Ontario Securities Commission Bulletin

Issue 46/29 - July 20, 2023

Ont. Sec. Bull. Issue 46/29

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

CIRO

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

FOR IMMEDIATE RELEASE

July 13, 2023

TORONTO -- Take notice that an attendance in the above-named matter is scheduled to be heard on July 18, 2023 at 2:00 p.m.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

July 13, 2023

TORONTO -- Take notice that the attendance in the above-named matter scheduled to be heard on July 18, 2023 will instead be heard on July 21, 2023 at 10:00 a.m.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

July 17, 2023

TORONTO -- The Tribunal issued its Reasons and Decision in the above-named matter.

A copy of the Reasons and Decision dated July 14, 2023 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

July 18, 2023

TORONTO -- The Tribunal issued an Order in the above-named matter.

A copy of the Order dated July 18, 2023 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

File No. 2022-6

Adjudicators: |

M. Cecilia Williams (chair of the panel) |

William Furlong |

July 18, 2023

WHEREAS on July 18, 2023, the Capital Markets Tribunal held a hearing by videoconference in relation to the application brought by Amin Mohammed Ali to review the decisions of the Mutual Fund Dealers Association (MFDA) dated February 11, 2022 and September 20, 2022;

ON HEARING the submissions of the representatives for Ali, for Staff of the Canadian Investment Regulatory Organization (formerly MFDA) (CIRO) and for Staff of the Ontario Securities Commission;

IT IS ORDERED that:

1. pursuant to subsection 2(2) of the Tribunal Adjudicative Records Act, 2019, SO 2019, c 7, Sch 60, and Rule 22(4) of the Rules of Procedure, Ali's written submissions (referred to in Ali's filing and in this order as Ali's Hearing Brief) and the Updated Record of Original Proceeding filed on July 10, 2023 (the Updated Record) shall be kept confidential, pending any further order of the Tribunal regarding confidentiality;

2. by 4:30 p.m. on July 21, 2023, Ali shall provide responding submissions regarding Staff of CIRO's request that a portion of paragraph 15 of Ali's Hearing Brief be struck for settlement privilege;

3. by 4:30 p.m. on July 21, 2023, Staff of CIRO shall provide its proposed redactions to Ali's Hearing Brief;

4. by 4:30 p.m. on July 24, 2023, Staff of the Commission shall provide its submissions, if any, on CIRO's proposed redactions to Ali's Hearing Brief;

5. by 4:30 p.m. on July 26, 2023, Ali shall advise which portions, if any, of Exhibit A at Tab 3 of the Updated Record he is seeking to have ordered confidential, along with his position on why such portions should ordered to be confidential;

6. by 4:30 p.m. on July 28, 2023, Staff of CIRO and Staff of the Commission shall advise of their position regarding Ali's confidentiality request over the Updated Record;

7. by 4:30 p.m. on July 28, 2023, Ali shall advise which portions, if any, of the transcript of the confidential portion of the June 26, 2023 hearing should be kept confidential, along with his position on why such portions should be marked as confidential;

8. by 4:30 p.m. on August 4, 2023, Staff of CIRO shall provide submissions regarding Ali's confidentiality request over the transcript of the confidential portion of the June 26, 2023 hearing;

9. by 4:30 p.m. on August 7, 2023, Staff of the Commission shall provide submission, if any, regarding Ali's confidentiality request over the transcript of the confidential portion of the June 26, 2023 hearing;

10. paragraph 5 c. of the Tribunal's June 1, 2023 Order is varied as follows: "by 4:30 p.m. on August 26, 2023, Ali shall:

i. give notice of any intention to rely on documents or things not included in the record of the original proceeding;

ii. disclose any documents or things not included in the record of the original proceeding on which he intends to rely;

iii. give notice of any intention to provide oral evidence and serve a summary of each witness' anticipated oral evidence; and

11. paragraphs 2 g. and h. of the Tribunal's June 28, 2023 Order are varied as follows:

g. by 4:30 p.m. on August 1, 2023, Staff of CIRO shall serve and file its hearing brief, if any, and written submissions; and

h. by 4:30 p.m. on August 15, 2023, Staff of the Commission shall serve and file its hearing brief, if any, and written submissions.

Binance Holdings Limited -- s. 144(1)

Citation: Binance Holdings Limited (Re), 2023 ONCMT 27

Date: 2023-07-14

File No. 2023-11

Adjudicators: |

Sandra Blake (chair of the panel) |

|

Timothy Moseley |

||

|

||

Hearing: |

By videoconference, June 2, 2023; final written submissions received June 6, 2023 |

|

|

||

Appearances: |

Aaron Dantowitz |

For Staff of the Ontario Securities Commission |

Alvin Qian |

||

|

||

Graeme Hamilton |

For Binance Holdings Limited |

|

Caitlin R. Sainsbury |

||

Teagan Markin |

||

Brianne Taylor |

||

[1] These are the reasons for our decision,{1} issued on June 7, 2023, that the Capital Markets Tribunal does not have jurisdiction under s. 144(1) of the Securities Act{2} to revoke an investigation order made by the Ontario Securities Commission under s. 11 of the Securities Act.

[2] Binance Holdings Limited (Binance) operates a crypto-asset trading platform. On May 10, 2023, the Commission issued an order under s. 11, appointing various individuals to investigate Binance's conduct.

[3] Binance then applied to this Tribunal under s. 144(1) of the Securities Act, asking that the Tribunal revoke the investigation order. That subsection provides that "[t]he Commission may make an order revoking or varying a decision of the Commission".

[4] At a preliminary attendance, the Tribunal directed that before proceeding to the application's merits, the parties first address whether the Tribunal has jurisdiction to grant the relief sought.

[5] Following a hearing at which the parties made submissions on that question, we decided that the Tribunal does not have jurisdiction under s. 144(1) to revoke the investigation order. As we explain below, we concluded that under the amendments to the Securities Act made in 2022, only the Commission, exercising its executive function, can revoke its own s. 11 order.

2.1 Introduction

[6] We begin our analysis by reviewing the legislative framework as it existed before the 2022 amendments to the Securities Act. We then examine Binance's application under the amended framework. We conclude that the word "Commission" is capable of more than one meaning within the Securities Act, and we must therefore apply principles of statutory interpretation to decide what "Commission" means in s. 144(1), the provision on which Binance relies.

2.2 Legislative framework before the 2022 amendments

[7] Before the 2022 amendments, the Commission was an integrated regulatory agency that comprised:

a. a quasi-legislative function (making rules and policies);

b. an executive function (applying and enforcing legislation, rules and policies); and

c. an adjudicative function (holding hearings at which parties appeared before panels of appointed members of the Commission).{3}

[8] Often in these reasons, we use the word "tribunal" to describe the Commission's adjudicative function before the 2022 amendments, even though that function was typically referred to as "the Commission". The Capital Markets Tribunal as currently constituted, to which we refer as "the Tribunal", did not yet exist.

[9] Before the 2022 amendments, the Commission, exercising its executive function, routinely issued investigation orders under s. 11 of the Securities Act. In some instances, an investigation resulted in an enforcement proceeding that was heard by a panel of appointed members of the Commission, sitting as a tribunal, exercising the Commission's adjudicative function.

[10] All members of the Commission, other than the person who was both Chair and CEO, sat as directors on the board of the Commission and as adjudicators on the tribunal. Despite this overlap of duties, the adjudicative function of the Commission operated independently from the executive function. The Chair/CEO supervised the enforcement branch of the Commission and therefore did not sit on any hearings before the tribunal. In addition, and with an irrelevant exception, s. 3.5(4) precluded any appointed member of the Commission who exercised a power under Part VI of the Securities Act, including issuing an investigation order under s. 11, from sitting on a hearing that dealt with that matter, unless the parties consented. Subsection 3.5(4) has since been repealed.

[11] Despite this separation, matters occasionally came before the Commission sitting as a tribunal, in which the tribunal was asked to make an order in relation to an ongoing investigation, as opposed to in relation to a proceeding that had already been commenced before the tribunal. One example is the 2003 case, Universal Settlements International Inc (Re).{4} In that case, the Commission had issued a s. 11 investigation order, and an application was brought before the Commission (sitting as the tribunal) to revoke that order under s. 144(1). The applicant said that before issuing the s. 11 investigation order, the Commission ought first to have satisfied itself that the products that were the subject of the investigation order were indeed securities.

[12] The tribunal dismissed the application. There was no controversy that a s. 11 order was subject to being revoked or varied under s. 144(1), because while that provision allowed for revoking or varying a "decision", the word "decision" was defined in the Securities Act to include an order of the Commission. The question was whether the tribunal should revoke the order in that case.

[13] In dismissing the application, the tribunal held that at the investigation stage, the Commission had no obligation to satisfy itself that the products at issue were securities. Even though the tribunal decided not to revoke the s. 11 order, it contemplated that it had the power to do so. However, the oral reasons for the decision do not address the question of jurisdiction.

2.3 Binance's application under the current legislative framework

[14] In this application, Binance relies on s. 144(1) of the Securities Act in asking the Capital Markets Tribunal to revoke or vary a s. 11 order issued by the Commission. The central question is whether changes to the legislative framework in 2022 mean that the Tribunal does not have jurisdiction to grant that relief.

[15] Those changes include separating the Chair and CEO roles and creating the Tribunal as "a division of the Commission".{5} The newly created Tribunal began its existence carrying on what had previously been the adjudicative function of the Commission. Proceedings that were ongoing before proclamation of the amendments continued without interruption. The most significant Tribunal-related changes are that:

a. there is no longer any overlap between the Commission's board of directors and the Tribunal members, who now have no role in the rule-making and policy-making functions of the Commission, or the oversight of its executive functions such as compliance and enforcement; and

b. conversely, the board has no involvement in, or oversight of, the Tribunal's adjudicative functions.

[16] The legislative amendments left s. 144(1) mostly intact, with the only change relating to who at the Commission can bring an application under that provision. Neither party before us suggested that this change was relevant on this application, and it does not factor into our decision.

[17] The most relevant change was the addition of a new section, s. 144.1. The operative words of s. 144.1(1) provide that the "Tribunal may make an order revoking or varying a decision of the Tribunal".

[18] As a result, there are now two parallel provisions in the Securities Act relating to the revocation or variation of orders. The first, s. 144(1), authorizes "the Commission" to revoke or vary a decision of "the Commission". The second, s. 144.1(1), authorizes "the Tribunal" to revoke or vary a decision of "the Tribunal".

[19] The narrow question we must decide is whether the first occurrence of "Commission" in s. 144(1) includes the Tribunal. In other words, does s. 144(1) authorize the Tribunal, as "a division of the Commission", to revoke or vary an order of the Commission?

2.4 Is the language of s. 144(1) precise and unequivocal?

[20] Focusing on that first occurrence of "Commission" in s. 144(1), i.e., the reference to the body that can do the revoking, is the term precise and unequivocal, capable of only one meaning? If so, we should simply apply it.{6} However, if the language is ambiguous, we must apply principles of statutory interpretation to decide whether the s. 144(1) authority extends to the Tribunal. As we will explain, we conclude that where the word "Commission" appears in the Securities Act, it can reasonably be read as either including or excluding the Tribunal, depending on the context. We must resolve the ambiguity.

[21] In deciding whether "Commission" is ambiguous, we did not limit ourselves to isolating the word and assessing its inherent ambiguity. We also referred to other occurrences of the word. This approach of considering other occurrences is consistent with Binance's submission that we should look at how "Commission" is defined in the Securities Commission Act, 2021 to help understand the meaning of "Commission" in s. 144 of the Securities Act. When we look to other instances within the Securities Act itself, we conclude that "Commission" is ambiguous, because there is at least one instance of the word "Commission" in the Securities Act where the legislature has clearly intended it to include the Tribunal, and there is at least one instance where the legislature clearly intended it not to. We examine each of these in turn.

[22] The word "Commission" clearly includes the Tribunal in s. 1(1) of theSecurities Act, which defines "Commission" to be "the Ontario Securities Commission continued under the Securities Commission Act, 2021".{7} That definition mirrors the definition of "Commission" found in the Securities Commission Act, 2021. Under these definitions, the Commission includes the Tribunal because the legal entity of the Commission is continued, and the legal entity contains within it the Tribunal "as a division of the Commission", according to s. 25 of the Securities Commission Act, 2021.

[23] In contrast, the word "Commission" clearly does not include the Tribunal in the definition of "Ontario securities law" in s. 1(1) of the Securities Act. That definition refers to decisions of "the Commission, the Tribunal or a Director". In that phrase, the word "Commission" must exclude the Tribunal, or else there would have been no need to mention the Tribunal.

[24] These examples demonstrate the ambiguity of the word "Commission" when looking at the statute overall. In reaching that conclusion, we distinguish ambiguity from absurdity. We consider absurdity to arise when there are instances of a word or phrase where the text superficially permits a particular interpretation but that interpretation would yield an absurd result (examples of which we cite below). In the case of the definition of "Ontario securities law", the problem is more than saying it would be absurd for "Commission" to include the Tribunal; the problem is that the words do not permit that interpretation. As a result, we are highlighting the legislature's clear intention to use "Commission" in different ways, depending on the context. In the face of this kind of ambiguity, one must examine each occurrence on its own, and turn to other rules and aids to assist with interpreting that occurrence. We do that now with respect to s. 144(1).

2.5 Consistent expression

[25] We begin that interpretation exercise by considering the idea of consistent expression. A word or expression is presumed to have the same meaning throughout a statute, so that the statute is internally consistent.{8} As with all "rules" of statutory interpretation, though, the rule of consistent expression is not inflexible. It is an aid to construction, and we must exercise our judgment to decide what weight to attach to the rule.{9}

[26] We have already shown that the legislature did not intend the word "Commission" to have a consistent meaning throughout the Securities Act. Further, if all instances of "Commission" in the statute were to bear the interpretation that Binance proposes for s. 144(1) (i.e., that it includes the Tribunal), the Tribunal would arguably be authorized to exercise powers granted to the Commission, with absurd results that include these examples:

a. the power under s. 11 of the Securities Act to appoint investigators, which would radically undermine rather than reinforce the separation of the investigation and adjudication functions; and

b. the power under s. 143 of the Securities Act to make rules in respect of a wide range of policy matters, including those relating to registration, the solicitation of trades, and record-keeping requirements, which would clothe the Tribunal with a quasi-legislative function that is antithetical to the adjudicative role of the Tribunal.

[27] Even more strikingly, it would yield an absurd result within s. 144(1) itself. If both occurrences of "Commission" within s. 144(1) include the Tribunal, then the Commission (including its executive function, e.g., the Chief Executive Officer) could revoke an order of the Tribunal. For example, if Staff of the Commission were to bring an enforcement proceeding before the Tribunal, and were dissatisfied with the outcome, then instead of appealing the decision to the Divisional Court as contemplated by s. 10 of the Securities Act, the Commission could simply revoke the Tribunal's order at the conclusion of the proceeding. Such an interpretation would be nonsensical on its own, and worse, it could, in a particular matter, lead to a never-ending cycle of the Commission (through its executive function) and the Tribunal revoking each other's orders.

[28] Where the rule of consistent expression would yield the kinds of absurdities cited above, we ought not to apply it.{10} The rule is therefore of no help to us here.

2.6 Applying context and legislative purpose

[29] We turn to what has been described as the modern approach to statutory interpretation, which calls on us to interpret a provision in its total context and in a manner that complies with the legislative text, promotes the legislative purpose, and produces a reasonable and just meaning.{11}

[30] As we engage in that exercise, we note the great emphasis Binance places on the fact that the 2022 amendments did not effect any consequential change to the text of s. 144(1). As a result, says Binance, those amendments do not oust the long-standing role of the Commission's adjudicative function with respect to s. 11 investigation orders.

[31] We cannot accept this singular focus on s. 144(1). The modern approach to statutory interpretation requires us to examine the full context, and as we noted above, that context includes the new s. 144.1.

[32] As for legislative purpose, that can be elusive. Binance submits that the 2022 amendments demonstrate the legislature's intent to enhance the Tribunal's oversight authority over the Commission, including over the Commission's investigatory activities. However, Binance did not offer any persuasive support for that assertion. The amendments clearly further the independence of the Tribunal, but we see no indication that the legislature intended the Tribunal to take on the greater supervisory role that Binance urges. Indeed, such a supervisory role over investigations would compromise rather than strengthen the Tribunal's independence, so we would need to see clear evidence of such a legislative intent. There is none.

[33] Indeed, the passage from the relevant legislative debates that Binance quoted in its submissions undermines rather than supports its position. According to remarks of the government representative at Second Reading of the amending bill, the new Tribunal "would ensure a clear separation between the regulatory and the policy functions of the commission [sic] and its adjudicative function."{12} The Commission's investigations are a regulatory function that should be clearly separated from, not supervised by, the Tribunal.

[34] In discussing legislative intent, we asked Binance for its position as to why the legislature added s. 144.1 as part of the 2022 amendments. If both occurrences of "Commission" include the Tribunal in s. 144(1), then that provision empowers the Tribunal to revoke an order of the Tribunal. That would make s. 144.1 completely unnecessary, since it accomplishes the same thing.

[35] In response, Binance submitted that s. 144.1 was added to make clear that it is only the Tribunal that can revoke an order of the Tribunal. We reject that submission. The words of s. 144(1) and s. 144.1 are more consistent with parallel grants of authority than they are with one section limiting the other. Had the legislature intended s. 144.1 to limit s. 144, it could easily have included clear language (e.g., "subject to") to do so.

[36] Binance's argument that s. 144.1 is meant to limit s. 144 is further undermined by similar occurrences of parallel provisions. One such instance is in subsections 127(5) and 127(5.1), which empower the Tribunal and the Commission, respectively, to make certain temporary orders. The two provisions are identical, except that one grants the authority to the Tribunal and the other grants the same authority to the Commission. Binance's submission about the function of s. 144.1 (i.e., limiting the Commission's authority) could not logically apply to this pair of parallel provisions. This is not fatal to Binance's argument on the point, but it makes it less persuasive.

[37] Staff submitted that we should also rely on s. 3 of the Transitional Matters Regulation{13} made under the Securities Commission Act, 2021. That section of the regulation empowers the Tribunal, under s. 144.1 of the Securities Act, to revoke or vary certain types of orders that the Commission made before the creation of the Tribunal. Staff submitted that such a provision would be unnecessary if, as Binance argues, that power already exists within s. 144(1).

[38] We are not persuaded by that argument. As Binance argued, the types of orders listed in s. 3 of the regulation are limited to orders that the prior adjudicative function of the Commission could have made. Accordingly, it is reasonable to conclude that the legislature merely intended to extend the application of s. 144.1(1) to orders made by the Tribunal's predecessor, before the Tribunal existed in its current form. We consider the existence of s. 3 of the regulation to be a neutral factor in our decision and reasoning.

[39] The final point we address in the context of legislative purpose is Binance's submission that the result Staff seeks would mean that a party seeking to challenge a s. 11 order would be left without an effective means of doing so. We disagree. Section 144(1) of the Securities Act expressly contemplates an application to the Commission (i.e., its executive function) for revocation or variation. In addition, we heard no submission to suggest that whatever routes may have been available through the courts have been changed in any way by the 2022 amendments. We understand the argument that there may be practical challenges associated with both of these options, but even if we were to so find, we could not rely on such a finding to clothe the Tribunal with jurisdiction it does not have. The Tribunal is a creature of statute with no inherent jurisdiction. It can exercise only those powers the legislature gives it, even if that leaves parties with options they consider less than ideal.{14}

[40] We concluded that in s. 144(1) of the Securities Act, the term "Commission" does not include the Tribunal. We therefore determined that s.144 does not give the Tribunal jurisdiction to revoke or vary a s. 11 order.

[41] Binance also asked that we quash a summons issued under s. 13 of the Securities Act, by a person appointed as an investigator under the s. 11 order. Given our decision that the Tribunal lacks jurisdiction to revoke the s. 11 order, we have no jurisdiction to consider the request to quash the summons.

[42] One final note is in order. At the hearing devoted to the jurisdictional question, we asked the parties for additional submissions about other occurrences of the word "Commission" in the Securities Act, and about potential issues arising from the interplay between "Commission" and "Director" in various provisions. In those additional submissions, it was common ground that we need not, and should not, address those issues in our decision. We agree. Accordingly, our decision and these reasons resolve only the interpretation of "Commission" in s. 144 of the Securities Act.

[43] In the result, we dismissed Binance's application.

Dated at Toronto this 14th day of July, 2023

{1} Binance Holdings Limited (Re), (2023) 46 OSCB 5019

{2} RSO 1990, c S.5

{3} Bridging Finance Inc (Re), 2022 ONSEC 3 at para 9

{4} (2003) 26 OSCB 1307

{5} Securities Commission Act, 2021, SO 2021, c 8, Sch 9, s 25

{6} Canada Trustco Mortgage Co v Canada, 2005 SCC 54 at para 10; R v McIntosh, 1995 CanLII 124 (SCC) at para 34

{7} Securities Commission Act, 2021, SO 2021 c*, Sched 9

{8} R v Zeolkowski, 1989 CanLII 72 (SCC), [1989] 1 SCR 1378 at 1387; Bapoo v Co-operators General Insurance Co., 1997 CanLII 6320 (ON CA) (Bapoo) at para 27

{9} Bapoo at para 28

{10} R v Middleton, 2009 SCC 21 at paras 14-16

{11} Bapoo at para 8

{12} Ontario, Legislative Assembly, Official Report of Debates (Hansard), 42nd Parl, 1st Sess, No 240 (29 March 2021) at 12318 (Stan Cho)

{13} O Reg 43/22, s 3, Schedule "B"

{14} B (Re), 2020 ONSEC 21 at para 17

CSA Notice regarding Coordinated Blanket Order 13-932 Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval +

July 17, 2023

The Canadian Securities Administrators (the CSA or we) are publishing substantively harmonized exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval + (SEDAR+).

Every member of the CSA is implementing the relief through a local blanket order entitled Coordinated Blanket Order 13-932 Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval + (collectively, Blanket Order 13-932). Although the outcome is the same in all CSA jurisdictions, the language of the blanket order issued by each province or territory may not be identical because each jurisdiction's blanket order must fit within the authority provided in local securities legislation.

The National Systems Renewal Program is an initiative of the CSA that will replace existing CSA national systems with a centralized system, SEDAR+. The first phase of SEDAR+ will replace the System for Electronic Document Analysis and Retrieval (SEDAR), the National Cease Trade Order Database, the Disciplined List, and certain filings in the British Columbia Securities Commission's eServices system and the Ontario Securities Commission's electronic filing portal.

SEDAR will no longer be available for filing as of 11 p.m. Eastern time on July 20, 2023. In order to accommodate the transfer of system data, there will be a period of time (the cutover period) during which SEDAR+ will not be available for filing. We anticipate that SEDAR+ will become available for filing at 7 a.m. Eastern time on July 25, 2023.

On June 9, 2023, National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (NI 13-103) came into force and National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) was repealed. As the launch of SEDAR+ was deferred, the CSA issued Coordinated Blanket Order 13-931 Exemptions from certain filing requirements in connection with the deferred launch of the System for Electronic Data Analysis and Retrieval + (Blanket Order 13-931) so that a person or company could continue to file on SEDAR.

During the cutover period, neither SEDAR nor SEDAR+ will be available for filing.

Blanket Order 13-932 revokes Blanket Order 13-931 and provides substantially the same relief as Coordinated Blanket Order 13-930 Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval +, which was published on May 11, 2023 but then revoked by Blanket Order 13-931 before coming into effect. Blanket Order 13-932 will essentially provide filers with an extension to file with, or deliver to, a securities regulatory authority or regulator documents that are required to be transmitted through SEDAR+ during the cutover period. However, as we recognize that there may be limited circumstances in which a person or company may wish to file or deliver certain documents during the cutover period, Blanket Order 13-932 also includes an exemption that provides filers with alternative means by which they can transmit a document, as specified in the appendix to Blanket Order 13-932 for each jurisdiction.{1}

The exemptions only apply to documents that will be required by NI 13-103 to be filed or delivered through SEDAR+. Accordingly, the exemptions do not apply to documents that will continue to be filed or delivered outside of SEDAR+, such as documents filed or delivered by insiders, registrants, derivatives market participants or regulated entities. Similarly, the exemptions do not apply to documents that are excluded by section 3 of NI 13-103 from being filed or delivered through SEDAR+, such as confidential material change reports. Blanket Order 13-932 also does not relieve a filer from any requirement under securities legislation to issue a news release or deliver a document to securityholders.

Exemption from certain filing and delivery requirements during the cutover period

As SEDAR+ will not be available during the cutover period, a person or company that is required to file or deliver a document through SEDAR+ to meet a deadline arising during the cutover period may rely on the exemption in Blanket Order 13-932 from those filing or delivery requirements. This exemption would be available, for example, for any continuous disclosure documents that are required to be filed by issuers during the cutover period, such as financial statements and business acquisition reports.

A person or company that relies on this exemption is subject to a condition to transmit the document through SEDAR+ no later than 2 business days after the cutover end date (as defined below). NI 13-103 and other applicable legislation will require any applicable system and regulatory fees to be paid at the time of transmitting the document through SEDAR+.

Exemption from the requirement to transmit through SEDAR+ during the cutover period

We anticipate that there will be exceptional circumstances where a person or company may choose to file or deliver certain documents during the cutover period. This could be to facilitate certain transactions, such as submitting documents in connection with a prospectus, a fund facts document or an ETF facts document for a distribution that will occur during or shortly after the cutover period. Blanket Order 13-932 therefore also provides an exemption from the requirement to transmit a document through SEDAR+ during the cutover period and allows the person or company to transmit the document by alternative means, as set out in the appendix to Blanket Order 13-932.

Filers that rely on this exemption are reminded that they must transmit the document to each applicable jurisdiction. They must also transmit the document through SEDAR+ no later than 2 business days after the cutover end date (as defined below) and will be required by NI 13-103 and other applicable securities legislation to pay any applicable system and regulatory fees at the time of transmitting the document through SEDAR+.

If a person or company chooses to file a prospectus during the cutover period, the person or company must, with respect to required documents in connection with the prospectus that are to be filed or delivered during the cutover period, file or deliver those documents in the manner set out in the appendix to Blanket Order 13-932, and must indicate in the cover letter whether the prospectus is being filed under Multilateral Instrument 11-102 Passport System.

Term of Blanket Order 13-932

Although Blanket Order 13-932 is being published today, the exemptions in Blanket Order 13-932 can only be relied on during the cutover period, which starts on July 21, 2023 and ends on the earlier of when SEDAR+ is available for filing and July 28, 2023 (the cutover end date). Blanket Order 13-932 will have no effect after the cutover end date.

Blanket Order 13-932 revokes Blanket Order 13-931 effective July 21, 2023, so that filers can continue to rely on Blanket Order 13-931 before the cutover period.

If you have any questions regarding Blanket Order 13-932, please contact any of the following:

{1} Although Blanket Order 13-932 is local, the alternative means of filing for all jurisdictions is included in the appendix to Blanket Order 13-932, for ease of reference.

CSA Notice regarding Coordinated Blanket Order 13-933 Temporary exemption from the requirement to transmit a report of exempt distribution through SEDAR+ in connection with distributions of eligible foreign securities to permitted clients

July 20, 2023

The Canadian Securities Administrators (the CSA or we) are publishing substantively harmonized exemptions from the requirement to transmit a Form 45-106F1 Report of Exempt Distribution (Report of Exempt Distribution) through the System for Electronic Data Analysis and Retrieval + (SEDAR+) subject to certain conditions.

Every member of the CSA is implementing the relief through a local blanket order entitled Coordinated Blanket Order 13-933 Temporary exemption from the requirement to transmit a report of exempt distribution through SEDAR+ in connection with distributions of eligible foreign securities to permitted clients (collectively, the blanket order). Although the outcome is the same in all CSA jurisdictions, the language of the blanket order issued by each province or territory may not be identical because each jurisdiction's blanket order must fit within the authority provided in local securities legislation.

On June 9, 2023, National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (NI 13-103) came into force. Pursuant to NI 13-103, a Report of Exempt Distribution must be transmitted through SEDAR+.

The blanket order provides an exemption from the requirement to transmit a Report of Exempt Distribution through SEDAR+ for a distribution of an "eligible foreign security" to a "permitted client", as such terms are defined in the Report of Exempt Distribution. A person or company eligible to rely on the blanket order must file the form of report in Appendix B to the blanket order{1} in each jurisdiction where a distribution occurred in the manner set out in Appendix A to the blanket order.{2}

In jurisdictions where a copy of an offering memorandum provided to a prospective purchaser is required to be delivered to the securities regulatory authority or regulator, the blanket order also provides an exemption from the requirement to transmit the offering memorandum through SEDAR+ provided that it is transmitted in the manner set out in Appendix A to the blanket order.

The exemption is available to allow the CSA to consider potential enhancements to the functionality of SEDAR+.

The blanket order does not otherwise relieve a person or company from any of the reporting requirements in Part 6 of National Instrument 45-106 Prospectus Exemptions or the filing fees or late fees in respect of the Report of Exempt Distribution. Reports of Exempt Distribution filed in reliance on the blanket order will be publicly available on request made to the CSA members.

The blanket order will come into effect on July 21, 2023. In certain jurisdictions, the blanket order includes an expiry date based on the term limits for blanket orders in the jurisdiction.{3} We expect that the blanket order will be revoked or replaced before the expiry date. We will provide advance notice before revoking or replacing the blanket order.

If you have any questions regarding the blanket order, please contact any of the following:

{1} The version of the report in Appendix B is based on the version of the report that was in force on June 8, 2023. The Report of Exempt Distribution was amended on June 9, 2023, to remove certain information captured by a SEDAR+ profile, to reduce duplication, but the issuers whose securities are being reported in reliance on the blanket order are not likely to have a SEDAR+ profile.

{2} Although the blanket order is local, the alternative manner of filing for all jurisdictions is included in Appendix A to the blanket order, for ease of reference. In all jurisdictions, filers must use the Excel spreadsheets for Schedule 1 and Schedule 2 of the report that are available on the Canadian Securities Administrators website at the following address: https://www.securities-administrators.ca/resources/reports-of-exempt-distribution/. In Ontario, the blanket order also requires filers use the fillable PDF form available on that website. The fillable PDF may not be used in Québec and its use is optional in jurisdictions other than Ontario and Québec

{3} For example, in Ontario, the term of the blanket order is 18 months.

Notice of Commission Approval of OSC Rule 52-503 Exemption from Disclosure of a Specified Financial Measure

July 20, 2023

On June 27, 2023, the Ontario Securities Commission (the Commission or we) made proposed OSC Rule 52-503 Exemption from Disclosure of a Specified Financial Measure (the Rule) as a rule under the Securities Act (Ontario) (the Act).

The Rule will, if approved by the Minister of Finance, provide an exemption in Ontario from National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure (NI 52-112) for a reporting issuer that is, or that has a subsidiary or an affiliate that is, a "federal financial institution" as defined in the Bank Act (Canada) and subject to OSFI Guidelines.

Under the Bank Act, "federal financial institution" means (a) a bank, (b) a body corporate to which the Trust and Loan Companies Act (Canada) applies, (c) an association to which the Cooperative Credit Associations Act (Canada) applies, or (d) an insurance company or a fraternal benefit society incorporated or formed under the Insurance Companies Act (Canada).

The purpose of the Rule is to make permanent the exemption set out in a blanket order issued on December 2, 2021, Ontario Instrument 52-502 Exemption from National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure (Interim Class Order) (the Class Order). The Class Order ceased to be effective on June 2, 2023. Blanket orders similar to the Class Order have been issued by members of the Canadian Securities Administrators (CSA). These blanket orders do not have a limited duration. The Rule will have the same effect as the orders granted by the other CSA members.

The Class Order provided an exemption to eligible issuers from NI 52-112 in respect of disclosure of a specified financial measure pursuant to an OSFI Guideline, if (a) the OSFI Guideline specifies the composition of the measure and the measure was determined in compliance with that OSFI Guideline, and (b) in proximity to the measure, the eligible issuer discloses the OSFI Guideline under which the measure is disclosed.

Terms defined in NI 52-112 and the Rule have the same meaning as used in this Notice.

The Commission has made the Rule as a rule pursuant to paragraph 143.2(5)(b) of the Act. Paragraph 143.2(5)(b) provides that publication of a notice and request for comment in respect of a proposed rule is not required if "the proposed rule grants an exemption or removes a restriction and is not likely to have a substantial effect on the interests of persons or companies other than those who benefit under it". We have determined that the Rule meets the criteria set out in paragraph 143.2(5)(b) of the Act. Accordingly, for this reason the Rule is not being published for comment.

The Rule was delivered to the Minister of Finance (the Minister) on July 19, 2023

The Minister may approve or reject the Rule or return it for further consideration. If the Minister approves the Rule or does not take any further action, the Rule will come into force on October 3, 2023.

The text of the Rule is contained in Annex A of this notice and is also available on the OSC website at www.osc.ca.

The primary objective of NI 52-112 is to help ensure investors receive, among other things, transparent and understandable information about financial measures that are not prepared in accordance with Generally Accepted Accounting Principles (GAAP). The OSFI Guidelines specify the composition of certain specified financial measures and contain specific disclosure requirements related to such measures. The Rule is intended to reduce regulatory burden for eligible issuers that are subject to OSFI Guidelines since sufficient disclosure exists surrounding these measures.

Although NI 52-112 contains an application exception in respect of disclosure of a specified financial measure that is required under law, such exception does not apply to the OSFI Guidelines because they are not law.

The Rule is based on a policy rationale that influenced the application exception in subparagraph 4(1)(e) of NI 52-112. The Rule is intended to substantially mirror the current application exception in respect of disclosure of a specified financial measure that is required under law to measure(s) that are disclosed by an eligible issuer in accordance with an OSFI Guideline. In essence, the Rule recognizes that although OSFI Guidelines are not law, an eligible issuer subject to OSFI Guidelines is required to comply with such requirements.

Consistent with subparagraph 4(1)(e) of NI 52-112, the Rule would limit the exception to specified financial measures where the OSFI Guideline specifies the composition of the measure and the measure was determined in compliance with that OSFI Guideline and in proximity to the measure, the eligible issuer discloses the OSFI Guideline under which the measure is disclosed.

The following provisions of the Act provide the Commission with authority to adopt the Rule:

• Paragraph 143(1)16

• Paragraph 143(1)22

• Paragraph 143(1)22.1

• Paragraphs 143(1)25

• Paragraphs 143(1)39

If you have any questions regarding the Rule, please contact any of the following:

1. Definitions

(1) In this Rule,

"Act" means the Securities Act, R.S.O. 1990, c. S.5, as amended from time to time;

"Bank Act" means the Bank Act (Canada);

"eligible issuer" means a reporting issuer that is, or that has a subsidiary or an affiliate that is, a federal financial institution subject to OSFI Guidelines;

"federal financial institution" has the same meaning as in the Bank Act;

"NI 14-101" means National Instrument 14-101 Definitions;

"NI 52-112" means National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure;

"OSFI" means the Office of the Superintendent of Financial Institutions of the Government of Canada; and

"OSFI Guideline" means any guideline or advisory guidance of OSFI that includes "best" or "prudent" practices that OSFI expects a federal financial institution to follow, clarifies OSFI's position regarding certain policy issues applicable to the federal financial institution or describes how OSFI administers and interprets provisions of the Bank Act or other applicable federal financial institution legislation.

(2) Terms used in this Rule that are defined in the Act, NI 14-101 and NI 52-112 have the same meaning if used in this Rule, unless otherwise defined in this Rule.

2. NI 52-112 does not apply to an eligible issuer in respect of disclosure of a specified financial measure pursuant to an OSFI Guideline, if

(a) the OSFI Guideline specifies the composition of the measure, and the measure was determined in compliance with that OSFI Guideline, and

(b) in proximity to the measure, the eligible issuer discloses the OSFI Guideline under which the measure is disclosed.

3. This Rule comes into force on October 3, 2023.

Ontario Securities Commission -- Coordinated Blanket Order 13-932 -- Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval +

Citation: Re Exemptions from certain filing requirements in connection with the launch of the System for Electronic Data Analysis and Retrieval +

July 17, 2023

1. Terms defined in the Securities Act (Ontario) (the Act) and National Instrument 14-101 Definitions have the same meanings in this order.

2. In this order:

"cutover end date" means the earlier of the date on which SEDAR+ becomes available for filing and July 28, 2023;

"cutover period" means the period beginning on July 21, 2023 and ending on the cutover end date;

"deferral blanket order" means Coordinated Blanket Order 13-931 Exemptions from certain filing requirements in connection with the deferred launch of the System for Electronic Data Analysis and Retrieval +.

3. The National Systems Renewal Program is an initiative of the CSA that will replace existing CSA national systems with a centralized system, the System for Electronic Data Analysis and Retrieval + (SEDAR+). The first phase of SEDAR+ will replace the System for Electronic Document Analysis and Retrieval (SEDAR), the National Cease Trade Order Database, the Disciplined List, and certain filings in the British Columbia Securities Commission's eServices system and the Ontario Securities Commission's electronic filing portal.

4. On June 1, 2023, the CSA announced that the launch of SEDAR+ would be deferred.

5. On June 9, 2023, National Instrument 13-101 System for Electronic Document Analysis and Retrieval (SEDAR) was repealed and National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (NI 13-103) was adopted. NI 13-103 requires a person or company to transmit through SEDAR+ certain documents required or permitted under securities legislation to be filed with or delivered to a securities regulatory authority or regulator. The deferral blanket order provides exemptions from certain requirements of NI 13-103 to address the deferral of the launch of SEDAR+.

6. The CSA intends to launch SEDAR+ on July 25, 2023. In order to accommodate the transfer of required system data, neither SEDAR nor SEDAR+ will be available for filing during the cutover period.

7. During the cutover period, a person or company will not be able to comply with the requirement in NI 13-103 to file a document with, or deliver a document to, the securities regulatory authority or regulator by transmitting it through SEDAR+ and would not be able to comply with the conditions of the exemptions in the deferral blanket order to transmit a document through SEDAR.

8. This order does not relieve a person or company from any requirement under securities legislation to issue a news release or deliver a document to securityholders.

Exemption from the requirement to file or deliver a document during the cutover period

9. The Commission, considering that to do so would not be prejudicial to the public interest, orders under subsection 143.11(2) of the Act that, in respect of a document that is required to be transmitted through SEDAR+ under NI 13-103, a person or company is exempt from the requirement to file the document with, or deliver the document to, the securities regulatory authority or regulator under securities legislation during the cutover period, provided that the person or company files or delivers the document through SEDAR+ no later than 2 business days after the cutover end date.

Exemption from the requirement to transmit a document through SEDAR+ during the cutover period

10. The Commission, considering that to do so would not be prejudicial to the public interest, orders under subsection 143.11(2) of the Act that a person or company is exempt from the requirement in section 2 of NI 13-103 to transmit a document through SEDAR+ during the cutover period, provided that the person or company transmits the document to the securities regulatory authority or regulator

(a) as set out in the Appendix to this order, and

(b) through SEDAR+ no later than 2 business days after the cutover end date.

11. The Commission, considering that to do so would not be prejudicial to the public interest, orders under subsection 143.11(2) of the Act that in respect of a document that is required to be transmitted through SEDAR+ under NI 13-103, a person or company filing the document with, or delivering a document to, the securities regulatory authority or regulator as contemplated in paragraph 10(a) of this order is exempt from the requirements in sections 32, 34 and 35 of Ontario Securities Commission Rule 13-502 Fees, provided the person or company pays the fee at the time of filing or delivering the document through SEDAR+.

12. The Commission orders that the deferral blanket order is revoked.

13. This order comes into effect on July 21, 2023.

For the Commission:

"D. Grant Vingoe"Chief Executive OfficerOntario Securities Commission

Jurisdictions |

General filing methods |

Exceptions to general filing methods |

|

||

British Columbia |

cutover@bcsc.bc.ca |

N/A |

|

||

Alberta |

transition@asc.ca |

Submit an application to the Commission or the Executive Director to legalapplications@asc.ca |

|

||

Saskatchewan |

corpfin@gov.sk.ca |

N/A |

|

||

Manitoba |

securities@gov.mb.ca |

N/A |

|

||

Ontario |

For investment funds: |

N/A |

IF_SEDARplus_cutover@osc.gov.on.ca |

||

|

||

and for all other cases: |

||

CF_SEDARplus_cutover@osc.gov.on.ca |

||

|

||

Québec |

For investment funds: Fonds_dinvestissement@lautorite.qc.ca |

CPC qualifying transaction filings are to be filed by email at the general email address or in paper at 800, rue du Square-Victoria, bureau 2200, Montréal (Québec) H3C 0B4 |

|

||

and for all other cases: Dispenses.passeport@lautorite.qc.ca |

||

|

||

New Brunswick |

transition@fcnb.ca |

Community Economic Development (CEDC) filings (forms under local NB rule 45-509) are to be filed by email at the general email or in paper at 300-85 Charlotte Street, Saint John, NB E2L 2J2 |

|

||

Nova Scotia |

NSSC_Corp_Finance@novascotia.ca |

An application that is not a full or partial revocation application is to be filed at NSSCEXEMPTIONS@novascotia.ca |

|

||

Prince Edward Island |

ccis@gov.pe.ca |

N/A |

|

||

Newfoundland and Labrador |

SecuritiesExemptions@gov.nl.ca |

N/A |

|

||

Yukon |

securities@yukon.ca |

N/A |

|

||

Northwest Territories |

Securitiesregistry@gov.nt.ca |

N/A |

|

||

Nunavut |

securities@gov.nu.ca |

N/A |

Ontario Securities Commission -- Coordinated Blanket Order 13-933 -- Temporary exemption from the requirement to transmit a report of exempt distribution through SEDAR+ in connection with distributions of eligible foreign securities to permitted clients

Citation: Re Temporary exemption from the requirement to transmit a report of exempt distribution through SEDAR+ in connection with distributions of eligible foreign securities to permitted clients

July 20, 2023

1. Terms defined in the Securities Act (Ontario) (the Act) and National Instrument 14-101 Definitions have the same meanings in this Order.

2. In this Order:

"eligible foreign security" has the same meaning as in Form 45-106F1 Report of Exempt Distribution;

"permitted client" has the same meaning as in Form 45-106F1 Report of Exempt Distribution;

"SEDAR+" has the same meaning as in National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+).

3. On June 9, 2023, National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (NI 13-103) came into force. Pursuant to NI 13-103, Form 45-106F1 Report of Exempt Distribution (Form 45-106F1) must be transmitted through SEDAR+.

4. The purpose of this Order is to provide an exemption from transmitting certain Forms 45-106F1 through SEDAR+ while the Canadian Securities Administrators consider potential enhancements to the functionality of SEDAR+.

5. The Commission, considering that to do so would not be prejudicial to the public interest, orders under subsection 143.11(2) of the Act that a person or company is exempt from the requirement in section 2 of NI 13-103 to transmit a Form 45-106F1 through SEDAR+, provided that

(a) the Form 45-106F1 is only in respect of a distribution of an eligible foreign security to a permitted client, and

(b) the person or company transmits the Form 45-106F1 to the securities regulatory authority or regulator

(i) in the manner set out in Appendix A to this Order, and

(ii) in the form set out in Appendix B to this Order.

6. The Commission, considering that to do so would not be prejudicial to the public interest, orders under subsection 143.11(2) of the Act that a person or company is exempt from the requirement in section 2 of NI 13-103 to transmit an offering memorandum through SEDAR+, provided that

(a) the offering memorandum was provided to a prospective purchaser in connection with a distribution of an eligible foreign security to a permitted client; and

(b) the person or company transmits the offering memorandum to the securities regulatory authority or regulator in the manner set out in Appendix A to this Order.

7. This Order comes into effect on July 21, 2023.

8. This Order will expire on January 21, 2025.

For the Commission:

"D. Grant Vingoe"Chief Executive OfficerOntario Securities Commission

Jurisdiction |

Manner of Filing |

|

|

||

British Columbia |

EDR@bcsc.bc.ca |

|

|

||

Alberta |

legalapplications@asc.ca |

|

|

||

Saskatchewan |

exemptions@gov.sk.ca |

|

|

||

Manitoba |

securities@gov.mb.ca |

|

|

||

Ontario |

A Form 45-106F1 must be: |

|

(1) completed using the fillable PDF of the form set out in Appendix B to this Order that is available on the Canadian Securities Administrators website at the following address: https://www.securities-administrators.ca/resources/reports-of-exempt-distribution/; and |

||

(2) filed through the OSC electronic filing portal (https://www.osc.ca/en/filing-documents-online) in the following manner: |

||

(a) under "PDF submissions"; |

||

(b) using the "Issuer" filer category; |

||

(c) under the document type "Report of Exempt Distribution Filings"; and |

||

(d) with Schedule 1 and, if applicable, Schedule 2 uploaded in Excel format under the "Other supporting documents" section. |

||

An offering memorandum must be delivered: |

||

(1) through the OSC electronic filing portal (https://www.osc.ca/en/filing-documents-online); and |

||

(2) in either of the following manners: |

||

(a) at the same time as a Form 45-106F1, uploaded under the "Other supporting documents section"; or |

||

(b) separately from a Form 45-106F1, under the "Issuer" filer category and the document type "Any other document not identified above". |

||

|

||

Québec |

Dispenses.passeport@lautorite.qc.ca |

|

|

||

The fillable PDF of the form set out in Appendix B to this Order that is available on the Canadian Securities Administrators website may not be used. |

||

|

||

New Brunswick |

emf-md@fcnb.ca |

|

|

||

Nova Scotia |

NSSC_corp_finance@novascotia.ca |

|

|

||

Prince Edward Island |

ccis@gov.pe.ca |

|

|

||

Newfoundland and Labrador |

SecuritiesExemptions@gov.nl.ca |

|

|

||

Yukon |

Securities@Yukon.ca |

|

|

||

Northwest Territories |

securitiesregistry@gov.nt.ca |

|

|

||

Nunavut |

securities@gov.nu.ca |

|

Filed in reliance on Coordinated Blanket Order 13-933

1. Filing instructions

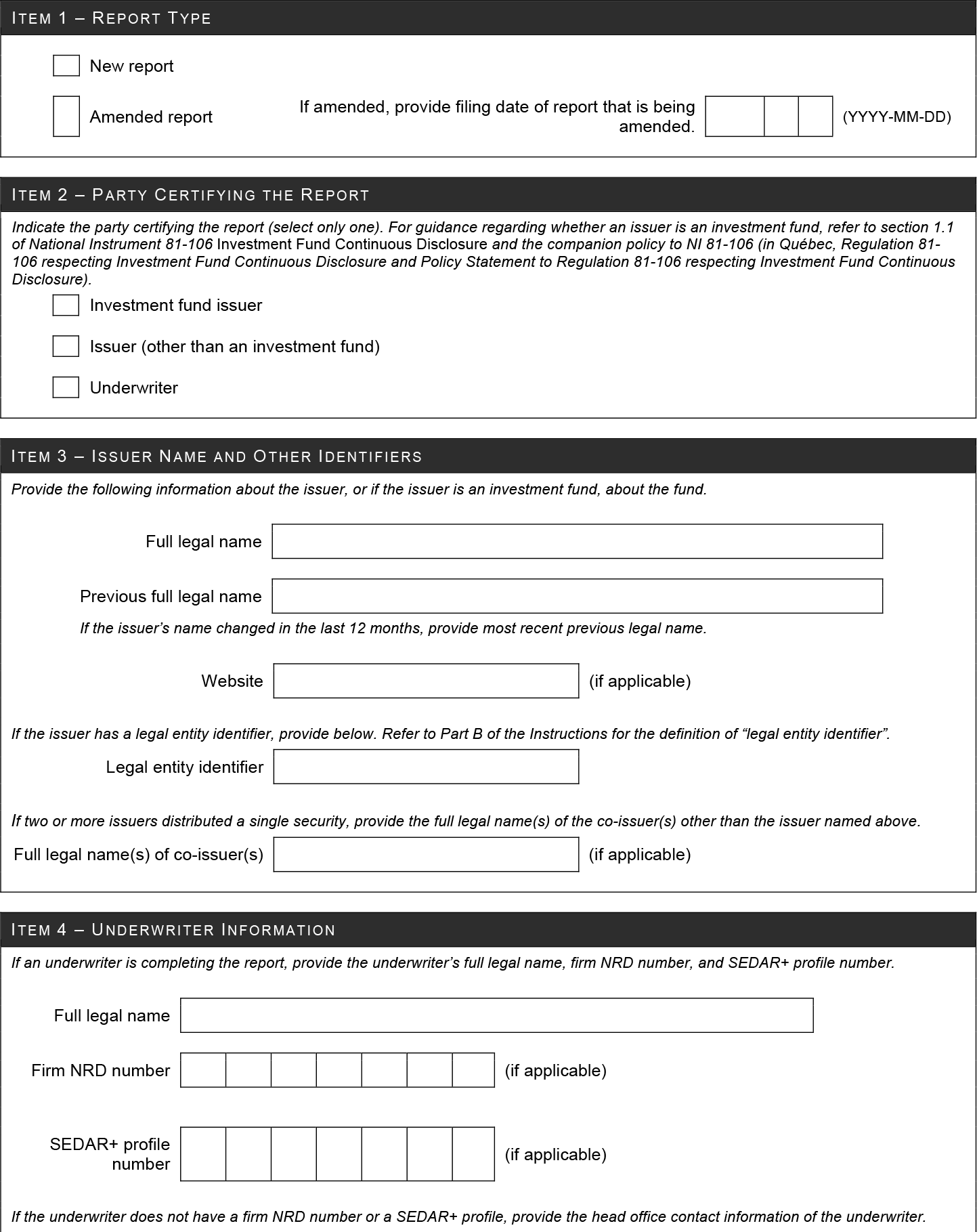

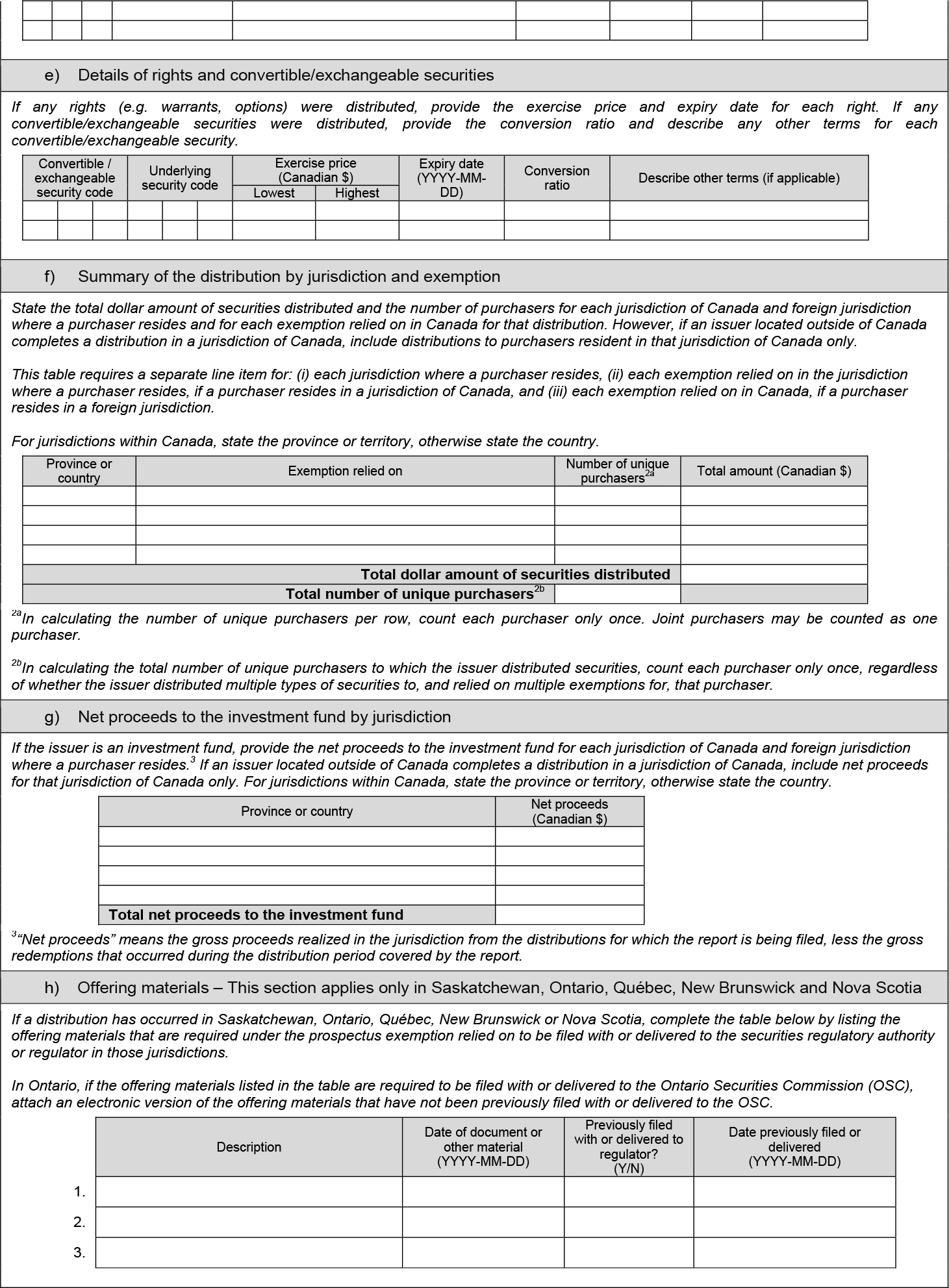

An issuer or underwriter must file the information required by this form in the manner specified in Appendix A to the blanket order. In all jurisdictions, the Excel spreadsheets for Schedule 1 and Schedule 2 that are available on the Canadian Securities Administrators website at the following address must be used: https://www.securities-administrators.ca/resources/reports-of-exempt-distribution/. In Ontario, the fillable PDF of this form available on the Canadian Securities Administrators website at that same address must be used. The fillable PDF may not be used in Québec and its use is optional in jurisdictions other than Ontario and Québec. Note: This form is only available in respect of distributions of eligible foreign securities to permitted clients as set out in Coordinated Blanket Order 13-933 Temporary exemption from the requirement to transmit a report of exempt distribution through SEDAR+ in connection with distributions of eligible foreign securities to permitted clients.

For all other reports of exempt distribution, an issuer or underwriter must file the information required by this form in the manner and using the templates specified in the System for Electronic Data Analysis and Retrieval + (SEDAR+) in accordance with National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (in Québec, Regulation 13-103 respecting System for Electronic Data Analysis and Retrieval + (SEDAR+)).

The issuer or underwriter must file the report in a jurisdiction of Canada if the distribution occurs in the jurisdiction. If a distribution is made in more than one jurisdiction of Canada, the issuer or underwriter may satisfy its obligation to file the report by completing a single report identifying all purchasers, and file the report in each jurisdiction of Canada in which the distribution occurs. Filing fees payable in a particular jurisdiction are not affected by identifying all purchasers in a single report.

In order to determine the applicable filing fee in a particular jurisdiction of Canada, consult the securities legislation of that jurisdiction.

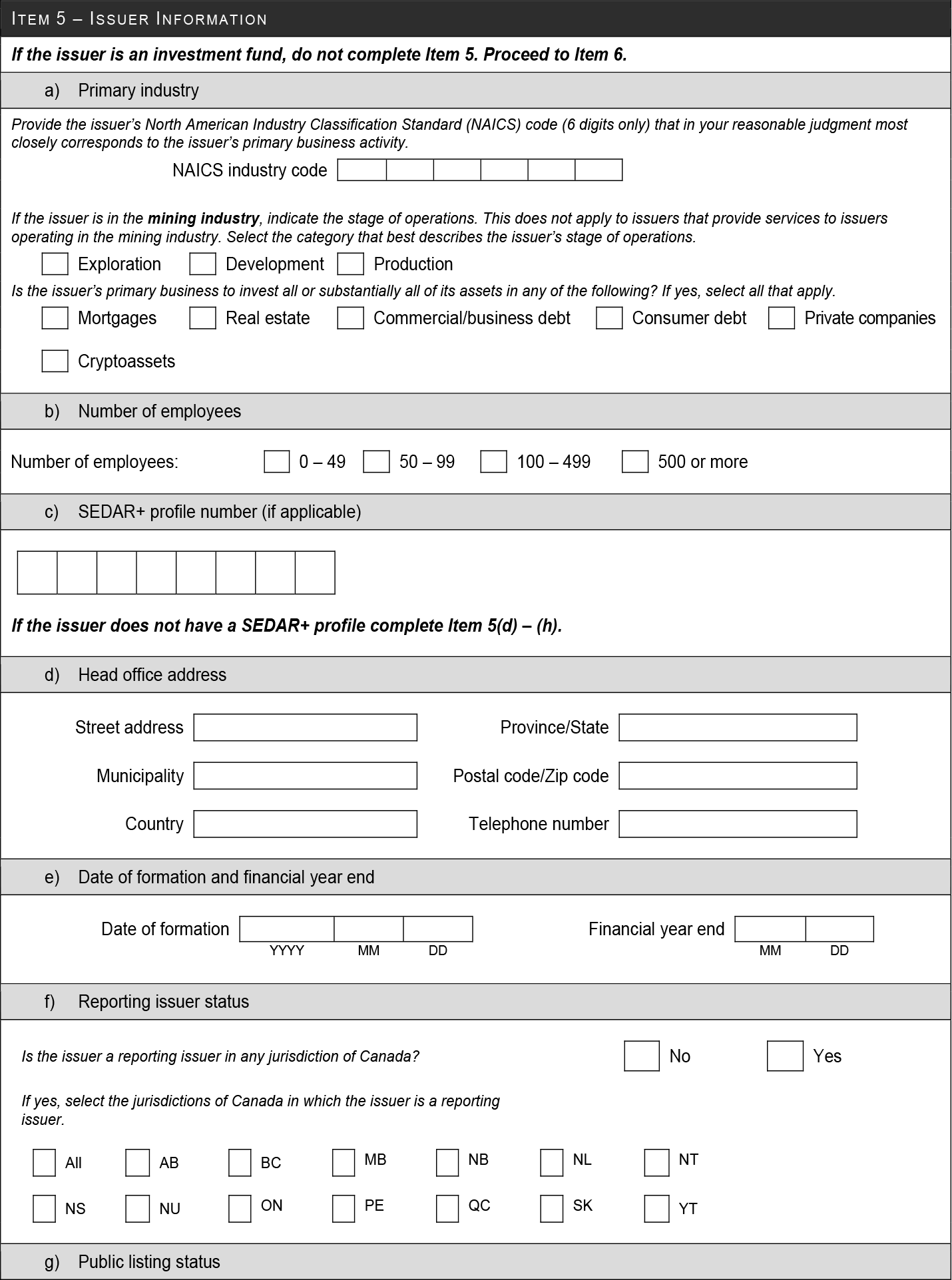

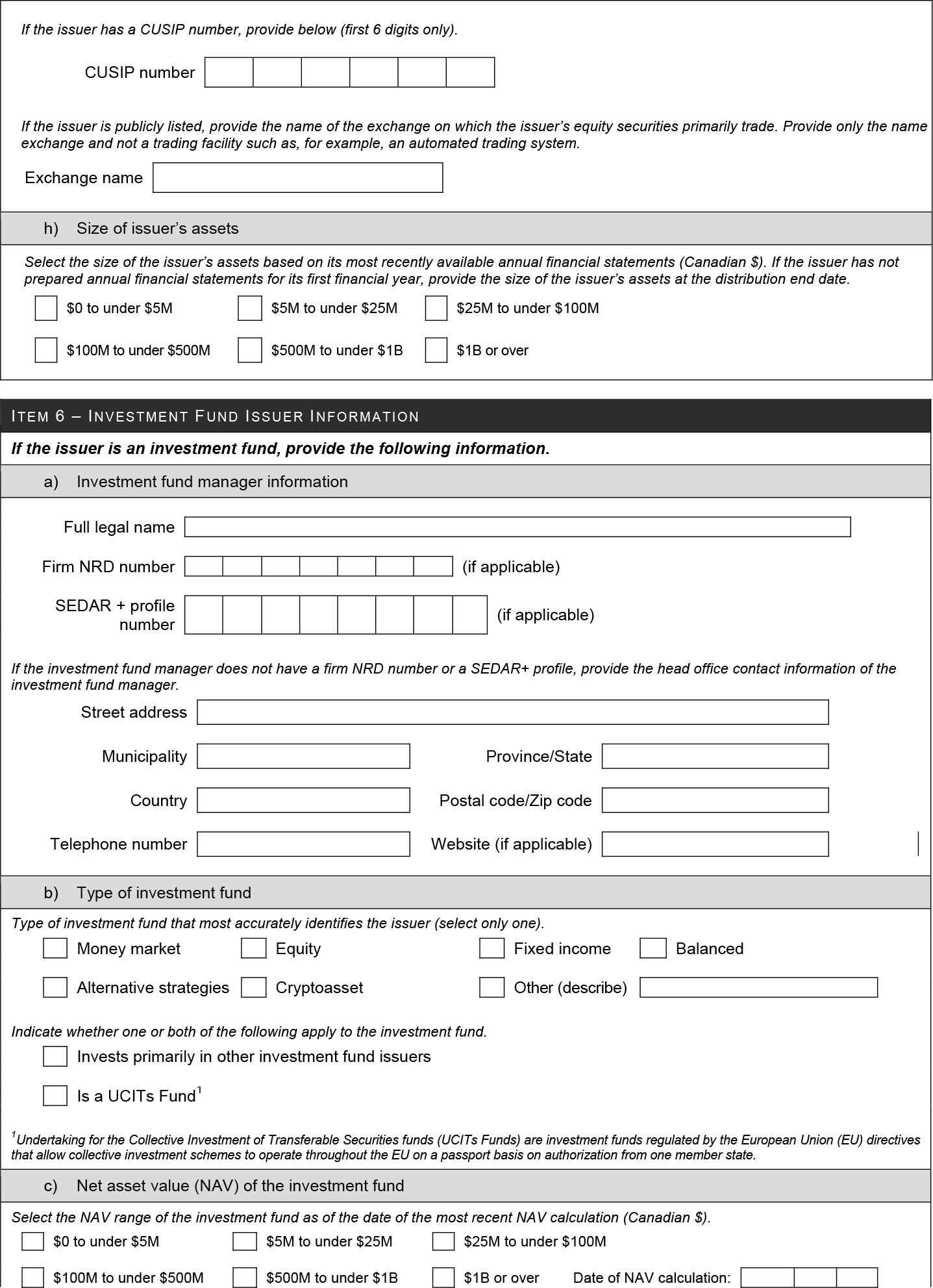

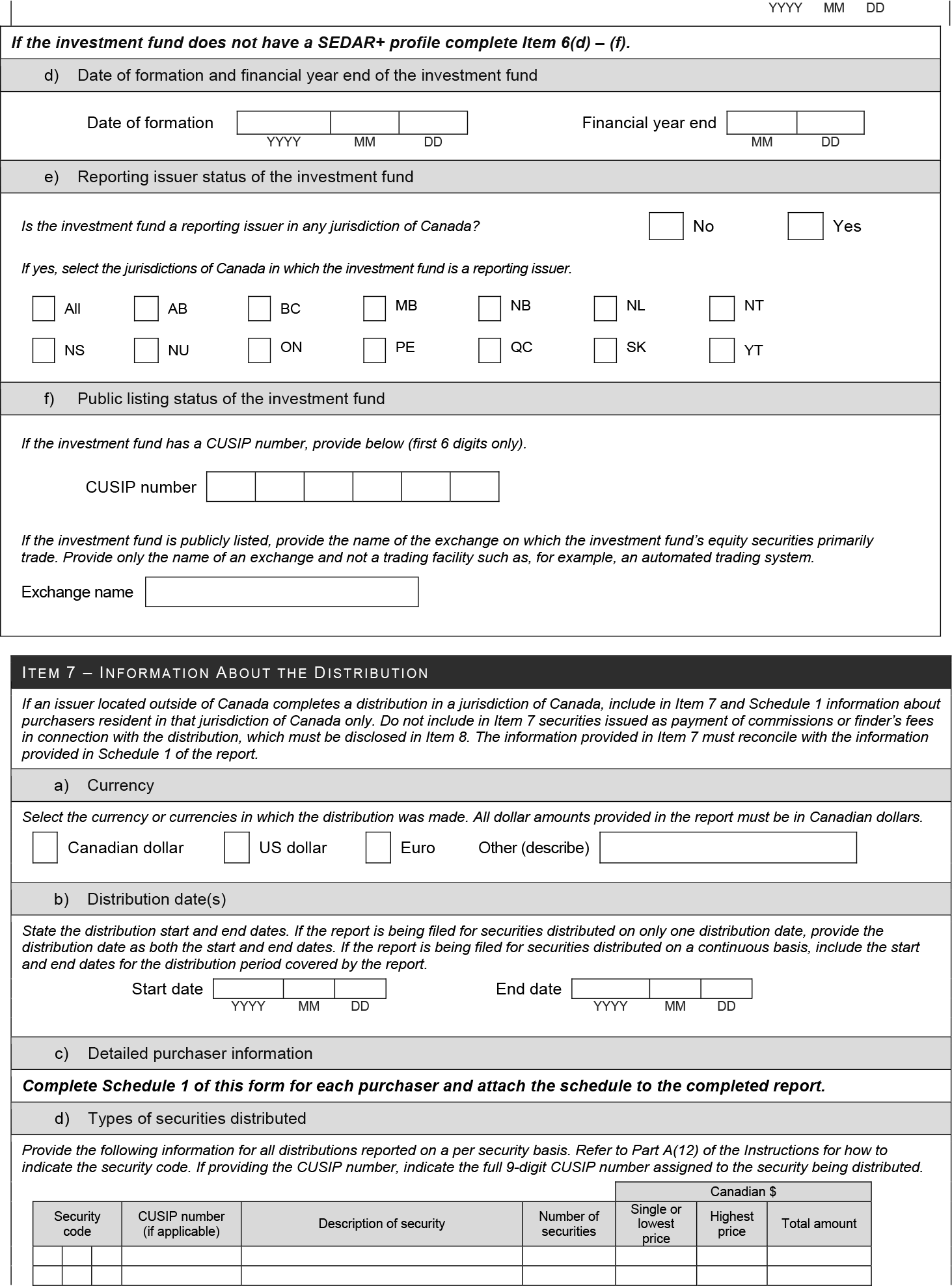

2. Issuers located outside of Canada

If an issuer located outside of Canada determines that a distribution has taken place in a jurisdiction of Canada, include information about purchasers resident in that jurisdiction only.

3. Multiple distributions

An issuer may use one report for multiple distributions occurring within 10 days of each other, provided the report is filed on or before the 10th day following the first distribution date. However, an investment fund issuer that is relying on the exemptions set out in subsection 6.2(2) of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) may file the report annually in accordance with that subsection.

4. References to purchaser

References to a purchaser in this form are to the beneficial owner of the securities.

However, if a trust company, trust corporation, or registered adviser described in paragraph (p) or (q) of the definition of "accredited investor" in section 1.1 of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) has purchased the securities on behalf of a fully managed account, provide information about the trust company, trust corporation or registered adviser only; do not include information about the beneficial owner of the fully managed account.

Joint purchasers may be treated as one purchaser for the purposes of Item 7(f) of this form.

5. References to issuer

References to "issuer" in this form include an investment fund issuer and a non-investment fund issuer, unless otherwise specified.

6. Investment fund issuers

If the issuer is an investment fund, complete Items 1-3, 6-8, 10, 11 and Schedule 1 of this form.

7. Mortgage investment entities

If the issuer is a mortgage investment entity, complete all applicable items of this form other than Item 6.

8. Language

The report must be filed in English or in French. In Québec, the issuer or underwriter must comply with linguistic rights and obligations prescribed by Québec law.

9. Currency

All dollar amounts in the report must be in Canadian dollars. If the distribution was made or any compensation was paid in connection with the distribution in a foreign currency, convert the currency to Canadian dollars using the daily exchange rate of the Bank of Canada on the distribution date. If the distribution date occurs on a date when the daily exchange rate of the Bank of Canada is not available, convert the currency to Canadian dollars using the most recent daily exchange rate of the Bank of Canada available before the distribution date. For investment funds in continuous distribution, convert the currency to Canadian dollars using the average daily exchange rate of the Bank of Canada for the distribution period covered by the report.

If the distribution was not made in Canadian dollars, provide the foreign currency in Item 7(a) of the report.

10. Date of information in report

Unless otherwise indicated in this form, provide the information as of the distribution end date.

11. Date of formation

For the date of formation, provide the date on which the issuer was incorporated, continued or organized (formed). If the issuer resulted from an amalgamation, arrangement, merger or reorganization, provide the date of the most recent amalgamation, arrangement, merger or reorganization.

12. Security codes

Wherever this form requires disclosure of the type of security, use the following security codes:

Security code

Security type

BND

Bonds

CER

Certificates (including pass-through certificates, trust certificates)

CMS

Common shares

CVD

Convertible debentures

CVN

Convertible notes

CVP

Convertible preferred shares

DCT

Digital coins or tokens

DEB

Debentures

DRS

Depository receipts (such as American or Global depository receipts/shares)

FTS

Flow-through shares

FTU

Flow-through units

LPU

Limited partnership units and limited partnership interests (including capital commitments)

MTG

Mortgages (other than syndicated mortgages)

NOT

Notes (include all types of notes except convertible notes)

OPT

Options

PRS

Preferred shares

RTS

Rights

SMG

Syndicated mortgages

SUB

Subscription receipts

UBS

Units of bundled securities (such as a unit consisting of a common share and a warrant)

UNT

Units (exclude units of bundled securities, include trust units and mutual fund units)

WNT

Warrants (including special warrants)

OTH

Other securities not included above (if selected, provide details of security type in Item 7d)

13. Distributions by more than one issuer of a single security

If two or more issuers distributed a single security, provide the full legal names of the co-issuers in Item 3.

1. For the purposes of this form:

"designated foreign jurisdiction" means Australia, France, Germany, Hong Kong, Italy, Japan, Mexico, the Netherlands, New Zealand, Singapore, South Africa, Spain, Sweden, Switzerland or the United Kingdom of Great Britain and Northern Ireland;

"eligible foreign security" means a security offered primarily in a foreign jurisdiction as part of a distribution of securities in either of the following circumstances:

(a) the security is issued by an issuer

(i) that is incorporated, formed or created under the laws of a foreign jurisdiction,

(ii) that is not a reporting issuer in a jurisdiction of Canada,

(iii) that has its head office outside of Canada, and

(iv) that has a majority of the executive officers and a majority of the directors ordinarily resident outside of Canada;

(b) the security is issued or guaranteed by the government of a foreign jurisdiction;

"foreign public issuer" means an issuer where any of the following apply:

(a) the issuer has a class of securities registered under section 12 of the 1934 Act;

(b) the issuer is required to file reports under section 15(d) of the 1934 Act;

(c) the issuer is required to provide disclosure relating to the issuer and the trading in its securities to the public, to security holders of the issuer or to a regulatory authority and that disclosure is publicly available in a designated foreign jurisdiction;

"legal entity identifier" means a unique identification code assigned to the person

(a) in accordance with the standards set by the Global Legal Entity Identifier System, or

(b) that complies with the standards established by the Legal Entity Identifier Regulatory Oversight Committee for pre-legal entity identifiers;

"NRD" means National Registration Database;

"permitted client" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (in Québec, Regulation 31-103 respecting Registration Requirements, Exemptions and Ongoing Registrant Obligations);

"SEDAR+" has the same meaning as in National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+)(in Québec, Regulation 13-103 respecting System for Electronic Data Analysis and Retrieval + (SEDAR+));

"SEDAR+ profile" means a profile required under section 4 of National Instrument 13-103 System for Electronic Data Analysis and Retrieval + (SEDAR+) (in Québec, Regulation 13-103 respecting System for Electronic Data Analysis and Retrieval + (SEDAR+)).

2. For the purposes of this form, a person is connected with an issuer or an investment fund manager if either of the following applies:

(a) one of them is controlled by the other;

(b) each of them is controlled by the same person.

Filed in reliance on Coordinated Blanket Order 13-933

- - - - - - - - - - - - - - - - - - - -

The personal information required under this form is collected on behalf of and used by the securities regulatory authority or regulator under the authority granted in securities legislation for the purposes of the administration and enforcement of the securities legislation.

If you have any questions about the collection and use of this information, contact the securities regulatory authority or regulator in the local jurisdiction(s) where the report is filed, at the address(es) listed at the end of this form.

Schedules 1 and 2 may contain personal information of individuals and details of the distribution(s). The information in Schedules 1 and 2 will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

By signing this report, the issuer/underwriter confirms that each individual listed in Schedule 1 or 2 of the report who is resident in a jurisdiction of Canada:

a) has been notified by the issuer/underwriter of the delivery to the securities regulatory authority or regulator of the information pertaining to the individual as set out in Schedule 1 or 2, that this information is being collected by the securities regulatory authority or regulator under the authority granted in securities legislation, that this information is being collected for the purposes of the administration and enforcement of the securities legislation of the local jurisdiction, and of the title, business address and business telephone number of the public official in the local jurisdiction, as set out in this form, who can answer questions about the security regulatory authority's or regulator's indirect collection of the information, and

b) has authorized the indirect collection of the information by the securities regulatory authority or regulator.

- - - - - - - - - - - - - - - - - - - -

Schedule 1 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

Provide the following information for each purchaser that participated in the distribution. For each purchaser, create separate entries for each distribution date, security type and exemption relied on for the distribution.

b) Legal name of purchaser

If two or more individuals have purchased a security as joint purchasers, provide information for each purchaser under the columns for family name, first given name and secondary given names, if applicable, and separate the individuals' names with an ampersand. For example, if Jane Jones and Robert Smith are joint purchasers, indicate "Jones & Smith" in the family name column.

1. Family name

2. First given name

3. Secondary given names (if applicable)

4. Full legal name of non-individual (if applicable)

c) Contact information of purchaser

1. Residential street address

2. Municipality

3. Province/State

4. Postal code/Zip code

5. Country

6. Telephone number

7. Email address (if available)

d) Details of securities purchased

1. Date of distribution (YYYY-MM-DD)

2. Number of securities

3. Security code

4. Amount paid (Canadian $)

e) Details of exemption relied on

1. Rule, section and subsection number

2. If relying on section 2.3 [Accredited investor] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions), provide the paragraph number in the definition of "accredited investor" in section 1.1 of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) that applies to the purchaser. (select only one -- if the purchaser is a permitted client that is not an individual, "NIPC" can be selected instead of the paragraph number)

3. If relying on section 2.5 [Family, friends and business associates] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions), provide:

a. the paragraph number in subsection 2.5(1) that applies to the purchaser (select only one); and

b. if relying on paragraphs 2.5(1)(b) to (i), provide:

i. the name of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser. (Note: if Item 9(a) has been completed, the name of the director, executive officer or control person must be consistent with the name provided in Item 9 and Schedule 2.)

ii. the position of the director, executive officer, control person, or founder of the issuer or affiliate of the issuer claiming a relationship to the purchaser.

4. If relying on subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) and the purchaser is an eligible investor, provide the paragraph number in the definition of "eligible investor" in section 1.1 of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) that applies to the purchaser. (select only one)

f) Other information

Paragraphs f)1. and f)2. do not apply if any of the following apply:

(a) the issuer is a foreign public issuer;

(b) the issuer is a wholly owned subsidiary of a foreign public issuer;

(c) the issuer is distributing only eligible foreign securities and the distribution is to permitted clients only.

1. Is the purchaser a registrant? (Y/N)

2. Is the purchaser an insider of the issuer? (Y/N) (not applicable if the issuer is an investment fund)

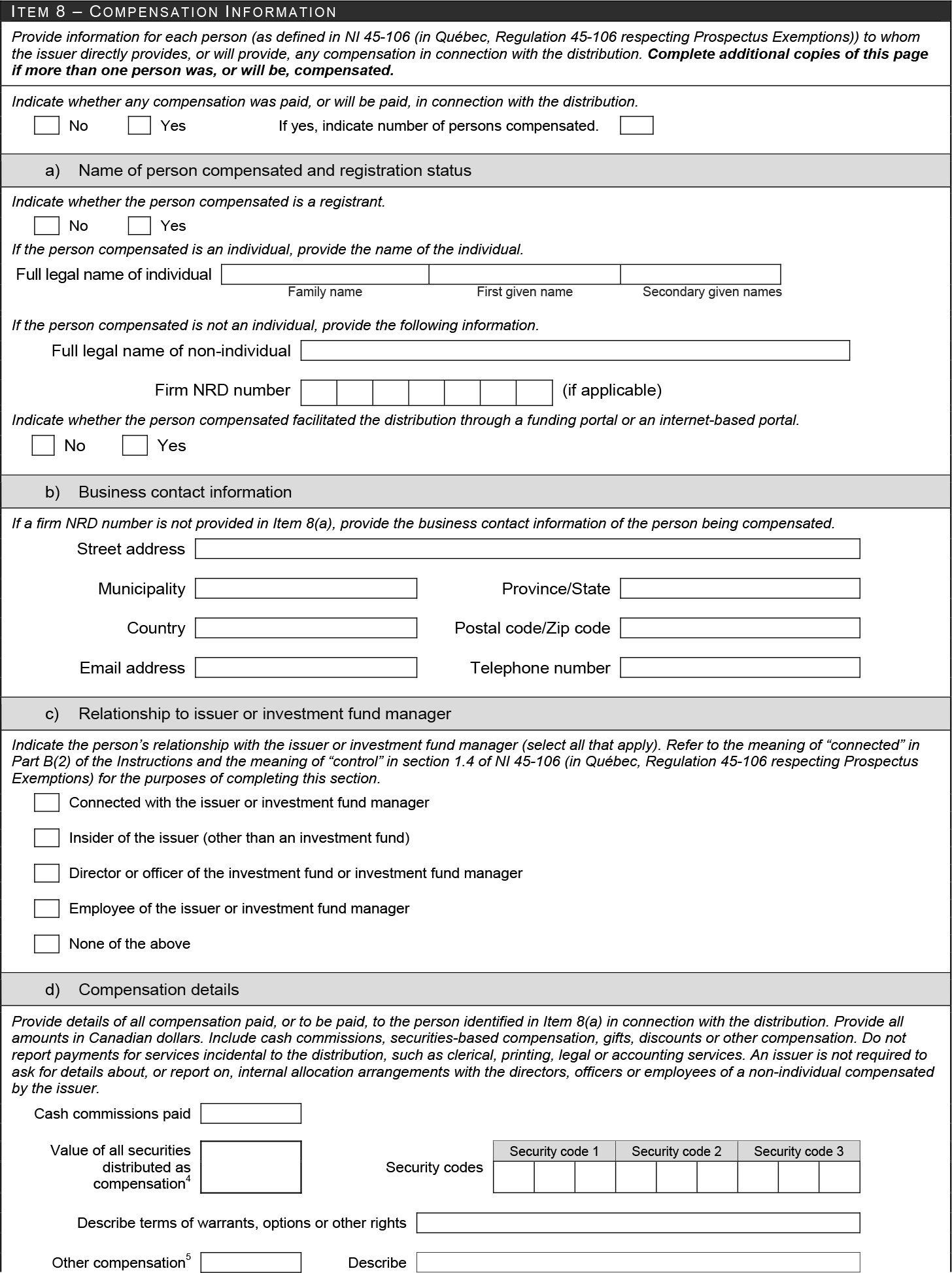

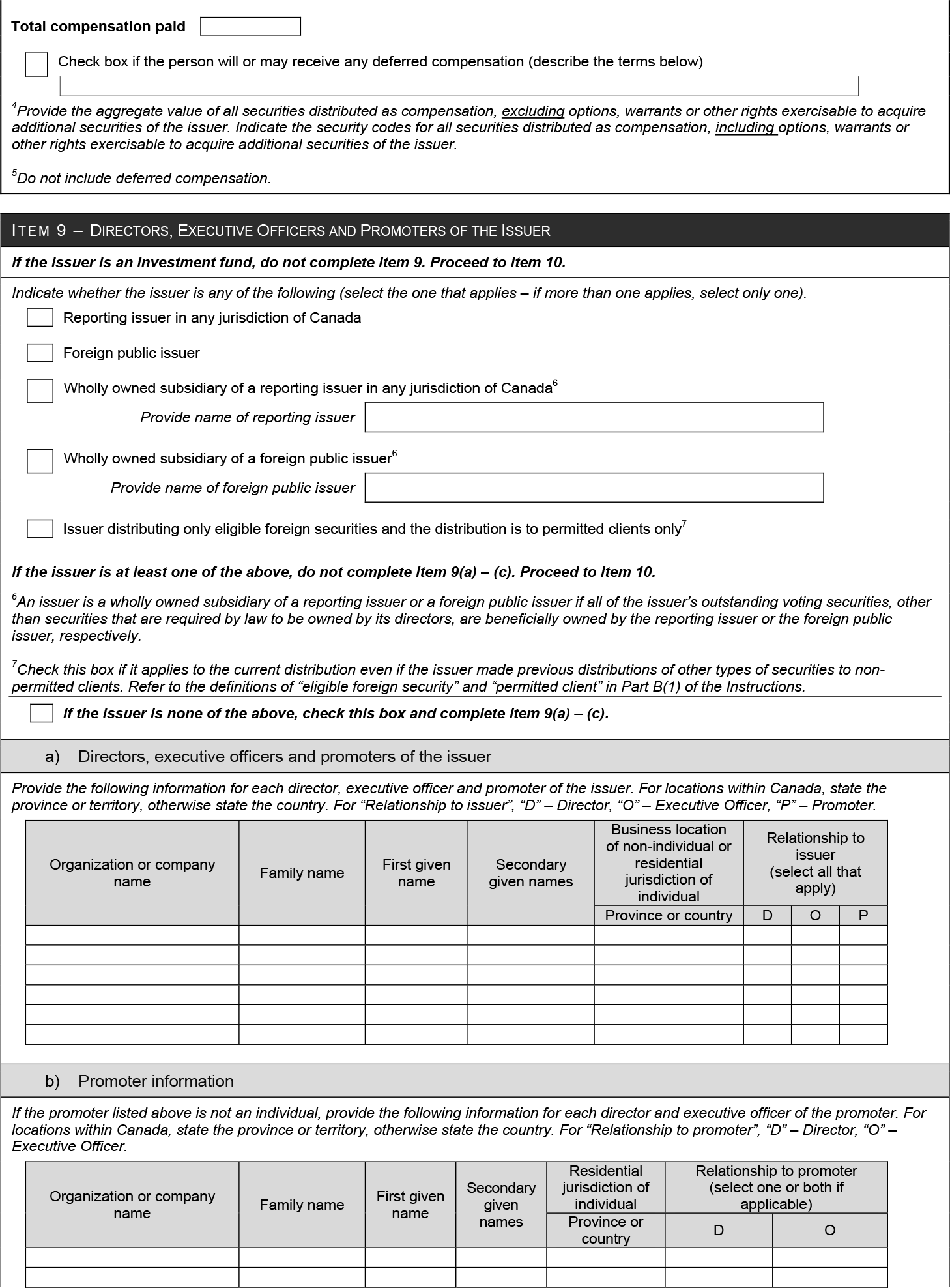

3. Full legal name of person compensated for distribution to purchaser. If a person compensated is a registered firm, provide the firm NRD number only. (Note: the names must be consistent with the names of the persons compensated as provided in Item 8.)

INSTRUCTIONS FOR SCHEDULE 1

Any securities issued as payment for commissions or finder's fees must be disclosed in Item 8 of the report, not in Schedule 1.

Details of exemption relied on -- When identifying the exemption the issuer relied on for the distribution to each purchaser, refer to the rule, statute or instrument in which the exemption is provided and identify the specific section and, if applicable, subsection or paragraph. For example, if the issuer is relying on an exemption in a National Instrument, refer to the number of the National Instrument, and the subsection or paragraph number of the specific provision. If the issuer is relying on an exemption in a local blanket order, refer to the blanket order by number.

For exemptions that require the purchaser to meet certain characteristics, such as the exemption in section 2.3 [Accredited investor], section 2.5 [Family, friends and business associates] or subsection 2.9(2) or, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec, or Saskatchewan, subsection 2.9(2.1) [Offering memorandum] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions), provide the specific paragraph in the definition of those terms that applies to each purchaser.

Reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions) -- For reports filed under paragraph 6.1(1)(j) [TSX Venture Exchange offering] of NI 45-106 (in Québec, Regulation 45-106 respecting Prospectus Exemptions), Schedule 1 must list the total number of purchasers by jurisdiction only, and is not required to include the name, residential address, telephone number or email address of the purchasers.

Schedule 2 must be filed in the format of an Excel spreadsheet in a form acceptable to the securities regulatory authority or regulator.

Complete the following only if Item 9(a) is required to be completed. This schedule also requires information to be provided about control persons of the issuer at the time of the distribution.

The information in this schedule will not be placed on the public file of any securities regulatory authority or regulator. However, freedom of information legislation may require the securities regulatory authority or regulator to make this information available if requested.

a) General information (provide only once)

1. Name of issuer

2. Certification date (YYYY-MM-DD)

b) Business contact information of Chief Executive Officer (if not provided in Item 10 or 11 of report)

1. Email address

2. Telephone number

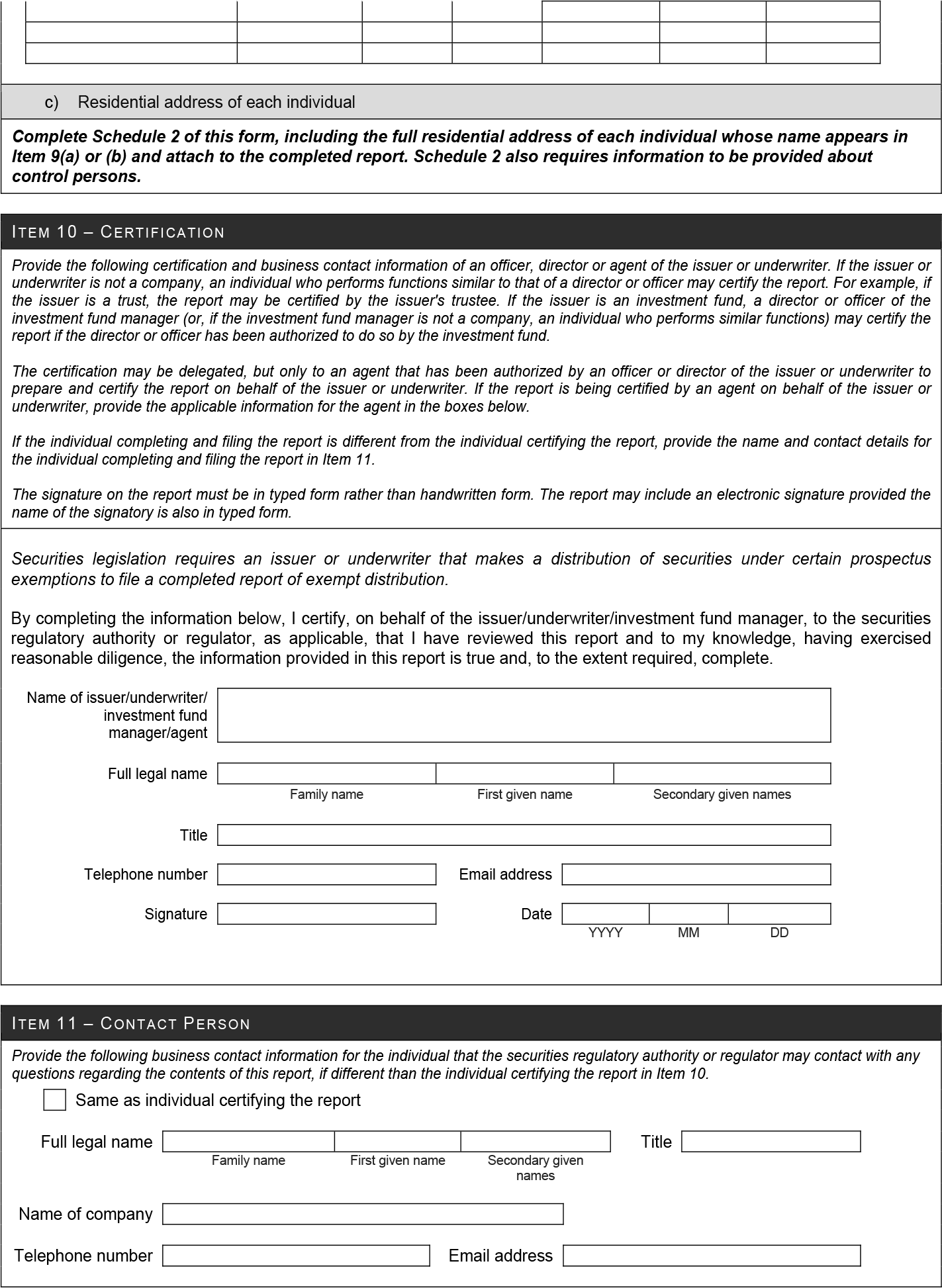

c) Residential address of directors, executive officers, promoters and control persons of the issuer

Provide the following information for each individual who is a director, executive officer, promoter or control person of the issuer at the time of the distribution. If the promoter or control person is not an individual, provide the following information for each director and executive officer of the promoter and control person. (Note: names of directors, executive officers and promoters must be consistent with the information in Item 9 of the report, if required to be provided.)

1. Family name

2. First given name

3. Secondary given names

4. Residential street address

5. Municipality

6. Province/State

7. Postal code/Zip code

8. Country

9. Indicate whether the individual is a control person, or a director and/or executive officer of a control person (if applicable)

d) Non-individual control persons (if applicable)

If the control person is not an individual, provide the following information. For locations within Canada, state the province or territory, otherwise state the country.

1. Organization or company name

2. Province or country of business location

Refer any questions to: