Ontario Securities Commission Bulletin

Issue 45/49 - December 08, 2022

Ont. Sec. Bull. Issue 45/49

• Mark Odorico -s. 2(2) of the TAR, Rule 22(4) of the CMT Rules of Procedure and Forms

• Ontario Securities Commission Staff Notice 51-734 Corporate Finance Branch 2022 Annual Report

• CSA Staff Notice 13-315 (Revised) Securities Regulatory Authority Closed Dates 2023

• CSA Staff Notice 25-306 Activist Short Selling Update

• Joint CSA and IIROC -- Staff Notice 23-329 Short Selling in Canada

• CME Amsterdam B.V. -- s. 144

• Evolve Funds Group Inc. and the Funds Listed in Schedule A

• GS Investment Strategies Canada Inc.

• Horizons ETFS Management (Canada) Inc. and the Funds Listed in Schedule A

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

Marketplaces

• CME Amsterdam B.V. -- Application for Variation of Exemption Order -- Notice of Commission Order

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

FOR IMMEDIATE RELEASE

December 1, 2022

TORONTO -- The Tribunal issued its Reasons for Decision in the above named matter.

A copy of the Reasons for Decision dated November 30, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

December 2, 2022

TORONTO -- The Tribunal issued an Order in the above named matter.

A copy of the Order dated December 2, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

December 2, 2022

TORONTO -- The Tribunal issued an Order in the above named matter.

A copy of the Order dated December 2, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

File No. 2022-9

Adjudicators: |

Timothy Moseley (chair of the panel) |

Sandra Blake |

|

Dale R. Ponder |

December 2, 2022

WHEREAS on November 28, 2022, the Capital Markets Tribunal held a hearing by videoconference;

ON HEARING the submissions of the representatives for Staff of the Ontario Securities Commission and for each of the receiver of Bridging Finance Inc., David Sharpe, Natasha Sharpe and Andrew Mushore, and on reading the written submissions delivered by those parties on November 30, 2022;

IT IS ORDERED, for reasons to follow, that:

1. the motions for disclosure brought by each of David Sharpe and Natasha Sharpe are scheduled to be heard by videoconference on January 30, 2023, at 10:00 a.m., or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat, and materials for the motions shall be delivered as follows:

a. Natasha Sharpe shall serve and file her motion record by 4:30 p.m. on December 2, 2022;

b. Staff of the Ontario Securities Commission shall serve and file its responding motion record, if any, by 4:30 p.m. on December 16, 2022;

c. David Sharpe and Natasha Sharpe shall each serve and file a reply record, if any, and written submissions by 4:30 p.m. on January 6, 2023;

d. Staff of the Ontario Securities Commission shall serve and file responding written submissions by 4:30 p.m. on January 18, 2023; and

e. David Sharpe and Natasha Sharpe shall each serve and file reply written submissions, if any, by 4:30 pm. on January 24, 2023;

2. the motions for a stay of this proceeding brought by each of David Sharpe and Natasha Sharpe are scheduled to be heard by videoconference on May 23, 2023, at 10:00 a.m., or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat; and

3. the merits hearing shall take place by videoconference and commence on June 26, 2023, at 10:00 a.m., and continue on June 27, 28 and 29, July 24, 25, 26, 27, 28 and 31, September 12, 13, 14, 26, 27, 28 and 29, October 2, 3, 4, 5, 23, 24, 25 and 26 and December 4, 5, 6, 7, 8, 11, 12, 13, 14 and 15, 2023, at 10:00 a.m. on each day, or on such other dates and times as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

File No. 2022-7

Adjudicators: |

Cathy Singer (chair of the panel) |

Dale Ponder |

December 2, 2022

WHEREAS on December 2, 2022, the Capital Markets Tribunal held a hearing by videoconference;

ON HEARING the submissions of the representatives for Staff of the Ontario Securities Commission (Staff) and for Mark Edward Valentine;

IT IS ORDERED THAT:

1. each party shall serve the other party with a hearing brief containing copies of the documents, and identifying the other things, that the party intends to produce or enter as evidence at the merits hearing, by 4:30 p.m. on August 11, 2023;

2. each party shall provide to the Registrar a completed copy of the E-hearing Checklist for Videoconference Hearings by 4:30 p.m. on August 18, 2023;

3. a further attendance in this matter is scheduled for August 23, 2023 at 10:00 a.m., by videoconference, or on such other date and time as may be agreed to by the parties and set by the Governance & Tribunal Secretariat;

4. if Staff elects to file affidavits for any of its witnesses, Staff shall serve on the respondent a final unsworn draft of any affidavit, by 4:30 p.m. on September 5, 2023, and shall serve and file a final sworn version of any affidavit by 10:00 a.m. on September 26, 2023;

5. each party shall provide to the Registrar the electronic documents that the party intends to rely on or enter into evidence at the merits hearing, along with an index file containing hyperlinks to the documents in the hearing brief, in accordance with the Protocol for E-hearings, by 4:30 p.m. on September 21, 2023; and

6. the merits hearing shall take place by videoconference and commence on September 26, 2023 at 10:00 a.m., and continue on September 28, 29 and October 2, 3, 4, 5, 10, 11, 12, 13, 17, 18, 19, and 20, 2023 at 10:00 a.m. on each day, or on such other dates and times as may be agreed to by the parties and set by the Governance & Tribunal Secretariat.

Mark Odorico -s. 2(2) of the TAR, Rule 22(4) of the CMT Rules of Procedure and Forms

Citation: Odorico (Re), 2022 ONCMT 36

Date: 2022-11-30

File No. 2022-18

Adjudicators: |

Andrea Burke (chair of the panel) |

|

|

||

Sandra Blake |

||

|

||

Dale Ponder |

||

|

||

Hearing: |

In writing; final written submissions received November 21, 2022 |

|

|

||

Appearances: |

Mark Odorico |

On their own behalf |

|

||

Kathryn Andrews |

For Staff of the Investment Industry Regulatory Organization of Canada |

|

Marie Abraham |

||

|

||

Erin Hoult |

For Staff of the Ontario Securities Commission |

|

[1] Mark Odorico (Odorico) requested a confidentiality order over certain documents contained in the Record of Original Proceeding (Record) filed within his application seeking hearing and review of two decisions of the Investment Industry Regulatory Organization of Canada (IIROC). We initially ordered that the entire Record would remain confidential pending further order of the Tribunal.

[2] Odorico, IIROC Staff and Staff of the Ontario Securities Commission (OSC) were able to reach agreement on the requested redactions, except for two redactions sought by Mr. Odorico which were opposed by IIROC Staff and OSC Staff.

[3] On November 22, 2022, we issued a confidentiality order over the agreed upon redactions to the Record and dismissed the two additional requests by Mr. Odorico. These are our reasons for that decision.

[4] Under Rule 22(4) of the Capital Market Tribunal Rules of Procedure and Forms and subsection 2(2) of the Tribunal Adjudicative Records Act, 2019,{1} a panel may order that an adjudicative record be kept confidential, if it determines that "intimate financial or personal matters or other matters contained in the record are of such a nature that the public interest or the interest of a person served by avoiding disclosure outweighs the desirability of adhering to the principle that the record be available to the public."{2}

[5] The redactions sought to the Record relate to intimate personal medical information regarding Odorico. The Tribunal has previously acknowledged that disclosure of medical information may infringe on privacy and avoiding the disclosure of those medical specifics which are not relevant to the proceeding outweighs the desirability that the medical information be made available to the public.{3}

[6] We accordingly ordered that the portions of the Record regarding Odorico's medical information, as agreed to by the parties, be marked as confidential and only redacted versions be available to the public. We find that the redactions requested appropriately balance the principles of transparency and privacy.

[7] Odorico made two additional requests for a confidentiality order, which were opposed by IIROC Staff and OSC Staff. Firstly, he requested that his doctor's name and contact information be redacted from Exhibit 9 of the Record as Mr. Odorico did not want the doctor "bothered by members of the public."

[8] We dismissed this request. The doctor's professional contact information is presumably publicly available and the fact that members of the public "may bother him", as submitted by Odorico, is not a relevant consideration in these circumstances. Furthermore, it is not "personal information" of the nature that should presumptively be redacted in accordance with section 3 of the Capital Markets Tribunal Practice Guideline.

[9] Secondly, he requested that a document contained at tab 74 of Exhibit 1 of the Record be fully redacted. The document is a letter of reprimand and warning from Odorico's former employer relating to events which were connected to the subject of the IIROC proceedings below. Odorico submits that because the letter is marked "Personal and Confidential" he feels that there is no need for it to be in the public record.

[10] We dismissed this request. Simply because a document is marked as "personal and confidential" does not mean it meets the standard required to depart from the principle that Tribunal hearings and the documents submitted must be open to public. The letter contains information which relates to this proceeding and which is also contained in the IIROC merits decision below. Odorico has not persuaded us that this letter meets the test for a confidentiality order.

[11] For the reasons set out above, we ordered that only the redacted version of the Record be available to the public and that Odorico's additional requests for confidentiality be dismissed.

Dated at Toronto this 30th day of November, 2022

{1} SO 2019, c 7, Sch 60

{2} Kitmitto (Re), 2022 ONCMT 12 (Kitmitto) at para 80

{3} Kitmitto at para 81

Ontario Securities Commission Staff Notice 51-734 -- Corporate Finance Branch 2022 Annual Report

Ontario Securities Commission Staff Notice 51-734 Corporate Finance Branch 2022 Annual Report is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

December 1, 2022

I am proud to share our annual Report, which provides an overview of the Branch's operational and policy work and guidance about our expectations and our interpretation of regulatory requirements in certain areas.

This year has brought new challenges to Ontario and capital markets worldwide, including geopolitical tensions, surging inflation, volatile crypto asset prices and continuing supply chain issues. These challenges and the resulting capital market uncertainty reinforce the need for balanced, tailored, flexible and responsive regulation to carry out the OSC's mandate to protect investors, to foster fair, efficient and competitive capital markets and confidence in capital markets, to foster capital formation and to contribute to the stability of the financial system and the reduction of systemic risk.

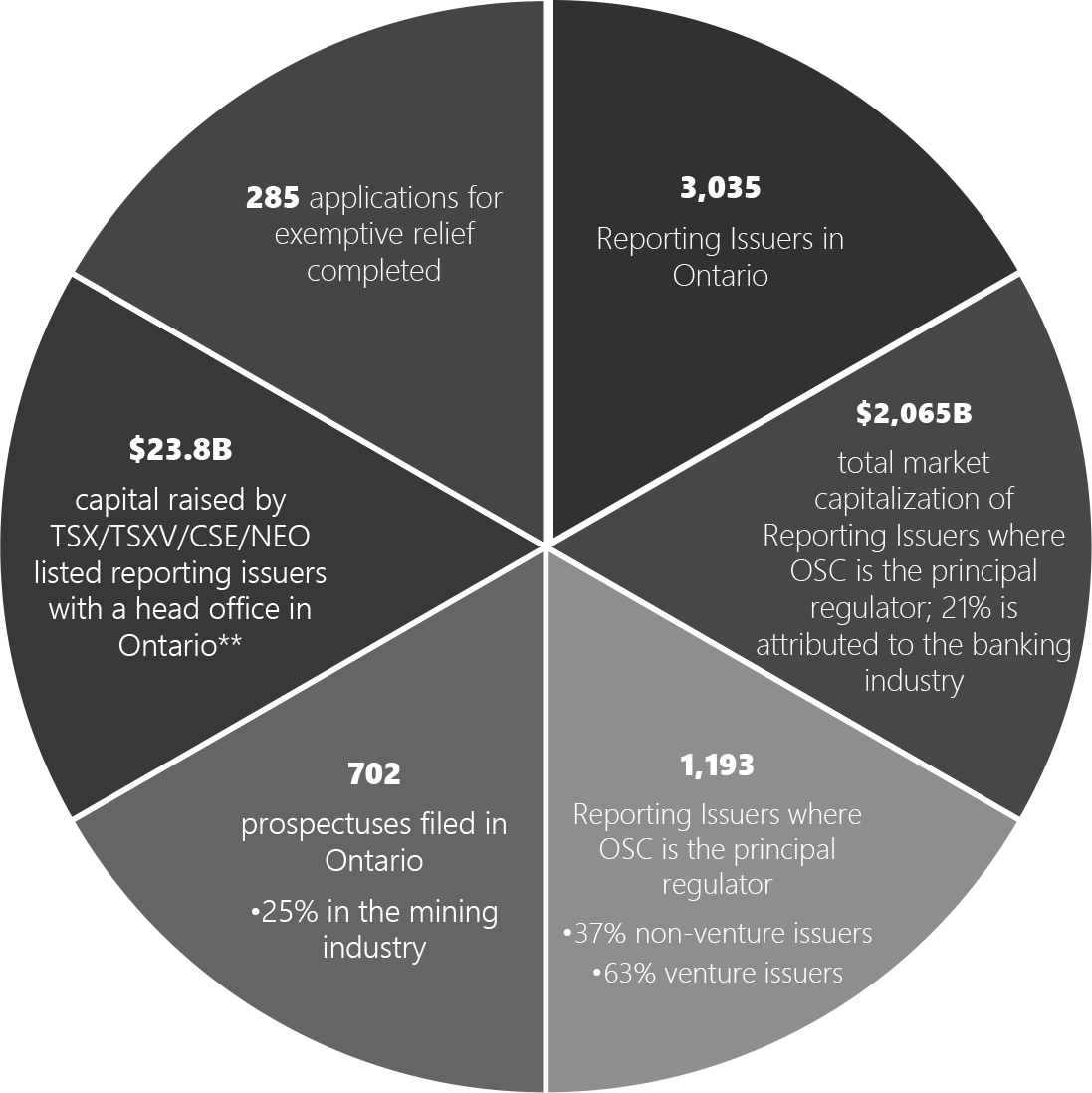

Capital raising in Ontario continued at a fast pace during Fiscal 2022, leading to a record number of prospectus filings; over 700 prospectuses were filed in Ontario.

Throughout Fiscal 2022, the Branch, with its CSA partners, continued to advance its policy work, including projects related to climate-related disclosure and diversity on board and in executive officer positions.

At the same time, the Branch, with its CSA partners, continued work on initiatives designed to reduce regulatory burden. On January 4, 2022, Ontario Instrument 44-501 Exemption from Certain Prospectus Requirements for Well-known Seasoned Issuers (Interim Class Order) came into effect, providing novel temporary exemptions from certain base shelf prospectus requirements for qualifying well-known seasoned issuers. On April 7, 2022, the CSA published proposed amendments to implement an access equals delivery model for prospectuses generally, annual financial statements, interim financial reports and related MD&A for non-investment fund Reporting Issuers.

These initiatives will continue to be part of the Branch's main policy focus in fiscal 2023. The Branch will continue to monitor and consider new market trends and potential areas of concern that may warrant a regulatory response.

This Report is an important tool for engaging with our stakeholders. We hope that this Report will serve as a guide to better understand disclosure and other regulatory obligations under Securities Law. We welcome any questions or feedback that you may have.

Kind regards,

Table of Contents

Glossary |

6 |

Fiscal 2022 Snapshot |

8 |

Introduction |

9 |

Ontario Securities Commission |

9 |

Corporate Finance Branch: Who We Are & What We D• |

10 |

Part A: Compliance |

12 |

1. Continuous Disclosure Review (CDR) Program |

13 |

A) Overview |

14 |

I) Objectives of the CDR program |

14 |

II) Types of CD reviews |

15 |

III) Tips for Reporting Issuers that are selected for a CD review |

16 |

B) CDR program outcomes for Fiscal 2022 |

16 |

C) Trends and guidance |

19 |

I) Management's discussion & analysis |

19 |

II) Non-GAAP and other financial measures |

24 |

III) Overly promotional press releases |

25 |

IV) Material contracts |

27 |

V) Diversity on boards and in executive officer positions |

29 |

VI) Related-party transactions/cross financial interests |

29 |

VII) Disclosure considerations pertaining to the war in Ukraine (the Conflict) |

30 |

VIII) Syndicated mortgages |

31 |

IX) Filing reports of exempt distribution |

32 |

X) Crypto asset industry |

32 |

2. Public Offerings |

36 |

A) Trends and guidance |

36 |

I) Primary business requirements in an IP• |

37 |

II) Description of business |

38 |

III) Prospectus filings by investment issuers |

39 |

IV) Base shelf prospectus -- sufficiency of proceeds and financial condition |

39 |

V) Prospectus lapse date |

40 |

VI) Comfort letter requirements |

41 |

VII) President's lists |

41 |

VIII) Flow-through units |

42 |

IX) Cessation of Canadian dollar offered rate |

42 |

X) Underwriting conflicts disclosure requirements |

43 |

XI) Confidential prospectus pre-file review |

43 |

XII) Actuarial consents |

46 |

3. Exemptive Relief Applications |

47 |

A) Trends and guidance |

47 |

I) Management cease trade orders (MCTO) |

48 |

4. Insider Reporting |

48 |

5. Our Service Commitments |

50 |

6. Administrative Matters |

51 |

A) Participation fee form |

51 |

B) Well-known seasoned issuers |

52 |

C) Common preliminary prospectus filing deficiencies |

54 |

D) Prospectus filings -- timing |

56 |

Part B: Responsive Regulation |

57 |

1. Access Equals Delivery |

58 |

2. Continuous Disclosure Requirements |

58 |

3. Listed Issuer Financing Exemption |

59 |

4. Environmental, Social and Corporate Governance |

59 |

5. Benchmarks |

60 |

6. Designated Rating Organizations |

60 |

7. NI 43-101 Consultation Paper |

62 |

Part C: Resources |

64 |

1. Prior Year Corporate Finance Branch Reports |

65 |

2. Key Staff Notices |

65 |

3. Staff Contact Information |

69 |

The following terms are used widely throughout the Report and have the meanings set forth below unless otherwise indicated. Words importing the singular number include the plural, and vice versa.

Act: means the Securities Act, R.S.O. 1990, chapter s.5.

AIF: means an annual information form as such term is defined in Form 51-102F2 Annual Information Form.

AMF: means the Autorité des marchés financiers.

Branch: means the Corporate Finance branch at the OSC.

CD: means the continuous disclosure obligations of a reporting issuer as set out in NI 51-102.

CDR program: means the harmonized program established in 2004 by the CSA for continuous disclosure reviews.

COVID-19: means the global pandemic of coronavirus disease declared on March 11, 2020.

CPC: means a capital pool company as such term is defined in TSXV Policy 2.4 Capital Pool Companies.

CSA: means the Canadian Securities Administrators.

CSE: means the Canadian Securities Exchange.

ESG: means environmental, social and governance.

Fiscal 2021: means the fiscal year ended March 30, 2021.

Fiscal 2022: means the fiscal year ended March 31, 2022.

Form 51-102F1: means Form 51-102F1 Management's Discussion & Analysis.

FLI: means forward-looking information as such term is defined in NI 51-102.

IOR: means an issue-oriented review conducted by the Branch.

IOSCO: means the International Organization of Securities Commissions.

IPO: means an initial public offering as such term is defined in the Act.

Issuer: means an issuer as such term is defined in the Act.

MD&A: means management's discussion and analysis as such term is defined in Form 51-102F1.

NEO: means the Neo Exchange Inc.

NI 31-103: means National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

NI 41-101: means National Instrument 41-101 General Prospectus Requirements.

NI 43-101: means National Instrument 43-101 Standards of Disclosure for Mineral Projects.

NI 44-101: means National Instrument 44-101 Alternative Forms of Prospectus.

NI 44-102: means National Instrument 44-102 Shelf Distributions.

NI 45-106: means National Instrument 45-106 Prospectus Exemptions.

NI 51-102: means National Instrument 51-102 Continuous Disclosure Obligations.

NI 52-112: means National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure.

NP 11-202: means National Policy 11-202 Process for Prospectus Reviews in Multiple Jurisdictions.

NGFM: Non-GAAP Financial Measures as such term is defined in NI 52-112.

OSC: means the Ontario Securities Commission.

PIF: means a personal information form as such term is defined in NI 41-101.

R&D: means research and development.

Report: means this 2022 annual report, published by the Branch.

Reporting Issuer: means a reporting issuer as defined in the Act.

Securities Law: means Ontario securities law as defined in the Act.

SEDAR: means the system for electronic document analysis as such term is defined in National Instrument 13-101 System for Electronic Document Analysis and Retrieval of the Act.

SEDI: means the system for electronic disclosure by insiders as such term is defined in National Instrument 55-102 System for Electronic Disclosure by Insiders (SEDI).

Staff: means staff at the Branch.

TSX: means the Toronto Stock Exchange.

TSXV: means the TSX Venture Exchange.

Venture Issuer: means a venture issuer as defined in NI 51-102.

* Note: all figures are as at / for Fiscal 2022 and are approximate or rounded.

** Includes public offerings and private placements of equity and convertible debentures.

This Report provides an overview of the Branch's operational and policy work during Fiscal 2022, including a summary of key findings and outcomes from our regulatory oversight program (Part A), and the nature, purpose and status of ongoing issuer-related policy initiatives (Part B). The Report is intended for entities and individuals we regulate, their advisors, as well as investors.

In publishing this Report we aim to

• REINFORCE the importance of compliance with regulatory obligations,

• PROVIDE GUIDANCE to improve disclosure in regulatory filings,

• HIGHLIGHT trends in the capital markets, and

• INFORM AND UPDATE stakeholders on new and ongoing policy initiatives.

The OSC continues to implement the Ontario government's five-point capital markets plan focused on strengthening investment in Ontario, promoting competition and facilitating innovation.{1}

• OSC VISION: to be an effective and responsive securities regulator -- fostering a culture of integrity and compliance and instilling investor confidence in the capital markets.

• OSC MANDATE: to provide protection to investors from unfair, improper or fraudulent practices; to foster fair, efficient and competitive capital markets and confidence in the capital markets; to foster capital formation; and to contribute to the stability of the financial system and the reduction of systemic risk.

• OSC VALUES:

Professional, People, and Ethical:

• protecting the public interest is our purpose and our passion;

• we value dialogue with the marketplace;

• we are professional, fair-minded and act without bias.

Each year, the OSC publishes a statement of priorities that sets out the OSC's strategic goals, priorities, and specific initiatives for the year. Our priorities are aligned with our statutory mandate and the annual mandate letter from the Minister of Finance.

Our 2022-2023 OSC Goals are

• GOAL 1 promote confidence in Ontario's capital markets,

• GOAL 2 reduce regulatory burden,

• GOAL 3 facilitate financial innovation, and

• GOAL 4 strengthen our organizational foundation.

In support of the OSC's mandate, the Branch regulates approximately 1,200 Reporting Issuers in Ontario that are not investment funds. The Branch assesses whether Reporting Issuers in Ontario provide the required level of disclosure of material information to investors so they can make informed investment decisions. Through this oversight role, the Branch supports the OSC's goal to improve transparency, trustworthiness, and efficiency in Ontario's capital markets.

To do this, our operational work includes:

• review of public offerings of securities;

• review of capital raising activities in the exempt market;

• review of CD filed by Reporting Issuers;

• review and consideration of applications for exemptive relief from regulatory requirements;

• review of insider reporting;

• review of credit rating agencies that are designated rating organizations;

• oversight of designated benchmarks and benchmark administrators;

• oversight of the listed Issuer function for OSC recognized exchanges;

• engagement with stakeholders through a number of activities, including external advisory committees;

• provision of guidance to stakeholders through staff notices that communicate expectations and interpretations of regulatory requirements in certain areas;

• delivery of Issuer education and outreach programs.

We regularly consult and partner with other branches across the OSC in executing our operational work. For example, we partner with the Market Regulation branch for oversight of recognized exchanges, the Compliance and Registrant Regulation branch for oversight of the exempt market and the Enforcement branch on matters of non-compliance with Securities Law requirements.

In addition, we also engage in policymaking to update, enhance and streamline securities regulation in alignment with the OSC's mandate.

1. Continuous Disclosure Review Program

2. Public Offerings

3. Exemptive Relief Applications

4. Insider Reporting

5. Our Service Commitments

6. Administrative Matters

This section of the Report provides an overview of the key findings and outcomes from our Fiscal 2022 CDR program. We discuss key or novel issues, suggest best practices, and specify applicable legislation and relevant guidance to assist Issuers in addressing each of the topic areas.

Under Canadian Securities Law, a Reporting Issuer must provide timely and periodic CD about its business and affairs.

CD includes periodic filings such as:

• interim and annual financial statements;

• MD&As;

• certificates of annual and interim filings;

• management information circulars;

• AIFs;

• technical reports.

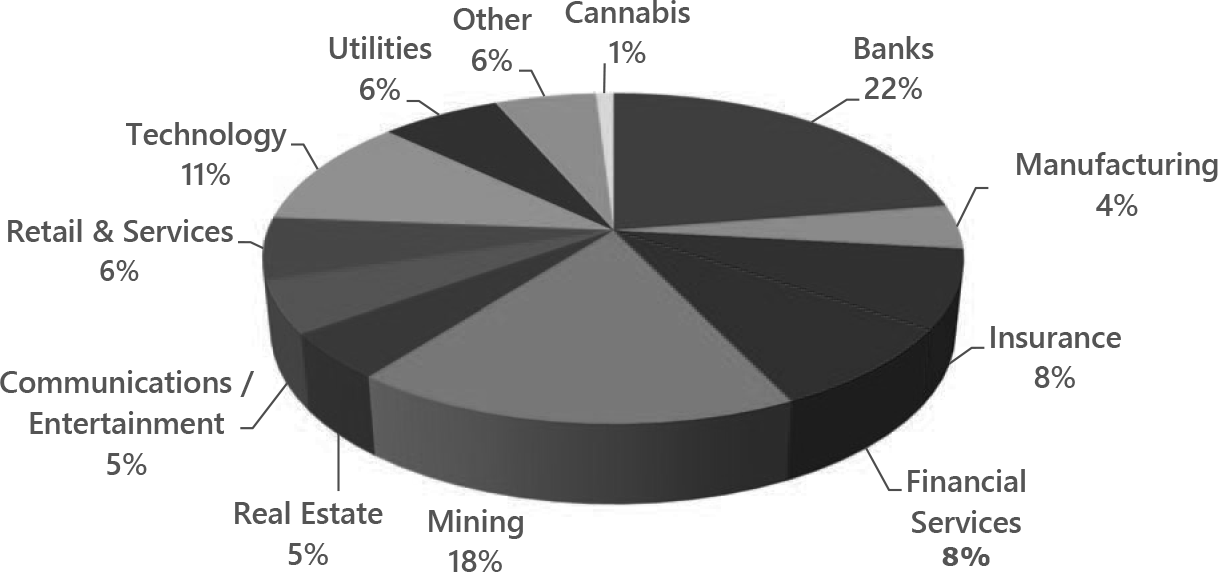

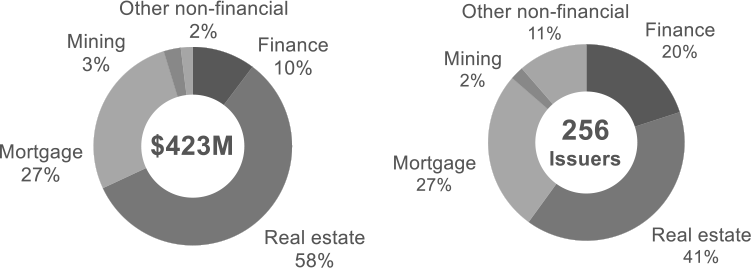

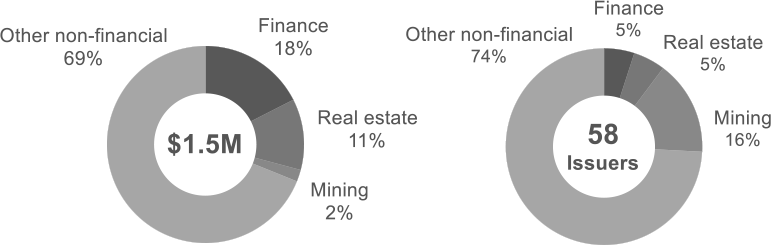

The Branch has primary responsibility as principal regulator{2} over approximately 1,200 Reporting Issuers with an aggregate market capitalization of approximately $2,065 billion as at March 31, 2022. The three largest industries by market capitalization were banking, mining, and technology.

Market capitalization of Ontario Reporting Issuers by industry as at March 31, 2022

A) Overview

Our CDR program is risk-based and outcome focused. It includes planned reviews based on risk criteria as well as ongoing monitoring through news releases, media articles, complaints, and other sources. The CDR program is conducted pursuant to the powers in subsection 20(1) of the Act and is part of a harmonized CD review program conducted by the CSA.{3}

I) Objectives of the CDR program

Compliance |

to assess whether Reporting Issuers are complying with disclosure obligations and to identify material disclosure deficiencies that affect the reliability and accuracy of an Issuer's disclosure record. |

Issuer Education and Outreach |

to help Reporting Issuers better understand disclosure obligations. |

The goal of the CDR program is to improve the completeness, quality and timeliness of CD provided by Reporting Issuers. This program assesses compliance with CD requirements through a review of a Reporting Issuer's filed documents, its website and social media. This review function is critical to facilitating fair and efficient markets, investor protection, and informed investment decision making and trading. Disclosure about a Reporting Issuer and its business is important not only when a Reporting Issuer first enters the market, but also on an ongoing basis; for example, many Reporting Issuers raise funds through short form prospectuses which incorporate CD documents by reference.

II) Types of CD reviews

In general, we conduct either a full review or an IOR of a Reporting Issuer's CD.

Full review |

broad in scope and generally covering a Reporting Issuer's CD record for a period of 12-15 months. |

IOR |

an in-depth review focusing on a specific accounting, legal or regulatory issue that we believe warrants regulatory scrutiny. |

In planning full reviews, we draw on our knowledge of Reporting Issuers and the industries in which they operate and use risk-based criteria to identify Reporting Issuers with a higher risk of deficient disclosure. The criteria are designed to identify Reporting Issuers whose disclosure is likely to be materially improved or brought into compliance with Securities Law or accounting standards as a result of our intervention. Our risk-based assessment incorporates both qualitative and quantitative factors that we review regularly to keep current with our evolving capital markets.{4} We also monitor new or novel and high growth areas of financing activity when developing our review program and consider any complaints received regarding the Reporting Issuer.

IORs are generally focused on a specific accounting, legal or regulatory issue, an emerging issue or industry or to assess compliance with a new or amended rule that recently came into force.

Conducting CD reviews helps us to

• monitor compliance with CD requirements by Reporting Issuers,

• communicate Staff interpretations and expectations on specific requirements, and identify areas of concern,

• address specific areas where there is heightened risk of investor harm,

• identify common deficiencies,

• provide industry-specific or topic-specific disclosure guidance that may assist preparers in complying with regulatory requirements, and

• assess compliance with new accounting standards and new or amended rules.

III) Tips for Reporting Issuers that are selected for a CD review

Below are tips on what to do if you receive a comment letter from Staff in connection with a CD review:

• read the first paragraph of the letter which will state whether we are conducting a full review or an IOR;

• consider whether you need to seek advice from legal, accounting, and/or other advisors. If so, engage them early in the process;

• reach out to Staff if you require clarification about any of the comments. Note that Staff cannot provide legal or accounting advice;

• provide a thorough response, referencing Securities Law or IFRS{5}, where relevant;

• continue to file required CD documents during the review. An ongoing review does not alleviate or alter a Reporting Issuer's ongoing CD obligations;

• note the response deadline and plan accordingly. Reach out to Staff well in advance of the deadline, should you require additional time to provide a response letter. In appropriate circumstances, Staff may grant an extension request.

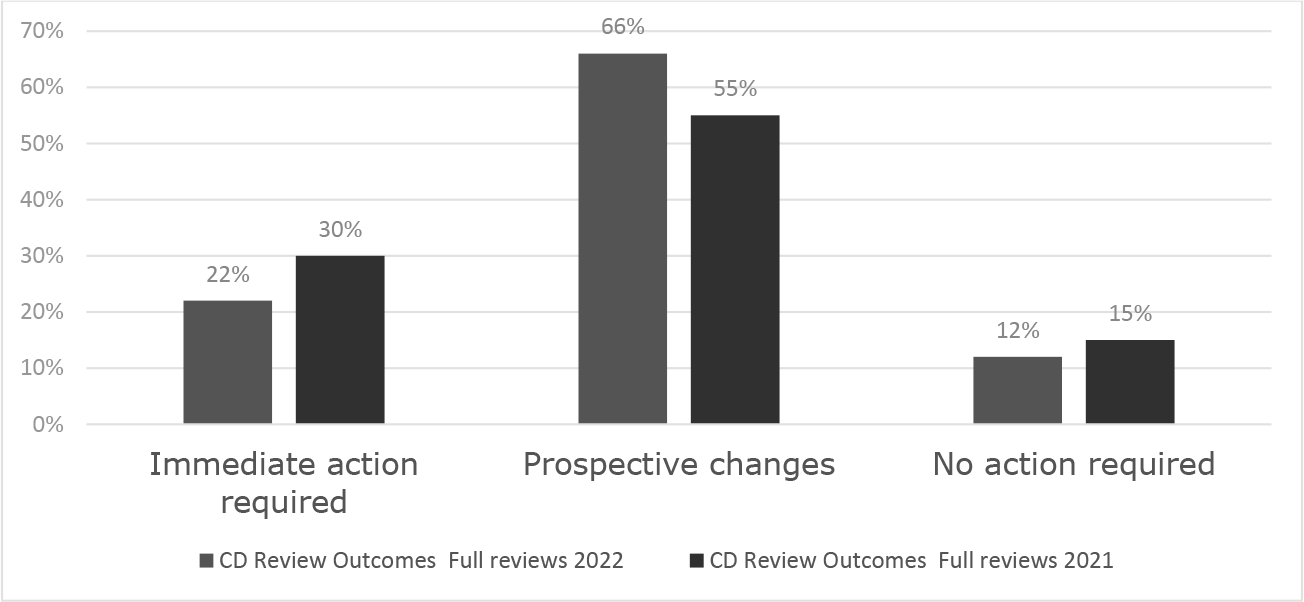

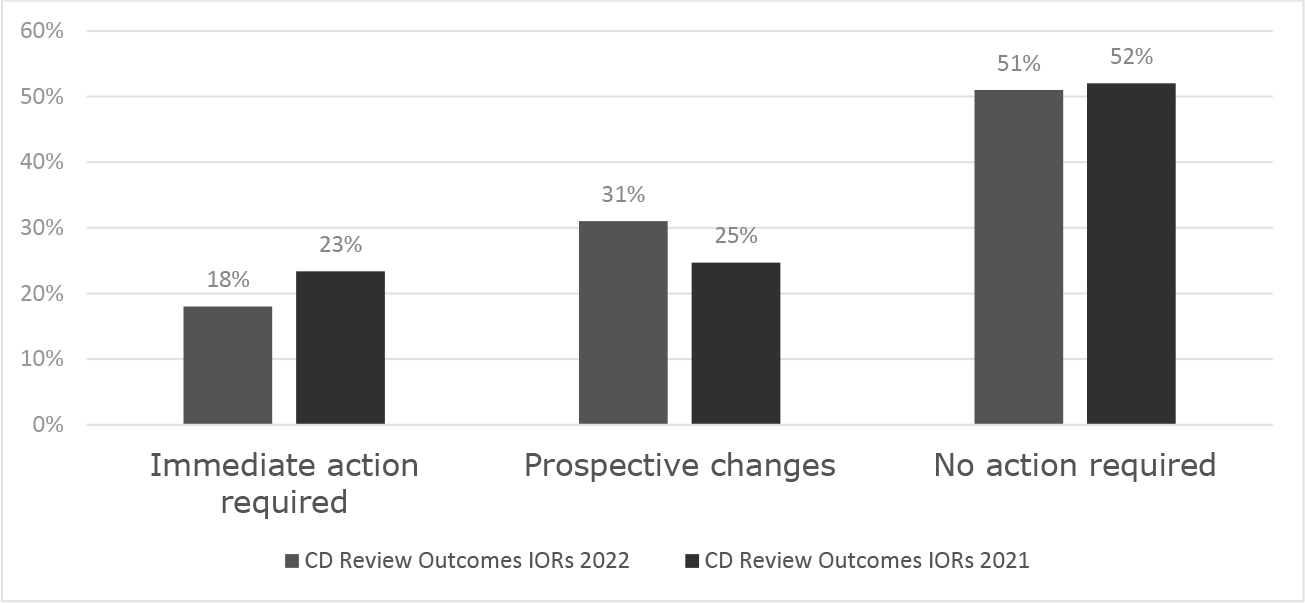

B) CDR program outcomes for Fiscal 2022

We track three categories of outcomes of the CD program: no action is required, prospective continuous disclosure enhancements are required, or immediate corrective action is required for deficiencies. Immediate corrective action includes the refiling of a previously filed CD document, a referral to the Enforcement branch or the issuance of a cease trade order. A CD review may result in more than one outcome. For example, a Reporting Issuer may be required to refile certain CD documents while also committing to prospective disclosure enhancements. Tracking these outcomes assists us in planning the CDR program in subsequent years, including the re-evaluation of existing risk-based factors.

Given our risk-based criteria to identify Reporting Issuers for review, the outcomes on a year-over-year basis should not necessarily be interpreted as trends since the issues and Reporting Issuers reviewed each year are generally different. Reviews may be issue-specific, focusing on a particular CD requirement for which we have noted widespread deficiencies. These reviews may result in an increased number of outcomes categorized as "prospective changes" or "immediate action required" if deficiencies identified are prevalent among several Reporting Issuers.

The following is the summary of the CD review outcomes for Fiscal 2022 and Fiscal 2021.

Outcomes of full CD reviews

Outcomes of IORs

The most common types of immediate action required from Reporting Issuers were the following:

• refiling of financial statements to correct material misstatements;

• refiling of an MD&A where the MD&A was materially deficient and did not meet the form requirements of Form 51-102F1;

• filing of a clarifying news release when a Reporting Issuer failed to include sufficient disclosure of material assumptions, milestones and risk factors pertaining to FLI or failed to update the market on FLI;

• refiling or filing (in instances when documents were not filed in the first place) of material contracts;

• refiling of a technical report where the report filed was not in compliance with NI 43-101.

Reporting Issuers that refile CD documents during a Staff review are placed on the Refilings and Errors List found on the OSC Website.

C) Trends and guidance

This section highlights some of the common deficiencies that were observed during our CD reviews in Fiscal 2022, and includes some best practices and guidance to assist Reporting Issuers and their advisors in meeting their regulatory obligations. We encourage Reporting Issuers to continue to review and improve the quality of their CD, including with reference to the guidance below.

I) Management's discussion & analysis

The MD&A is the cornerstone of an Issuer's overall financial disclosure and is intended to provide an analytical and balanced discussion of the Issuer's results of operations and financial condition through the eyes of management. MD&A disclosure should be specific, useful, and understandable. The MD&A requirements are set out in Part 5 of Form 51-102F1.

Over the past year, the world has been impacted by a number of major, ongoing events including COVID-19, geopolitical tensions (notably the war in Ukraine), rising interest rates, inflationary pressures and supply chain disruptions. These events have generally had a material adverse impact on the economy and continue to pose challenges for many Issuers. It is critical that Issuers provide meaningful disclosure about the impact of these events on their business. An Issuer should consider its specific business and operations, and provide clear, transparent and balanced disclosure of the business impacts and potential uncertainties regarding these events in its MD&A. Such information is necessary to meet Securities Law requirements and for investors to make informed investment decisions. It is important that each Issuer tailors its disclosure to provide investors with insight into the specific and material operational challenges, financial impacts and risks it faces, and its related responses. Issuers should also keep in mind that the financial statements may also need to reflect and disclose the impacts of these events.

Staff have discussed certain MD&A deficiencies below but refer Issuers to previous Branch reports (links in Part C) that discuss other MD&A matters that remain relevant.

Discussion of operations -- development stage issuers and significant projects without revenue

Issuers are required to discuss significant projects that have not yet generated significant revenue in their MD&A (Item 1.4(d) of Form 51-102F1). Staff frequently raised comments in respect of this requirement over the past year, both in the context of CD and prospectus reviews. We continue to see Issuers that do not provide sufficient information to enable the reader to understand the project, including timing and costs associated with the project. While this issue is most often observed with early-stage/development-stage Issuers or those with a change in business, this requirement applies to allIssuers that have significant projects that have not yet generated significant revenue. Over the past year, this has been particularly prevalent for technology-based and manufacturing Issuers conducting R&D and those developing new products or technologies. Issuers will often disclose the total expense incurred during the period in the variance analysis but will fail to provide sufficient disaggregation of the material components of the costs, how those costs impact timing and the remaining costs to take the project to the next stage. In addition, the disclosure often does not include sufficient detail to understand the Issuer's plan for the project, including significant milestones.

- - - - - - - - - - - - - - - - - - - -

Tip: Issuers should describe each significant project in sufficient detail, including, but not limited to, the following information:

• the Issuer's overall plan for the project and the status of the project relative to that plan. The discussion should include short and long-term plans. For R&D activity, this discussion should be included for each stage;

• the expected timeline of the project, including the Issuer's progress compared to the timeline;

• the key concrete milestones in the plan and what specific events need to occur to meet each milestone;

• the expenditures made to date for each project/stage/milestone, and how these expenditures relate to anticipated timing and costs to take the project to the next stage of the project plan;

• the license(s) and regulatory approval(s) that the Issuer must obtain. The discussion should include the anticipated timeline and expenditures associated with obtaining the license/regulatory approval and the risks and associated impact if regulatory approval and licenses are not obtained;

• the status of the project, including any delays in the disclosed timeline and/or anticipated cost overruns. In addition, if the Issuer previously disclosed material FLI, the MD&A must include a discussion of events and circumstances that occurred during the period that are reasonably likely to cause actual results to differ materially from the FLI and the expected differences.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Reminder: Venture Issuers without significant revenue from operations must provide a breakdown of material costs incurred, including, but not limited to, the following:

• exploration and evaluation assets or expenditures;

• expensed research and development costs;

• intangible assets arising from development;

• general and administration expenses.

If the Venture Issuer's business primarily involves mining exploration and development, the analysis of exploration and evaluation assets or expenditures must be presented on a property-by-property basis.

See item 5.3 of NI 51-102.

- - - - - - - - - - - - - - - - - - - -

Non-Venture Issuers must also include disclosure in their AIF about R&D. Item 5.1(1)(a)(iv) of Form 51-102F2 Annual Information Form requires Issuers with R&D to describe

• the stage of development of the products and services and, if the products are not at the commercial production stage, the timing and stage of R&D programs,

• whether the Issuer is conducting its own R&D, subcontracting out the R&D or using a combination of those methods, and

• the additional steps required to reach commercial production and an estimate of costs and timing.

Discussion of operations -- variance analysis

In discussing period-over-period financial statement variances, Issuers reviewed continued to provide limited narrative discussion of the factors resulting in the variances and any trends or potential trends.

Simply stating the percentage change or amount, which is information that is readily available from the financial statements, is not sufficient and does not provide investors with insight into the Issuer's operations, or how the economic environment and trends, events and uncertainties impact its business. It is important to be specific and to disclose information that readers need to make informed investment decisions.

When discussing variances in financial statement line items, Issuers should

• quantify changes and clearly explain the factors, drivers and reasons contributing to the period-over-period variances that affect revenues and expenses. For example, in discussing revenues, discuss variables such as price, volume or quantity of goods or services being sold, introduction of new products or services (or discontinuation) or other significant factors by segment. In discussing expenses, quantify the material components of the expense and provide a detailed explanation of each variance, and

• provide insight into the Issuer's past and future performance.

When discussing the changes in financial condition and results, it is also important to include an analysis of the effect on continuing operations of any acquisition, disposition, write-off, abandonment or other similar event.

Forward-looking information (FLI)

FLI is an area of interest to many investors and can provide valuable insight about a Reporting Issuer's business and how it intends to attain its corporate objectives and targets. It is important that investors receive transparent and clear disclosure that is specific, understandable, and relevant. The FLI, together with the accompanying disclosures, should be presented in an easy-to-read manner by, for example, providing the required disclosures near the FLI statement and presenting the information in tabular form that clearly links the particular FLI to the associated factors, assumptions and material risks. These disclosures will enable investors to interpret the FLI and simplify monitoring of progress in subsequent reporting periods.

FLI continued to be an area of challenge for Reporting Issuers over the past year, whether in the context of a prospectus or CD. We continue to see deficiencies, including a lack of balanced discussion of key factors and assumptions used and the material risk factors that could cause actual results to differ materially from the FLI. We have highlighted a few of the more common deficiencies below.

Updating and withdrawing FLI

We continue to see Reporting Issuers that do not provide updates to previously disclosed FLI or do not explain the reasons why they have withdrawn FLI.

Reporting Issuers that have previously disclosed FLI have an obligation to update the FLI in CD documents. Simply providing an update to the figures, without disclosing the underlying factors and assumptions that drive the change, does not provide insight on why the FLI is being updated. Reporting Issuers must provide a comparison of actual results to the previously disclosed FLI. The comparison of actual results to previously disclosed FLI is important for investors in making investment decisions, in their assessment of management and of the current and future business performance of the Reporting Issuer.

In certain circumstances, which may include broader economic and market developments, Reporting Issuers must consider whether they should withdraw previously published guidance and financial outlooks if these outlooks can no longer be supported by reasonable assumptions and there is no longer a reasonable basis for the achievement, or accurate updating, of conclusions, forecasts or projections in the FLI. Reporting Issuers that choose to withdraw or cease to report previously disclosed material FLI must disclose the decision to withdraw and discuss events and circumstances that led to the decision to withdraw previously disclosed FLI, including a discussion of any assumptions that are no longer valid. Simply deleting the FLI from the CD documents does not relieve the Reporting Issuer of its disclosure obligations under section 5.8 of NI 51-102.

FLI disclosed outside of MD&A

Many Reporting Issuers disclose FLI in news releases, marketing materials, investor presentations, social media platforms or on their website. Often, FLI in these documents is not supported by the required FLI disclosures. Most notably, some Reporting Issuers do not include the accompanying factors and assumptions to support such FLI and fail to discuss and/or update the FLI in the MD&A. Irrespective of where the FLI is disclosed, Reporting Issuers must comply with the disclosure requirements of Parts 4A/4B and section 5.8 of NI 51-102.

Multi-Year FLI

Some Reporting Issuers present FLI that span multiple years, without providing reasonable and sufficient quantitative and qualitative assumptions to support the FLI. While such multi-year FLI is more prevalent in prospectus filings, we have also observed multi-year FLI on a CD basis. Reporting Issuers must not disclose a financial outlook unless it is based on assumptions that are reasonable in the circumstances. The assumptions for financial projections should be specific and comprehensive, particularly with respect to quantitative details, such that an investor is able to clearly understand how each assumption was used to develop the FLI that contributes to the projections. In general, FLI or future-oriented financial information, must be limited to a time period that can be reasonably estimated, which generally will not go beyond the end of the Reporting Issuer's next fiscal year. Where FLI is presented for multiple years without sufficient support, Staff may ask Reporting Issuers to limit the disclosure of FLI to a shorter period that can be more clearly supported (for example, one or two years, depending on facts and circumstances).

We may also raise questions in cases where a Reporting Issuer's FLI assumptions are not reflected in the Reporting Issuer's track record. For example:

• the Reporting Issuer projects aggressive growth targets (i.e. revenue; store openings) over a certain number of years without the benefit of historical experience or concrete plans in place to support the growth;

• the disclosure does not provide detailed explanations for expected changes to items such as revenue, gross margins, costs or does not provide a reasonable basis for the targets, including the key drivers behind the projected growth with reference to specific plans and objectives that support the projected growth;

• the disclosure does not explain why management believes that each of the targets/FLI is reasonable;

• factors and assumptions do not appear reasonable in light of the Reporting Issuer's size and the scope of the Reporting Issuer's current business plans.

In some cases, Reporting Issuers have been able to address our concerns by amending the FLI disclosure in one or more of the following ways:

• providing more robust factors and assumptions to support the FLI;

• providing more recent information about its operations since the date of the Reporting Issuer's last MD&A in support of the FLI included in the prospectus;

• limiting the disclosure of FLI to a shorter period;

• removing the FLI.

Practice Points

Where FLI is presented for multiple years, we may also ask Issuers to specifically confirm that updates will be provided at least annually, in their continuous disclosure documents of their progress towards achieving the targets. The disclosure includes information on the previously disclosed targets, actual results, and a discussion of the variances. |

We may also ask the Issuer to disclose its policy and processes should it decide to withdraw previously disclosed FLI. |

II) Non-GAAP and other financial measures

NI 52-112 was issued in 2021 to replace the guidance in CSA Staff Notice 52-306 (Revised) Non-GAAP Financial Measures (SN 52-306). Whereas SN 52-306 outlined disclosure expectations for non-GAAP financial measures (as previously defined in SN 52-306), NI 52-112 outlines disclosure requirements for six different categories of measures, being historical NGFMs, forward-looking NGFMs, non-GAAP ratios, capital management measures, total of segments measures and supplementary financial measures (as each are now defined in NI 52-112).

To assess compliance with certain aspects of NI 52-112, during Fiscal 2022, CSA staff reviewed the disclosures in the annual MD&A, related earnings release, and investor presentation of approximately 85 Issuers with financial years ended on or after October 15, 2021. The review primarily focused on disclosures that were "new or different" compared to SN 52-306. Reporting Issuers selected for review varied by size and industry.

Our reviews resulted in outcomes where no action was required, where prospective disclosure enhancements were made, where retrospective restatements were made, or where communication is ongoing to resolve any issues identified. While we were generally pleased with the quality of the disclosure that we observed, we noted the following areas where Reporting Issuers should improve their disclosure:

CSA staff identified the following key deficiencies:

• failure to include the required quantitative reconciliation to the most directly comparable financial measure disclosed in the primary financial statements (i.e. GAAP measure), in earnings releases;

• failure to comply in earnings releases with the requirement that NGFM must be presented with no more prominence than that of the most directly comparable financial measure disclosed in the primary financial statements of the entity to which the measure relates;

• failure to describe the significant differences between NGFMs that are FLI and the equivalent historical NGFMs;

• inappropriate identification of a total of segments measure and consequently, failure to include the required disclosure;

• mislabeling of supplementary financial measures that could lead to confusion or misleading disclosure;

• inappropriate incorporation of information by reference in investor presentations.

For a more fulsome discussion of CSA staff's findings, including examples, please refer to CSA Staff Notice 51-364 Continuous Disclosure Review Program Activities for fiscal years ended March 31, 2022 and March 31, 2021.

Non-GAAP and other financial measures continue to be an area of focus for Staff and we will continue to monitor and review disclosure of NGFMs as part of our normal course CD review program.

III) Overly promotional press releases

Disclosure must be factual and balanced, giving equal prominence to favorable and unfavorable information, with unfavorable information being disclosed as promptly and completely as favorable information.

Increasingly, we are observing Reporting Issuers that disseminate numerous news releases that include overly promotional or "good news" announcements and do not balance this disclosure with unfavorable information that may exist. This trend is particularly prevalent with early stage, pre-revenue Reporting Issuers that are engaged in multiple business opportunities. These Reporting Issuers provide news releases that frequently do not disclose material information or any new material facts and may obscure the true business activity of the Reporting Issuer. We have concerns that this type of promotional disclosure may cause an artificial increase in a Reporting Issuer's share price or trading volume, thereby undermining the integrity of the capital markets, and putting investors at risk of harm by making misinformed investment decisions. In these instances, we may request Reporting Issuers to limit these types of news releases or to issue a clarifying news release. In certain instances, it may also lead to further regulatory action. Further guidance is provided in CSA Staff Notice 51-356 Problematic Promotional Activity by Issuers and National Policy 51-201 Disclosure Practices (NP 51-201).

We have also observed Reporting Issuers that provide news releases announcing multiple partnerships, agreements, transactions or findings from R&D activities, but fail to provide an update on such matters in their MD&A or subsequent news releases. We emphasize that the MD&A is a core document of a Reporting Issuer's continuous disclosure (as well as the AIF, if applicable) and should provide investors with allthe relevant material information impacting the Reporting Issuer's business and operations. Reporting Issuers providing a chronology of news releases issued in the description of business and/or recent developments section of the MD&A should also supplement that disclosure with the necessary updates about the status of these developments.

Reporting Issuers are reminded that if a news release includes information that is forward-looking in nature (for example, estimating production targets, profitability and/or revenue estimates), supporting material factors and assumptions must be provided as required by Part 4A/B of NI 51-102.

- - - - - - - - - - - - - - - - - - - -

Tip: Reporting Issuers should consider the following disclosure best practices:

• establish appropriate written disclosure policies focused on promoting consistent disclosure practices aimed at providing informative, timely and broadly disseminated disclosure of material information to the market;

• consult with advisors, as appropriate, to ensure that the information in the news release is balanced and not misleading or overly-promotional;

• assess the materiality of the information being disseminated and consider whether a material change report should be filed;

• ensure that disclosure in any news release is sufficiently detailed to understand its substance and importance to the Reporting Issuer's business and operations;

• ensure the disclosure is consistent with disclosures previously filed by the Reporting Issuer in news releases or continuous disclosure documents;

• ensure FLI is appropriately supported by material factors and assumptions and updated as required;

• have the board of directors or audit committee review the disclosure in advance of public release, which may increase the quality, credibility and objectivity of such disclosure. Refer to 6.4 (1) of NP 51-201;

• ensure all material information has been included and discussed in the MD&A.

- - - - - - - - - - - - - - - - - - - -

IV) Material contracts

Timing of filing

We continue to see Reporting Issuers who do not file material contracts on a timely basis or at all. We encourage Reporting Issuers to review all contracts entered into within the last financial year, or before the last financial year if the contract is still in effect, to determine whether the contract is a "material contract" that must be filed on SEDAR. While material contracts entered into in the ordinary course of business are generally exempt from filing, we remind Reporting Issuers that any material contract on which the Reporting Issuer's business is substantially dependent must be filed.

The following chart sets out the timeline for filing material contracts that are required to be filed under NI 51-102.

Description |

Timeline for Filing |

|

|

If the Reporting Issuer is required to file an AIF |

|

|

|

• A material contract for which a material change report is filed |

The material contract must be filed no later than the material change report |

|

|

• All other material contracts |

Material contracts made or adopted before the date of the AIF must be filed no later than the time of filing the AIF |

|

|

If the Reporting Issuer is not required to file an AIF |

|

|

|

• A material contract for which a material change report is filed |

The material contract must be filed no later than the material change report |

|

|

• All other material contracts |

Material contracts must be filed within 120 days after the end of the financial year in which they were made/adopted |

- - - - - - - - - - - - - - - - - - - -

Tip: A Reporting Issuer must file any material contracts that are required to be filed under NI 51-102, but that have not been previously filed, at the same time as filing a preliminary prospectus, accelerating the timing for filing a material contract in the context of a prospectus offering. If a material contract is not executed at the time the final prospectus is filed, the Reporting Issuer must file an undertaking to file the contract no later than seven days after the document becomes effective.

- - - - - - - - - - - - - - - - - - - -

Redactions

Reporting Issuers may omit or redact a provision of a material contract that is required to be filed if there are reasonable grounds to believe that disclosing the omitted or redacted provision would violate a confidentiality provision. In these cases, subsection 12.2(5) of NI 51-102 directs the Reporting Issuer to include a description of the type of information that has been omitted or redacted. A brief description immediately following the omitted or redacted information is generally sufficient.

Staff have identified instances where redacted material contracts are filed without these required disclosures. Staff may ask Reporting Issuers to re-file material contracts in instances where the required description of omitted or redacted information has not been included.

V) Diversity on boards and in executive officer positions

Disclosure requirements for the representation of women on boards and in executive officer positions are set out in NI 58-101 and have been in place for eight annual reporting periods. The disclosure requirements are intended to increase transparency for investors and other stakeholders regarding the representation of women in these roles and the approach that specific TSX-listed Reporting Issuers take in respect of such representation. This transparency is intended to assist investors when making investment and voting decisions.

CSA Multilateral Staff Notice 58-314 Review of Disclosure Regarding Women on Boards and in Executive Officer Positions -- Year 8 Report (SN 58-314) was published on October 27, 2022. SN 58-314 reports the findings of our eighth review of disclosure regarding women on boards and in executive officer positions. Of note, 45% of board vacancies filled during the year were filled by women, resulting in 24% of overall board seats being occupied by women, compared to 22% in the prior year. 87% of Reporting Issuers in the review sample had at least one woman on the board and 70% of Reporting Issuers in the review sample had at least one woman in an executive officer position.

The CSA Diversity Initiative Working Group also concluded research and consultations with various stakeholders between June 2021 and October 2021 to determine whether and how the disclosure needs of Canadian investors and corporate governance practices among public companies have evolved since the above noted gender diversity requirements were originally adopted. A virtual 'Diversity in Capital Markets' roundtable, moderated and hosted by the OSC, was held on October 13, 2021. The AMF and ASC also held public roundtables on October 14, 2021 and December 10, 2021, respectively. CSA Staff are continuing to consider feedback received during these consultations.

VI) Related-party transactions/cross financial interests

Staff have observed M&A transactions where either the acquiror or the acquiree (or a director/executive officer of either entity) had an undisclosed financial interest in the other entity. Staff are of the view that, in the context of M&A transactions, detailed disclosure of the cross-ownership of financial interests (held either by the acquirer, the acquiree, or either of their directors or executive officers) is material information for investors and their investment/voting decisions and should be disclosed in the applicable disclosure document.

The cross-ownership of financial interests could give rise to conflicts of interest that may lead investors to re-examine other variables such as purchase price, transaction timing or contingent payments. These variables may not otherwise be considered in the same manner if the potential conflict of interest is not disclosed. Non-disclosure of the cross-ownership of financial interests may also cause investors to question whether the M&A transaction occurred on its own merits.

The document in which disclosure is required will vary depending on the structure of the proposed transaction, whether the Reporting Issuer is the acquiror or acquiree, and the applicable requirements of the stock exchange on which the Reporting Issuer's securities are listed. For example, an M&A transaction may give rise to an obligation to file a material change report, a take-over bid circular, a listing statement / filing statement, or an information circular. A prospectus may also be filed in connection with the M&A transaction. Regardless of the form of document required to be filed, we remind Reporting Issuers to disclose the cross-ownership of financial interests based on the broader materiality requirements of the applicable disclosure document.

Further information on this topic can be found in CSA Multilateral Staff Notice 51-359 Corporate Governance Related Disclosure Expectations for Reporting Issuers in the Cannabis Industry. We note that, while this topic was initially presented in a staff notice specific to the cannabis industry, the same principles are applicable to Reporting Issuers, especially those in emerging growth industries.

VII) Disclosure considerations pertaining to the war in Ukraine (the Conflict)

The unprecedented sanctions imposed by most major governments and disruptions to the global economy as a result of the Conflict have contributed to financial market volatility, and directly and indirectly impacted businesses in Canada and around the world. Issuers that have been or could be materially impacted should provide timely, meaningful, transparent, and balanced disclosures about the impact and the uncertainties to allow investors to make informed investment decisions. Issuers should also keep apprised of ongoing changes and continuously evaluate the necessity to update previously issued disclosure or to provide new disclosure.

Issuers should think broadly when assessing the impact and the uncertainties the Conflict has on its business and operations, for instance, disruption to supply-chains and the ability to access raw materials, and the prices paid for such raw materials, or heightened cybersecurity risks given the potential for cyberattacks perpetuated by state actors. While this list is not exhaustive, some disclosures that may be relevant to understanding the impact of the Conflict include:

• key risks that the conflict presents to the Issuer. Risks should be tailored and disclosures relating to such risks should not be boilerplate;

• known and expected trends, demands, events or uncertainties related to the Conflict that management reasonably believes will materially affect the Issuer's financial condition, future revenue, expenses or projects;

• operational challenges and other measures taken by management in response to the Conflict, including any detailed plans to divest investments or exit operations in Russia, Belarus or Ukraine;

• whether the Issuer has been impacted by the sanctions imposed by the Canadian Federal government or by other jurisdictions. Additionally, Issuers should disclose how management is monitoring compliance with the sanctions imposed;

• discussions about challenges relating to flow of funds and other resources (e.g. raw materials, utilities and labor) that might not be as accessible as a result of the Conflict;

• financial reporting considerations including areas subject to significant judgment and measurement uncertainties relating to the Conflict.

Issuers should carefully consider whether the requirement to file a material change report has been triggered as a result of the impact of the Conflict. Additionally, while Issuers might have provided detailed operational updates via news releases, we remind Issuers that such disclosure should also be included and updated in prospectuses and CD documents, such as MD&A and AIFs.

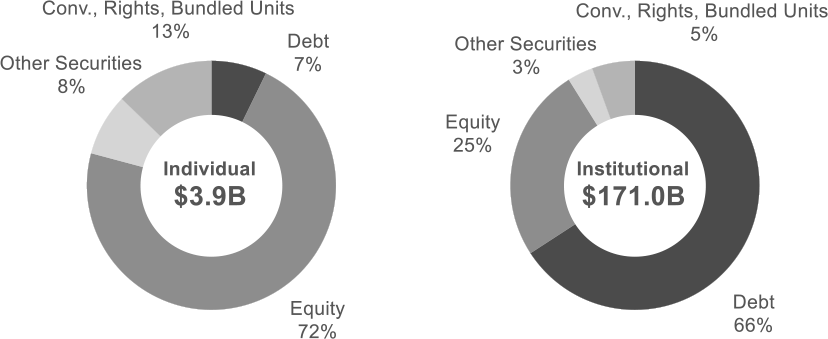

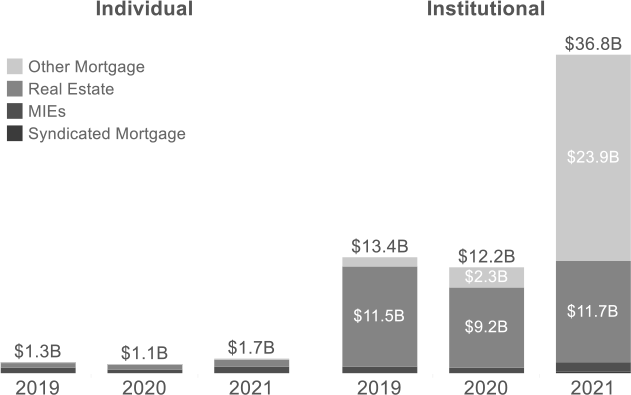

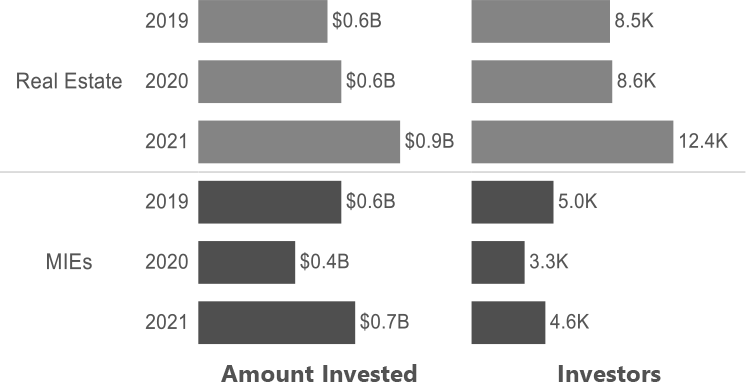

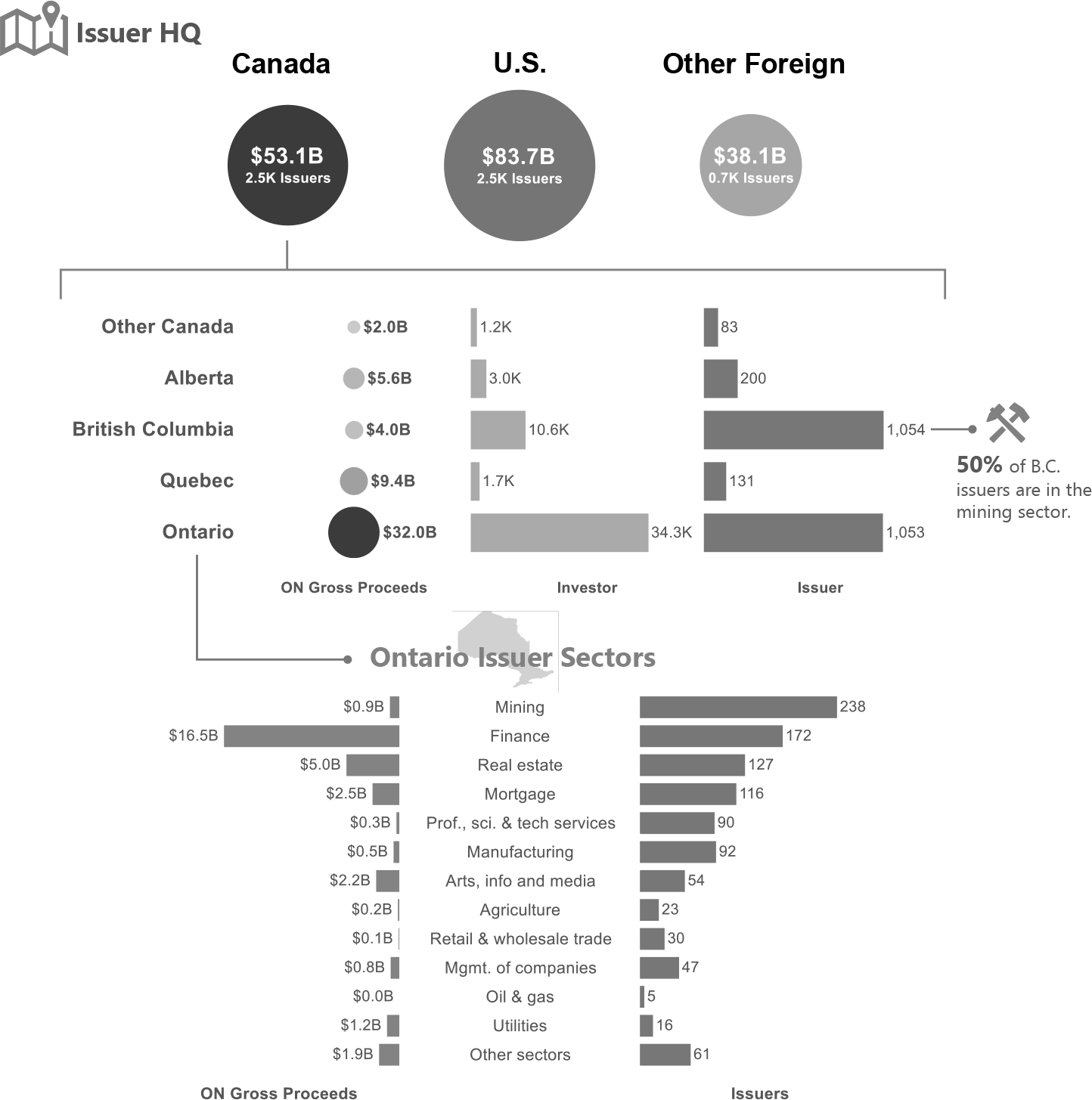

VIII) Syndicated mortgages

Following amendments to NI 45-106, NI 31-103, and OSC Rule 45-501 Ontario Prospectus and Registration Exemptions related to syndicated mortgages that came into force on July 1, 2021, the OSC assumed oversight of higher risk syndicated mortgages sold to retail investors in Ontario and introduced requirements for non-qualified syndicated mortgages distributed to non-permitted clients that are the same as, or stricter than, the requirements for the distribution of other forms of real estate investments.

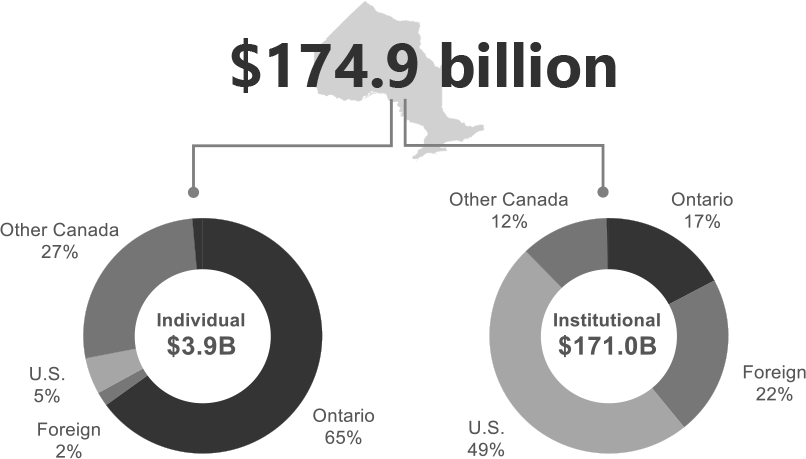

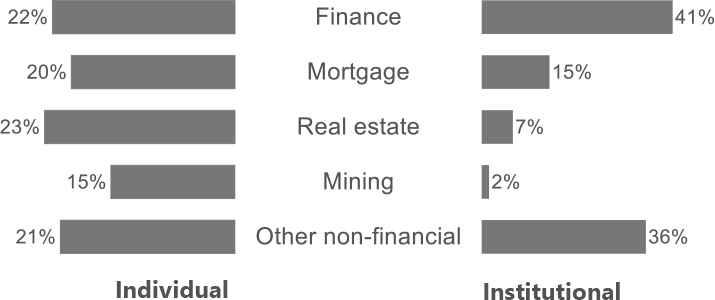

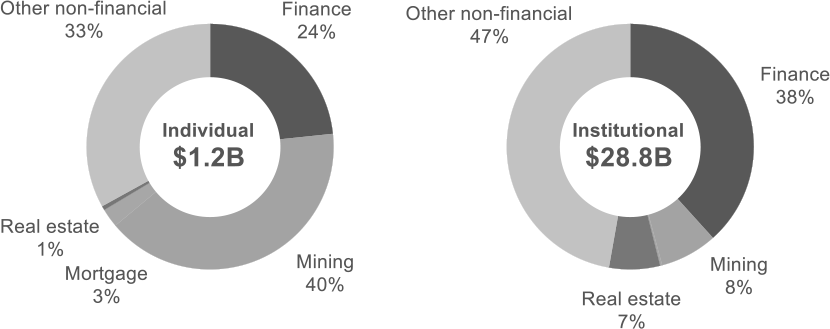

Over the past 12 months, filers reported the issuance of syndicated mortgages for which the OSC has principal oversight under the amended regime with a value of approximately $390 million. The capital raising activity in the syndicated mortgage sector continues to increase at a steady pace.

Capital Raised |

Number of Distributions |

Number of Issuers |

Number of Exempt Market Dealers |

|

|

||||

Q3 & Q4 2021 |

$201,453,531 |

31 |

8 |

4 |

|

||||

Q1 & Q2 2022 |

$189,195,336 |

29 |

14 |

3 |

|

||||

Total 12-month period |

$390,648,868 |

60 |

19 |

4 |

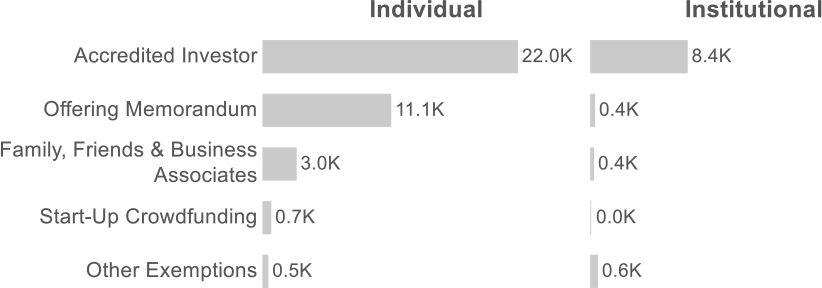

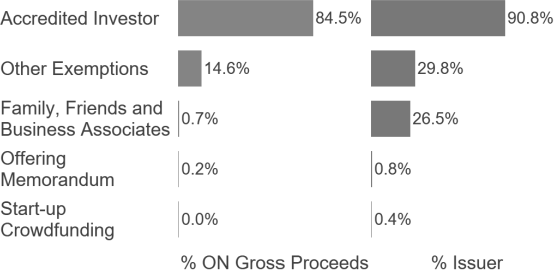

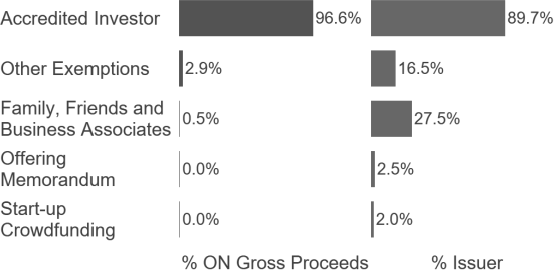

Most distributions (98.3%) were completed under the accredited investor prospectus exemption under section 73.3 of the Act. The remaining distributions were completed using the minimum amount investment prospectus exemption under section 2.10 of NI 45-106 and the family, friends and business associates prospectus exemption under sections 2.5 and 2.6.1 of NI 45-106.

Based on our review of syndicated mortgage investment (SMI) filings, Staff note that Issuers have quickly aligned themselves with the new compliance and reporting requirements, and that legacy loans are being repaid or refinanced through conventional channels. Staff have also observed that non-qualifying SMI issuances are concentrated in a handful of Issuers and exempt market dealers, suggesting that the market is maturing and becoming more specialized.

The OSC works closely with the Financial Services Regulatory Authority to ensure that market participants are licensed or registered with the appropriate regulatory authority and meet the appropriate requirements. Educational information for investors is also regularly updated on https://www.getsmarteraboutmoney.ca/.

IX) Filing reports of exempt distribution

Issuers and underwriters that rely on certain prospectus exemptions to distribute securities are required to file a report of exempt distribution (RED Report) on Form 45-106F1 Report of Exempt Distribution within a prescribed timeframe set out in NI 45-106. We sometimes see Issuers that either file the RED Report late or not at all. The deadline for filing the report is generally 10 days after the distribution.

A distribution occurs in the jurisdiction where a purchaser is resident. In most cases, a distribution also occurs in the jurisdiction where the Issuer's head office is located. A distribution may also occur in a jurisdiction if the Issuer has a significant connection to that jurisdiction. A RED Report must be filed in each jurisdiction in which a distribution takes place.

To determine if a distribution has occurred in one or more jurisdictions of Canada, consult applicable Securities Law. If an Issuer is uncertain as to whether a distribution has occurred in a jurisdiction of Canada, should seek advice as to where the distribution occurred.

For more information on filing a RED Report, please refer to the "Frequently Asked Questions -- Form 45-106F1 Report of Exempt Distribution" document, available on the OSC's website.

X) Crypto asset industry

The crypto asset industry has continued to see growth as well as significant volatility. We have made the following observations regarding recent disclosure by Issuers in the crypto asset industry but also remind Issuers of previous guidance listed at the end of this section. We will continue to monitor disclosure in the crypto asset industry through our review program activities moving forward.

Applicable regulatory regime

Given that the regulatory environment for the crypto asset industry differs across jurisdictions and may, in some cases, be evolving or lack certainty, we consider the following disclosure to be necessary to fairly present all material facts, risks and uncertainties:

• For each jurisdiction in which the Issuer operates:

• details of the Issuer's operations in the jurisdiction;

• the applicable regulatory regime;

• any registrations, exemptions or no action letters relied upon by the Issuer;

• any terms and conditions on those registrations, exemptions or no action letters;

• discussion of any statements or other available guidance made by applicable regulators;

• whether legal advice has been obtained, either in the form of a legal opinion or otherwise, regarding compliance with applicable regulatory regimes;

• Discussion of the Issuer's policies and procedures for monitoring compliance with applicable regulatory regimes, including monitoring for any changes to those regimes;

• Related risks, which may include uncertainty around regulatory regimes applicable to the Issuer's business or crypto assets that are material to the issuer.

We expect the above disclosures to be clearly and prominently disclosed in prospectus filings and other required documents such as an Issuer's AIF, marketing materials, and MD&A (see for example Part 2, Item 1.2 of Form 51-102F1). We also expect Issuers that enter our capital markets through a reverse takeover or spinoff transaction to include these disclosures in their listing statement or other documents, as applicable.

Further to the OSC and CSA news releases from March 29, 2021{6}, we also remind Issuers with operations in Canada (whether providing products or services from a location in Canada or to residents of Canada) that there are potential public interest concerns if an Issuer that is not in compliance with Securities Law were to become an Reporting Issuer. For example, this would be the case if an Issuer that is conducting business that requires registration under Securities Law is not yet registered. If we receive a prospectus from such an Issuer , or an Issuer that is already a Reporting Issuer and not in compliance with Securities Law, we would likely have receipt refusal concerns. We encourage Issuers engaged in novel crypto businesses to consider submitting a confidential prospectus pre-file, if eligible.

Material changes

The determination of whether something is a material fact or material change under Securities Law is fact specific. The CSA has provided guidance on this determination in NP 51-201, which is applicable to Issuers in all industries.

In addition to the examples provided in section 4.3 of NP 51-201, we note the following non-exhaustive list of types of events or information that may be material to Issuers in the crypto asset industry:

• a collapse in the price of a crypto asset to which an Issuer has material exposure;

• an announcement by a regulator of its views about whether a crypto asset that an issuer has material exposure to is a security and/or derivative, or regulatory action taken that includes a view that it is a security and/or derivative;

• entering into by an Issuer of an arrangement for the borrowing or lending of a significant amount of crypto assets or any significant encumbering of the Issuer's crypto assets, including details of the counterparty;

• announcements by a regulator of its views about the business in which the Issuer is engaged, or regulatory action taken against an Issuer with a similar business;

• the issuance by a regulator of a cease-and-desist order against the Issuer, and if the regulator allows the Issuer to operate in the interim, any restrictions placed on its business.

In addition to disclosure requirements regarding material changes and material facts under Securities Law, we remind listed Issuers that the exchange on which they are listed may have timely disclosure policies in respect of material information.

Material contracts

We have observed Issuers that have not filed material contracts on SEDAR as required. We remind Issuers that the exception in subsection 12.2(2) of NI 51-102, for material contracts entered into in the ordinary course of business, is not available in respect of a contract on which the Issuer's business is substantially dependent. For example, if an Issuer enters into a crypto asset loan agreement upon which the solvency of its business is dependent, we would consider this to be a material contract required to be filed.

We also refer Issuers to section 12.3 of NI 51-102 as well as the above guidance regarding material changes (including whether entering into a contract constitutes a material change for the issuer) in regard to the timing for filing a material contract on SEDAR.

Corporate governance

We note there has recently been significant consolidation of Issuers within the crypto asset industry. We remind Issuers that the guidance in Multilateral Staff Notice 51-359 Corporate Governance Related Disclosure Expectations (SN 51-359) for Reporting Issuers in the cannabis industry is equally applicable to Issuers in other emerging growth industries, like the crypto asset industry.

As discussed in SN 51-359, Issuers should

• disclose the cross-ownership of financial interests by Issuers (or their directors and officers) involved in mergers, acquisitions or other significant corporate transactions (M&A transactions), as Staff are of the view that this is material information for investors and their investment/voting decisions,

• give adequate consideration to potential conflicts of interest, or other factors that may compromise their independence when identifying board members as being independent, and

• adopt a written code of business conduct and ethics, which includes standards for ethical decision making and compliance, and which addresses potentially challenging situations that may arise during the normal course of business.

- - - - - - - - - - - - - - - - - - - -

For more information and guidance issuers should also review:

• CSA Staff Notice 51-363 Observations on Disclosure by Crypto Assets Reporting Issuers

• Joint CSA/IIROC Staff Notice 21-330 Guidance for Crypto-Trading Platforms: Requirements relating to Advertising, Marketing and Social Media Use

• CSA Staff Notice 51-356 Problematic promotional activities by issuers

• National Policy 51-201 Disclosure Standards Multilateral Staff Notice 51-359

- - - - - - - - - - - - - - - - - - - -

Under Canadian Securities Law, to distribute securities, an Issuer must file and obtain a receipt for a prospectus or rely upon a prospectus exemption. Another key component of our compliance work stream is the review of prospectuses in connection with public offerings. This section outlines data and trends with respect to public offerings and provides guidance on common issues that arise during our prospectus reviews.

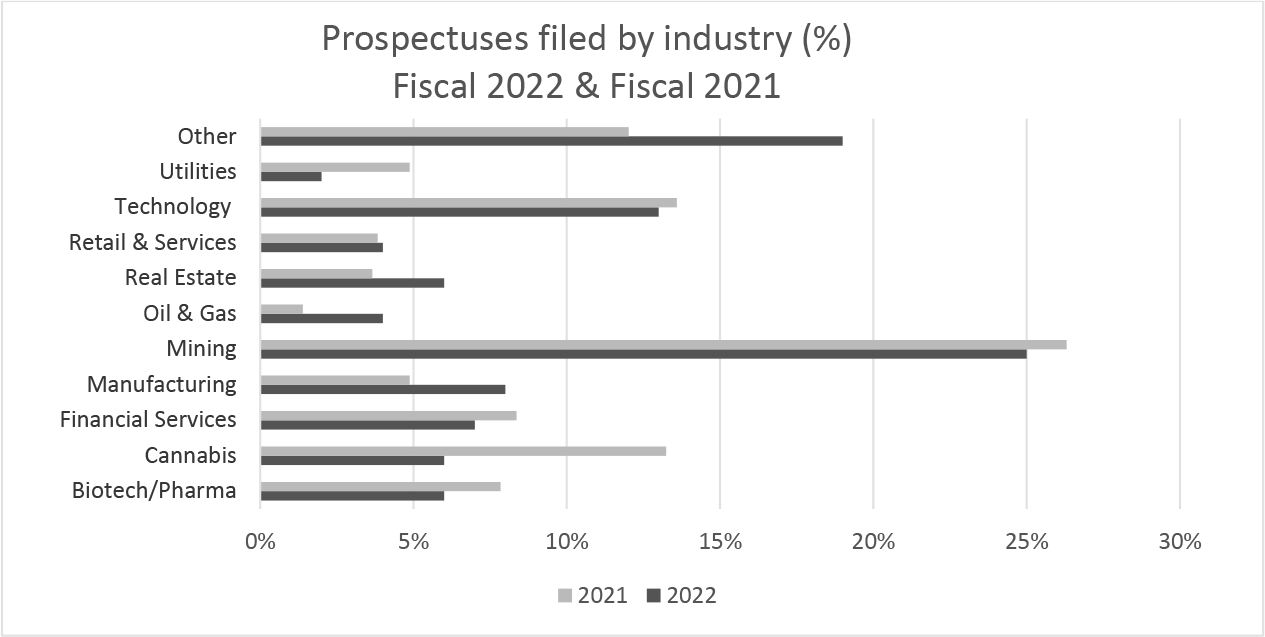

In Fiscal 2022, 702 prospectuses were filed in Ontario (Fiscal 2021: 574). These filings covered a wide range of industries with mining, technology and cannabis being the most active sectors based on the number of offerings.

A) Trends and guidance

Fiscal 2022 was another record-breaking year for prospectus volumes, particularly in the first half of the year. Overall capital raising activity was high for that period, driven by an increase in offerings in the manufacturing and technology industries, as well as a range of other{7} industries. The last quarter of the year saw a drop in activity, partly attributed to geopolitical tensions, volatile markets and other economic factors.

- - - - - - - - - - - - - - - - - - - -

Tip: The guidance in this section also applies to prospectus-level disclosure included in an information circular in connection with a proposed significant acquisition or a restructuring transaction as required by section 14.2 of Form 51-102F5 Information Circular.

- - - - - - - - - - - - - - - - - - - -

Key takeaways from our reviews of prospectuses in Fiscal 2022 are set out below.

I) Primary business requirements in an IPO

Form 41-101F1 Information Required in a Prospectus (Form 41-101F1) requires an Issuer that is not an investment fund to include certain financial statements in its long form prospectus. This includes the financial statements of the Issuer and any business or businesses acquired, or proposed to be acquired, if a reasonable investor reading the prospectus would regard the primary business of the Issuer to be the business or businesses acquired, or proposed to be acquired. The purpose of the primary business requirements is to provide investors with the financial history of the business of the Issuer even if this financial history spanned multiple legal entities over the relevant time period.

On April 14, 2022, changes were made to Companion Policy 41-101CP related to primary business requirements. The purpose of the changes was to harmonize the interpretation of the financial statement requirements for a long form prospectus in situations where an Issuer has acquired a business, or proposes to acquire a business, that a reasonable investor would regard as being the primary business of the Issuer{8}. The changes provide additional guidance on the interpretation of primary business, including in what situations, and for which time periods, financial statements should be required. The changes provide guidance in circumstances when additional information may be necessary for the prospectus to meet the requirement to contain full, true and plain disclosure of all material facts relating to the securities being distributed.

The changes also clarify when an Issuer can use the optional tests in Part 8 of NI 51-102 to calculate the significance of an acquisition, and when an acquisition of mining assets would not be considered an acquisition of a business. The changes were informed by stakeholder feedback that certain inconsistent interpretations of the primary business requirements add time, cost and uncertainty for Issuers. These changes will facilitate a harmonized approach for Issuers across Canada and will reduce regulatory burden by giving Issuers additional clarity on the historical financial information required in an IPO, without compromising investor protection.

The changes came into effect on April 14, 2022.

II) Description of business