) of the Act, Scheinman be prohibited permanently from becoming or acting as a director or officer of any issuer or registrant;

vi. pursuant to paragraph 8.5 of subsection 127(1) of the Act, Scheinman be prohibited permanently from becoming or acting as a registrant or promoter; and

b. such other order or orders as the Tribunal considers appropriate.

DATED this 6th day of September, 2023. |

|

|

|

Hansen Wong |

|

Litigation Counsel |

|

Enforcement Branch |

|

LSO No. 76486D |

|

Tel: 647-202-7312 |

|

Email: hwong@osc.gov.on.ca |

|

Traders Global Group Inc. and Muhammad Murtuza Kazmi -- ss. 127(1), 127(8)

FILE NO.: 2023-21

PROCEEDING TYPE: Application for Extension of Temporary Order

HEARING DATE AND TIME: September 13, 2023 at 10:00 a.m.

LOCATION: By videoconference

The purpose of this proceeding is to consider whether the Capital Markets Tribunal should grant the Application filed by Staff of the Commission to extend the temporary order issued by the Ontario Securities Commission on August 29, 2023.

Any party to the proceeding may be represented by a representative at the hearing.

IF A PARTY DOES NOT ATTEND, THE HEARING MAY PROCEED IN THE PARTY'S ABSENCE AND THE PARTY WILL NOT BE ENTITLED TO ANY FURTHER NOTICE IN THE PROCEEDING.

This Notice of Hearing is also available in French on request of a party. Participation may be in either French or English. Participants must notify the Tribunal in writing as soon as possible if the participant is requesting a proceeding be conducted wholly or partly in French.

L'avis d'audience est disponible en français sur demande d'une partie, que la participation à l'audience peut se faire en français ou en anglais et que les participants doivent aviser le Tribunal par écrit dès que possible si le participant demande qu'une instance soit tenue entièrement ou partiellement en français.

Dated at Toronto this 7th day of September, 2023

For more information

Please visit capitalmarketstribunal.ca or contact the Registrar at registrar@osc.gov.on.ca.

(For Extension of a Temporary Order Under Subsections 127(1) and 127(8) of the Securities Act, RSO 1990 c S.5)

The Applicant, Staff of the Ontario Securities Commission (the Commission), requests that the Capital Markets Tribunal (the Tribunal) make the following orders:

1. An Order extending the Temporary Order of the Commission dated August 29, 2023 (Temporary Order) made with respect to Traders Global Group Inc. (TGG) and Muhammad Murtuza Kazmi (Kazmi) for such period as it considers necessary pursuant to subsection 127(8) of the Securities Act, RSO 1990, c S.5 (the Act);

2. If necessary, an Order abridging the time required for service pursuant to Rules 3 and 4(2) of the Tribunal's Rules of Procedure and Forms; and

3. Such other Order as the Tribunal considers appropriate in the public interest.

The grounds for the request are:

1. In January 2023, the Enforcement Branch commenced its current investigation into TGG and Kazmi following a Request for Assistance from the United States Commodities Futures Trading Commission (CFTC);

2. During the course of the investigation, the Enforcement Branch found evidence of the following:

(a) From at least November 1, 2021 and continuing to the present (the Material Time), TGG, an Ontario based federal corporation, TGG has operated as "My Forex Funds" on its website myforexfunds.com (the MFF Website), and represented itself as a retail foreign exchange and commodities trading firm;

(b) Kazmi, an Ontario resident, is the principal of TGG;

(c) The MFF Website offers retail investors, who pay funds to open accounts, the opportunity to become a "professional trader," trade foreign exchange and commodities using third-party "liquidity providers" and share in any trading profits;

(d) There is virtually no real trading taking place at TGG. For the vast majority of investors, trading is simulated by TGG with various rules in place designed to benefit TGG to the detriment of investors;

(e) TGG and Kazmi appear to have raised at least USD 294 million from at least 135,000 investors worldwide;

(f) TGG and Kazmi may have used money received from investors to pay simulated "profits" to other investors and for Kazmi's personal expenses;

(g) TGG and Kazmi are continuing to raise funds from investors; and

(h) Each of the accounts offered on myforexfunds.com is a security as an "investment contract" under s. 1(1)(n) of the Act or is otherwise a "security" or a "derivative" under s. 1(1) of the Act;

3. During the course of the investigation, the Enforcement Branch found evidence that:

(a) TGG and Kazmi may have engaged in conduct that perpetrates a fraud in breach of subsection 126.1(1)(b) of the Act;

(b) TGG may be engaged in the business of trading securities without registration, contrary to subsection 25(1) of the Act;

(c) TGG may have distributed securities without filing a prospectus, contrary to subsection 53(1) of the Act; and

(d) TGG and Kazmi may have provided false and misleading information to the Commission, contrary to subsection 122(1)(a) of the Act;

4. On August 28, 2023, the CFTC filed a Complaint for Injunctive Relief, Civil Monetary Penalties and Other Equitable Relief against TGG, Kazmi and a related TGG entity located in New Jersey, in the United States District Court for the District of New Jersey (the CFTC Proceeding);

5. As part of the CFTC Proceeding, the CFTC filed a motion for a Statutory Restraining Order and Preliminary Injunction, which, among other things, sought certain asset freezes, appointment of a temporary receiver over TGG and Kazmi, and a preliminary injunction. The motion was granted by the U.S. District Court on August 29, 2023;

6. On August 29, 2023, the Commission issued the Temporary Order;

7. The Temporary Order provided that:

(a) all trading in any securities of TGG shall cease;

(b) all trading in any securities by TGG and Kazmi, or by any person their behalf, including but not limited to any act, advertisement, solicitation, conduct, or negotiation, directly or indirectly in furtherance of a trade, shall cease;

(c) any exemptions contained in Ontario securities law do not apply to TGG or Kazmi; and

(d) the Temporary Order shall take effect immediately and shall expire on the 15th day after its making unless extended by order of the Tribunal;

8. The investigation into the conduct described in the Temporary Order and this Application is continuing and is the subject of the CFTC Proceeding;

9. The Order sought by the Commission is necessary to protect investors from serious and ongoing harm and is in the public interest;

10. Subsections 127(1) and 127(8) of the Act; and

11. Such further grounds as counsel may advise and the Tribunal may permit.

The Applicant intends to rely on the following evidence at the hearing:

1. The Affidavit of Louisa Fiorini, sworn September 6, 2023 and its exhibits;

2. The Affidavit of Matthew Edelstein, sworn September 1, 2023 and its exhibits;

3. The Affidavit of Stephanie Collins, sworn September 5, 2023 and its exhibits; and

4. Such further evidence as counsel may advise and the Tribunal may permit.

Date: September 6, 2023 |

|

|

|

ONTARIO SECURITIES COMMISSION |

|

|

|

Sarah McLeod |

|

Litigation Counsel |

|

Tel: (416) 303-2638 |

|

Email: smcleod@osc.gov.on.ca |

|

|

|

Hansen Wong |

|

Litigation Counsel |

|

Tel: (647) 202-7312 |

|

Email: hwong@osc.gov.on.ca |

|

Phemex Limited and Phemex Technology Pte. Ltd.

FOR IMMEDIATE RELEASE

September 6, 2023

TORONTO -- The Tribunal issued a Notice of Hearing on September 6, 2023 setting the matter down to be heard on September 26, 2023 at 10:00 a.m. or as soon thereafter as the hearing can be held in the above-named matter.

A copy of the Notice of Hearing dated September 6, 2023 and Statement of Allegations dated September 5, 2023 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

September 6, 2023

TORONTO -- The Tribunal issued a Notice of Hearing pursuant to Subsections 127(1) and 127(10) of the Securities Act in the above-named matter.

A copy of the Notice of Hearing dated September 6, 2023 and Statement of Allegations dated September 6, 2023 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Traders Global Group Inc. and Muhammad Murtuza Kazmi

FOR IMMEDIATE RELEASE

September 7, 2023

TORONTO -- The Tribunal issued a Notice of Hearing on September 7, 2023 setting the matter down to be heard on September 13, 2023 at 10:00 a.m. to consider whether the Capital Markets Tribunal should grant the Application filed by Staff of the Commission to extend the temporary order issued by the Ontario Securities Commission on August 29, 2023.

A copy of the Notice of Hearing dated September 7, 2023 and Application dated September 6, 2023 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Go-To Developments Holdings Inc. et al.

FOR IMMEDIATE RELEASE

September 8, 2023

TORONTO -- The Tribunal issued its Reasons and Decision in the above-named matter.

A copy of the Reasons and Decision dated September 7, 2023 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Go-To Developments Holdings Inc. et al.

FOR IMMEDIATE RELEASE

September 11, 2023

TORONTO -- Take notice that an attendance in the above named matter is scheduled to be heard on September 13, 2023 at 9:00 a.m.

For Media Inquiries:

For General Inquiries:

Traders Global Group Inc. and Muhammad Murtuza Kazmi

FOR IMMEDIATE RELEASE

September 11, 2023

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated September 11, 2023 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

September 12, 2023

TORONTO -- Take notice of the merits hearing time change on September 14, 2023, in the above-named matter. The hearing on September 14, 2023, scheduled to commence at 10:00 a.m. will instead commence at 11:00 a.m.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

September 12, 2023

TORONTO -- Take notice of the merits hearing time change on September 13, 2023, in the above-named matter. The hearing on September 13, 2023, scheduled to commence at 10:00 a.m. will instead commence at 11:00 a.m.

For Media Inquiries:

For General Inquiries:

Traders Global Group Inc. and Muhammad Murtuza Kazmi -- ss. 127(1), 127(8)

File No. 2023-21

Adjudicator: |

James Douglas (chair of the panel) |

September 11, 2023

WHEREAS Staff of the Ontario Securities Commission brought an application before the Capital Markets Tribunal to extend a temporary order dated August 29, 2023 (the Temporary Order);

ON READING the materials filed by Staff, and on being advised that the parties consent to an order on the following terms extending the Temporary Order and adjourning the application hearing originally scheduled for September 13, 2023;

IT IS ORDERED THAT:

1. the Temporary Order is extended until 4:30 pm on October 31, 2023; and

2. the hearing of the application is scheduled for October 30, 2023 at 10:00 a.m., by videoconference, or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Go-To Developments Holdings Inc. et al. -- Rule 27(3) of the Capital Markets Tribunal Rules of Procedure and Forms

Citation: Go-To Developments Holdings Inc (Re), 2023 ONCMT 29

Date: 2023-09-07

File No. 2022-8

Adjudicators: |

M. Cecilia Williams (chair of the panel) |

|

Geoffrey D. Creighton |

||

Dale R. Ponder |

||

|

||

Hearing: |

In writing; final written submissions received July 13, 2023 |

|

|

||

Appearances: |

Erin Hoult |

For Staff of the Ontario Securities Commission |

|

Braden Stapleton |

|

|

||

|

Melissa MacKewn |

For Oscar Furtado |

|

Dana Carson |

|

|

Asli Deniz Eke |

|

[1] On March 30, 2023, Staff of the Ontario Securities Commission brought a motion for a further and better witness summary from Oscar Furtado, requesting that the Tribunal order Furtado's witness summary to comply with the requirements of Rule 27(3) (the Witness Summary Motion).

[2] Furtado served a witness list on November 23, 2022, as required by the Capital Markets Tribunal Rules of Procedure and Forms and as ordered by this panel. He identified himself as the only anticipated witness that he may be calling in this matter, and he provided a summary of his anticipated evidence (the Initial Witness Summary). The Initial Witness Summary listed topics that Furtado was expected to testify about but did not disclose the substance of his testimony about any of them.

[3] On June 30, 2023, Furtado served a "fresh as amended" witness summary (Amended Witness Summary) in response to Staff's Witness Summary Motion. The Amended Witness Summary states that Furtado will testify generally in accordance with the transcripts of his compelled interviews by Staff. Staff's position is that the Amended Witness Summary is also deficient.

[4] For the following reasons, we find that the Amended Witness Summary does not meet the requirements of Rule 27(3).

[5] Staff initially requested that the Witness Summary Motion be conducted in writing. Furtado did not consent to Staff's request, and the Witness Summary Motion was subsequently scheduled to be heard on June 2, 2023.

[6] Before the June 2, 2023 hearing date, Furtado requested that the motion be adjourned to address other issues in advance of the hearing on the merits. The parties agreed that other issues in this proceeding be dealt with on that date.

[7] At the June 2, 2023 attendance, Furtado agreed the Witness Summary Motion could now be conducted in writing but stated he required time to provide responding submissions. Staff, however, submitted that the Witness Summary Motion should go ahead as scheduled. Furtado also indicated that there was a possibility he might serve a further and better witness summary on Staff, and so make the Witness Summary Motion unnecessary. However, he added that he could not do so in the short term due to his health issues.

[8] On June 22, 2023, we ordered that the motion for a new witness summary be conducted in writing, pursuant to Rule 23(6). We also extended the timelines for the Respondents to file their materials.{1} Since whether a witness summary complies with Rule 27(3), is a purely legal question, we concluded there was good reason to conduct the hearing in writing.

[9] We now turn to the law regarding witness summaries.

3.1 The law

[10] Rule 27 (3) of the Tribunal's Rules provides that a party to a proceeding shall serve on every other party a "summary of the evidence that each witness is expected to give that includes, unless previously disclosed: ... (b) the substance of the witness's evidence; and (c) the identification of any document or thing to which the witness is expected to refer."

[11] The Tribunal has previously identified some of the purposes served by requiring pre-hearing disclosure of anticipated oral evidence in the form of witness summaries. For example, witness summaries:

a. allow the parties to understand the issues in the proceeding better;

b. facilitate the narrowing of issues;

c. allow parties to identify and resolve evidentiary issues that may arise at the hearing;

d. facilitate settlement;

e. permit more reliable estimates of the time required to conduct the hearing; and

f. as a result of all of the above, they minimize the time and resources required, and the cost of the hearing to the benefit of the Tribunal and the parties.{2}

[12] When the Tribunal is asked to assess the sufficiency of a witness summary at the pre-hearing stage, the summary must be assessed on its face.{3} The Tribunal's review of the witness summary's sufficiency at this stage "necessarily affords the party delivering the witness summary more latitude than would be the case with a challenge during the merits hearing."{4}

[13] We now briefly describe the Witness Summary and the Amended Witness Summary before turning to the parties' positions and our analysis supporting our conclusion that the Amended Witness Summary is deficient.

3.2 The Initial Witness Summary and the Amended Witness Summary

[14] Furtado's Initial Witness Summary listed the topics about which Furtado would testify if he testifies. Staff submits that the Initial Witness Summary was deficient because it did not disclose the substance of his testimony about each of the topics. It said only that the witness would refer to documents that were included in Staff's disclosure, or would otherwise be provided or were publicly available. It did not disclose the specific documents or things Furtado would refer to in his evidence.

[15] Furtado's Amended Witness Summary states that he will testify generally in accordance with the transcripts of his compelled interviews. It states that he will refer only to documents in Staff's disclosure, or which have otherwise been provided to Staff through prior correspondence or are publicly available.

[16] Staff submits that it appears from the title of the Amended Witness Summary ("Fresh as Amended") and the fact that it does not refer to the initial Witness Summary, that the Amended Witness Summary is intended to replace the Initial Witness Summary. We agree. The focus of our analysis is therefore on whether the Amended Witness Summary complies with Rule 27(3). We conclude it does not.

3.3 Parties' positions and our analysis

3.3.1 Does the Amended Witness Summary comply with Rule 27(3)(b)?

[17] Rule 27(3)(b) requires that a witness summary disclose the "substance" of the witness's evidence.

[18] Furtado submits that the Amended Witness Summary complies with Rule 27(3)(b) because it incorporates, by reference, Furtado's compelled interview transcripts. Relying on the Tribunal's decision in BDO, Furtado's submits that:

a. a witness summary will fail to comply with the Rules only if it fails to disclose any substance of the witness's anticipated evidence;

b. it can be assumed that compelled interview transcripts contain some substantive testimony even if such transcripts are not before the Tribunal; and

c. therefore, a witness summary that incorporates by reference interview transcripts will disclose some substance of the anticipated testimony and will be compliant with the Rules.{5}

[19] Furtado submits that in BDO, the Tribunal found that the witness summaries of nine witnesses, which did not disclose any substance of the witnesses' anticipated testimony other than through the incorporation by reference of the interview transcripts for eight of the nine witnesses, sufficiently disclosed the substance of the witnesses' evidence and therefore complied with Rule 27(3).{6}

[20] In addition, Furtado submits that since he is to tender any in-chief evidence by affidavit in advance of the merits hearing, as agreed to by the parties, the Amended Witness Summary, together with the affidavit evidence, will clearly satisfy the purposes of mutual pre-hearing disclosure of anticipated oral evidence.

[21] Staff submits that the Amended Witness Summary provides no disclosure of intended topics for Furtado's evidence, other than a reference to the transcripts. In contrast, they submit that the Initial Witness Summary did identify categories in which Furtado may provide evidence, but without identifying the substance of the evidence. In BDO, the witness summaries, Staff submits, at least identified that each witness was to speak to their involvement, or that of a certain organization, in the audits in issue.{7}

[22] Staff further submits that in BDO the Tribunal found that where a witness summary discloses no substance other than by reference to compelled interview transcripts, introductory language such as "including, but not limited to" and "broadly consistent with" raises reasonable concerns about the intended use of such phrases by the respondent"{8}. The respondents in BDO conceded that the broad introductory language was "largely nominal". The panel in BDO accepted the witness summaries holding that the substance of those witness summaries was "confined to whatever substance may be found in the transcripts of their examinations."{9}

[23] Furtado's Amended Witness Summary states that Furtado "will testify generally in accordance with the transcripts." Staff submits that this language raises the question of what use Furtado intends to make of the words "generally in accordance with", and whether he may attempt to testify beyond the scope of or contrary to the transcripts in reliance on this language. In addition, Staff submits that the concern is exacerbated by the covering letter from Furtado's counsel that accompanied the Amended Witness Summary, which states, "Should Mr. Furtado intend any corrections to the [Transcripts] in the course of reviewing his evidence and preparing for the merits hearing, we will advise staff expeditiously."

[24] We conclude that the Amended Witness Summary does not comply with Rule 27(3)(b). While the Amended Witness Summary arguably provides less substance than the Initial Witness Summary (because it does not refer to categories or topics Furtado will testify about), Tribunal precedent supports a conclusion that incorporating by reference the transcripts of compelled interviews constitutes sufficient substance for the purposes of Rule 27(3)(b) at the pre- hearing challenge stage.

[25] However, by stating that he will "testify generally in accordance with" the transcripts and raising the possibility of future challenges to the contents of the transcripts, Furtado has created sufficient ambiguity about the scope of his evidence that we conclude that the Amended Witness Summary does not disclose the intended substance of his evidence.

3.3.2 Does the Amended Witness Summary comply with Rule 27(3)(c)?

[26] Rule 27(3)(c) requires that a witness summary disclose the "identification of any document or thing to which the witness is expected to refer".

[27] Staff submits that the Amended Witness Summary does not comply with Rule 27(3)(c) because it does not list any documents, rather it refers to documents only in broad categories. Further, Furtado has not limited himself to even those broad categories by indicating that he may identify other documents not captured in those broad categories.

[28] Furtado submits that the Amended Witness Summary is compliant with Rule 27(3)(c) and is consistent with routinely accepted practices of the Tribunal.

[29] Both parties rely on BDO to support their respective positions. In BDO the witness summaries at issue stated that the witnesses were "expected to refer to documents in the hearing brief of BDO, which is expected to include, among other documents, BDO's Audit Working Papers and e-mail correspondence relating to the audits in question."{10}

[30] The panel in BDO dismissed the reference to the hearing brief as illogical and of no assistance, given that the hearing brief did not exist at the time and was not due to be delivered until closer to the commencement of the merits hearing.{11}

[31] The BDO panel went on to exclude the general introductory language "which is expected to include, among other documents" from its consideration of the witness summary as being of no value.{12} The BDO panel effectively read the witness summaries as referring to "BDO's Audit Working Papers end e-mail correspondence relating to the audits in question".{13}

[32] The BDO panel declined to grant Staff's request for "further and better" witness summaries because the requested order lacked any specifics and there was no basis for the panel to determine a more specific order. Given the broad nature of the allegations in BDO, the panel commented it had no basis to conclude that BDO would not rely on every document and every e-mail in presenting its case.{14}

[33] Contrary to Furtado's submissions, the circumstances before us differ from those in BDO. In BDO, the witness summaries disclosed that the witnesses would give evidence about "BDO's Audit Working Papers and e-mail correspondence relating to the audits in question." The Amended Witness Summary before us lacks anything close to that specificity. The reference to "documents that have been included in Staff's disclosure, have otherwise been provided to Staff through prior correspondence, or are publicly available" does not identify any documents in a meaningful way that would facilitate the narrowing of issues, identification and resolution of evidentiary issues or facilitate settlement in this matter.

[34] In addition, Furtado leaves open the possibility that he may identify additional documents outside the very broad category of documents he identified. He states that in such event, he will advise Staff in advance of the hearing and will include any such documents in his hearing brief. In our view the statement further undermines Furtado's position that the Amended Witness Summary identifies the documents that he will refer to in his evidence.

[35] We conclude that the broad and open-ended nature of the description of the documents that Furtado may refer to in his evidence, as described in the Amended Witness Summary, does not sufficiently identify the documents for the purposes of Rule 27(3)(c).

[36] With respect to the substance of Furtado's evidence and the identification of the documents he may refer to in evidence, Furtado states that both will be addressed in the affidavit of his in-chief evidence. We agree with Staff's position that the affidavit is not a substitute for providing a proper witness summary. An affidavit that will be delivered mere weeks before the merits hearing does not achieve the purposes of proper pre-hearing disclosure of anticipated witness evidence as we set out in paragraph 16 above.

[37] For the reasons above, we conclude that the Amended Witness Summary does not comply with Rule 27(3). We order Furtado to deliver a further and better witness summary to all other parties by September 20, 2023.

Dated at Toronto this 7th day of September, 2023

{1} Go-To Developments Holdings Inc. (Re) (2023), 46 OSCB 5469

{2} Hutchinson (Re), 2019 ONSEC 9 at para 22

{3} BDO Canada LLP (Re), 2020 ONSEC 2 at para 30 (BDO)

{4} BDO at para 30

{5} BDO at paras 31, 33, 34-35

{6} BDO at para 40

{7} BDO at para 15

{8} BDO at paras 36-37

{9} BDO at paras 19-22, 34-35, 38, 41

{10} BDO at para 43

{11} BDO at para 44

{12} BDO at para 45

{13} BDO at para 46

{14} BDO at para 51

OSC Staff Notice 81-734 -- Summary Report for Investment Fund and Structured Product Issuers

OSC Staff Notice 81-734 -- Summary Report for Investment Fund and Structured Product Issuers is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

September 13, 2023

Contents

Director's Message |

3 |

||

|

|||

Introduction |

5 |

||

|

|||

|

Responsibilities of the IFSP Branch |

5 |

|

|

Structure of the IFSP Branch |

7 |

|

|

What is an Investment Fund |

8 |

|

|

Investment Funds Market Landscape |

9 |

|

|

|

Indicators of Competition |

10 |

|

|

Mutual Fund Assets and Net Redemptions |

11 |

|

|

ETF Assets and Net Sales |

12 |

|

|

Crypto Asset and ESG Funds |

13 |

|

|||

Part A: Operational Highlights |

15 |

||

|

|||

|

I. |

Prospectus Filings |

15 |

|

|

Pre-File Process |

15 |

|

|

Review Process for Substantive Changes |

15 |

|

|

Data on Prospectus Reviews |

16 |

|

|

Prospectus Reviews of ESG-Related Funds |

17 |

|

|

Noteworthy Prospectus Filings |

18 |

|

|||

|

II. |

Exemptive Relief Applications |

19 |

|

|

Data on Exemptive Relief Applications |

20 |

|

|

Noteworthy Exemptive Relief Applications |

21 |

|

|||

|

III. |

Continuous Disclosure Reviews |

22 |

|

|

Summary of Completed Reviews |

22 |

|

|||

Part B: Regulatory Policy |

28 |

||

|

|

Access Based Model for Investment Fund Reporting Issuers |

28 |

|

|

Investment Fund Settlement Cycle |

28 |

|

|

Proposed Modernization of the Prospectus Filing Model |

29 |

|

|

Modernization of Continuous Disclosure Documents |

29 |

|

|

Review of Principal Distributor Practices |

29 |

|

|||

Part C: Emerging Issues and Initiatives Impacting Investment Funds |

31 |

||

|

|

Changes to OSC Fees Rule |

31 |

|

|

Transition to SEDAR+ |

31 |

|

|

Cessation of Canadian Dollar Offered Rate |

32 |

|

|

Investment Fund Survey |

32 |

|

|

Cybersecurity Breaches |

33 |

|

|||

Part D: Stakeholder Outreach |

35 |

||

|

|

IFSP Landing Page on OSC Website |

35 |

|

|

IFSP eNews |

35 |

|

|

Investment Funds Technical Advisory Committee |

36 |

|

|||

Staff Contact Information |

37 |

||

|

|||

Contact Information |

38 |

||

I am happy to share this Summary Report (Report) which provides an overview of the activities of the Investment Funds and Structured Products Branch (IFSP) of the Ontario Securities Commission (OSC) for the fiscal year ended March 31, 2023 (Fiscal 2023).

The capital markets have been impacted by a challenging economic environment during the year with market volatility, rising interest rates and inflation. There were high-profile collapses of several U.S. and foreign banks, as well as a large crypto asset firm. Investor confidence in the asset management industry is even more critical during economic uncertainty. As a regulator, we must be agile and proactive in responding to emerging issues to ensure investors are protected. Equally important, we work with industry professionals and leaders to facilitate solutions, provide guidance and to foster an environment for innovation and fair competition.

The asset management industry is very dynamic. Constant innovation is needed to compete, to break boundaries and to serve investors more effectively. We have continuously been working with the industry to bring new investment products and solutions to retail investors, with appropriate guardrails.

Our focus on communication, outreach and consultation has allowed staff to get better and more balanced insights in resolving regulatory issues and in setting policy direction and expectations. We leverage our Investor Office resources to understand investors' needs and behaviour. We also provide timely, relevant information with our eNews, an email subscription program.

With the completed launch of the third annual Investment Fund Survey (IFS), we are building an extensive database to enhance our risk-based oversight of investment fund issuers. IFS data is also critical to support global efforts to have better information and insight into various risks and leverage in the asset management industry globally. We appreciate the efforts of all IFMs in providing timely and complete responses to the survey requests.

While prospectus filings and new fund creations dipped as compared to the prior year, the number of continuous disclosure reviews rose significantly. We performed several issue-oriented reviews of funds that primarily hold crypto-assets. Our work around environmental, social and governance (ESG) funds also continued with a focus on the prospectus disclosure and sales communications of investment funds with an ESG focus. ESG offerings and popularity have evolved quickly, and we hope these reviews have brought greater clarity and consistency to disclosure so that investors can understand what ESG means and make more informed investment decisions about ESG products.

In the policy area, IFSP has continued to make progress on existing burden reduction policy initiatives, including an access-based model for investment fund reporting issuers, and the modernization of continuous disclosure documents. We are excited about this modernization initiative as we have invested significantly in consumer testing to enhance investors' understanding and engagement in reviewing these important documents. For new initiatives, we have commenced the review of principal distributor practices as well as whether the investment funds settlement cycle must move to T+1. Most recently, the CSA announced that it is examining chargeback practices which will help determine whether rule modernization is needed in this area to enhance investor protection.

We hope you find this Report helpful and informative. As always, if you have a question, comment, or would like to discuss regulatory matters, please reach out to us. Our Staff Contact Information has been included for your convenience.

This Report provides an overview of the key operational and policy initiatives of the IFSP Branch that impact investment fund and structured product issuers during Fiscal 2023. Consistent with the prior fiscal year's summary report, the Report can be used as a resource for IFMs, entities who perform services on their behalf and other stakeholders, including investors.

The Report is organized into four key areas:

Part A -- Operational Highlights

• Summarizes our key activities, including prospectus reviews, applications for exemptive relief and continuous disclosure reviews.

Part B -- Regulatory Policy Initiatives

• Identifies policy initiatives that are ongoing with detail on their status.

Part C -- Emerging Issues and Initiatives Impacting Investment Funds

• Summarizes changes that affect the investment funds industry.

Part D -- Stakeholder Outreach

• Describes some of the outreach undertaken by the IFSP branch.

The OSC's mandate is to protect investors from unfair, improper or fraudulent practices, to foster fair, efficient and competitive capital markets and confidence in the capital markets, to foster capital formation, and to contribute to the stability of the financial system and the reduction of systemic risk.

In support of the OSC's mandate, the IFSP Branch is responsible for administering the regulatory framework for investment funds and structured products, including linked notes and scholarship plans, that are sold to Ontario investors. Publicly offered investment fund assets in Canada are comprised broadly of mutual funds (conventional mutual funds, exchange traded funds or ETFs and alternative mutual funds) and non-redeemable investment funds (NRIFs).

Our key functions include:

• reviewing and assessing product disclosure for all types of publicly offered investment funds,

• considering applications for discretionary relief from securities legislation,

• policy making to adapt to changes in the investment funds industry,

• engagement with stakeholders, including on advisory committees, and through regulatory updates in IFSP eNews articles,

• issuing guidance to stakeholders through staff notices to communicate our expectations on process or policy matters,

• monitoring and responding to emerging capital market and investor protection risks more effectively, using tools such as our continuous disclosure review program, the IFS, and other information and analytical resources, and

• monitoring and participating in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO), and other financial regulators.

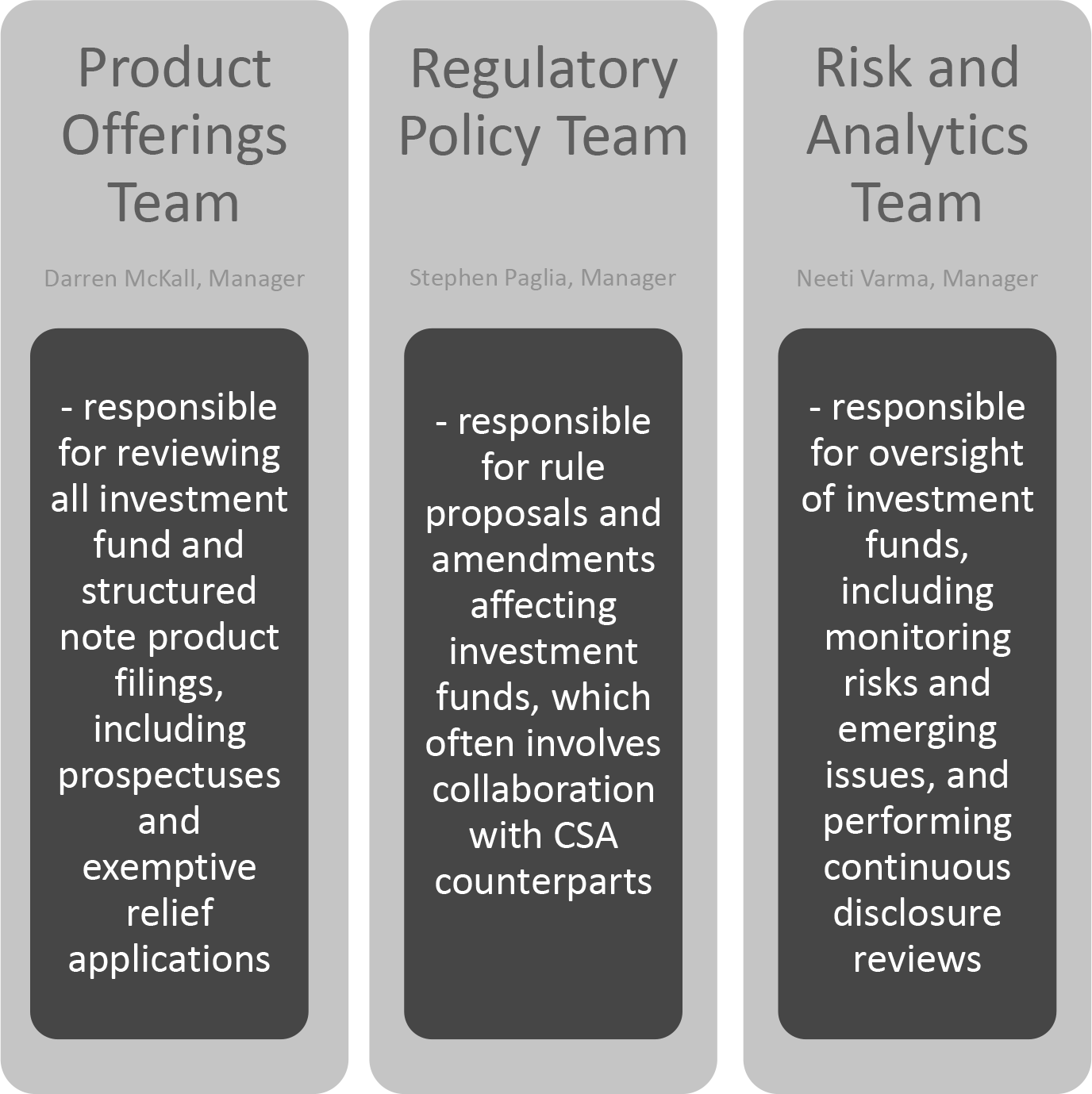

The IFSP Branch is organized into three dedicated teams:

There are two main types of investment funds: mutual funds and NRIFs{1}. Investors in mutual funds are generally able to purchase or redeem securities of mutual funds on demand for a price representing a proportionate interest of the fund's net assets. In contrast, NRIFs, also referred to as closed end funds, generally offer investors minimal, if any, right to redeem securities, and the price received may not necessarily represent a proportionate interest of the fund's net assets.

We get many inquiries from issuers on whether a product fits within the definition of an investment fund. As this topic is one of the most frequently asked questions of IFSP, we are outlining several criteria that may be considered when evaluating whether a product is an investment fund. These criteria are not exhaustive and are provided only as factors to consider. Satisfying or not satisfying any one criterion may not necessarily be indicative of whether an issuer is an investment fund or not. Issuers should collectively consider all the product features along with the criteria to determine whether, on balance, an issuer falls within the investment fund definition under securities law.

Ability to redeem and frequency of redemptions

An investment fund provides investors with an ability to redeem with reference to net asset value (NAV). If redemptions are allowed more frequently than annually, staff has interpreted this feature as being "upon demand" as is considered within the definition of a 'mutual fund'. If, however, redemptions are allowed annually only (or less frequently), the issuer may still be considered an investment fund under the 'non-redeemable investment fund' definition if it meets the other tests.

Calculation of NAV and investor entitlement

Upon redemption, consider what the investor receives and whether there is a NAV calculated in accordance with Part 14 of National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106).

No active management of underlying assets

The definition of 'investment fund' typically contemplates an entity which takes a passive approach to its investee entities. Factors which may indicate active management of an investee company include:

• whether the issuer holds securities representing more than 10% of the outstanding equity or voting securities of the investee company;

• any right of the issuer to appoint board or board observer seats on the investee company or have representation on the board of directors;

• restrictions on the management, or approval or veto rights over decisions made by the management, of the investee company by the issuer;

• any right of the issuer to restrict the transfer of securities by other securityholders of the investee company;

• direct involvement in the appointment of managers; and

• a say in material management decisions.

No control of underlying issuers

Investment funds generally do not control or seek to control underlying issuers.

Operations and purpose of the issuer

The primary purpose of an investment fund is to invest monies provided by its security holders in portfolio assets. Accordingly, investment fund issuers do not conduct operating businesses.

Investor expectations

Consider whether there is a reasonable expectation from the investor that they will have their money professionally managed or invested as part of an investment strategy and how the issuer is being marketed to the public.

The above-mentioned criteria may be useful to consider along with the specific facts and features of the issuer. Issuers should also consult with their legal counsel for assistance as being an investment fund involves different continuous disclosure and reporting obligations than other types of issuers, and IFM registration will also be required in these instances.

Canada's public investment funds are a significant component of the asset portfolios of retail investors, representing over one-third of household financial wealth.{2} As at March 31, 2023, investment funds in Canada have about $2.3 trillion in assets under management (AUM){3}:

Investment Fund Product

AUM as of March 31, 2022

AUM as of March 31, 2023

% of Investment Fund AUM as at March 31, 2023

Conventional Mutual Funds

$2.0 trillion

$1.9 trillion

83%

ETFs

$324.7 billion

$337.1 billion

15%

Closed End Funds

$36.8 billion

$36.2 billion

2%

TOTAL

$2.36 trillion

$2.3 trillion

Structured notes outstanding as of March 31, 2023, were approximately $30.4 billion{4}.

On a global scale, based on data compiled by IOSCO as part of its 2021 Investment Funds Statistics Survey from participating IOSCO members, Canada accounts for approximately 7% of the conventional mutual funds captured in that survey and approximately 5% of the total net asset value of these funds. Canada sits among the top five jurisdictions globally in both categories.{5}

Indicators of Competition

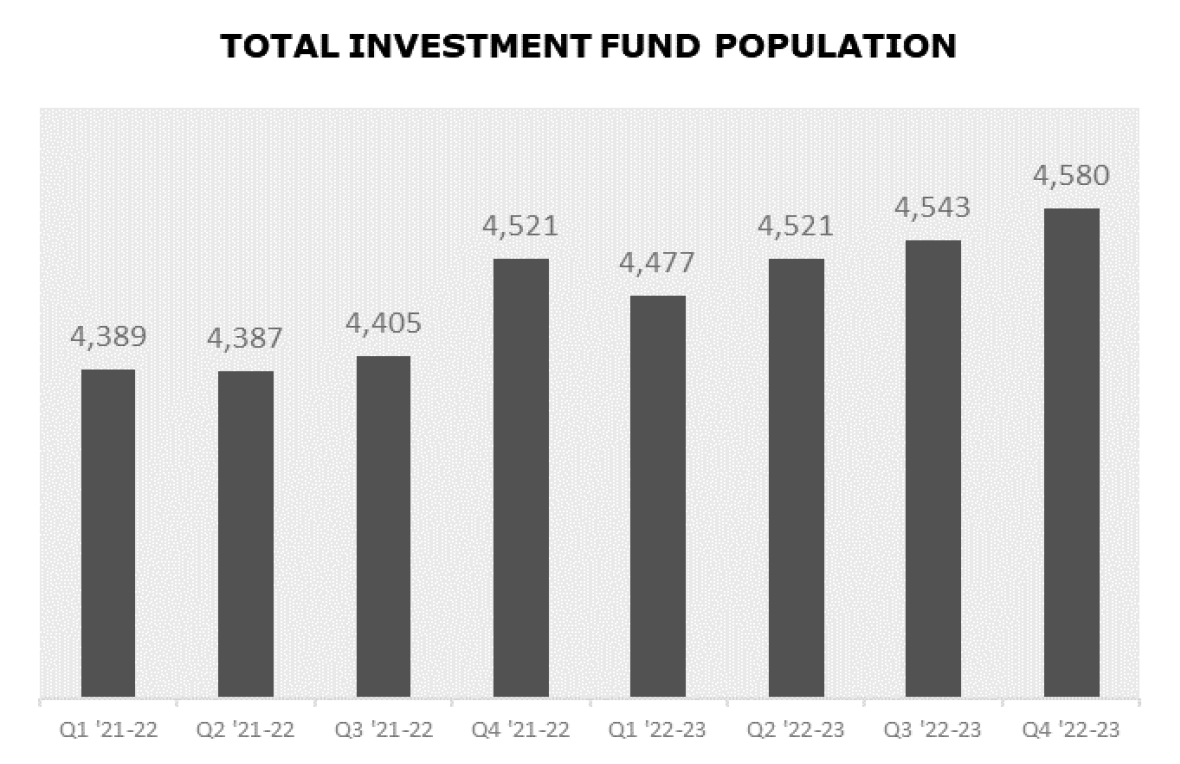

The total investment funds population has steadily increased over the past several years, but this trend slowed in Fiscal 2023 when the investment funds population in Ontario remained relatively flat. There was an increase of approximately 59 funds in Fiscal 2023 as compared to growth of 144 funds in the previous fiscal year as shown in the chart below:

Source: Internal reporting issuer database showing investment funds active in Ontario

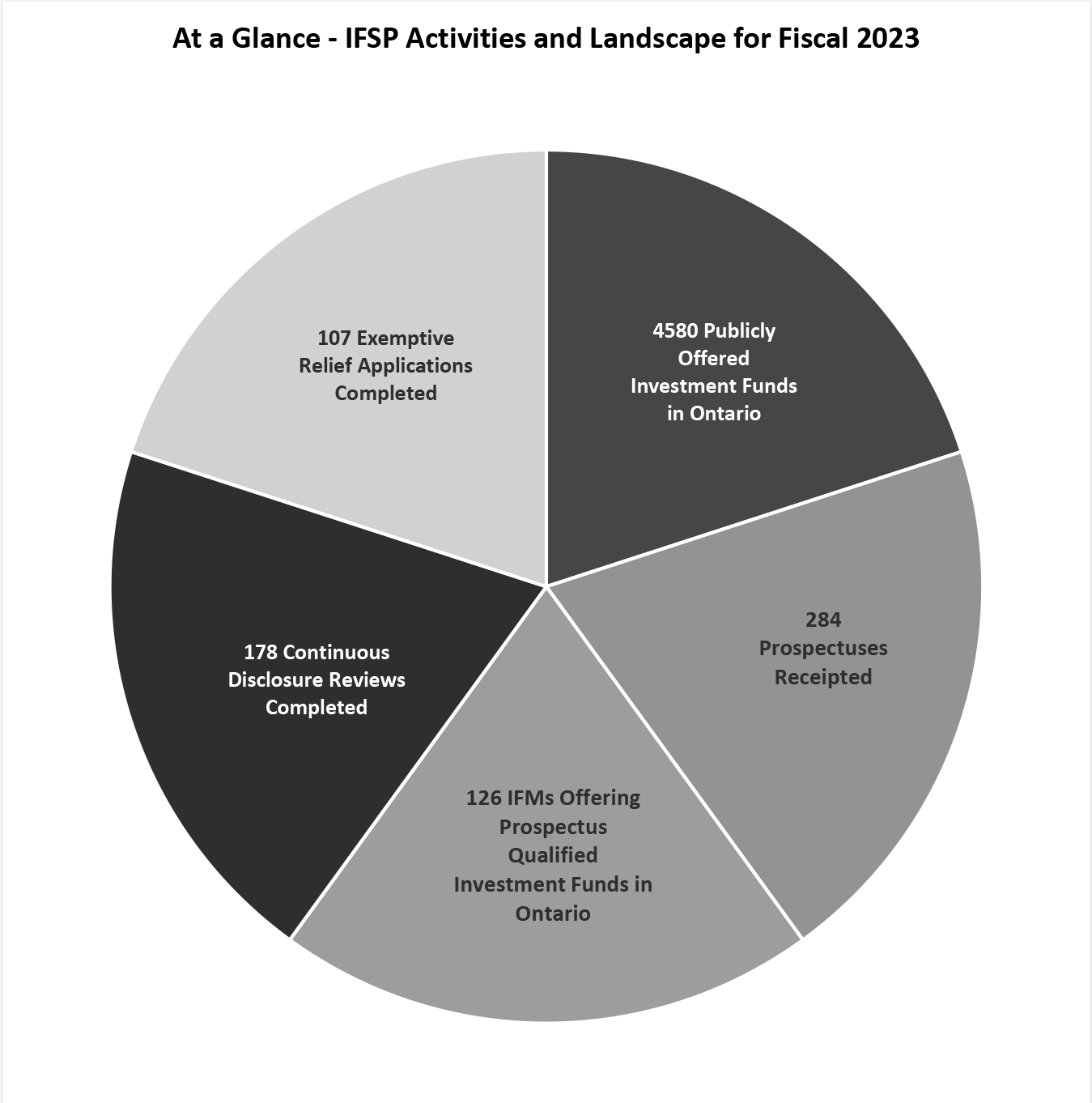

As of December 31, 2022, there were 126 IFMs offering over 4,500 publicly offered investment funds as compared to 128 IFMs in the prior year.{6} The three largest IFMs had a combined market share of 31%{7} of AUM for all prospectus qualified investment funds, including conventional mutual funds and ETFs. When conventional mutual funds and ETFs are looked at separately, the three largest IFMs who manage mutual funds had a combined market share of 36%{8} of AUM whereas the ETF market appears to be more concentrated with the top three IFMs who manage ETFs accounting for approximately 67% of ETF AUM{9}. However, the ETF market has become more diversified in the past five years based on manufacturer market share.

After rising steadily in the early 2000s, the market share of bank affiliated IFMs has remained relatively flat in the past decade at approximately 45% of prospectus qualified funds{10}. Small to mid-size IFMs have remained competitive and have played a key role in the launch of several novel investment fund products in recent years.

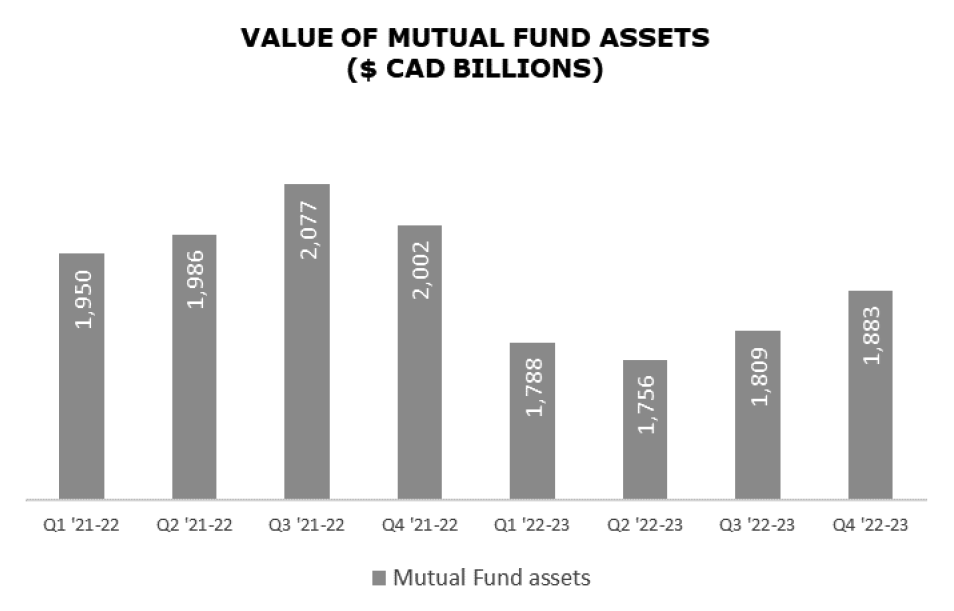

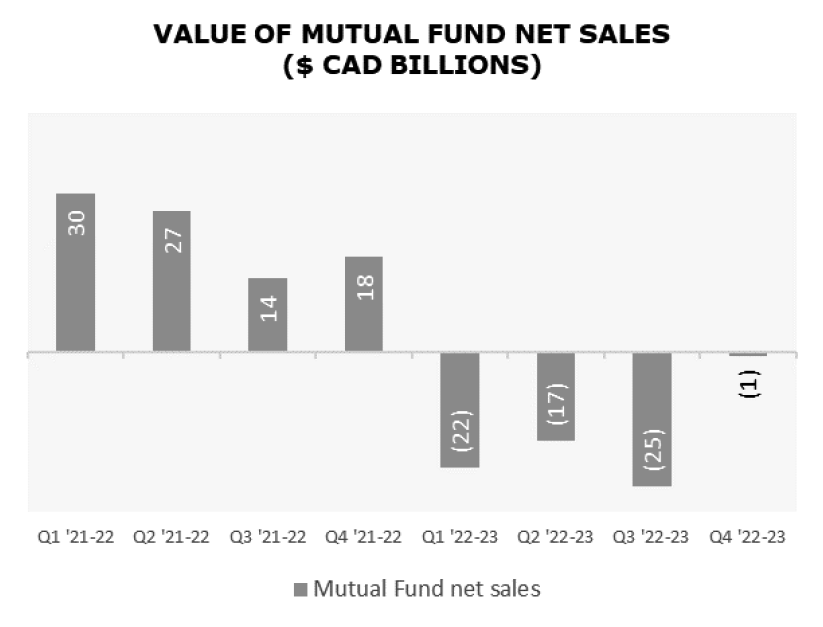

Mutual Fund Assets and Net Redemptions

Total investment fund AUM fell slightly from $2.36 trillion in the previous fiscal year to $2.3 trillion at the end of Fiscal 2023, of which $1.9 trillion is conventional mutual funds. After a strong bounce back in 2021 following the uncertainty of the COVID-19 pandemic, mutual fund AUM declined by 5% during Fiscal 2023 as mutual funds experienced net redemptions during this time. Net redemptions were primarily in the balanced asset class category, while money market mutual funds experienced positive sales, signalling that investors were being more cautious with their investments.

Source: IFIC Industry Statistics

Source: IFIC Industry Statistics

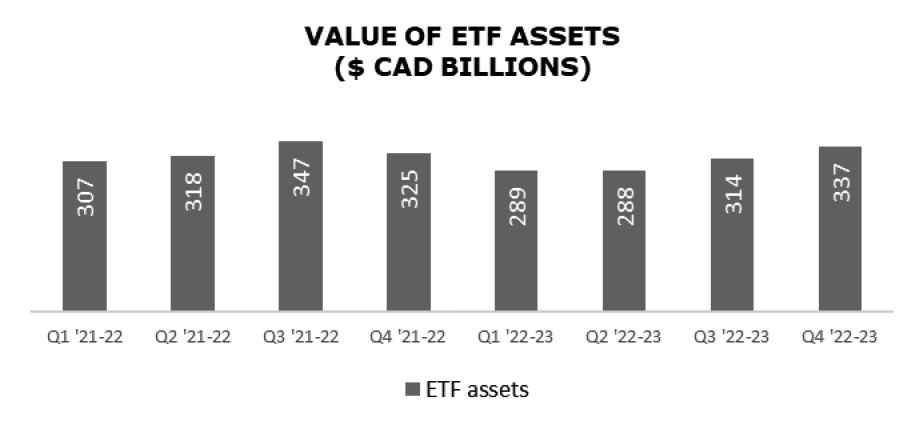

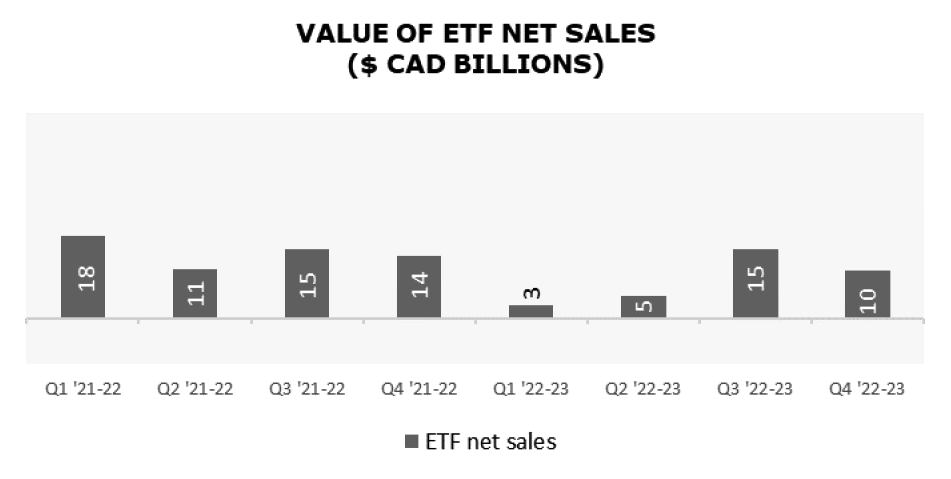

ETF Assets and Net Sales

ETFs also experienced a decline in AUM through most of Fiscal 2023 but rising net sales near the end of the year resulted in a small increase in AUM of 4% from the previous fiscal year. ETF net sales were mostly in the equity asset category and similar to mutual funds, money market ETFs (primarily high interest savings funds) also saw strong inflows compared to previous years{11} as investors sought safety and capital preservation.

Source: IFIC Industry Statistics

Source: IFIC Industry Statistics

Crypto Asset and ESG Funds

As these two areas have evolved quickly in the past couple of years in the investment funds landscape, IFSP staff continue to monitor crypto asset and ESG funds closely.

Crypto Asset Funds

In Ontario, crypto asset funds are offered by eight IFMs and the crypto asset figures and activity for Fiscal 2023 as compared to the prior fiscal year are shown below:

Year

# of Public Crypto Asset Funds in Ontario

AUM of Crypto Asset Funds

# Crypto Asset Funds Receipted

# Crypto Asset Funds Terminated

Fiscal 2023

24{12}

$2.85 billion

2

1

Fiscal 2022

23

$6.9 billion

17

0

{12} After the end of Fiscal 2023, there were two fewer crypto asset funds. One crypto asset fund was terminated, and another changed its investment objectives and name to reflect it becoming a non- crypto asset fund.

While there was one fund termination, much of the decline in AUM is due to the declining value of cryptocurrencies, rather than significant fund outflows. Net redemptions totaled $866 million in Fiscal 2023.

ESG Funds

ESG funds continue to gain awareness and popularity, although like most investment fund products there was a slowdown in product launches in the latter part of the year. AUM of ESG funds totalled $44. million in 2022, up slightly from $41.8 million in 2021. Net sales totalled $6.9 million, down from a high of $17.6 million in 2021.{13} The top 10 ESG providers account for 92% of the ESG assets in Canada.{14}

With the increased presence of ESG funds in the market, the Canadian Investment Funds Standards Committee (CIFSC) released its responsible investment identification framework in January 2023. The CIFSC categories are aimed at standardizing the classifications of Canadian-domiciled retail mutual funds. The framework includes 6 CIFSC categories, and investment funds can belong to more than one category.

ESG funds remained a focus of the IFSP branch's operational activities during Fiscal 2023, and these initiatives will be described in detail in the next section.

The OSC has set service standards and timelines which stakeholders can rely on when interacting with the OSC. The Service Commitment document can be found on our website and includes timelines for prospectus filings and amendments, and the review of exemptive relief applications, which comprise some of our key operational functions. The IFSP Branch is committed to ensuring that services are delivered efficiently and effectively, and in accordance with those standards.

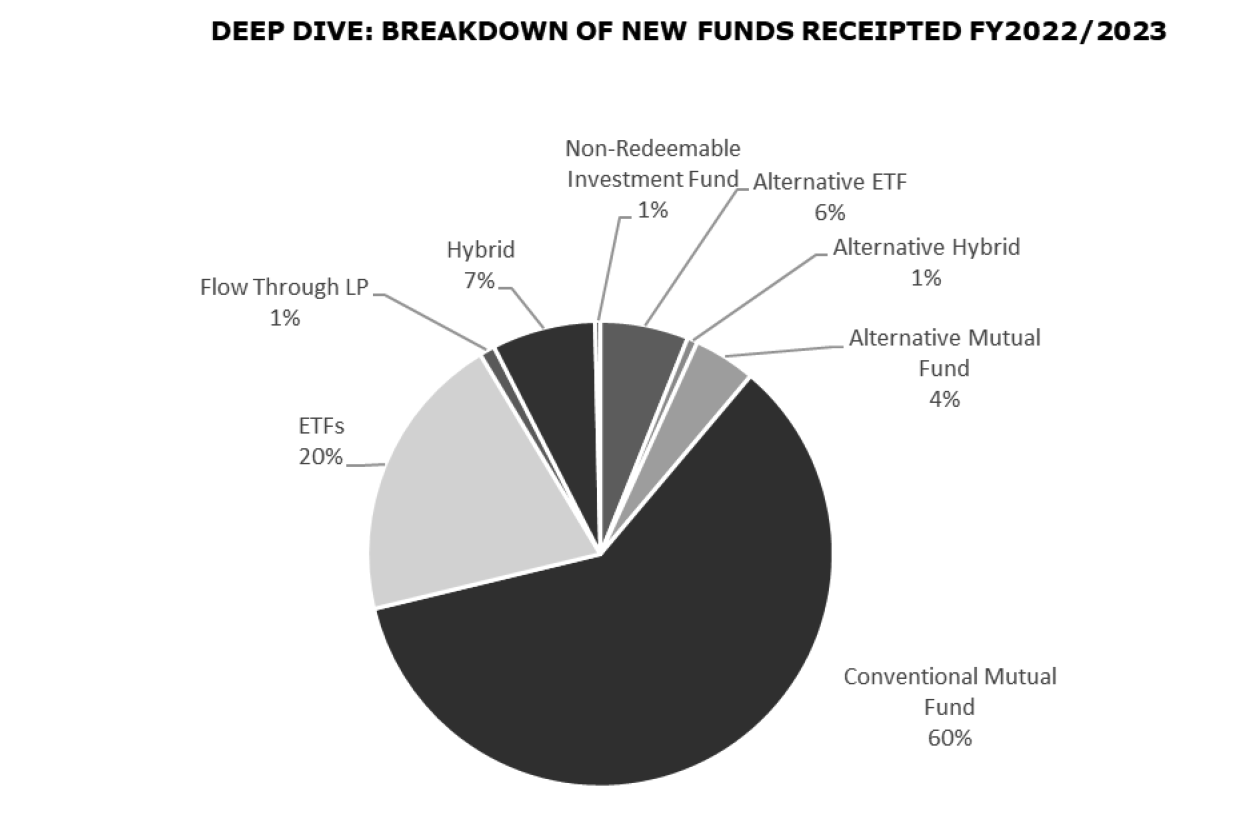

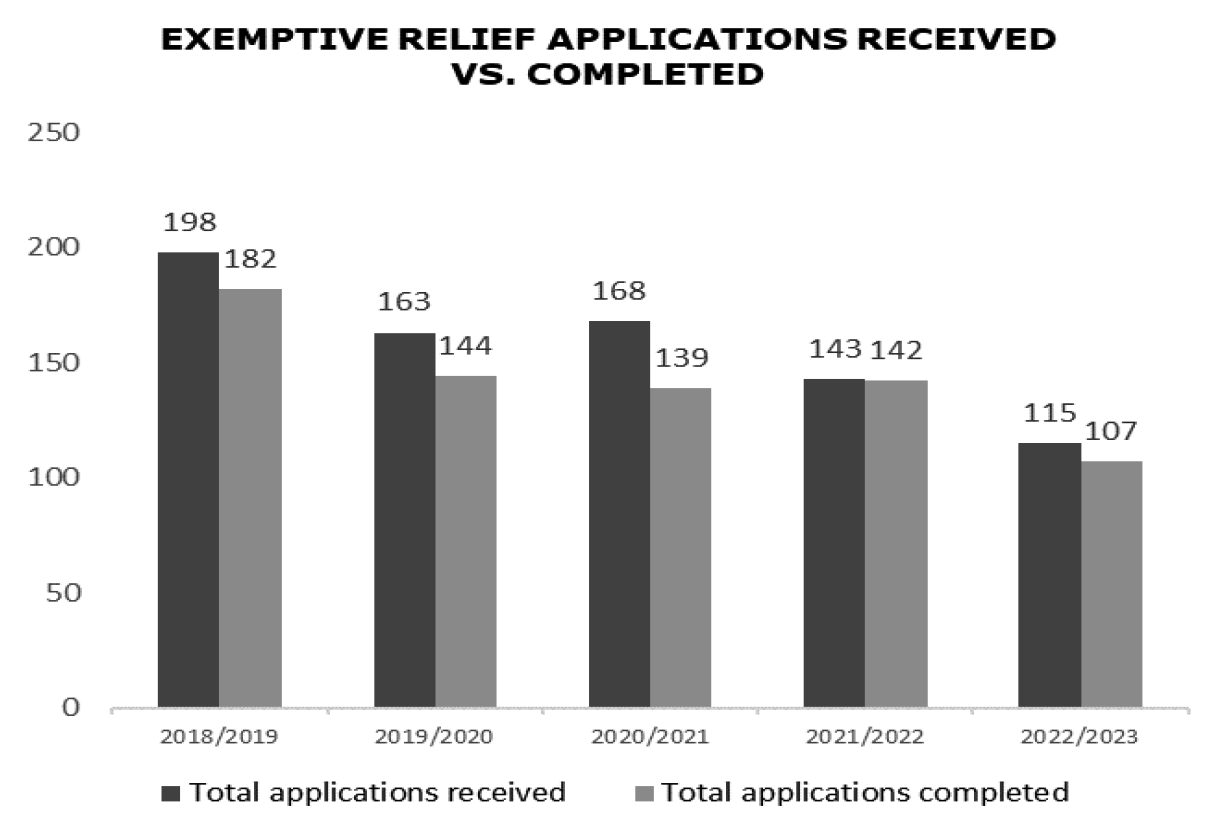

Sections I to III below will highlight each of our main operational functions in more detail, including noteworthy files during Fiscal 2023. Issuer activity around novel prospectus filings and applications for exemptive relief were down this year, and accordingly oversight activities focused on conducting more continuous disclosure reviews.

I. Prospectus Filings

One of our key operational functions is the review of prospectuses and supplements in connection with the distribution of publicly offered investment funds and linked notes. Under Canadian securities law, an issuer must file and obtain a receipt for a prospectus to "distribute" securities to the public or rely upon a prospectus exemption.

Prospectus filings are categorized by IFSP into one of three review types: standard, issue-oriented or full review. Most prospectus filings are subject to standard review, as these generally relate to investment funds that are already in distribution and have been previously reviewed. An issue-oriented review targets specific issues with the filing while a full review is undertaken when the prospectus is for a new manager, new fund or product that has features or characteristics that could raise novel issues. These filings may also be accompanied by a related application for exemptive relief.

Pre-File Process

For unique or novel products, we recommend that filers use the confidential pre-file process for prospectus and exemptive relief applications. Many filers who wish to launch a novel type of product in the market have used this process as it maintains the confidentiality of the product offering as the regulatory issues are resolved. For more information on the pre-file process click here.

Review Process for Substantive Changes

Staff remind IFMs that substantive changes to prospectus disclosure made after a preliminary or pro forma prospectus has been filed or cleared for final may cause delays in receiving a receipt for the final prospectus. Delays may occur as staff need to conduct a new review of those changes, and depending on the outcome of that review, may need to reverse the "clear for final" status and issue additional comments. Situations like this may potentially cause lapse date-related issues.

For preliminary prospectuses, consideration will also be given to whether an amended and restated preliminary prospectus will need to be filed. Staff note that such substantive changes to prospectus disclosure will be subject to the same level of review as the disclosure included in the filed preliminary or pro forma prospectus. For example, during the fiscal year, staff observed a number of prospectuses in which material ESG related disclosure was added after a preliminary or pro forma prospectus was filed or cleared for final. In each case, the additional disclosure was not prompted by comments raised by staff and required additional review time since the additions/revisions were substantive.

Staff encourage IFMs to file their prospectus amendments and preliminary and pro forma prospectuses as early as possible and, if applicable, in advance of their filing deadlines, in order to avoid delays in the prospectus review process.

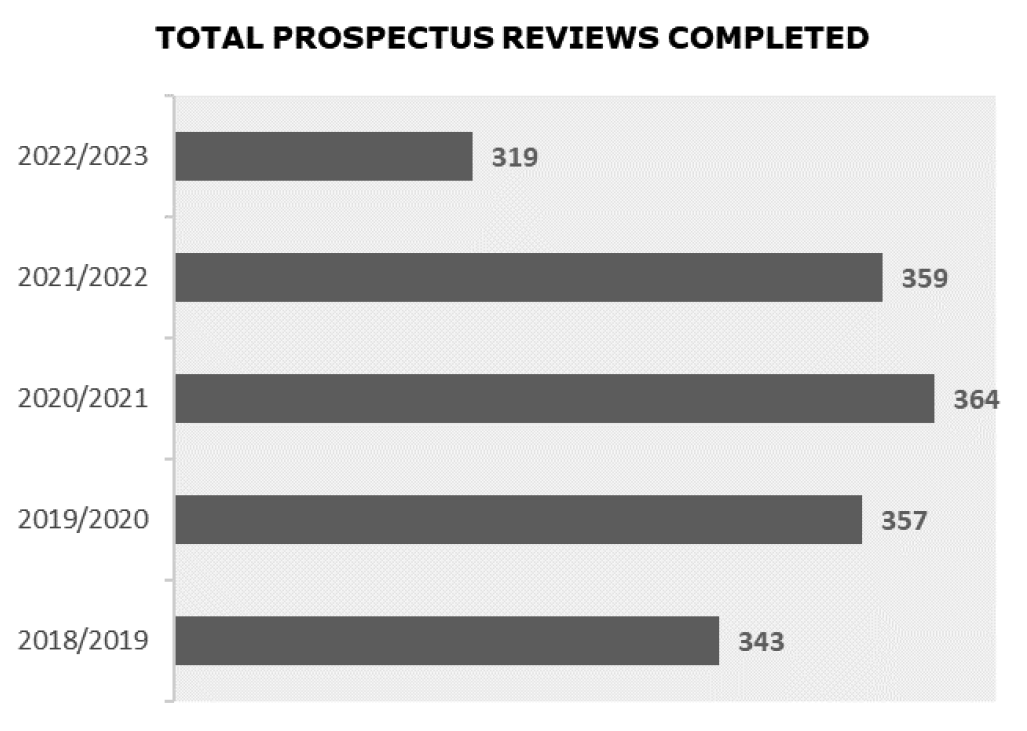

Data on Prospectus Reviews

Total prospectus filings declined 11% in Fiscal 2023 compared to the previous fiscal year and the total volume was at its lowest level over the last five years. As new fund creations were relatively flat and fund terminations also slowed during Fiscal 2023, the decline in prospectus filings is partly attributable to the continuing consolidation of prospectuses by IFMs. Most of the filings were in the category of standard review for conventional mutual fund and ETF offerings.

Prospectus Reviews of ESG-Related Funds

During the past fiscal year, staff have continued to review the prospectuses and related documents of funds whose investment objectives reference ESG factors and other funds that use ESG strategies (ESG-Related Funds), in accordance with the guidance provided in CSA Staff Notice 81-334 ESG-Related Investment Fund Disclosure(the ESG Staff Notice), which was published on January 19, 2022 to assist IFMs in improving the disclosure of ESG-Related Funds.

These prospectus reviews have generally been focused on, but are not limited to, the fund's:

• investment objectives and name

• investment strategies

• proxy voting policies and procedures

• risk disclosure

• suitability disclosure

To date, most of the issues raised by staff during these reviews have been in relation to investment strategies disclosure. In particular, most comments have sought to clarify:

• which types of ESG strategies are being used;

• which specific ESG factors are relevant to the portfolio manager's analysis; and

• how such factors are being evaluated and monitored by the portfolio manager.

Staff have also encountered issues relating to the investment strategies disclosure of funds that do not have ESG-related investment objectives but that consider ESG factors, where the consideration of ESG factors plays a more limited role in the investment process. In some cases, we have found that IFMs have included disclosure about how ESG considerations are incorporated into the investment process for their funds, without being clear about the limited role that the consideration of ESG factors and/or the use of ESG strategies plays in the investment process of such funds. For funds where the consideration of ESG factors plays a more limited role, where disclosure is included in their prospectuses about the incorporation of ESG considerations, staff have asked issuers to clarify the limited role that the consideration of ESG factors and/or use of ESG strategies plays in the fund's investment process, including the weight given to ESG factors and the impact that ESG factors will have on the portfolio selection process.

Staff have also raised and resolved issues relating to fund names, investment objectives, ESG risk disclosure, and ESG-related disclosure in the summary of proxy voting policies and procedures. Through these reviews, we have required issuers to improve the prospectus disclosure of ESG-Related Funds, in keeping with the stated purposes of the ESG Staff Notice and the ESG prospectus reviews.

As part of these reviews, staff have also requested and reviewed copies of recent sales communications relating to the funds being reviewed. A discussion of staff's ESG-focused sales communication reviews is included later in this document under the "Reviews of Continuous Disclosure, Sales Communications, and Portfolio Holdings of ESG-Related Funds" heading.

Staff will continue to review the prospectus disclosure of ESG-Related Funds in accordance with the guidance in the ESG Staff Notice.

Noteworthy Prospectus Filings

Some of the novel prospectus filings that were receipted during the fiscal period are summarized below, along with details on any related exemptive relief.

Single Stock ETFs

During the year, IFSP issued final prospectus receipts on behalf of several ETFs that each invest in a single specified U.S. public issuer. The first ETFs were launched in December 2022 and are based on five large-cap U.S. companies. The fundamental investment objective of each ETF is to link its return to a single specified U.S. issuer. Some of these funds are alternative mutual funds which use a limited amount of leverage through cash borrowing to purchase additional securities of that single issuer. The ETFs received exemptive relief from the concentration restrictions set out in subsections 2.1(1) and 2.1(1.1) of National Instrument 81-102 Investment Funds (NI 81-102) to permit each ETF to invest in only one single issuer in excess of the investment restrictions contained in those sections.

Decumulation Funds

After a confidential pre-file prospectus application process, two mutual funds were receipted that are targeted to investors in the decumulation phase of their life (i.e., retirement). The two funds have a set term of 20 years, terminating on December 31, 2042:

i. a Decumulation Fund which aims to pay set distributions for the life of the fund and decumulate down to $0 by the termination date; and