Ontario Securities Commission Bulletin

Issue 45/42 - October 20, 2022

Ont. Sec. Bull. Issue 45/42

• Aux Cayes Fintech Co. Ltd. -- ss. 127(1), 127.1

• Mark Hamlin -- s. 2(2) of the TARA, subrule 22(4) of the CMT Rules of Procedure and Forms

• OSC Staff Notice 81-733 -- Summary Report for Investment Fund and Structured Product Issuers

• Ignite International Brands, Ltd.

• Brookfield Asset Management Ltd.

• iA Global Asset Management Inc.

• iA Global Asset Management Inc. and Industrial Alliance, Investment Management Inc.

• Brookfield Property Partners L.P. et al.

• E-L Financial Corporation Limited

• Economic Investment Trust Limited

• Coinsquare Capital Markets Ltd.

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

Marketplaces

• Coinsquare Capital Markets Ltd. -- Notice of Completion of Staff Review of Initial Operation Report

• TriAct Canada Marketplace LP -- Notice of Approval of Proposed Change to the MATCHNow Trading System

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

FOR IMMEDIATE RELEASE

October 11, 2022

TORONTO -- Take notice that the hearing in the above named matter scheduled to be heard on October 13, 2022 at 10:00 a.m. will proceed on October 13, 2022 at 9:30 a.m.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2022

TORONTO -- The Tribunal issued its Reasons and Decision in the above named matter.

A copy of the Reasons and Decision dated October 11, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2022

TORONTO -- Following a hearing held today, the Tribunal issued an Order in the above named matter approving the Settlement Agreement reached between Staff of the Commission and Aux Cayes Fintech Co. Ltd.

A copy of the Order dated October 12, 2022, Oral Reasons for Approval of a Settlement and Settlement Agreement dated September 22, 2022 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2022

TORONTO -- The Tribunal issued an Order in the above named matter.

A copy of the Order dated October 6, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2022

TORONTO -- The Tribunal issued an Order in the above named matter.

A copy of the Order dated October 12, 2022 is available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2022

TORONTO -- Following a hearing held today, the Tribunal issued an Order in the above named matter approving the Settlement Agreement reached between Staff of the Commission and Aux Cayes Fintech Co. Ltd.

A copy of the Order dated October 12, 2022, Oral Reasons for Approval of a Settlement dated October 12, 2022 and Settlement Agreement dated September 22, 2022 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 13, 2022

TORONTO -- The Applicant, Mark Hamlin, filed an Application dated July 8, 2022.

A copy of the Application dated July 8, 2022 and the Order dated September 21, 2022 are available at capitalmarketstribunal.ca.

For Media Inquiries:

For General Inquiries:

Plateau Energy Metals Inc. et al.

FOR IMMEDIATE RELEASE

October 13, 2022

TORONTO -- Take notice of the following merits hearing date changes in the above named matter:

(1) the merits hearing days scheduled on October 17, 18 and 19, 2022 are vacated; and

(2) the merits hearing shall commence on October 24, 2022 at 10:00 a.m., and continue on October 26, 27, 28, 31, 2022, November 1, 2, 2022 and January 11 and 12, 2023 at 10:00 a.m. on each day.

For Media Inquiries:

For General Inquiries:

Aux Cayes Fintech Co. Ltd. -- ss. 127(1), 127.1

File No. 2021-29

Adjudicators: |

Timothy Moseley (chair of the panel) |

|

|

Russell Juriansz |

|

|

|

Sandra Blake |

|

October 12, 2022

WHEREAS on October 12, 2022, the Capital Markets Tribunal (the Tribunal) held a hearing by videoconference to consider the request for approval of a settlement agreement dated September 22, 2022 (the Settlement Agreement) in the matter of Aux Cayes Fintech Co. Ltd. (Aux Cayes);

ON READING the Joint Request for a Settlement Hearing, including the Statement of Allegations dated August 18, 2021, the Settlement Agreement, and the written submissions, on hearing the submissions of the representatives for each of the parties, on considering that Aux Cayes has paid $600,000.00 CAD, $514,950.00 USD and $25,000.00 CAD to the Commission in accordance with the terms of the Settlement Agreement, and on considering the undertaking of Aux Cayes dated September 22, 2022 and attached as Schedule "A" to this Order;

IT IS ORDERED THAT:

1. The Settlement Agreement is approved pursuant to subsection 127(1) of the Securities Act (the Act)

2. Aux Cayes is reprimanded, pursuant to paragraph 6 of subsection 127(1) of the Act; and

3. Aux Cayes shall:

a) pay an administrative penalty in the amount of $600,000 CAD, pursuant to paragraph 9 of subsection 127(1) of the Act;

b) disgorge $514,950.00 USD to the Commission, pursuant to paragraph 10 of subsection 127(1) of the Act; and

c) pay costs of the Commission's investigation in the amount of $25,000.00 CAD, pursuant to section 127.1 of the Act.

1. This Undertaking is given by Aux Cayes Fintech Co. Ltd. (Aux Cayes) to the Ontario Securities Commission (the Commission) in connection with the settlement agreement dated September 22, 2022 in the matter of Aux Cayes Fintech Co. Ltd. (the Settlement Agreement).

2. For the purposes of this Undertaking:

a) "Restricted Products" means any contracts that involve leverage, margin, or the extension of credit, including but not limited to contracts that are marketed/labelled by Aux Cayes as:

(i) futures;

(ii) forward contracts;

(iii) OTC contracts on margin;

(iv) perpetual swaps and futures;

(v) rolling spot;

(vi) contracts for difference;

(vii) options; or

(viii) leveraged tokens.

b) "Retail Customers" means investors who are not "permitted clients" as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

3. In respect of Retail Customers, Aux Cayes undertakes to:

a) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), determine which existing Ontario accounts are held by Retail Customers, including implementing appropriate systems and procedures, acceptable to the Commission, to make that determination;

b) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), implement systems and procedures, acceptable to the Commission, to prevent any Ontario Retail Customers from opening new positions in Restricted Products;

c) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), notify existing Ontario Retail Customers, in a form acceptable to the Commission, that (i) they are only permitted to reduce their existing positions in Restricted Products, (ii) they must close out and settle their existing positions in Restricted Products (including for greater certainty, any margined positions) within 90 days from the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission); and (iii) any funds or assets remaining in Ontario Retail Customer accounts can continue to be used for non-Restricted Products or withdrawn from the OKX Platform.

4. In respect of permitted clients (as defined in National Instrument 31-103), Aux Cayes undertakes to, within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), take steps, acceptable to the Commission, to determine which, if any, Ontario accounts are held by permitted clients, including implementing appropriate systems and procedures to make that determination;

5. Aux Cayes undertakes to engage in discussions with the Commission, with diligence and good faith, with a view to bringing the operations of the crypto asset trading platform www.okx.com (the OKX Platform) into compliance with Ontario securities law, on the following terms:

a) While these discussions are ongoing, Aux Cayes will abide by the following limitations:

(i) Aux Cayes will stop accepting new accounts for investors identified as residents of Ontario. Aux Cayes will maintain and implement the following procedures and controls to prevent Ontario investors from opening new accounts on the OKX Platform:

1) Aux Cayes will maintain the language in the terms of use of the OKX Platform that indicates that residents of Ontario are not permitted to open new accounts on the OKX Platform;

2) as of a date to be determined by Aux Cayes, but no later than 30 days from the approval of the Settlement Agreement, Aux Cayes will ensure that potential investors who identify themselves as residents of Ontario based on the address or identification provided through the account onboarding process are not permitted to open an account with Aux Cayes; and

3) as of a date to be determined by Aux Cayes, but no later than 30 days from the approval of the Settlement Agreement, Aux Cayes will screen the IP address location of potential investors and ensure that potential investors accessing the OKX Platform from an Ontario based IP address are not permitted to open an account with Aux Cayes;

(collectively, the Enhanced Procedures and Controls);

(ii) Aux Cayes will not offer any new products to existing accounts held by Ontario investors;

(iii) Aux Cayes will not engage in any marketing or promotional activities specifically directed at Ontario investors, which include marketing or promotional activities at events that take place in Ontario; and

(iv) Aux Cayes will comply with any additional restrictions that the Commission may require as a condition of continuing registration discussions, or if not prepared to comply with such additional restrictions, terminate registration discussions in accordance with paragraph 6.

6. If at some time during registration discussions (the Decision Date) the Commission concludes and communicates to Aux Cayes that it will not be feasible for the OKX Platform to operate in a manner that is compliant with Ontario securities law, or Aux Cayes, acting in good faith, elects to terminate registration discussions, Aux Cayes undertakes to:

a) identify the accounts on the OKX Platform associated with Ontario investors (Ontario Accounts) and report to the Commission on the number of Ontario Accounts and the aggregate holdings in the Ontario Accounts within 30 days of the Decision Date;

b) cease trading in all Ontario Accounts with no funds or assets remaining in them and close those accounts within 30 days of the Decision Date;

c) with respect to Ontario Accounts with funds or assets remaining in them (Funded Ontario Accounts), initiate steps to return all funds or assets to the account holders by completing the following steps:

(i) send correspondence to account holders of the Funded Ontario Accounts within 30 days of the Decision Date, indicating that:

1) no new deposits of funds or other assets shall be made in the Funded Ontario Accounts;

2) account holders will have a grace period to trade and withdraw their existing holdings, which period expires within 90 days of the Decision Date;

3) upon the expiry of the grace period, no further trading will be permitted in the Funded Ontario Accounts and any funds or assets remaining in the Funded Ontario Accounts will be returned to the account holders; and

4) account holders must contact Aux Cayes to provide instructions regarding the return of funds or assets in their Funded Ontario Accounts.

(ii) attempt to contact the account holders by any other means provided by the account holder if no response to the correspondence referred to above is received within 30 days of sending the correspondence;

(iii) on instruction from the account holders, return the funds or assets in the Funded Ontario Accounts without charging fees;

(iv) close the Funded Ontario Accounts where the funds or assets have been returned to the account holders;

(v) provide email reminders to all remaining Funded Ontario Account holders every 30 days in relation to unreturned funds until all funds are returned;

(vi) deliver to the Commission, on the first and second anniversary of the Decision Date, certificates signed by a senior officer of Aux Cayes listing the Funded Ontario Accounts with funds or assets remaining in them and certifying that Aux Cayes has taken the steps set out above to attempt to obtain instructions from each account holder; and based on the senior officer's knowledge, after exercising reasonable due diligence, also certifying that:

1) Aux Cayes did not open any accounts for clients resident in Ontario since the Decision Date;

2) Aux Cayes has ceased trading in and closed all Ontario Accounts with no funds or assets remaining in them; and

3) the Enhanced Procedures and Controls remain in place on the OKX Platform; and

(vii) if Aux Cayes has not obtained instructions regarding the return of any remaining funds or assets in the Funded Ontario Accounts by the second anniversary of the Decision Date, Aux Cayes shall segregate and maintain control of the remaining funds or assets, or sufficient funds or assets to satisfy all claims by the holders of these accounts, and shall not dispose of them other than in accordance with the relevant user's instructions, or as required by law, or as agreed in writing by the Commission, and provide confirmation to the Commission that it has done so.

7. Aux Cayes shall donate, to Prosper Canada Centre for Financial Literacy, revenues earned from Ontario accounts between June 20, 2022 and either (i) the date registration discussions are successfully completed or (b) if registration discussions are terminated without registration, the date that Aux Cayes has ceased trading in and closed all Ontario accounts.

8. Aux Cayes will refrain from any non-compliance with Ontario securities law in the future.

Dated this 22nd day of September, 2022.

I have authority to bind the corporation

1. Regulators across the globe serve to protect the investing public and preserve the integrity of the capital markets in their respective jurisdictions; therefore, it is imperative that foreign market participants, including online crypto asset trading platforms, make a real and meaningful effort to identify and comply with local securities laws prior to entering a jurisdiction.

2. Foreign companies in the business of online trading of securities or derivatives for Ontario residents are subject to Ontario securities law. The registration and prospectus requirements of the Act foster integrity, fairness and enhance protection for Ontario investors.

3. Aux Cayes Fintech Co. Ltd. (Aux Cayes or the Respondent) operates an online crypto asset trading platform under the trade name "OKX"{1} on which Ontario investors could trade in securities and derivatives based on exposure to underlying assets that included crypto assets.

4. Aux Cayes contravened sections 25 and 53 of the Act by operating as an unregistered dealer of securities to Ontario investors, without any exemption from the registration requirements, and issuing securities without a prospectus or any exemption from the prospectus requirements.

5. A Notice of Hearing was issued and a Statement of Allegations was published in respect of a proceeding against Aux Cayes (the Proceeding) on August 19, 2021.

6. The parties shall jointly file a request that the Capital Markets Tribunal (the Tribunal) issue a Notice of Hearing to announce that it will hold a hearing to consider whether, pursuant to sections 127 and 127.1 of the Securities Act, RSO 1990, c S5, as amended (the Act), it is in the public interest for the Tribunal to make certain orders in respect of Aux Cayes described herein.

7. The Respondent agrees to the making of an order substantially in the form attached as Schedule "A" (the Order) based on the facts set out below. For the purposes of the Proceeding, and any other regulatory proceeding commenced by a securities regulatory authority, derivatives regulatory authority or financial regulatory authority, the Respondent agrees with the facts set out in Part III and the conclusions in Part IV of this Settlement Agreement (the Settlement Agreement).

A. Aux Cayes

8. Aux Cayes is a corporation incorporated under the laws of the Republic of Seychelles on March 7, 2018.

9. Aux Cayes has never been registered with the Ontario Securities Commission (the Commission) to engage in the business of trading or obtained an exemption from the registration requirement. Aux Cayes has never filed a prospectus with the Commission or obtained an exemption from the prospectus requirement.

10. Aux Cayes operates the crypto asset trading platform www.okx.com{2} (the OKX Platform). The OKX Platform was launched on or about October 1, 2017 by Aux Cayes' predecessor company, OKEX Technology Company Limited. Aux Cayes assumed the operation of the OKX Platform upon Aux Cayes' incorporation.

11. Investors access the OKX Platform by first creating an account on the OKX Platform using an online account opening process. After opening an account, an investor may deposit crypto assets into the account. An investor makes a crypto asset deposit by transferring crypto assets to a wallet controlled by Aux Cayes. Through a "Buy/Sell crypto gateway" on the OKX Platform, an investor may also use fiat currency to purchase crypto assets, which are then credited to the investor's account and are held in a wallet controlled by Aux Cayes. (Aux Cayes does not handle customer fiat currency, but operates the "Buy/Sell gateway" in partnership with various vendors and fiat processors.)

12. Investors may trade crypto assets credited to their account for a variety of other crypto assets. The crypto assets available on the platform include, among others, Bitcoin and Ether.

13. Aux Cayes maintains custody of crypto assets deposited and traded on the OKX Platform in wallets Aux Cayes controls. Investors do not have possession or control of crypto assets deposited or traded on the OKX Platform. Rather, they see a crypto asset balance displayed on their account on the OKX Platform. In order to take possession of crypto assets reflected in their OKX account balance, an investor must request a withdrawal and is dependent on Aux Cayes to satisfy that withdrawal request by delivering crypto assets to an investor-controlled wallet.

14. While Aux Cayes purports to facilitate trading of the crypto assets in its investors' accounts, in practice, Aux Cayes only provides its investors with instruments or contracts involving crypto assets. These instruments or contracts constitute securities and derivatives.

15. Investors may also trade crypto asset futures, swap and options contracts on the OKX Platform that constitute securities and derivatives. The OKX Platform allows investors to engage in leveraged trading of up to 125:1 on various futures and swap contracts.

16. Aux Cayes charges fees for trades made on the OKX Platform and a fee for crypto asset withdrawals.

B. Ontario Investors

17. Aux Cayes made the OKX Platform available to Ontario investors. There was no restriction in the OKX Platform's terms of service to disallow Ontario investors from using the OKX Platform. Aux Cayes' website indicated that investors may, through third-party payment providers, use Canadian fiat currency to purchase crypto assets on the OKX Platform. Ontario was also not identified in the list of restricted jurisdictions on Aux Cayes' website.

18. As of June 20, 2022, Aux Cayes and its predecessor company had opened approximately 21,292 accounts for investors resident in Ontario since the launch of its trading platform on or about October 1, 2017. Ontario investors deposited crypto assets into 1,534 of these accounts, and used these accounts to trade the products offered on the OKX Platform, as described above. The remaining 19,758 accounts opened by Ontarians did not receive any deposits and no trading was conducted in them.

19. The total revenue Aux Cayes and its predecessor company obtained from the 1,534 Ontario accounts that received deposits and were used for trading was approximately $514,950 USD as of June 20, 2022.

C. Communications with Aux Cayes

20. On March 29, 2021, the Commission issued a press release notifying crypto asset trading platforms that currently offer trading in derivatives or securities to persons or companies located in Ontario that they must bring their operations into compliance with Ontario securities law or face potential regulatory action. The press release included a deadline of April 19, 2021 for such platforms to start registration discussions. The press release followed regulatory guidance issued by the Canadian Securities Administrators and the Investment Industry Regulatory Organization of Canada on the application of securities legislation to crypto asset trading platforms.

21. Despite this warning, Aux Cayes did not contact the Commission by April 19, 2021 to start registration discussions.

22. In May 2021, the Commission took steps to inform Aux Cayes that it may be conducting registrable activity in Ontario. Aux Cayes responded to the Commission in June 2021 and advised that Aux Cayes would identify and close its Ontario accounts.

D. Aggravating Factors

23. In July 2021, the Commission requested information from Aux Cayes regarding its Ontario accounts including the information listed above in paragraphs 18-19. Aux Cayes represented to the Commission that the requested information was not available. Upon further inquiry by the Commission as to why it was not available, Aux Cayes did not provide an explanation. Aux Cayes's representation was incorrect.

24. In April 2022, Aux Cayes repeated its representation to the Commission that it no longer had the data that the Commission was inquiring about. Aux Cayes informed the Commission that the reason it did not have the data was because it had closed Ontario accounts, which had led to the deletion of customers' personal information pursuant to various data protection and privacy laws. This representation was incorrect.

25. In June 2022, Aux Cayes advised the Commission that the Ontario account information was available and that Aux Cayes was willing to provide it.

26. In July 2022, Aux Cayes provided the Commission with information regarding its Ontario operations, including the information set out in paragraphs 18-19 above.

E. Mitigating Factors

27. After being contacted by the Commission in May 2021, Aux Cayes took steps aimed at limiting Ontario investors' access to the OKX Platform, including:

a) amending its Terms of Service in June 2021 to include Ontario in the list of restricted locations;

b) by July 2021, blocking deposits by users attempting to make deposits in pre-existing accounts while connected to an Ontario IP address;

c) by August 2021, implementing pop up notifications for users attempting to open new accounts while connected to an Ontario IP address, and for existing users attempting to trade on the OKX Platform while connected to an Ontario IP address;

28. Since late June 2022, Aux Cayes has maintained an open dialogue, expressed an interest in reaching a negotiated resolution and has provided all requested information promptly and in a transparent manner, making a disgorgement order possible.

29. Aux Cayes will take steps to explore the registration and compliance process with the Commission. To that end, Aux Cayes is prepared to give a comprehensive undertaking to restrict its Ontario business while it pursues registration, and to leave Ontario in an orderly fashion if registration discussions terminate (as further described below).

30. The Respondent admits and acknowledges that it breached Ontario securities law by, without lawful exemption:

a) engaging in the business of trading in securities without registration in accordance with Ontario securities law, contrary to subsection 25(1) of the Act; and

b) engaging in trading in securities which constitute distributions without a preliminary prospectus or a prospectus having been filed with the Commission, contrary to subsection 53(1) of the Act.

31. The Respondent agrees to the terms of settlement listed below and consents to the Order in substantially the form attached hereto as Schedule "A", which provides that:

a) the Settlement Agreement is approved;

b) Aux Cayes is reprimanded, pursuant to paragraph 6 of subsection 127(1) of the Act;

c) Aux Cayes shall:

(i) pay an administrative penalty in the amount of $600,000.00 CAD by wire transfer to the Commission before the commencement of the Settlement Hearing, pursuant to paragraph 9 of subsection 127(1) of the Act;

(ii) disgorge $514,950.00 USD by wire transfer to the Commission before the commencement of the Settlement Hearing, pursuant to paragraph 10 of subsection 127(1) of the Act. This amount represents the total revenue earned from Ontario accounts up to June 20, 2022; and

(iii) pay costs of the Commission's investigation in the amount of $25,000.00 CAD by wire transfer to the Commission before the commencement of the Settlement Hearing, pursuant to section 127.1 of the Act.

32. Aux Cayes has given the undertaking (the Undertaking) to the Commission attached as Schedule "B" to this Settlement Agreement, pursuant to which Aux Cayes undertakes as follows:

a) Aux Cayes will take the steps outlined in the Undertaking to wind down its existing Ontario business in respect of Restricted Products (as defined in the Undertaking) for Retail Customers (as defined in the Undertaking);

b) Aux Cayes will engage in discussions with the Commission, with diligence and good faith, with a view to bringing the operations of the OKX Platform into compliance with Ontario securities law, on terms that include the following limitations while such discussions are ongoing:

(i) Aux Cayes will stop accepting new accounts for investors identified as residents of Ontario;

(ii) Aux Cayes will not offer any new products to existing accounts held by Ontario investors;

(iii) Aux Cayes will not engage in any marketing or promotional activities specifically directed at Ontario investors, which include marketing or promotional activities at events that take place in Ontario; and

(iv) Aux Cayes will comply with any additional restrictions that the Commission may require as a condition of continuing registration discussions, or if not prepared to comply with such additional restrictions, terminate registration discussions in accordance with the terms prescribed in the Undertaking;

c) If at any time during registration discussions, the Commission concludes and communicates to Aux Cayes that it will not be feasible for the OKX Platform to operate in a manner that is compliant with Ontario securities law, or Aux Cayes, acting in good faith, elects to terminate registration discussions, Aux Cayes will wind down its Ontario operations within the time frame and on the terms prescribed in the Undertaking;

d) Aux Cayes will donate to Prosper Canada Centre for Financial Literacy , ongoing revenues from Ontario accounts until Aux Cayes either (i) becomes registered, or (ii) has wound down its operations;

e) Aux Cayes will refrain from any non-compliance with Ontario securities law in the future.

33. Aux Cayes agrees to attend at the hearing before the Tribunal to consider the proposed settlement by video conference.

34. If the Tribunal approves this Settlement Agreement, no enforcement proceeding will be commenced or continued under Ontario securities law against Aux Cayes in relation to the facts set out in Part III of this Settlement Agreement, subject to paragraphs 35 and 36 below.

35. This Settlement Agreement is premised on, among other things, representations made by Aux Cayes, including about the number of Ontario accounts (approximately 21,292) and the amounts obtained by Aux Cayes and its predecessor company (approximately $514,950.00 USD in revenue from the Ontario accounts) as of June 20, 2022. If Aux Cayes and its predecessor company opened and operated materially more Ontario accounts or if Aux Cayes and its predecessor company obtained materially more funds than it represented, enforcement proceedings under Ontario securities law may be brought against the Respondent.

36. If the Respondent fails to comply with any term in this Settlement Agreement or the Undertaking, enforcement proceedings under Ontario securities law may be brought against the Respondent.

37. A proceeding referenced in paragraph 35 or 36 may be based on, among other things, the facts set out in Part III of this Settlement Agreement as well as the breach of this Settlement Agreement or the Undertaking.

38. The Respondent waives any defences to a proceeding referenced in paragraph 35 or 36 that are based on the limitation period in the Act, provided that no proceeding referenced in paragraph 36 shall be commenced later than six years from the date of the occurrence of the last failure to comply with this Settlement Agreement or the Undertaking.

39. The parties will seek approval of this Settlement Agreement at a public hearing (the Settlement Hearing) before the Tribunal, according to the procedures set out in this Settlement Agreement and the Tribunal's Rules of Procedure and Forms.

40. The parties agree that this Settlement Agreement sets forth all of the agreed facts that will be submitted at the Settlement Hearing, unless the parties agree that additional facts should be submitted at the Settlement Hearing.

41. If the Tribunal approves this Settlement Agreement:

a) Aux Cayes irrevocably waives all rights to a full hearing, judicial review or appeal of this matter under the Act; and

b) neither party will make any public statement that is inconsistent with this Settlement Agreement or with any additional agreed facts submitted at the Settlement Hearing.

42. Whether or not the Tribunal approves this Settlement Agreement, Aux Cayes will not use, in any proceeding, this Settlement Agreement or the negotiation or process of approval of this Settlement Agreement as the basis for any attack on the Commission's or the Tribunal's jurisdiction, alleged bias, alleged unfairness, or any other remedies or challenges that may otherwise be available.

43. If the Tribunal does not approve this Settlement Agreement or does not make an order substantially in the form of the Order attached as Schedule "A" to this Settlement Agreement:

a) this Settlement Agreement and all discussions and negotiations between the parties before the Settlement Hearing takes place will be without prejudice to either party; and

b) the parties will each be entitled to all available proceedings, remedies and challenges, including proceeding to a hearing on the merits of the allegations contained in the Statement of Allegations. Any such proceedings, remedies and challenges will not be affected by this Settlement Agreement, or by any discussions or negotiations relating to this Settlement Agreement.

44. The parties will keep the terms of this Settlement Agreement confidential until the Tribunal approves the Settlement Agreement, except as is necessary to make submissions at the Settlement Hearing. If, for whatever reason, the Tribunal does not approve the Settlement Agreement, the terms of the Settlement Agreement shall remain confidential indefinitely, unless the parties otherwise agree in writing or if required by law.

45. This Settlement Agreement may be signed in one or more counterparts which, together, constitute a binding agreement.

46. A facsimile copy or other electronic copy of any signature will be as effective as an original signature.

Dated this 22nd day of September, 2022.

I have authority to bind the corporation

{1} On January 18, 2022, the crypto asset trading platform was rebranded from OKEx to OKX.

{2} Formerly www.okex.com.

FILE NO.: 2021-29

WHEREAS on [date], the Capital Markets Tribunal (the Tribunal) held a hearing by videoconference to consider the request for approval of a settlement agreement dated September 22, 2022 (the Settlement Agreement) in the matter of Aux Cayes Fintech Co. Ltd. (Aux Cayes);

ON READING the Joint Request for a Settlement Hearing, including the Statement of Allegations dated August 19, 2021, the Settlement Agreement, and the written submissions, on hearing the submissions of the representatives for each of the parties, on considering that Aux Cayes has paid $600,000.00 CAD, $514,950.00 USD and $25,000.00 CAD to the Commission in accordance with the terms of the Settlement Agreement, and on considering the undertaking of Aux Cayes dated September 22, 2022 and attached as Schedule "A" to this Order;

IT IS ORDERED THAT:

1. The Settlement Agreement is approved pursuant to subsection 127(1) of the Securities Act (the Act)

2. Aux Cayes is reprimanded, pursuant to paragraph 6 of subsection 127(1) of the Act; and

3. Aux Cayes shall:

a) pay an administrative penalty in the amount of $600,000 CAD, pursuant to paragraph 9 of subsection 127(1) of the Act;

b) disgorge $514,950.00 USD to the Commission, pursuant to paragraph 10 of subsection 127(1) of the Act; and

c) pay costs of the Commission's investigation in the amount of $25,000.00 CAD, pursuant to section 127.1 of the Act.

1. This Undertaking is given by Aux Cayes Fintech Co. Ltd. (Aux Cayes) to the Ontario Securities Commission (the Commission) in connection with the settlement agreement dated September 22, 2022 in the matter of Aux Cayes Fintech Co. Ltd. (the Settlement Agreement).

2. For the purposes of this Undertaking:

a) "Restricted Products" means any contracts that involve leverage, margin, or the extension of credit, including but not limited to contracts that are marketed/labelled by Aux Cayes as:

(i) futures;

(ii) forward contracts;

(iii) OTC contracts on margin;

(iv) perpetual swaps and futures;

(v) rolling spot;

(vi) contracts for difference;

(vii) options; or

(viii) leveraged tokens.

b) "Retail Customers" means investors who are not "permitted clients" as defined in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations.

3. In respect of Retail Customers, Aux Cayes undertakes to:

a) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), determine which existing Ontario accounts are held by Retail Customers, including implementing appropriate systems and procedures, acceptable to the Commission, to make that determination;

b) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), implement systems and procedures, acceptable to the Commission, to prevent any Ontario Retail Customers from opening new positions in Restricted Products;

c) within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), notify existing Ontario Retail Customers, in a form acceptable to the Commission, that (i) they are only permitted to reduce their existing positions in Restricted Products, (ii) they must close out and settle their existing positions in Restricted Products (including for greater certainty, any margined positions) within 90 days from the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission); and (iii) any funds or assets remaining in Ontario Retail Customer accounts can continue to be used for non-Restricted Products or withdrawn from the OKX Platform.

4. In respect of permitted clients (as defined in National Instrument 31-103), Aux Cayes undertakes to, within 60 days of the approval of the Settlement Agreement (unless a different time frame is agreed to in writing by the Commission), take steps, acceptable to the Commission, to determine which, if any, Ontario accounts are held by permitted clients, including implementing appropriate systems and procedures to make that determination;

5. Aux Cayes undertakes to engage in discussions with the Commission, with diligence and good faith, with a view to bringing the operations of the crypto asset trading platform www.okx.com (the OKX Platform) into compliance with Ontario securities law, on the following terms:

a) While these discussions are ongoing, Aux Cayes will abide by the following limitations:

(i) Aux Cayes will stop accepting new accounts for investors identified as residents of Ontario. Aux Cayes will maintain and implement the following procedures and controls to prevent Ontario investors from opening new accounts on the OKX Platform:

1) Aux Cayes will maintain the language in the terms of use of the OKX Platform that indicates that residents of Ontario are not permitted to open new accounts on the OKX Platform;

2) as of a date to be determined by Aux Cayes, but no later than 30 days from the approval of the Settlement Agreement, Aux Cayes will ensure that potential investors who identify themselves as residents of Ontario based on the address or identification provided through the account onboarding process are not permitted to open an account with Aux Cayes; and

3) as of a date to be determined by Aux Cayes, but no later than 30 days from the approval of the Settlement Agreement, Aux Cayes will screen the IP address location of potential investors and ensure that potential investors accessing the OKX Platform from an Ontario based IP address are not permitted to open an account with Aux Cayes;

(collectively, the Enhanced Procedures and Controls);

(ii) Aux Cayes will not offer any new products to existing accounts held by Ontario investors;

(iii) Aux Cayes will not engage in any marketing or promotional activities specifically directed at Ontario investors, which include marketing or promotional activities at events that take place in Ontario; and

(iv) Aux Cayes will comply with any additional restrictions that the Commission may require as a condition of continuing registration discussions, or if not prepared to comply with such additional restrictions, terminate registration discussions in accordance with paragraph 6.

6. If at some time during registration discussions (the Decision Date) the Commission concludes and communicates to Aux Cayes that it will not be feasible for the OKX Platform to operate in a manner that is compliant with Ontario securities law, or Aux Cayes, acting in good faith, elects to terminate registration discussions, Aux Cayes undertakes to:

a) identify the accounts on the OKX Platform associated with Ontario investors (Ontario Accounts) and report to the Commission on the number of Ontario Accounts and the aggregate holdings in the Ontario Accounts within 30 days of the Decision Date;

b) cease trading in all Ontario Accounts with no funds or assets remaining in them and close those accounts within 30 days of the Decision Date;

c) with respect to Ontario Accounts with funds or assets remaining in them (Funded Ontario Accounts), initiate steps to return all funds or assets to the account holders by completing the following steps:

(i) send correspondence to account holders of the Funded Ontario Accounts within 30 days of the Decision Date, indicating that:

1) no new deposits of funds or other assets shall be made in the Funded Ontario Accounts;

2) account holders will have a grace period to trade and withdraw their existing holdings, which period expires within 90 days of the Decision Date;

3) upon the expiry of the grace period, no further trading will be permitted in the Funded Ontario Accounts and any funds or assets remaining in the Funded Ontario Accounts will be returned to the account holders; and

4) account holders must contact Aux Cayes to provide instructions regarding the return of funds or assets in their Funded Ontario Accounts.

(ii) attempt to contact the account holders by any other means provided by the account holder if no response to the correspondence referred to above is received within 30 days of sending the correspondence;

(iii) on instruction from the account holders, return the funds or assets in the Funded Ontario Accounts without charging fees;

(iv) close the Funded Ontario Accounts where the funds or assets have been returned to the account holders;

(v) provide email reminders to all remaining Funded Ontario Account holders every 30 days in relation to unreturned funds until all funds are returned;

(vi) deliver to the Commission, on the first and second anniversary of the Decision Date, certificates signed by a senior officer of Aux Cayes listing the Funded Ontario Accounts with funds or assets remaining in them and certifying that Aux Cayes has taken the steps set out above to attempt to obtain instructions from each account holder; and based on the senior officer's knowledge, after exercising reasonable due diligence, also certifying that:

1) Aux Cayes did not open any accounts for clients resident in Ontario since the Decision Date;

2) Aux Cayes has ceased trading in and closed all Ontario Accounts with no funds or assets remaining in them; and

3) the Enhanced Procedures and Controls remain in place on the OKX Platform; and

(vii) if Aux Cayes has not obtained instructions regarding the return of any remaining funds or assets in the Funded Ontario Accounts by the second anniversary of the Decision Date, Aux Cayes shall segregate and maintain control of the remaining funds or assets, or sufficient funds or assets to satisfy all claims by the holders of these accounts, and shall not dispose of them other than in accordance with the relevant user's instructions, or as required by law, or as agreed in writing by the Commission, and provide confirmation to the Commission that it has done so.

7. Aux Cayes shall donate, to Prosper Canada Centre for Financial Literacy, revenues earned from Ontario accounts between June 20, 2022 and either (i) the date registration discussions are successfully completed or (b) if registration discussions are terminated without registration, the date that Aux Cayes has ceased trading in and closed all Ontario accounts.

8. Aux Cayes will refrain from any non-compliance with Ontario securities law in the future.

Dated this 22nd day of September, 2022.

I have authority to bind the corporation

Mark Hamlin -- s. 2(2) of the TARA, subrule 22(4) of the CMT Rules of Procedure and Forms

File No. 2022-16

Adjudicators: |

Andrea Burke (Chair of the panel) |

|

|

Timothy Moseley |

|

October 06, 2022

WHEREAS on September 28, 2022, Staff of the Ontario Securities Commission requested that the Capital Markets Tribunal revoke paragraph 4 of the order of the Tribunal dated September 21, 2022, which provided among other things that material filed in connection with this application be kept confidential;

ON CONSIDERING that Hamlin is no longer seeking the confidentiality relief requested in paragraph 3 of his Application dated July 8, 2022, and that he takes no position on this request by Staff;

IT IS ORDERED THAT paragraph 4 of the order of September 21, 2022, is revoked.

File No. 2022-16

Adjudicators: |

Andrea Burke (Chair of the panel) |

|

|

Timothy Moseley |

|

October 12, 2022

WHEREAS Mark Hamlin applied under s. 17 of the Securities Act for an order authorizing him to make various disclosures in connection with a proceeding in the United States District Court for the Southern District of New York;

AND WHEREAS the Capital Markets Tribunal directed that Hamlin and Staff of the Ontario Securities Commission make written submissions on the preliminary question of whether the Capital Markets Tribunal has jurisdiction to grant the s. 17 order that Hamlin seeks;

ON READING the submissions from Hamlin and from Staff of the Ontario Securities Commission;

IT IS ORDERED THAT:

1. the preliminary question, whether the Capital Markets Tribunal has jurisdiction to grant the order sought, is answered in the affirmative, with reasons to follow; and

2. the balance of the application shall be heard on a date to be fixed by the Registrar.

File No. 2022-16

Adjudicators: |

Andrea Burke (Chair of the panel) |

|

|

Timothy Moseley |

|

September 21, 2022

WHEREAS on September 20, 2022, the Capital Markets Tribunal received submissions from representatives for Mark Hamlin and for Staff of the Ontario Securities Commission regarding a joint request for a proposed timetable and further submissions from the representative for Mark Hamlin on September 21, 2022 regarding his position on the relief sought in the application;

IT IS ORDERED THAT:

1. Staff serve and file submissions of no longer than three pages, to address the jurisdiction of the Tribunal to make the order requested in paragraph 1 of the Notice of Application, by no later than 12:00 p.m. on September 28, 2022;

2. the Applicant serve and file responding submissions, if any, of no longer than three pages, by no later than 9:00 a.m. on October 3, 2022;

3. Staff serve and file reply submissions, if any, of no longer than two pages, by 12:00 p.m. on October 7, 2022; and

4. pursuant to subsection 2(2) of the Tribunal Adjudicative Records Act, 2019, SO 2019, c 7, Sch 60, and Rule 22(4) of the Rules of Procedure, the material filed with the Tribunal in connection with this application, and this Order, shall be kept confidential, pending any further order regarding the confidentiality of this application.

The Applicant, Mark Hamlin ("Hamlin"), requests that the Tribunal make an order (the "Section 17 Order") pursuant to section 17 of the Securities Act, RSO 1990 c. S.5 (the "OSA" or the "Act") which provides that:

1. Hamlin is authorized to provide deposition testimony in the SDNY Action (as defined below) and make related disclosures to the United States District Court for the Southern District of New York (the "SDNY Court"), concerning the following topics:

a. the Commission's investigation order which was issued in relation to this matter on April 2, 2019 pursuant to section 11 of the OSA (the "Investigation Order");

b. Hamlin's compelled testimony given at an examination conducted on May 23, 2019 under section 13 of the OSA (the "Hamlin Examination");

c. the transcript of the Hamlin Examination (the "Hamlin Transcript");

d. any other document, correspondence, information or evidence relating to the Hamlin Examination and any related interactions with OSC Staff or the Commodity Futures Trading Commission's Division of Enforcement Staff ("CFTC Staff") that is subject to the confidentiality restrictions set out in section 16 of the OSA or by the Investigation Order;

2. Except as expressly provided for, nothing in the Section 17 Order shall abrogate any of the rights or privileges afforded to Hamlin under:

a. the OSA in relation to the information described in paragraph 1 above or any other protections that may otherwise apply to this information pursuant to section 16 of the OSA;

b. the Stipulated Protective Order of the Honourable Judge H. Paul Oetken dated July 30, 2020, or the Ontario Court Order (as each are defined below); and

c. any other rights and privileges under the laws of Canada, Ontario, and the United States.

3. This application, the Tribunal's decision and the Section 17 Order shall remain confidential and shall not be made available to the public, but this does not prohibit the Tribunal's decision and the Section 17 Order from being disclosed as necessary in the Applicant's deposition in the SDNY Action, to the SDNY Court (redacted or filed under seal, if and as appropriate), or to the parties in the SDNY Action.

The grounds for the request are:

I. Background

4. On April 2, 2019, at the request of CFTC Staff, the Ontario Securities Commission ("OSC" or the "Commission") issued an order authorizing certain members of the Commission's staff ("OSC Staff") and CFTC Staff to investigate and inquire into "possible violations of the United States Commodity Exchange Act and CFTC Regulations thereunder concerning manipulation of certain swap rates involving" a certain U.S. financial institution (the "Investigation Order").

5. On April 15, 2019, pursuant to the Investigation Order, Hamlin was issued a section 13 summons compelling his attendance at the Commission's offices on May 23, 2019.

6. On May 23, 2019, the Hamlin Examination was conducted by OSC Staff and CFTC Staff at the Commission's offices in Toronto.

7. On May 31, 2019, OSC Staff sent a letter to Hamlin's Canadian counsel, Usman Sheikh of Gowling WLG (Canada) LLP ("Sheikh"), advising him that OSC Staff had authorized the release of the Hamlin Transcript to Sheikh. Among other things, OSC Staff's letter excerpted subsection 16(1) of the OSA in its entirety and stated: "[p]lease note that section 16 of the Act prohibits the disclosure of information or evidence obtained under section 11."

II. The SDNY Action

8. On December 20, 2019, the CFTC commenced an action (the "SDNY Action") against Christophe Rivoire ("Rivoire") in the United States District Court for the Southern District of New York (the "SDNY Court"). Hamlin is not a party to the SDNY Action.

9. By Order of the SDNY Court dated May 26, 2022, in the SDNY Action (Docket No. 70), fact discovery in the SDNY Action, including any deposition of Hamlin, must be completed by no later than August 1, 2022.

III. The SDNY Letter of Request

10. On September 24, 2021, Rivoire filed an unopposed motion with the SDNY Court for the issuance of a letter of request to seek the assistance of the Ontario courts in order to compel Hamlin to provide deposition testimony in the SDNY Action.

11. On January 24, 2022, the SDNY Court granted Rivoire's motion pursuant to an order of the Honourable Judge J. Paul Oetken. On February 3, 2022, the SDNY Court signed and issued the Letter of Request (the "Letter of Request").

12. On February 9, 2022, with Mr. Hamlin's consent, Rivoire applied to the Ontario Superior Court of Justice (the "Ontario Superior Court") to recognize and enforce Judge Oetken's Letter of Request. On March 8, 2022, the Ontario Superior Court issued an Order on consent recognizing the Letter of Request and directing Mr. Hamlin to give deposition testimony in the SDNY Action (the "Ontario Court Order").

IV. The CFTC's Disclosure of the Hamlin Examination to Rivoire's U.S. Counsel

13. During the pre-trial discovery phase of the SDNY Action, the Applicant learned that CFTC Staff had produced a copy of the Hamlin Transcript to Rivoire's US counsel during pre- trial discovery in the SDNY Action.

14. CFTC Staff did not request that the OSC issue an order under Section 17 of the OSA to disclose the Hamlin Transcript to Rivoire's counsel, and took the position that a Section 17 order was not required. Furthermore, CFTC Staff advised the Applicant that they intended to elicit deposition testimony from Hamlin concerning the Hamlin Examination and the Hamlin Transcript. Both the Hamlin Examination and Hamlin Transcript are subject to the confidentiality restrictions set out in section 16 of the OSA.

15. In March and April 2022, Hamlin's counsel requested guidance from OSC Staff as to whether answering questions concerning his prior testimony at the Hamlin Examination would be construed as a violation of the OSA. OSC Staff did not answer this question directly, but advised the Applicant that they did not believe it would be in the public interest to bring a proceeding against Hamlin for a breach of section 16 of the OSA in the circumstances. OSC Staff declined to provide further guidance and simply stated that Hamlin "may seek an order under subsection 17(1) of the [Ontario Securities] Act" and that, "if your client decides to bring a section 17 application, we expect that Staff would consent to an order permitting him to testify in the U.S. CFTC's proceeding."

16. Hamlin's deposition in the SDNY Action is currently scheduled for July 20, 2022.

17. As a current registrant who takes his obligations under Ontario securities laws seriously, Hamlin will not answer questions about his prior testimony during the Hamlin Examination without express authorization from the Commission to do so.

18. On June 15, 2022, the Applicant's US counsel provided CFTC Staff with a copy of his draft materials in support of this Application. On June 17, 2022, CFTC Staff advised Applicant's US counsel that CFTC Staff consented to the relief requested herein (though not to the factual or legal assertions set forth herein).

19. On June 17, 2022, Mr. Sheikh emailed a copy of the draft application materials to OSC Staff for their consent.

20. On June 29, 2022, OSC Staff contacted Mr. Sheikh in response to his request for their consent. Instead of providing their consent, OSC Staff asserted its view that a section 17 Order "may not be required in relation to at least some of the relief being sought by Mr. Hamlin". OSC Staff further indicated that they would respond to Hamlin's application "in the ordinary course" rather than provide advanced consent as previously suggested.

21. In subsequent correspondence with OSC Staff on June 29 and 30, 2022, OSC Staff provided no further meaningful insight as to their apparent change in position.

V. Legal Basis For Order Sought

22. Subsection 11(1) of the OSA empowers the Commission to issue an order appointing one or more persons to investigate a matter "for the due administration of Ontario securities law or the regulation of the capital markets in Ontario" and also "to assist in the due administration of the securities or derivatives laws or the regulation of the capital markets in another jurisdiction".

23. Section 13 of the OSA permits persons appointed under section 11 of the OSA to summons and compel a person to produce documents and/or provide testimony. That evidence is then protected by subsection 16(1)(b) of the OSA which provides that, except in accordance with section 17, no person shall disclose, except to his/her counsel:

...the name of any person examined or sought to be examined under section 13, any testimony given under section 13, any information obtained under section 13, the nature or content of any questions asked under section 13, the nature or content of any demands for the production of any document or other thing under section 13, or the fact that any document or other thing was produced under section 13.

24. Subsection 17(1) of the OSA empowers the Commission to authorize the disclosure of information protected by section 16 if such authorization is in the "public interest".

25. In this proceeding, the Applicant submits that it is in the public interest to authorize Hamlin to answer questions related to his prior evidence given at the Hamlin Examination (and in relation to any correspondence with OSC Staff and CFTC Staff concerning the Hamlin Examination that may be protected by section 16 or the Investigation Order) for a number of reasons, including:

a. it would allow Hamlin to provide full testimony under the Ontario Court Order and attend the deposition for the SDNY Action without being put in a position of breaching Ontario securities laws. Put simply, it is not in the public interest to put the Applicant in the position of being forced to choose between seeking a protective order from the SDNY Court enforcing the confidentiality restrictions of section 16 of the OSA and violating section 16 of the OSA by answering deposition questions about the Hamlin Examination in the presence of third-party counsel for Rivoire;

b. it would allow Hamlin to attend the deposition and, thus, give effect to the Letter of Request from the SDNY Court. It is in the public interest to facilitate cooperation with foreign courts where appropriate, taking into consideration principles of comity, public policy and sovereignty;

c. the Ontario Court Order sufficiently protects the interests of Hamlin by permitting him to rely on any rights contained within the Ontario and Canada Evidence Acts, the Charter of Rights and Freedoms, as well as the protections in the Stipulated Protective Order issued by Judge J. Paul Oetken of the SDNY Court dated July 30, 2020 (the "US Protective Order") and other protections under U.S. law. Under the Ontario Court Order, Hamlin may also assert any of the protections that would have otherwise been available to a party examined in a case pending in an Ontario court; and

d. CFTC Staff has consented to the relief sought in this application.

26. For all of these reasons, it is in the public interest for the Tribunal to grant the relief sought in this application.

27. Rules 12(1), 12(2) and 23 of the Capital Markets Tribunal Rules of Procedure and Forms.

28. Sections 11, 13, 16 and 17 of the OSA.

The Applicant intends to rely on the following evidence at the hearing:

29. The affidavit of Matthew Coogan sworn July 8, 2022;

30. Such further other evidence as counsel may advise and this Tribunal may permit.

DATED this 8th day of July, 2022

Citation: Gong (Re), 2022 ONCMT 29

Date: 2022-10-11

File No. 2022-14

Adjudicators: |

Russell Juriansz (chair of the panel) |

|

|

||

Timothy Moseley |

||

|

||

Sandra Blake |

||

|

||

Hearing: |

In writing |

|

|

||

Appearances: |

Alice Zhou |

For herself |

[1] Alice Zhou, a non-party to this proceeding, moved unsuccessfully for intervenor status. Upon seeing the decision dismissing her application, and the reasons for that decision, she brings this new application to keep the decision and reasons confidential. As we explain below, her application is improper, and we dismiss it summarily.

[2] On June 13, 2022, Staff of the Ontario Securities Commission filed a Statement of Allegations against the respondent Xiao Hua (Edward) Gong, alleging securities fraud and unregistered trading.

[3] On July 29, 2022, Zhou filed her motion seeking intervenor status in this proceeding. On October 5, 2022, following an oral hearing, we dismissed Zhou's motion.{1} Our decision and reasons were delivered to the parties and published by this Tribunal.

[4] The next day, Zhou brought this application under section 25.0.1 of the Statutory Powers Procedure Act{2}, asking that our order and the reasons not be disclosed to the public. She submits that the panel misunderstood her submissions and that the reasons, as drafted, may impact investors and other concerned parties.

[5] Zhou's current application is improper. Zhou's only ground is that she is dissatisfied with the hearing, decision and reasons on her intervenor motion.

[6] We cannot re-hear Zhou's motion for intervenor status. Zhou has other avenues available to her if she is dissatisfied with our decision, but asking us to keep that decision from the public is not one of them.

[7] We therefore dismiss her current application summarily, without the need to hear from the parties to the proceeding (i.e., Staff of the Ontario Securities Commission, and the respondent Gong).

Dated at Toronto this 11th day of October, 2022

{1} Gong (Re), 2022 ONCMT 27

{2} RSO 1990, c S.22

Aux Cayes Fintech Co. Ltd. -- ss. 127(1), 127.1

Citation: Aux Cayes Fintech Co Ltd (Re), 2022 ONCMT 30

Date: 2022-10-12

File No. 2021-29

Adjudicators: |

Timothy Moseley (chair of the panel) |

|

|

||

Russell Juriansz |

||

|

||

Sandra Blake |

||

|

||

Hearing: |

By videoconference, October 12, 2022 |

|

|

||

Appearances: |

Aaron Dantowitz |

For Staff of the Ontario Securities Commission |

|

||

Vincent Amartey |

||

|

||

Brad Moore |

For Aux Cayes Fintech Co. Ltd. |

|

|

||

Tina Cody |

||

The following reasons have been prepared for publication, based on the reasons delivered orally at the hearing, as edited and approved by the panel, to provide a public record of the oral reasons.

[1] Staff of the Ontario Securities Commission has alleged that Aux Cayes Fintech Co. Ltd. contravened the Securities Act{1} (the Act) by engaging in the business of trading in securities without the necessary registration or an applicable exemption from the registration requirement. Staff also alleges that Aux Cayes engaged in trades of securities that were distributions under the Act, without complying with or being exempt from the prospectus requirements.

[2] Staff and Aux Cayes seek approval of a settlement agreement they have entered into regarding these allegations. We conclude that it would be in the public interest to approve the settlement, for the following reasons.

[3] The factual background is set out in more detail in the settlement agreement, but we summarize the most important facts here.

[4] Aux Cayes operates an online crypto asset trading platform. Investors can open an account, and can trade in securities and derivatives based on exposure to underlying assets that include crypto assets. Whether the investor deposits crypto assets or uses fiat currency to purchase crypto assets, those assets are held in a wallet that Aux Cayes controls.

[5] The investors have neither possession of, nor control over, the crypto assets. Aux Cayes maintains custody. An investor who wants to take possession of their crypto assets must ask Aux Cayes for the assets and then transfer those assets to a wallet that the investor controls. What Aux Cayes actually provides to an investor is an instrument or contract involving crypto assets (e.g., crypto asset futures contracts, swap and options contracts), as opposed to the crypto assets themselves. Aux Cayes admits that these instruments or contracts are securities and derivatives.

[6] From the time that Aux Cayes launched its platform on October 1, 2017, to June 20, 2022, Aux Cayes opened more than 21,000 accounts for Ontario investors. Ontario investors deposited crypto assets into 1,534 of these accounts, from which Aux Cayes obtained revenue of approximately 514,950 US dollars. The remaining accounts received no deposits, and no trading was conducted in them.

[7] Canadian securities regulators, including the Ontario Securities Commission, have publicized their concerns about unregistered crypto asset trading platforms. The Commission issued a news release in March 2021 advising that those platforms must bring their operations into compliance with Ontario securities law or they may face regulatory action. The press release included a deadline of April 19, 2021, for such platforms to begin registration discussions.

[8] Aux Cayes did not contact the Commission by the deadline set out in that news release. In May 2021, the Commission took steps to inform Aux Cayes that it may be conducting registrable activity in Ontario. Aux Cayes responded to the Commission in June 2021 and advised that Aux Cayes would identify and close its Ontario accounts.

[9] Aux Cayes's misconduct was compounded by the fact that in later communications with the Commission, Aux Cayes made incorrect representations about what information was available regarding its Ontario accounts. Aux Cayes later corrected those misrepresentations.

[10] There are also mitigating factors. After being contacted by the Commission in May 2021, Aux Cayes took various steps aimed at limiting Ontario investors' access to their platform, including amending its Terms of Service to include Ontario in the list of restricted locations, and by adopting technology solutions to attempt to block Ontario investors.

[11] In addition, since late June 2022, Aux Cayes has maintained an open dialogue, expressed an interest in reaching a negotiated resolution and has provided all requested information promptly and in a transparent manner, making a disgorgement order possible. Aux Cayes is taking steps to explore the registration and compliance process with the Commission and has provided an undertaking to the Commission to restrict its business while it pursues registration and to leave Ontario in an orderly fashion if registration discussions terminate.

[12] The written undertaking provides, among other things, that until Aux Cayes either becomes registered or has wound down its operations, Aux Cayes will donate ongoing revenues from Ontario accounts to a payee named in the undertaking.

[13] Aux Cayes has admitted that its conduct breached the registration and prospectus requirements and that it thereby contravened ss. 25(1) and 53(1) of the Act. Staff and Aux Cayes have agreed that Aux Cayes will pay an administrative penalty of 600,000 Canadian dollars, will disgorge to the Commission the 514,950 US dollars that it obtained in the form of revenue, and will pay 25,000 Canadian dollars for costs of the Commission's investigation. Aux Cayes paid those amounts to the Commission before this hearing, and they are being held in escrow pending approval of the settlement.

[14] We have reviewed the settlement agreement in detail. In addition, we had the benefit of a confidential settlement conference with counsel for both parties.

[15] Our role at this settlement hearing is to determine whether the negotiated result falls within a range of reasonable outcomes, and whether it would be in the public interest to approve the settlement.

[16] We have considered Aux Cayes's failure to obtain registration and to comply with the prospectus requirements, both of which requirements are cornerstones of securities regulation in Ontario. We have also considered the aggravating and mitigating factors I have mentioned.

[17] This Tribunal respects the negotiation process and accords significant deference to the resolution reached by the parties. In our view, given all the circumstances, including the avoidance of significant resource consumption that would be required for a contested hearing, it is in the public interest for us to approve the settlement.

[18] We will therefore issue an order substantially in the form of the draft attached to the settlement agreement.

Dated at Toronto this 12th day of October, 2022

{1} RSO 1990, c S.5

OSC Staff Notice 81-733 -- Summary Report for Investment Fund and Structured Product Issuers

OSC Staff Notice 81-733 -- Summary Report for Investment Fund and Structured Product Issuers is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

October 19, 2022

Contents

Director's Message |

3 |

Part A: Introduction |

5 |

Responsibilities of the IFSP Branch |

5 |

Structure of the IFSP Branch |

6 |

Product Offerings Team |

6 |

Regulatory Policy Team |

7 |

Risk and Analytics Team |

7 |

Market Composition |

7 |

Part B: Operational Highlights |

10 |

I. Prospectus Filings |

10 |

Pre-File Process |

10 |

Data on Prospectus Reviews |

11 |

Novel Prospectus Filings |

12 |

ESG-Related Funds |

14 |

II. Exemptive Relief Applications |

14 |

Data on Exemptive Relief Applications |

15 |

Novel Exemptive Relief Applications |

16 |

III. Continuous Disclosure Reviews |

18 |

Summary of Completed Reviews |

18 |

Part C: Regulatory Policy |

23 |

Prohibition of Deferred Sales Charges |

23 |

Blanket Order Issued to Codify Permitted Means to Comply with the Trailer Ban |

|

for Order Execution Only (OEO) Dealers |

23 |

Reducing Regulatory Burden for Investment Fund Issuers |

24 |

Consolidate the Simplified Prospectus and the Annual Information Form |

24 |

Mandate each Reporting Issuer Investment Fund have a Designated Website |

24 |

Codify Exemptive Relief Granted in Respect of Notice-and-Access Applications |

25 |

Minimize Filings of Personal Information Forms |

25 |

Codify Exemptive Relief Granted in Respect of Conflicts Applications |

25 |

Broaden Pre-Approval Criteria for Investment Fund Mergers |

25 |

Repeal Regulatory Approval Requirements for a Change of Manager, a Change of Control of a Manager, and a Change of Custodian that Occurs in Connection with a Change of Manager |

26 |

Codify Exemptive Relief Granted in Respect of the Fund Facts Delivery Requirement and Corresponding Exemptions from the ETF Facts Delivery Requirement |

26 |

Proposed Modernization of the Prospectus Filing Model |

26 |

Blanket Relief for Proficiency Requirements to Distribute Alternative Mutual Funds |

27 |

Part D: Emerging Issues and Initiatives |

28 |

Environmental, Social and Governance Funds |

28 |

Investment Fund Survey |

28 |

Exchange Traded Funds |

29 |

Part E: Stakeholder Outreach |

31 |

IFSP Landing Page on OSC Website |

31 |

Launch of IFSP eNews |

31 |

Stakeholder Survey |

32 |

Investment Funds Technical Advisory Committee |

32 |

Staff Contact Information |

34 |

I am pleased to share this overview of the activities of the Investment Funds and Structured Products Branch (IFSP) of the Ontario Securities Commission (OSC) during this continuing period of unprecedented change and challenges. This Summary Report (Report) will cover the activities of IFSP during the 2021-2022 fiscal year.

The OSC is strongly committed to its mandate of investor protection. Investor profiles are diverse and wide-ranging, as are the investment fund products available today. More than ever, investors can benefit from competitive investment funds and product choices to meet their financial goals. We continue to facilitate investment fund offerings which provide different market and asset class exposure, objectives, and portfolio and risk management skills. Traditional and innovative products alike are reviewed to ensure that there is appropriate transparency to allow investors to make informed investment decisions. We enhanced consultation and communication with industry stakeholders to ensure emerging issues are managed to protect the interests of investors, while acknowledging and facilitating the innovation in the capital markets.

I am very proud of the accomplishments of IFSP during this fiscal year. I am even more proud of how IFSP worked collaboratively with stakeholders, recognizing different views, and embracing new skills and approaches, to accomplish our goals. I want to thank IFSP staff for their dedication and passion in their work.

Throughout the pandemic, the investment funds industry has continued to show its resilience and innovation. During the period of significant market volatility which occurred at the onset of the pandemic in March 2020, no public funds suspended redemptions and assets under management (AUM) were able to rebound over the course of several months. IFSP issued final prospectus receipts in connection with several novel investment funds, including those with exposure to crypto assets which were the first of their kind in the world. As we do with all novel products, IFSP is continuing to monitor developments in crypto asset funds closely.

Environmental, social and governance (ESG) funds are another emerging area which IFSP prioritized this year. OSC and IFSP staff have been extensively involved in domestic and international initiatives on disclosure practices related to ESG products and investor protection concerns. As a result of these initiatives, the Canadian Securities Administrators (CSA) published CSA Staff Notice 81-334 ESG-Related Investment Fund Disclosure. With this first milestone for ESG-specific regulation of investment funds in Canada, we are hopeful that this guidance will bring greater clarity to ESG-related fund disclosure and sales communications and enable investors to make more informed investment decisions about ESG products.

In the policy area, IFSP has continued to work on rule proposals and amendments that align with our commitment to burden reduction while maintaining investor protection. After years of consultation and collaboration, a series of amendments came into effect during the period which eliminate duplication, streamline regulatory processes, and codify frequently granted exemptions from certain requirements for investment fund issuers. Another notable achievement in the policy area is the ban on the deferred sales charge option which now harmonizes Ontario with the rest of the CSA.

Finally, IFSP is excited to be working with the new Digital Solutions Branch to use internal and external data to operationalize our oversight of larger market risks. Data obtained from the annual Investment Fund Survey will be a key input in developing a risk framework to help us identify higher risk issuers using key performance indicators.

We hope you find this Report helpful and informative. As always, if you have a question, comment, or would like to discuss regulatory matters, please reach out to us. Our Staff Contact Information has been included for your convenience.

This Report provides an overview of the key activities and initiatives of the IFSP Branch that impact investment fund and structured product issuers, and is organized into four broad areas:

1. Operational highlights

I. Prospectus filings

i) Pre-file process

ii) Data on prospectus filings

iii) Novel prospectus filings

iv) ESG-related funds

II. Exemptive relief applications

i) Data on exemptive relief applications

ii) Novel exemptive relief applications

III. Continuous disclosure reviews

i) Summary of completed reviews

2. Regulatory policy initiatives

3. Emerging issues and initiatives

4. Stakeholder outreach

These activities were conducted within the scope of IFSP's responsibilities and structure which are briefly described below, along with market composition data to provide context on the scale of the industry.

Responsibilities of the IFSP Branch

The OSC's mandate is to protect investors from unfair, improper or fraudulent practices, to foster fair, efficient and competitive capital markets and confidence in the capital markets, to foster capital formation, and to contribute to the stability of the financial system and the reduction of systemic risk.

In support of the OSC's mandate, the IFSP Branch is responsible for administering the regulatory framework for investment funds and structured products, including linked notes and scholarship plans, that are sold to Ontario investors. Ontario-based publicly offered investment funds account for over 80% of the approximately $2.39 trillion in publicly offered investment fund assets in Canada which are comprised of conventional mutual funds, non-redeemable investment funds, exchange traded funds (ETFs), and alternative mutual funds.

Our key functions include

• reviewing and assessing product disclosure for all types of investment funds,

• considering applications for discretionary relief from securities legislation,

• developing new rules and policies to adapt to changes in the investment funds industry,

• using data sources to identify and monitor risks, and

• monitoring and participating in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO).

Structure of the IFSP Branch

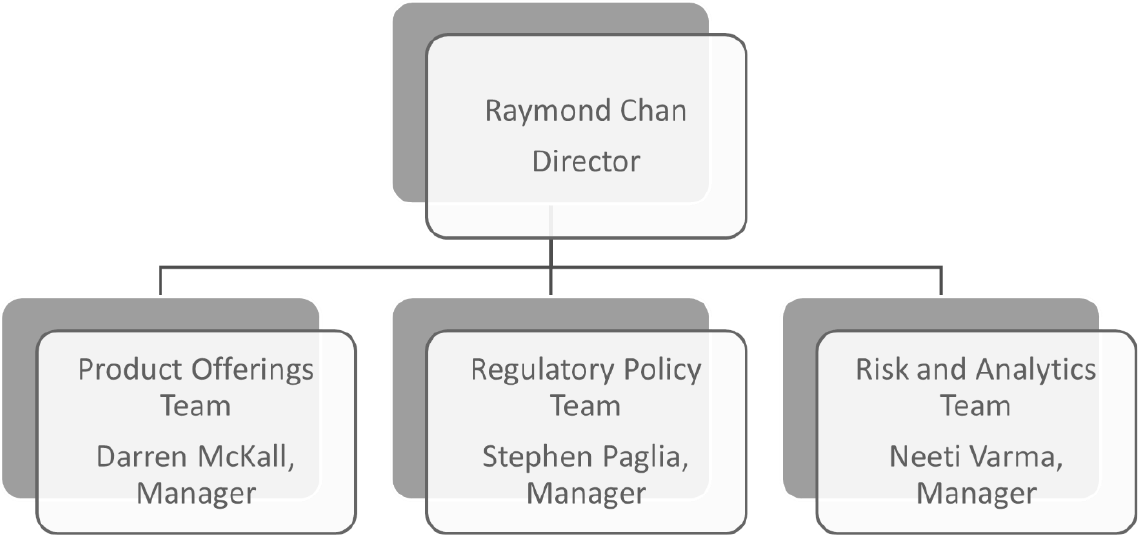

In 2020, the IFSP Branch was reorganized from one operational group into three dedicated teams with the objective of streamlining and improving processes and proactively assessing and monitoring risks. Each team has its own Manager and staff which may include lawyers, accountants, a financial examiner, review officers, a business and market analyst and administrative assistants. The new structure is presented below:

Product Offerings Team

The Product Offerings team is responsible for reviewing all investment fund and structured note product filings. By streamlining the review of prospectuses and applications onto one team, the IFSP Branch is building efficiencies and identifying redundancies to improve the filings process while developing product offering expertise. On novel filings, members of the team interact directly with the CSA Investment Funds Operations Committee to brief and resolve any issues raised.

The OSC currently has a Service Commitment document on its website that sets out stakeholder expectations and service standards. The IFSP Branch is committed to ensuring that services are delivered efficiently and effectively, and in accordance with those standards. The service standards include timelines for prospectus filings and amendments, and the review of exemptive relief applications.

Regulatory Policy Team