Ontario Securities Commission Bulletin

Issue 44/47 - November 25, 2021

Ont. Sec. Bull. Issue 44/47

• OSC Staff Notice 51-732 -- Corporate Finance Branch 2021 Annual Report

• Minister of Finance -- Notice of Request Made under Subsection 143.7(1) of the Securities Act

• Fidelity Advantage Bitcoin ETF et al.

• 1317774 B.C. Ltd. and Penn National Gaming, Inc.

• Canada Jetlines Operations Ltd.

• CI Investments Inc. and The Funds

• TSX Inc.

• Fidelity Investments Canada ULC and the Funds

• Convergence Blended Finance, Inc.

• Dynamic Active Canadian Dividend ETF et al.

• Horizons ETFs Management (Canada) Inc. and Horizons Morningstar Hedge Fund Index ETF

• Fidelity Investments Canada ULC and Fidelity Advantage Bitcoin ETFTM

• First Global Data Ltd. et al.

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Toronto Stock Exchange -- TSX Company Manual -- Notice of Housekeeping Rule Amendments

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Notice of Memorandum of Understanding with the Croatian Financial Services Supervisory Agency Concerning Consultation, Cooperation and the Exchange of Information Related to the Supervision of Cross-Border Alternative Investment Fund Managers

November 25, 2021

The Ontario Securities Commission, together with the Autorité des marchés financiers, Alberta Securities Commission and British Columbia Securities Commission (the "Canadian Authorities"), recently entered into a supervisory Memorandum of Understanding (the "Supervisory MOU") concerning consultation, cooperation and the exchange of information related to the supervision of managers of alternative investment funds with the Croatian Financial Services Supervisory Agency ("Hanfa").

The Canadian Authorities entered into similar supervisory MOUs with other European Union and European Economic Area member state financial securities regulators in 2013. The entering into of such supervisory MOUs was a pre-condition under the EU Alternative Investment Fund Managers Directive ("AIFMD") for allowing non-EU Alternative Investment Fund Managers ("AIFMs") to manage and market Alternative Investment Funds ("AIFs") in the EU and to perform fund management activities on behalf of EU Managers. Under the AIFMD, AIFMs are legal persons whose regular business is the risk and/or portfolio management of AIFs and AIFs are collective investment undertakings other than those that comply with the EU Undertakings for Collective Investment in Transferable Securities Directive.

The purpose of the Supervisory MOU is to facilitate consultation, cooperation and the exchange of information related to the supervision of AIFMs that operate on a cross-border basis in the jurisdictions of both Hanfa and the relevant Canadian Authority.

The Supervisory MOU is subject to the approval of the Minister of Finance and was delivered to the Minister of Finance on November 19, 2021.

Questions may be referred to:

Cindy WanManager, Global AffairsGlobal and Domestic Affairs416-263-7667cwan@osc.gov.on.caConor BreslinAdvisorGlobal and Domestic Affairs416-593-8112cbreslin@osc.gov.on.ca

In view of the growing globalization of the world's financial markets and the increase in cross-border operations and activities of Managers of alternative investment funds, the Ontario Securities Commission, the Autorité des marchés financiers (Québec), the Alberta Securities Commission and the British Columbia Securities Commission on one side, and Croatian Financial Services Supervisory Agency (Croatia) on the other side have reached this Memorandum of Understanding (MoU) regarding mutual assistance in the supervision and oversight of Managers of Covered Funds, and their delegates and depositaries that operate on a cross-border basis in the jurisdictions of the signatories of this MoU. The authorities express, through this MoU, their willingness to cooperate with each other in the interest of fulfilling their respective regulatory mandates, particularly in the areas of investor protection, fostering market and financial integrity, and maintaining confidence and systemic stability. The authorities also express through this MoU, their desire to provide one another with the fullest mutual assistance possible to facilitate the performance of the functions with which they are entrusted within their respective jurisdictions to secure compliance with their laws and regulations.

This MoU is a bilateral arrangement between each Canadian Authority and each EU Authority and should not be considered a bilateral arrangement between each Canadian Authority.

For the purpose of this MoU:

a) "Authority" means:

i. An EU Authority (including the EEA authorities listed above) or any successor, or any other EU authority which may become a party to this MoU in the manner set out in Article 9; or

ii. The Autorité des marchés financiers (Québec) (AMF), the Ontario Securities Commission (OSC), the Alberta Securities Commission (ASC), the British Columbia Securities Commission (BCSC), or any other Canadian securities regulatory authority which may become a party to this MoU in the manner set out in Article 9 (individually a Canadian Authority, or collectively the Canadian Authorities).

b) "Requested Authority" means:

i. Where the Requesting Authority is an EU Authority, the Canadian Authority to which a request is made under this MoU; or

ii. Where the Requesting Authority is a Canadian Authority, the EU Authority to which a request is made under this MoU.

c) "Requesting Authority" means the Authority making a request under this MoU.

d) "EU competent authority": means any authority appointed in an EU or an European Economic Area (EEA) Member State in accordance with Article 44 of the AIFMD for the supervision of Managers, delegates, depositaries and, where applicable, Covered Funds.{1}

e) "AIFMD" means the Directive 2011/61/EU of the European Parliament and of the Council of 8 June 2011 on Alternative Investment Fund Managers and amending Directives 2003/41/EC and 2009/65/EC and Regulations (EC) No 1060/2009 and (EU) No 1095/2010.

f) "Manager" means a legal person whose regular business is managing one or more Covered Funds in accordance with the AIFMD or a person or company that acts as an adviser or as an investment fund manager, as those terms are defined by the Securities Act of the relevant Canadian Authority, to one or more Covered Funds. For clarity, an "EU Manager" means a Manager that is established in an EU member state and a "Canadian Manager" means a Manager that is registered in one or more jurisdictions of a Canadian Authority.

g) "Covered Fund" means a collective investment undertaking, including investment compartments thereof, which: (i) raises capital from a number of investors, with a view to investing it in accordance with a defined investment policy for the benefit of those investors; and (ii) is not a UCITS. For clarity, an "EU Covered Fund" means a Covered Fund that is domiciled in an EU member state and a "Canadian Covered Fund" means a Covered Fund that is domiciled in one or more jurisdictions of a Canadian Authority.

h) "UCITS" means an undertaking for collective investment in transferable securities authorised in accordance with Article 5 of Directive 2009/65/EC.

i) "Delegate" means an entity to which a Manager delegates the tasks of carrying out the portfolio management or risk management of one or more Covered Funds under its management.

j) "Depositary" means an entity appointed to perform the depositary functions of a Covered Fund.

k) "Operate(s) on a cross-border basis" includes the following situations:

i. EU Managers managing Canadian Covered Funds,

ii. EU Managers marketing Canadian Covered Funds in an EU Member State,

iii. EU Managers marketing Canadian and/or non-Canadian Covered Funds in Canada,

iv. Canadian Managers marketing EU Covered Funds and/or non-EU Covered Funds, including Canadian Covered Funds, in an EU Member State,

v. EU Managers marketing Canadian Covered Funds in the EU with a passport,

vi. Canadian Managers managing EU Covered Funds,

vii. Canadian Managers marketing EU Covered Funds in the EU with a passport,

viii. Canadian Managers marketing non-EU Covered Funds in the EU with a passport,

ix. Non-EU Managers marketing Canadian Covered Funds in the EU with a passport,

x. Non-Canadian managers marketing EU Covered Funds in Canada

l) Insofar as there is a link to the activity of the Managers and the Covered Funds, the MoU also covers delegates and depositaries as defined in letters i) and j) of this Article. "Covered Entity" means a Manager that operates on a cross border basis, a Covered Fund, where applicable, and, insofar as there is a link to the Manager and the Covered Fund, delegates and depositaries as defined in letters i) and j) of this Article, including the persons employed by such entities, provided that these entities are subject to the regulatory authority of an EU Authority or a Canadian Authority, as applicable.

m) "Cross-border on-site visit" means any regulatory visit by one Authority to the premises of a Covered Entity located in the other Authority's jurisdiction, for the purposes of on-going supervision.

n) "Governmental Entity" means:

i. Those Ministries of Finance, Central Banks and other national prudential authorities listed in Appendix A, if the Requesting Authority is an EU Authority;

ii. The Bank of Canada or the Office of the Superintendent of Financial Institutions of Canada, if the Requesting Authority is the ASC, BCSC or OSC;

iii. The Alberta Ministry of Treasury Board and Finance, if the Requesting Authority is the ASC;

iv. The British Columbia Ministry of Finance, if the Requesting Authority is the BCSC;

v. The Ontario Ministry of Finance, if the Requesting Authority is the OSC;

vi. The Québec ministère des Finances, if the Requesting Authority is the AMF; and

vii. Such other entity, as agreed to by the signatories, as may be responsible for any other Canadian Authority which may become a party to this MoU in the manner set out in Article 9.

o) "Local Authority" means the Authority in whose jurisdiction a Covered Entity is physically located.

p) "Emergency Situation" means:

i. In the EU, the occurrence of an event that could materially impair the financial or operational condition of a Covered Entity, investors or the markets, independently from a decision of the European Council within the meaning of Article 18 of the ESMA Regulation (Regulation 1095/2010/EU); and

ii. In Canada, the occurrence of an event that could materially impair the financial or operational condition of a Covered Entity, investors or the markets

q) "ESMA" means the European Securities and Markets Authority established by Regulation (EU) No 1095/2010 of the European Parliament and of the Council, of 24 November 2010 establishing a European Supervisory Authority (European Securities and Markets Authority).

r) "ESRB" means the European Systemic Risk Board established by Regulation (EU) No 1092/2010 of the European Parliament and of the Council of 24 November 2010 on European Union macro-prudential oversight of the financial system and establishing a European Systemic Risk Board.

1) This MoU is a statement of intent to consult, cooperate and exchange information in connection with the supervision and oversight of Covered Entities that operate on a cross-border basis in the jurisdictions of the signatories, in a manner consistent with, and permitted by, the laws, regulations and requirements that govern the Authorities. This MoU provides for consultation, cooperation and exchange of information related to the supervision and oversight of Covered Entities between each EU Authority and each Canadian Authority individually. The Authorities anticipate that cooperation will be primarily achieved through on-going, informal, oral consultations, supplemented by more in-depth, ad hoc cooperation. The provisions of this MoU are intended to support such informal and oral communication as well as to facilitate the written exchange of non-public information where necessary.

2) This MoU does not create any legally binding obligations, confer any rights, or supersede domestic laws and regulations. This MoU does not confer upon any person the right or ability directly or indirectly to obtain, suppress, or exclude any information or to challenge the execution of a request for assistance under this MoU.

3) This MoU does not intend to limit an Authority to taking solely those measures described herein in fulfilment of its supervisory or oversight functions. In particular, this MoU does not affect any right of any Authority to communicate with, or obtain information or documents from, any person or Covered Entity subject to its jurisdiction that is established in the territory of the other Authority.

4) This MoU complements, but does not alter the terms and conditions of the IOSCO Multilateral Memorandum of Understanding Concerning Consultation and Cooperation and the Exchange of Information (the "IOSCO MMoU"), to which the Authorities are signatories, which also covers information-sharing in the context of enforcement investigations; and any of the existing arrangements concerning cooperation in securities matters between the signatories.

5) The Authorities will, within the framework of this MoU, provide one another with the fullest cooperation permissible under the law in relation to the supervision and oversight of Covered Entities. Following consultation, cooperation may be denied:

a) Where the cooperation would require an Authority to act in a manner that would violate domestic law;

b) Where a request for assistance is not made in accordance with the terms of the MoU; or

c) On the grounds of the public interest.

6) No domestic banking secrecy, blocking laws or regulations should prevent an Authority from providing assistance to other Authority.

7) The Authorities will periodically review the functioning and effectiveness of the cooperation arrangements between the Authorities with a view, inter alia, to expanding or altering the scope or operation of this MoU should that be judged necessary.

8) To facilitate cooperation under this MoU, the Authorities hereby designate contact persons as set forth in Appendix B.

1) The Authorities recognize the importance of close communication concerning Covered Entities, and intend to consult at the staff level where appropriate regarding: (i) general supervisory issues, including with respect to regulatory, oversight or other program developments; (ii) issues relevant to the operations, activities, and regulation of Covered Entities; and (iii) any other areas of mutual supervisory interest.

2) Cooperation will be most useful in, but is not limited to, the following circumstances where issues of regulatory concern may arise:

a) The initial application with an Authority for authorization, designation, recognition, qualification, registration or exemption therefrom by a Covered Entity that is authorized, designated, recognized, qualified or registered by an Authority in another jurisdiction;

b) The on-going oversight of a Covered Entity; or

c) Regulatory approvals or supervisory actions taken in relation to a Covered Entity by one Authority that may impact the operations of the entity in the other jurisdiction.

3) Notification. Each Authority will, where such information is known and accessible to the Authority, inform the other Authority as soon as practicable of

a) Any known material event that could have a significant adverse impact on a Covered Entity; and

b) Enforcement or regulatory actions or sanctions, including the revocation, suspension or modification of relevant licenses or registration, concerning or related to a Covered Entity which may have, in its reasonable opinion, material effect on the Covered Entity.

4) Exchange of Information. To supplement informal consultations, each Authority intends to provide the other Authority, upon written request, with assistance in obtaining information accessible to the Requested Authority and not otherwise available to the Requesting Authority, and, where needed, interpreting such information so as to assist the Requesting Authority to assess compliance with its laws and regulations. The information covered by this paragraph includes, without limitation, information such as:

a) Information that would assist the Requesting Authority to verify that the Covered Entities covered by this MoU comply with the relevant obligations and requirements of the laws and regulations of the Requesting Authority;

b) Information relevant for monitoring and responding to the potential implications of the activities of an individual Manager, or Managers collectively, for the stability of systemically relevant financial institutions and the orderly functioning of markets in which Managers are active;

c) Information relevant to the financial and operational condition of a Covered Entity, including, for example, reports of capital reserves, liquidity or other prudential measures, and internal controls procedures;

d) Relevant regulatory information and filings that a Covered Entity is required to submit to an Authority including, for example: interim and annual financial statements and early warning notices; and

e) Regulatory reports prepared by an Authority, including for example: examination reports, findings, or information drawn from such reports regarding Covered Entities.

1) Authorities should discuss and reach understanding on the terms regarding cross-border on-site visits, taking into full account each other's sovereignty, legal framework and statutory obligations, in particular, in determining the respective roles and responsibilities of the Authorities. The Authorities will act in accordance with the following procedure before conducting a cross-border on-site visit.

a) The Authorities will consult with a view to reaching an understanding on the intended timeframe for and scope of any cross-border on-site visit. The Local Authority shall decide whether the visiting officials shall be accompanied by its officials during the visit.

b) When establishing the scope of any proposed visit, the Authority seeking to conduct the visit will give due and full consideration to the supervisory activities of the other Authority and any information that was made available or is capable of being made available by that Authority.

c) The Authorities intend to assist each other in obtaining, reviewing, and interpreting the contents of public and non-public documents and obtaining information from directors and senior management of Covered Entities.

1) To the extent possible, a request for written information pursuant to Article 3(4) should be made in writing, and addressed to the relevant contact person identified in Appendix B. A request generally should specify the following:

a) The information sought by the Requesting Authority, including specific questions to be asked and an indication of any sensitivity about the request;

b) A concise description of the facts underlying the request and the supervisory purpose for which the information is sought, including the applicable regulations and relevant provisions behind the supervisory activity; and

c) The desired time period for reply and, where appropriate, the urgency thereof.

2) In Emergency Situations, the Authorities will endeavour to notify each other of the Emergency Situation and communicate information to the other as would be appropriate in the particular circumstances, taking into account all relevant factors, including the status of efforts to address the Emergency Situation. During Emergency Situations, requests for information may be made in any form, including orally, provided such communication is confirmed in writing as promptly as possible following such notification.

1) The Requesting Authority may use non-public information obtained under this MoU solely for the purpose of supervising Covered Entities and seeking to ensure compliance with the laws or regulations of the Requesting Authority, including assessing and identifying systemic risk in the financial markets or the risk of disorderly markets.

2) This MoU is intended to complement, but does not alter the terms and conditions of the existing arrangements between Authorities concerning cooperation in securities matters, including the IOSCO MMoU. The Authorities recognize that while information is not to be gathered under this MoU for enforcement purposes, subsequently the Authorities may want to use the information for law enforcement purposes. In such cases, further use of the information should be governed by the terms and conditions of the IOSCO MMoU.

1) Except for disclosures in accordance with this MoU, including permissible uses of information under Article 7, each Authority will keep confidential to the extent permitted by law information shared under this MoU, requests made under this MoU, the contents of such requests, and any other matters arising under this MoU. The terms of this MoU are not confidential.

2) To the extent legally permissible, the Requesting Authority will notify the Requested Authority of any legally enforceable demand from a third party for non-public information that has been furnished under this MoU. Prior to compliance with the demand, the Requesting Authority intends to assert all appropriate legal exemptions or privileges with respect to such information as may be available.

3) In certain circumstances, and as required by law, it may become necessary for the Requesting Authority to share information obtained under this MoU with other Governmental Entities in its jurisdiction. In these circumstances and to the extent permitted by law:

a) The Requesting Authority will notify the Requested Authority.

b) Prior to passing on the information, the Requested Authority will receive adequate assurances concerning the Governmental Entity's use and confidential treatment of the information, including, as necessary, assurances that the information will not be shared with other parties without getting the prior consent of the Requested Authority.

4) Except as provided in paragraphs 2 and 6, the Requesting Authority must obtain the prior consent of the Requested Authority before disclosing non-public information received under this MoU to any other party. If consent is not obtained from the Requested Authority, the Authorities will discuss the reasons for withholding approval of such use and the circumstances, if any, under which the intended use by the Requesting Authority might be allowed.

5) The Authorities intend that the sharing or disclosure of non-public information, including but not limited to deliberative and consultative materials, pursuant to the terms of this MoU, will not constitute a waiver of privilege or confidentiality of such information.

6) Onward sharing of information between signatories of this MoU, ESMA and the ESRB shall be permitted in the following circumstances:

a) In accordance with Article 25(2) of the AIFMD, an EU Authority may need to share information received from a non-EU authority with other EU Authorities where a Manager under its responsibility or a Covered Fund managed by that Manager could potentially constitute an important source of counterparty risk to a credit institution or other systemically relevant institutions in other EU Member States.

b) In accordance with Article 50(4) of the AIFMD, the EU Authority of the Member State of reference of a non-EU Manager shall forward the information received from non-EU authorities in relation to that non-EU Manager to the EU Authority of the host Member States, as defined in Article 4(1)(r) of the AIFMD.

c) In accordance with Article 53 of the AIFMD, an EU Authority shall communicate information to other EU Authorities, the ESMA and the ESRB where this is relevant for monitoring and responding to the potential implications of the activities of individual Manager or Managers collectively for the stability of systemically relevant financial institutions and the orderly functioning of markets on which the Managers are active.

7) For purposes of Article 8(6), the EU Authority, ESMA or the ESRB, as applicable will provide written notification to the relevant Canadian Authority at the time of sharing non-public information with another EU Authority. ESMA or the ESRB, as applicable. The written notification will specify the EU Authority, or ESMA or the ESRB, as applicable, with which the non-public information is shared, and the reason for sharing such information.

8) Restrictions in this MoU with respect to the use and confidential treatment of non-public information continue to apply to any non-public information shared, pursuant to this Article, by an EU Authority with another EU Authority, ESMA or the ESRB.

9) The Authorities acknowledge that no transfer of personal data under this MoU will take place in the usual course of business or practice, unless the jurisdiction of the relevant Canadian Authority is recognised by the European Commission as ensuring an adequate level of protection of personal data, or unless the relevant Authorities who need to transfer personal data under this MoU are signatories to the administrative arrangement for the transfer of personal data between each of the EEA Authorities and each of the non-EEA Authorities ("AA").{2}

1) The Authorities will periodically review the functioning and effectiveness of the cooperation arrangements between the EU Authorities and the Canadian Authorities with a view, inter alia, to expanding the scope or operation of this MoU should that be judged necessary.

2) The EU Authority shall notify the Canadian Authorities of any change or modification to its laws, regulations and requirements with respect to the protection of non-public information, and shall explain the consequences of the change or modification on the protection of non-public information in the context of the MoU. If the Canadian Authority is of the view that the change or modification results in lesser protection for non-public information than provided for under the laws, regulations and requirements of the Canadian Authority, the MoU shall be terminated between the authorities concerned and the provisions in Article 8(4) shall apply.

3) Any Canadian authority may become a party to the MoU by executing a counterpart hereof together with the EU Authorities and providing notice of such execution to the other Canadian Authorities that are signatories to this MoU.

4) Any EU authority or EU competent authority may become a party to the MoU by executing a counterpart hereof together with the Canadian Authorities and providing notice of such execution to the other EU Authorities that are signatories to this MoU.

1) If a signatory wishes to terminate the MoU, it shall give written notice to the counterparty. ESMA would coordinate the action of EU authorities in this regard. Cooperation in accordance with this MoU will continue until the expiration of 30 days after an Authority gives written notice to the others. If either Authority gives such notice, cooperation will continue with respect to all requests for assistance that were made under the MoU before the effective date of notification until the Requesting Authority terminates the matter for which assistance was requested. In the event of termination of this MoU, information obtained under this MoU will continue to be treated in a manner prescribed under Article 7 to 9.

2) Where the relevant functions of a signatory to this MoU are transferred or assigned to another authority or authorities, the terms of this MoU shall apply to the successor authority or authorities performing those relevant functions without the need for any further amendment to this MoU or for the successor to become a signatory to the MoU. This shall not affect the right of the successor authority and its counterparty to terminate the MoU as provided hereunder if it wishes to do so.

This MoU enters into force at the date of signature, and in the case of the OSC, on the date determined in accordance with the applicable legislation.

Ante [ZCARON]igman |

D. Grant Vingoe |

President of the Board |

Chair and Chief Executive Officer |

Croatian Financial Services Supervisory Agency |

Ontario Securities Commission |

Date of signature: November 17, 2021 |

Date of signature: November 17, 2021 |

Louis Morisset |

Stan Magidson |

President and Chief Executive Officer |

Chair and Chief Executive Officer |

Autorité des marchés financiers (Québec) |

Alberta Securities Commission |

Date of signature: November 17, 2021 |

Date of signature: November 17, 2021 |

Brenda Leong |

|

Chair and Chief Executive Officer |

|

British Columbia Securities Commission |

|

Date of signature: November 18, 2021 |

|

{1} Some EU Member States have more than one competent authority designated to carry out the duties provided under the AIFMD.

{2} Hanfa signed the AA on 10 April 2019, AMF on 30 April 2019, OSC on 10 May 2019 and ASC on 15 October 2019. More information regarding the AA is available on the IOSCO website page: https://www.iosco.org/about/?subsection=administrative_arrangement.

None

Croatian Financial Services Supervisory Agency |

Anamarija Stanicic |

Head of Division |

|

Regulatory Harmonisation and International Cooperation Division |

|

Croatian Financial Services Supervisory Agency |

|

Franje Rackoga 6, 10 000 Zagreb |

|

E-mail: <<anamarija.stanicic@hanfa.hr>> |

|

Ontario Securities Commission |

Director |

Global and Domestic Affairs Branch |

|

Ontario Securities Commission |

|

20 Queen Street West, 20th Floor |

|

Toronto, ON M5H 3S8 |

|

E-mail: <<inquiries@osc.gov.on.ca>> |

|

Autorité des marchés financiers (Québec) |

Me Philippe Lebel |

Corporate Secretary and Executive Director, Legal Affairs |

|

Place de la Cité, tour Cominar |

|

2640, boulevard Laurier, bureau 400 |

|

Québec (Québec) G1V 5C1 |

|

Canada |

|

Email: <<secretariat@lautorite.qc.ca>> |

|

+ 1 418.525.0337 |

|

Alberta Securities Commission |

Samir Sabharwal |

General Counsel |

|

Alberta Securities Commission |

|

Suite 600, 250-5th Street SW |

|

Calgary, AB T2P 0R4 |

|

Email: <<Samir.Sabharwal@asc.ca>> |

|

British Columbia Securities Commission |

Secretary to the Commission |

P.O. Box 10142, Pacific Centre |

|

701 West Georgia |

|

Vancouver, BC V7Y 1L2 |

|

Canada |

|

Email: <<commsec@bcsc.bc.ca>> |

|

+ 1 604 899 6533 |

|

OSC Staff Notice 51-732 -- Corporate Finance Branch 2021 Annual Report

OSC Staff Notice 51-732 -- Corporate Finance Branch 2021 Annual Report is reproduced on the following separately numbered pages. Bulletin pagination resumes at the end of the Report.

Corporate Finance Branch

2021 Annual Report

November 25, 2021

I am pleased to share our annual Report which provides an overview of the Branch's operational and policy work for Fiscal 2021 and shares timely guidance for Issuers and advisors about our expectations and our interpretation of regulatory requirements in certain areas.

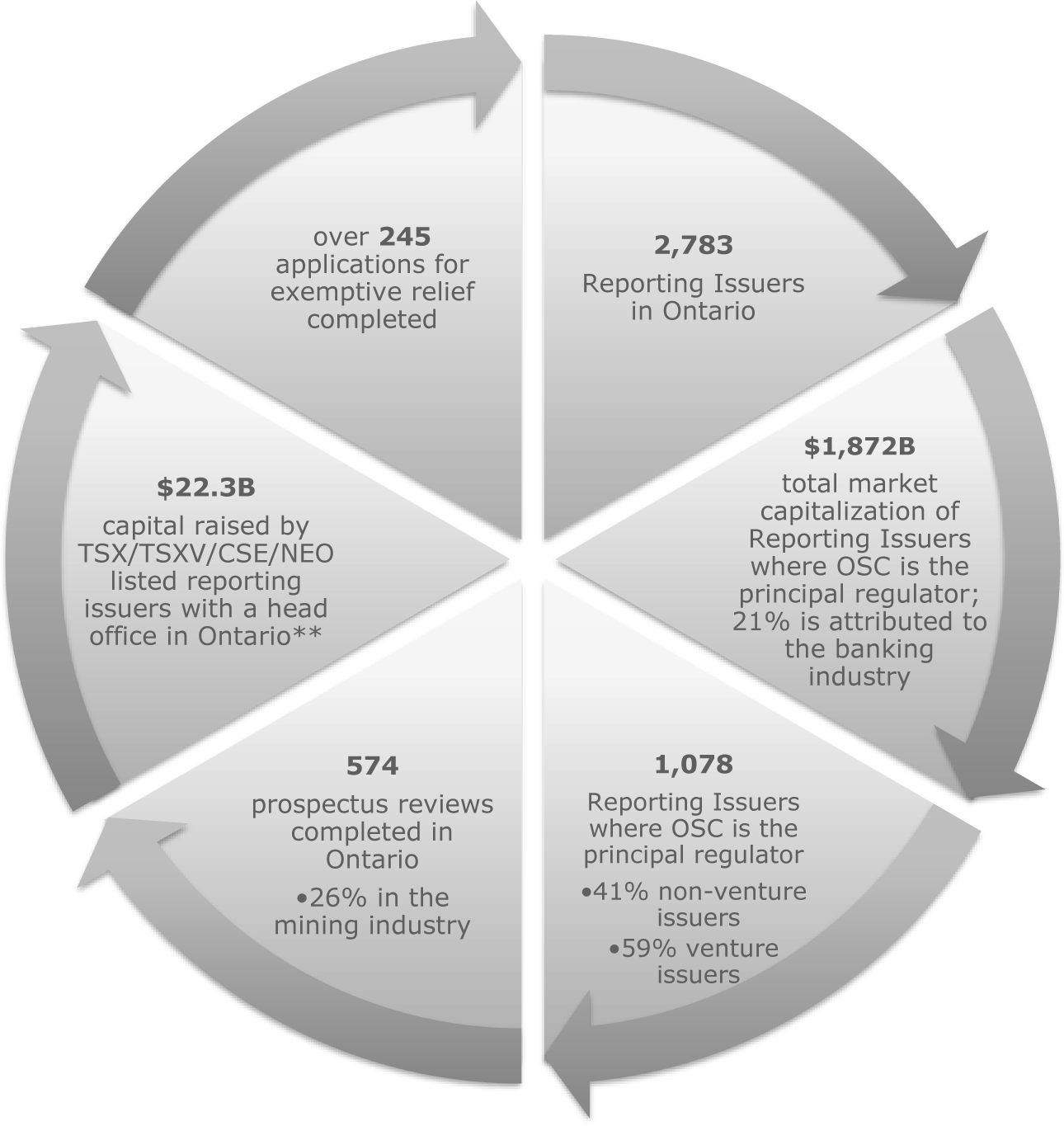

Capital raising in Ontario continued to grow at a remarkable pace in Fiscal 2021, leading to a record number of prospectus filings; over 574 prospectuses filed in Ontario were completed, representing a near 50% increase over the comparable Fiscal 2020, and more than our Branch has seen in over a decade. The high level of prospectus filings has continued into the current fiscal year. Despite these large volumes, Staff effectively processed files in a timely manner, focusing on material disclosure or public interest concerns. Further, we issued best practice guidance in January to assist Issuers in capital raising efforts.

The continued high demand for liquidity underscores the impact of low interest rates and new records in equity market performance in the midst of the continuing COVID-19 pandemic. Our goal continues to be to provide balanced, tailored, flexible and responsive regulation to carry out the OSC's broad mandate. With this at the forefront, the Branch also supported Reporting Issuers through several measures including a multi-pronged approach of financial statement filing extensions, late filing fee waivers and hosting an OSC virtual webinar on disclosure expectations with access to OSC staff for real time questions. To assist Reporting Issuers in meeting their continuous disclosure obligations, we also conducted a comprehensive review of their COVID-19 disclosure and published guidance on our disclosure expectations. We continue to monitor the impacts and challenges of the pandemic on the capital markets and will respond accordingly.

In addition to the significant increase in our operational work, we continue to prioritize and make progress on several new and existing policy projects, as highlighted in this Report. This includes a number of key policy milestones subsequent to Fiscal 2021, such as, the publication of the proposed changes to the CD requirements to streamline and clarify annual and interim filings, publication of proposed climate-related disclosure requirements, as well as key considerations around broader diversity. Further, throughout Fiscal 2021, the Branch, with its CSA partners, continued work on several policy initiatives designed to reduce regulatory burden which are outlined in our Report and will continue to be part of the Branch's main policy focus in the fiscal year ended March 31, 2022.

Engagement with our stakeholders remains a critical component of our work. As in previous years, we welcome any questions or feedback that you may have.

Lastly, I want to thank Staff for their continued dedicated support, flexibility and professionalism in carrying out our regulatory role during a time of increased operational activity and uncertainty in the capital markets.

Kind regards,

Table of Contents

GLOSSARY |

6 |

FISCAL 2021 SNAPSHOT |

8 |

INTRODUCTION |

9 |

ONTARIO SECURITIES COMMISSION |

9 |

CORPORATE FINANCE BRANCH: WHO WE ARE & WHAT WE DO |

10 |

Part A: Compliance |

11 |

1. CONTINUOUS DISCLOSURE REVIEW (CDR) PROGRAM |

12 |

A) Overview |

13 |

I) Objectives of the CDR program |

13 |

II) Types of CD reviews |

14 |

B) CDR program outcomes for Fiscal 2021 |

15 |

I) Management's discussion & analysis |

17 |

II) COVID-19 disclosure |

21 |

III) Mining disclosure |

21 |

IV) Non-GAAP financial measures |

23 |

V) Diversity on boards and in executive officer positions |

24 |

VI) Cease Trade Order -- Content Deficiency |

25 |

2. PUBLIC OFFERINGS |

26 |

60) Trends and guidance |

26 |

I) Primary business in an IPO |

27 |

II) Timing for inclusion of financial statements in an IPO venture issuer's prospectus |

28 |

III) Description of business |

28 |

IV) Forward-Looking Information |

29 |

V) Disclosure improvements |

31 |

VI) Sufficiency of proceeds and financial condition of an Issuer |

33 |

VII) Filing of non-offering prospectus for a qualifying transaction when there are operations in emerging markets |

35 |

VIII) Auditor's review of financial statements |

35 |

IX) Audit committees |

36 |

X) Post-receipt pricing prospectuses |

36 |

XI) Confidential prospectus pre-file review |

37 |

XII) Special purpose acquisition corporations |

39 |

XIII) Concurrent filing of a base shelf prospectus and prospectus supplement |

40 |

XIV) Use of business combination exemption |

41 |

XV) Industry specific |

41 |

XVI) Distributions out |

44 |

3. EXEMPTIVE RELIEF APPLICATIONS |

45 |

A) Trends and guidance |

45 |

I) Start-up crowdfunding |

46 |

II) RTO transactions -- relief from financial statements |

46 |

III) At-will financing/equity lines |

47 |

4. INSIDER REPORTING |

48 |

5. OUR SERVICE COMMITMENTS |

49 |

6. ADMINISTRATIVE MATTERS |

50 |

A) Participation fee form |

50 |

B) Refiling of CD documents |

51 |

C) Making documents private on SEDAR |

51 |

D) Reports of Exemption Distribution |

52 |

Part B: Responsive Regulation |

54 |

1. CONTINUOUS DISCLOSURE REQUIREMENTS |

55 |

2. PROSPECTUS GUIDANCE |

55 |

3. BUSINESS ACQUISITION REPORT |

56 |

4. LISTED ISSUER FINANCING EXEMPTION |

56 |

5. SYNDICATED MORTGAGES |

57 |

6. ENVIRONMENTAL, SOCIAL AND CORPORATE GOVERNANCE |

58 |

7. CRYPTOCURRENCY |

59 |

8. BENCHMARKS |

59 |

9. DESIGNATED RATING ORGANIZATIONS |

60 |

KEY STAFF NOTICES |

62 |

STAFF CONTACT INFORMATION |

65 |

The following terms are used widely throughout the Report and have the meanings set forth below unless otherwise indicated. Words importing the singular number include the plural, and vice versa.

Act: means the Securities Act, R.S.O. 1990, chapter s.5.

AIF: means an annual information form as such term is defined in Form 51-102F2.

BAR: means a business acquisition report as such term is defined in NI 51-102.

Branch: means the Corporate Finance branch at the OSC.

CD: means the continuous disclosure obligations of a reporting issuer as set out in NI 51-102.

CDR program: means the harmonized program established in 2004 by the CSA for continuous disclosure reviews.

COVID-19: means the global pandemic of coronavirus disease 2019.

CPC: means a capital pool company as such term is defined in TSXV Policy 2.4 Capital Pool Companies.

CSA: means the Canadian Securities Administrators.

CSE: means the Canadian Securities Exchange.

Fiscal 2021: means the fiscal year ended March 31, 2021.

Fiscal 2020: means the fiscal year ended March 30, 2020.

Form 41-101F1: means Form 41-101F1 Information Required in a Prospectus as set out in the Act.

Form 45-106F1 means Form 45-106F1 Report of Exempt Distribution as set out in the Act.

Form 51-102F1: means Form 51-102F1 Management's Discussion & Analysis as set out in the Act.

Form 51-102F2: means Form 51-102F2 Annual Information Form as set out in the Act.

Form 51-102F5: means Form 51-102F5 Information Circular as set out in the Act.

FLI: means forward-looking information, as such term is defined in NI 51-102.

IFRS: means the standards and interpretations adopted by the International Accounting Standards Board, as amended from time to time.

IOR: means an issue-oriented review conducted by the Branch.

IOSCO: means the International Organization of Securities Commissions.

IPO: means an initial public offering as such term is defined in the Act.

Issuer: means an issuer as such term is defined in the Act.

MD&A: means a management's discussion and analysis as such term is defined in Form 51-102F1.

Modernization Taskforce: means the Capital Markets Modernization Taskforce appointed by the Ontario government in 2020.

Modernization Taskforce Report: means the final report issued by the Modernization Taskforce in January 2021.

NI 31-103: means National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations as set out in the Act.

NI 41-101: means National Instrument 41-101 General Prospectus Requirements as set out in the Act.

NI 43-101: means National Instrument 43-101 Standards of Disclosure for Mineral Projects as set out in the Act.

NI 43-101CP: means Companion Policy 43-101CP to NI 43-101.

NI 44-101: means National Instrument 44-101 Alternative Forms of Prospectus as set out in the Act.

NI 44-103: means National Instrument 44-103 Post-Receipt Pricing as set out in the Act.

NI 45-106: means National Instrument 45-106 Prospectus Exemptions as set out in the Act.

NI 51-102: means National Instrument 51-102 Continuous Disclosure Obligations as set out in the Act.

NI 51-102CP: means Companion Policy 51-102CP to NI 51-102.

NI 52-112: means National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure as set out in the Act.

NI 58-101: means National Instrument 58-101 Disclosure of Corporate Governance Practices as set out in the Act.

NP 11-202: means National Policy 11-202 Process for Prospectus Reviews in Multiple Jurisdictions as set out in the Act.

NGFM: Non-GAAP Financial Measures as such term is defined in NI 52-112.

OSC: means the Ontario Securities Commission.

OSC Rule 45-501: means OSC Rule 45-501 Ontario Prospectus and Registration Exemptions as set out in the Act.

PEA: Preliminary Economic Assessment as such term is defined in NI 43-101 Standards of Disclosure for Mineral Projects.

PIF: means a personal information form as such term is defined in NI 41-101.

QT: mean a qualifying transaction as such term is defined in TSXV policy 2.4 Capital Pool Companies.

Report: means this 2021 annual report, published by the Branch.

Reporting Issuer: means a reporting issuer as such term is defined in the Act.

SEDAR: means the system for electronic document analysis as such term is defined in National Instrument 13-101 System for Electronic Document Analysis and Retrieval of the Act.

SEDI: means the system for electronic disclosure by insiders.

SN 51-352: means CSA Staff Notice 51-352 Issuers with U.S. Marijuana-Related Activities.

SN 52-306: means CSA Staff Notice 52-306 (Revised) Non-GAAP Financial Measures.

Staff: means staff at the Branch.

TSX: means the Toronto Stock Exchange.

TSXV: means the TSX Venture Exchange.

* Note: all figures are as at / for the fiscal year ended March 31, 2021 and are approximate or rounded.

** Includes IPOs, public offerings and private placements of equity and convertible debentures.

This Report provides an overview of the Branch's operational and policy work during Fiscal 2021, including a summary of key findings and outcomes from our regulatory oversight program (Part A), and the nature, purpose and status of ongoing issuer-related policy initiatives (Part B). The Report is intended for entities and individuals we regulate, their advisors, as well as investors.

In publishing this Report we aim to

• REINFORCE the importance of compliance with regulatory obligations,

• PROVIDE GUIDANCE to improve disclosure in regulatory filings,

• HIGHLIGHT trends in the capital markets, and

• INFORM AND UPDATE on new and ongoing policy initiatives.

The OSC continues to implement the Ontario government's five-point capital markets plan focused on strengthening investment in Ontario, promoting competition and facilitating innovation.{1}

• OSC VISION: to be an effective and responsive securities regulator -- fostering a culture of integrity and compliance and instilling investor confidence in the capital markets.

• OSC MANDATE: to provide protection to investors from unfair, improper or fraudulent practices, to foster fair, efficient and competitive capital markets and confidence in the capital markets, to foster capital formation, and to contribute to the stability of the financial system and the reduction of systemic risk.

• OSC VALUES:

Professional, People, and Ethical:

• protecting the public interest is our purpose and our passion;

• we value dialogue with the marketplace;

• we are professional, fair-minded and act without bias.

Each year, the OSC publishes a statement of priorities that sets out the OSC's strategic goals, priorities, and specific initiatives for the year. Our priorities are aligned with our statutory mandate and the annual mandate letter from the Minister of Finance.

Our 2020-2021 OSC Goals are

• GOAL 1 promote confidence in Ontario's capital markets,

• GOAL 2 reduce regulatory burden,

• GOAL 3 facilitate financial innovation, and

• GOAL 4 strengthen our organizational foundation.

In support of the OSC's mandate, the Branch regulates approximately 1,100 Reporting Issuers in Ontario that are not investment funds. The Branch is responsible for assessing that Reporting Issuers in Ontario provide the required level of disclosure of material information to investors so they can make informed investment decisions. As a result of this oversight role, the Branch aids in the OSC's goal to improve transparency, trustworthiness, and efficiency in Ontario's capital markets.

To do this, our work includes, but is not limited to:

[X] review of public offerings of securities;

[X] review of capital raising activities;

[X] review of CD filed by Reporting Issuers;

[X] review and consideration of applications for exemptive relief from regulatory requirements;

[X] consideration and formulation of policy initiatives;

[X] review of insider reporting;

[X] review of credit rating agencies that are designated rating organizations;

[X] oversight of the listed Issuer function for OSC recognized exchanges;

[X] engagement with stakeholders through a number of activities, including external advisory committees; and

[X] delivery of Issuer education and outreach programs.

We also regularly consult and partner with other branches across the OSC in executing our work. For example, we partner with the Market Regulation branch for oversight of recognized exchanges, the Compliance and Registrant Regulation branch for oversight of the exempt market and the Enforcement branch on matters of non-compliance.

1. Continuous Disclosure Review Program

2. Public Offerings

3. Exemptive Relief Applications

4. Insider Reporting

5. Our Service Commitments

6. Administrative Matters

This section of the Report provides an overview of the key findings and outcomes from our CDR Program conducted during Fiscal 2021. Here, we discuss key or novel issues, suggest best practices, and specify applicable legislation and relevant guidance to assist companies in addressing each of the topic areas.

Under Canadian securities laws, a Reporting Issuer must provide timely and periodic CD about its business and affairs.

CD includes periodic filings such as

• interim and annual financial statements,

• MD&As,

• certificate of annual and interim filings,

• management information circulars,

• AIFs, and

• technical reports.

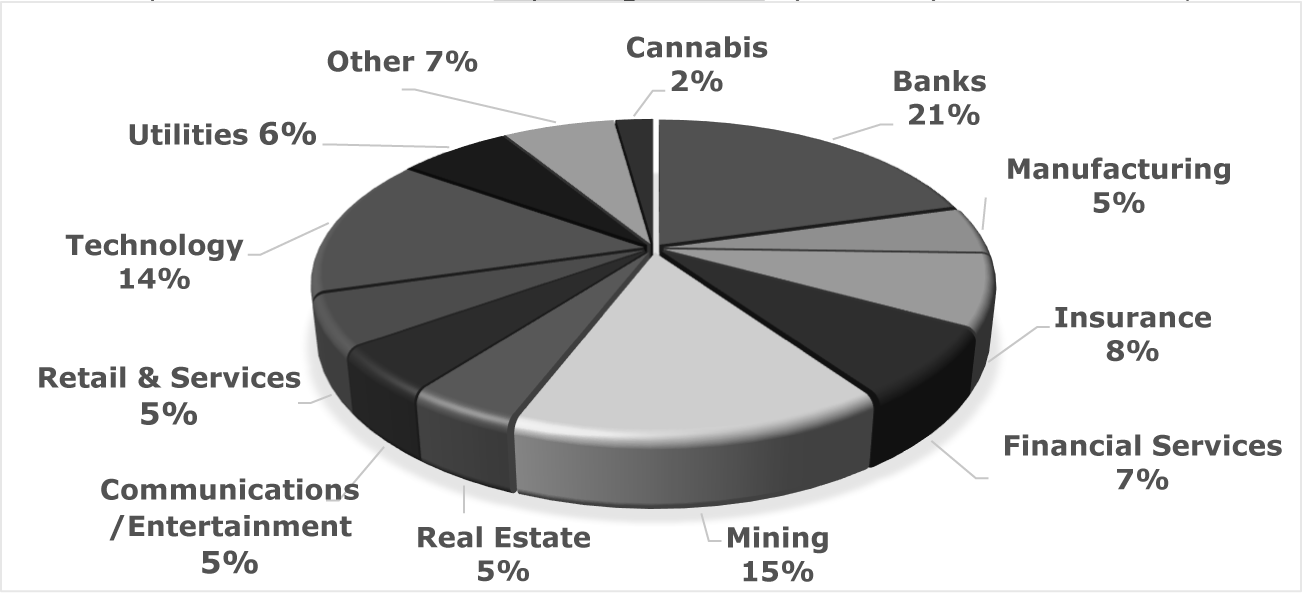

The Branch oversees approximately 1,100 Reporting Issuers for which the OSC has primary responsibility as principal regulator{2} with an aggregate market capitalization of $1,872 billion as at March 31, 2021. The three largest industries by market capitalization were banking, mining, and technology.

Market capitalization of Ontario Reporting Issuers by industry as at March 31, 2021

A) Overview

Our CDR program is risk-based and outcome focused. It includes planned reviews based on risk criteria as well as ongoing monitoring through news releases, media articles, complaints, and other sources. The CDR program is conducted pursuant to the powers in subsection 20(1) of the Act and is part of a harmonized CD review program conducted by the CSA.{3}

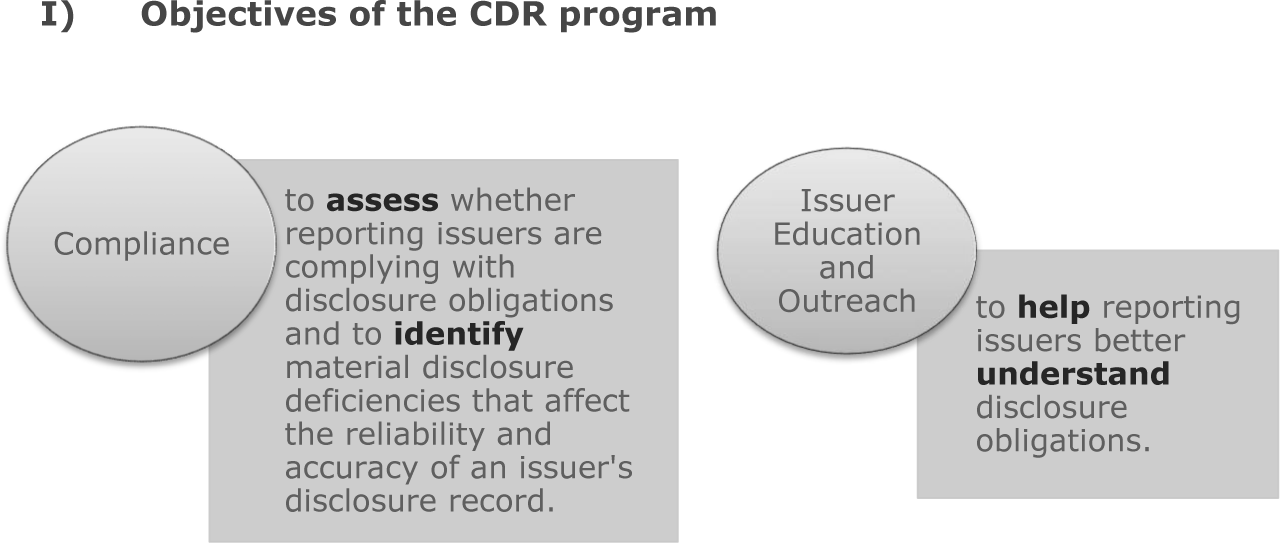

I) Objectives of the CDR program

We assess compliance with CD requirements through a review of a Reporting Issuer's filed documents, its website and social media. This review function is critical to facilitating fair and efficient markets, investor protection, and informed investment decision making and trading. Enhanced disclosure is important not only when a Reporting Issuer first enters the market, but also on an ongoing basis; for example, many Reporting Issuers raise funds through short form prospectuses which incorporate CD documents by reference.

II) Types of CD reviews

In general, we conduct either a full review or an IOR of a Reporting Issuer's CD.

In planning full reviews, we draw on our knowledge of Reporting Issuers and the industries in which they operate and use risk-based criteria to identify Reporting Issuers with a higher risk of non-compliant disclosure. The criteria are designed to identify Reporting Issuers whose disclosure is likely to be materially improved or brought into compliance with securities laws or accounting standards as a result of our intervention. Our risk-based assessment incorporates both qualitative and quantitative criteria which we review regularly to keep current with our evolving capital markets.{4} We also monitor novel and high growth areas of financing activity when developing our review program and consider any complaints received regarding the Reporting Issuer.

IORs are generally focused on a specific accounting, legal or regulatory issue, an emerging issue or industry or to assess compliance with a new or amended rule that recently came into force. Conducting IORs allows us to

• monitor compliance with CD requirements by Reporting Issuers,

• communicate Staff interpretations and expectations on specific requirements, and identify areas of concern,

• quickly address specific areas where there is heightened risk of investor harm,

• identify common deficiencies,

• provide industry specific disclosure guidance that may assist preparers in complying with regulatory requirements, and

• assess compliance with new accounting standards.

III) What to do when you are selected for a CD review

If you receive a comment letter from Staff in connection with a CD review, consider all of the following:

[X] read the first paragraph of the letter which will state whether we are conducting a full review or an IOR review;

[X] consider whether you need to seek advice from legal, accounting, and/or other advisors. If so, engage them early in the process;

[X] reach out to Staff if you require clarification about any of the comments. Note that Staff cannot provide legal or accounting advice;

[X] provide a thorough response, referencing securities laws or IFRS, where relevant;

[X] continue to file required CD documents during the course of the review. An ongoing review does not alleviate or alter a Reporting Issuer's ongoing CD obligations;

[X] note the response deadline and plan accordingly. Reach out to Staff well in advance of the deadline, should you require additional time to provide a response letter. In appropriate circumstances, Staff may consider granting an extension request.

B) CDR program outcomes for Fiscal 2021

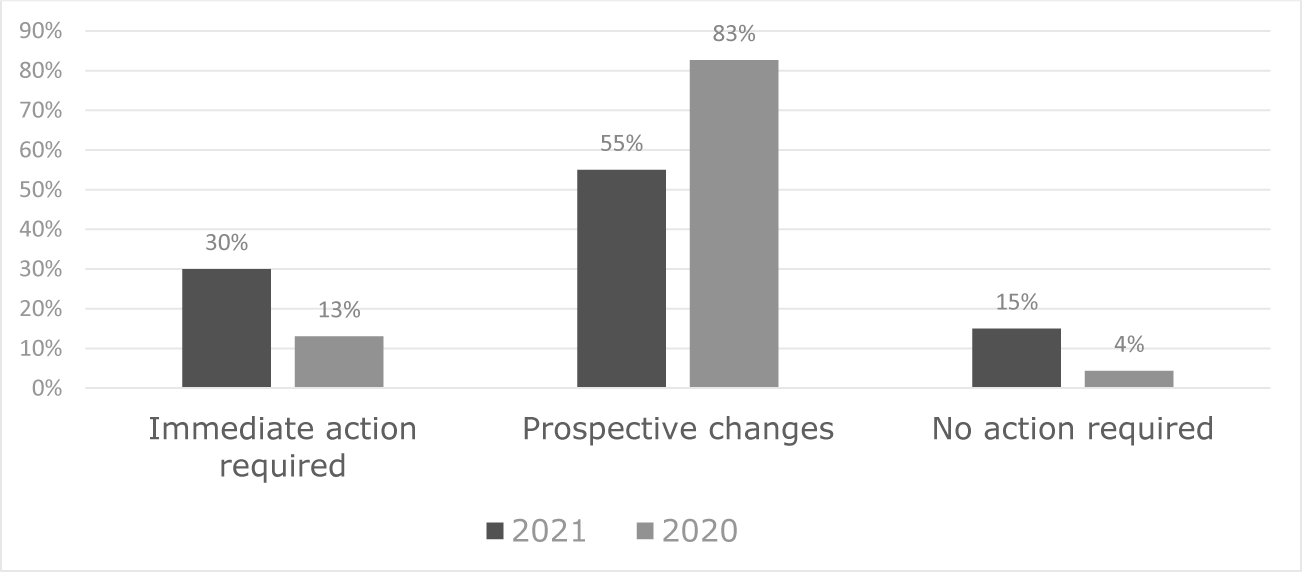

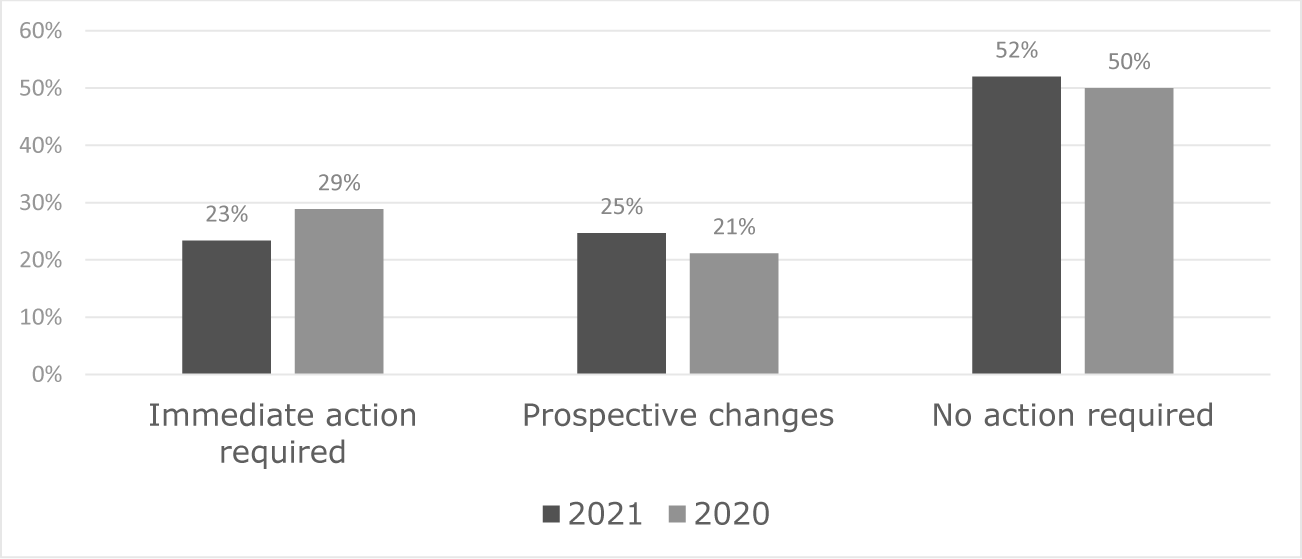

For each Reporting Issuer, we measure outcomes of a CD review by tracking when no action is required, when prospective continuous disclosure enhancements are required, or when immediate corrective action is required for deficiencies identified during a review (for example, a refiling of a previously filed CD document or a referral to the Enforcement branch). A CD review may result in more than one outcome. For example, a Reporting Issuer may be required to refile certain CD documents while also to commit to prospective disclosure enhancements.

Given our risk-based criteria to identify Reporting Issuers for review, the outcomes on a year-over-year basis should not be interpreted as trends since the issues and Reporting Issuers reviewed each year are generally different. Reviews may be issue-specific, focusing on a particular CD requirement for which we have noted widespread deficiencies. These reviews may result in an increased number of outcomes categorized as "prospective changes" or "immediate action required" if deficiencies identified are prevalent among several Reporting Issuers.

The following is the summary of the CD review outcomes for Fiscal 2021.

Outcomes of full CD reviews

Outcomes of IOR CD Reviews

The most common instances where immediate action was required from Reporting Issuers were the following:

• refiling of financial statements to correct material misstatements;

• refiling of an MD&A where the MD&A was materially deficient and did not meet the form requirements of Form 51-102F1;

• filing of a clarifying news release when an Issuer failed to include sufficient disclosure of material assumptions, milestones and risk factors pertaining to FLI or failed to update the market on FLI;

• refiling of a technical report where the report filed was not in compliance with NI 43-101.

Issuers that refile CD documents during a Staff review are placed on the Refilings and Errors list found on the OSC Website.

Generally, MD&A, mining technical reports (and related news releases) and material contracts are the documents we most often request Reporting Issuers to refile or file (in instances when documents were not filed in the first place).

C) Trends and guidance

This section highlights some of the common deficiencies that were observed during our CD reviews in Fiscal 2021, and includes some best practices and guidance to assist Reporting Issuers and their advisors in meeting their regulatory obligations. We encourage Reporting Issuers to continue to review and improve the CD filed, including with reference to the guidance below.

I) Management's discussion & analysis

The MD&A is the cornerstone of a Reporting Issuer's overall financial disclosure and is intended to provide an analytical and balanced discussion of the Issuer's results of operations and financial condition through the eyes of management. MD&A disclosure should be specific, useful and understandable. The MD&A requirements are set out in Part 5 of Form 51-102F1.

The following table presents a summary of certain key issues, observations and best practices identified in our reviews. This is not an exhaustive list.

Since the World Health Organization declared COVID-19 as a global pandemic on March 11, 2020, it has had a material adverse impact on the economy generally. The impact of COVID-19 continues to pose widespread challenges for many Issuers, including, but not limited to, reporting on and disclosing the impact it has had on the Issuer's business. An Issuer should consider its specific business and operations, and provide clear and transparent disclosure of the impact of COVID-19 in its MD&A.{5}

Issue |

Observations |

Best practices |

|

|

|||

Updating previously disclosed <<FLI>> |

<<Reporting Issuers>> who have previously disclosed <<FLI>> in a prospectus and/or <<CD>> do not provide appropriate updates to those <<FLI>> in <<CD>> documents. |

<<Reporting Issuers>> that have disclosed <<FLI>>, especially in a prospectus, have an obligation to update the <<FLI>> in <<CD>> documents going forward and to provide a comparison of actual results to the previously disclosed <<FLI>>. It is important to provide investors with information to assess how well the <<Reporting Issuer>> is progressing towards the achievement of its disclosed targets and objectives. |

|

|

|||

<<Reporting Issuers>> should |

|||

• |

disclose events and circumstances that are reasonably likely to cause actual results to differ materially from the previously disclosed <<FLI>>, |

||

• |

disclose expected differences between actual results and previously disclosed <<FLI>>, |

||

• |

update quantified data that relate to factors and assumptions that may impact future performance and discuss how and why these changes may impact future performance, and |

||

• |

disclose the decision to withdraw previously disclosed <<FLI>> and discuss events and circumstances that led to the decision to withdraw material <<FLI>>, including a discussion of any assumptions in the previously disclosed <<FLI>> that are no longer valid. |

||

|

|||

There is flexibility to disclose the updated information in a news release before filing the <<MD&A>>. This approach would help ensure the new information is communicated to the market on a timely basis. The <<MD&A>> must refer to the press release to satisfy the requirement in <<NI 51-102>>. Including the information in a news release instead of <<MD&A>> is not permitted. |

|||

|

|||

We also continue to see other deficiencies in <<FLI>> disclosure including a lack of balanced discussion of the key assumptions used and the risk factors inherent in the <<FLI>>. <<Issuers>> should consider the guidance in prior <<Corporate Finance Branch Annual Reports>>. |

|||

|

|||

Non-GAAP Financial Measures (NGFM) |

<<Reporting Issuers>> continue to present <<NGFM>>s where the stated purpose and usefulness of the measure is unclear. The <<NGFM>>s are also being presented without the relevant reconciliations to the most directly comparable GAAP measure. |

<<NGFM>>s can provide investors with additional insight into the performance of the <<Issuer>>. However, where the stated purpose and usefulness of the measure is unclear and fails to align with the nature of the adjustments that are being made in the reconciliation, there is potential that investors may be confused or even misled. |

|

|

|||

To assist in understanding the purpose of the <<NGFM>>, <<Issuers>> are expected to provide a quantitative reconciliation of the <<NGFM>> for its current and comparative period to the most directly comparable GAAP measure. To support understandability, explanations for each reconciling item should be provided, as appropriate. |

|||

|

|||

Quantitative reconciliations are expected to be included when <<NGFMs>> are presented in the <<MD&A>> and earnings releases and included or incorporated by reference when <<NGFMs>> are included in other documents, such as <<AIF>>, investor presentations, websites, etc. |

|||

|

|||

Also refer to the discussion on <<non-GAAP financial measures>> in section IV below. |

|||

|

|||

Discussion of operations -- Variances |

The variances in financial statement line items are explained with limited narrative discussion of (a) the factors resulting in the variance, and (b) any trends or potential trends. |

The discussion of financial statement variances should |

|

• |

quantify key changes and clearly explain the factors and reasons for the variances that affect revenues and expenses beyond simply stating the percentage change or amount (for example, variables such as price and volume or other significant factors should be discussed by segment), |

||

• |

provide insight into the <<Issuer's>> past and future performance, and |

||

• |

be clear and transparent. |

||

|

|||

When discussing the changes in financial condition and results, it is also important to include an analysis of the effect on continuing operations of any acquisition, disposition, write-off, abandonment or other similar transaction. |

|||

|

|||

Be specific and disclose information that gives insight into an <<Issuer's>> operations and economic environment that may assist readers in making informed investment decisions. |

|||

|

|||

Discussion of operations -- Early stage/development stage Reporting Issuers |

<<Reporting Issuers>> that have projects that have not yet generated revenues do not provide sufficient detail regarding the projects and/or business plans. |

Disclosures should include |

|

• |

a description of each project including the plan for the project and status of the project relative to that plan. For R&D activity, include this discussion for each stage, |

||

• |

identification of concrete milestones in the plan, and |

||

• |

for each project/stage/milestone, a description of expenditures made and how these relate to anticipated timing and costs to take the project to the next stage of the project plan. |

||

II) COVID-19 disclosure

In the fall of 2020, CSA staff initiated an IOR of approximately 85 Reporting Issuers across various industries to assess compliance of Reporting Issuers' disclosure of the current and anticipated impacts related to COVID-19 on the Issuer's operations, its financial condition, liquidity and future prospects. CSA staff observed that the majority of Reporting Issuers reviewed provided detailed and quality disclosure. However, CSA staff also identified instances where Reporting Issuers did not provide sufficient detail related to the current and expected impact of COVID-19, resulting in requests for those Reporting Issuers to make prospective disclosure enhancements.

On February 25, 2021, the CSA published CSA Staff Notice 51-362 Staff Review of COVID-19 Disclosures and Guide for Disclosure Improvements that summarizes the findings from our review and sets out guidance to assist Reporting Issuers and advisors in disclosing and reporting on the impact of COVID-19 on its business and operations.

We expect Reporting Issuers to continue to discuss the impacts of COVID-19 on their business and operations, to the extent applicable.

III) Mining disclosure

Preliminary Economic Assessment

Reporting Issuers that disclose potential economic outcomes based on mineral resources should be aware that forecasts of cash flows, operating costs, capital costs, production rates, or mine life are all considered to be the results of a PEA. Such disclosure may trigger the requirement to file a technical report supporting these potential economic outcomes.

We continue to see non-compliant disclosure in technical reports of PEA based on inferred mineral resources which combine potential economic outcomes from PEAs with economic outcomes based on more advanced mining studies used to support mineral reserves. All CSA jurisdictions take the position that when a feasibility or pre-feasibility study has estimated a mineral reserve, a PEA that presents a different development option for any part of the reserve invalidates the earlier study. Disclosure that treats both the mineral reserve estimate and the PEA results as current may potentially be misleading and Staff will ask that either the reserve estimate or the PEA be retracted. Reporting Issuers that integrated these economic outcomes in the disclosure have been required to amend and refile the technical report.

Calculation of equivalent grades

It is common for Reporting Issuers to provide metal-equivalent or mineral-equivalent grades in disclosures of mineral reserve or resource estimates, drill intervals, or other samples. Reporting Issuers sometimes base mineral reserve or resource estimates on equivalent cut-off grades. Staff have encountered equivalent grades weighted by commodity prices only, without regard to differing recoveries of the component elements. No operating mine gets 100% recoveries so equivalent grades weighted only by price are potentially misleading.

To avoid potentially misleading disclosure, Reporting Issuers should calculate equivalent grades taking both recovery of each element, either drawn from test results or reasonably assumed, and prices, into account. They should also consider whether cost factors such as treatment charges and payable ratio may be relevant.

Independence of authors

When independent authors are required for a technical report, all its authors must meet these requirements. Some Reporting Issuers have sought guidance on whether a particular person is independent for that purpose. The existing guidance in NI 43-101CP, section 1.5, notes that a person's potential for a pecuniary interest in the Reporting Issuer or the subject mineral property would be relevant to the assessment of an author's independence. Recent experience also suggests that potential employment, potential sale of services or intellectual property, or previous involvement with the mineral property -- amounting to reviewing one's own work -- may also compromise a report author's independence.

Impacts of COVID-19

Travel restrictions imposed in reaction to the coronavirus epidemic created difficulties for Reporting Issuers required to file technical reports, as those reports could not be completed without a current personal inspection by a report author. Reporting Issuers should consider the guidance in CSA Staff Notice 51-360 (Updated) Frequently asked questions regarding filing extension relief granted by way of a blanket order in response to COVID-19, dated May 13, 2020, in particular the guidance under P2, Is there relief from the NI 43-101 requirement for a Current Personal Inspection? Staff consider a personal inspection essential if a mineral resource estimate, or any study based on one, is disclosed. For earlier-stage projects, exemptive relief may be possible. We encourage Reporting Issuers to reach out to Staff who may be able to provide guidance on options and solutions to comply with the requirements while also respecting the personal health and safety of the qualified person.

Estimation best practices

Staff also reminds Reporting Issuers in the mineral industry that the Canadian Institute of Mining, Metallurgy, and Petroleum (CIM) has revised its guidance on estimation and exploration best practices. CIM Estimation of Mineral Resources & Mineral Reserves Best Practice Guidelines and CIM Mineral Exploration Best Practice Guidelines are significant enhancements of previous CIM best-practice documents, and we encourage Reporting Issuers and practitioners to consult the new editions for current guidance on exploration and mineral resource and reserve estimation practices.

- - - - - - - - - - - - - - - - - - - -

Reminder: Reporting Issuers that disclose a PEA on an advanced property containing mineral reserves should follow the guidance outlined in CSA Staff Notice 43-307 Mining Technical Reports -- Preliminary Economic Assessments.

We encourage public mining Reporting Issuers to request a review of the issuer's publicly filed technical disclosure, as discussed in OSC Staff Notice 43-706 Pre-filing Review of Mining Technical Disclosure.

- - - - - - - - - - - - - - - - - - - -

IV) Non-GAAP financial measures

On May 27, 2021, the CSA published, in final form, NI 52-112, the associated companion policy, and related consequential amendments which will replace existing staff guidance in SN 52-306. NI 52-112 addresses the disclosure surrounding NGFM, non-GAAP ratios, and other financial measures (e.g., capital management measures, supplementary financial measures, and total of segments measures, as defined in the national instrument). Although the definition of a NGFM has been updated from SN 52-306, NI 52-112 has substantially incorporated the disclosure guidance in SN 52-306 for non-GAAP financial measures. To ensure investors appreciate the context of other financial measures, NI 52-112 introduces new disclosure requirements if such financial measures are disclosed outside of the financial statements.

The companion policy includes extensive guidance and examples. NI 52-112 applies to all Reporting Issuers, except investment funds, SEC foreign issuers, and designated foreign issuers. NI 52-112 also applies to non-Reporting Issuers; in particular, to documents prepared by such issuers in connection with certain prospectus exempt offerings or other transactions (such as, but not limited to, an offering memorandum, long-form prospectus, or a filing statement / listing statement).

The rule applies to disclosures for a financial year ending on or after October 15, 2021.

Examples are as follows:

- - - - - - - - - - - - - - - - - - - -

Reporting Issuers

• a non venture reporting issuer with a December 31st year end, will first apply the rule in the following documents, such as;

-- in its MD&A for the year ended December 31, 2021;

-- in its earnings release containing disclosures for the year ended December 31, 2021.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

Non-Reporting Issuers

• a non reporting issuer, will first apply the rule in any document in scope of NI 52 112 after December 31, 2021 (i.e. January 1, 2022 and beyond).

- - - - - - - - - - - - - - - - - - - -

If a non-Reporting Issuer files a preliminary long form prospectus, or similar document, prior to December 31, 2021, but anticipates that a final long form prospectus may not be filed until after December 31, 2021, the non-Reporting Issuer should consider preparing the preliminary prospectus in accordance with the rule. A final prospectus filed after December 31, 2021 must comply with NI 52-112 in respect of any specified financial measures disclosed.

V) Diversity on boards and in executive officer positions

The disclosure requirements on the representation of women on boards and in executive officer positions are set out in NI 58-101 and have been in place for seven annual reporting periods. The disclosure requirements are intended to increase transparency for investors and other stakeholders regarding the representation of women in these roles and the approach that specific TSX-listed Reporting Issuers take in respect of such representation. This transparency is intended to assist investors when making investment and voting decisions.

On March 10, 2021, CSA Multilateral Staff Notice 58-312 Report on Sixth Staff Review of Disclosure regarding Women on Boards and in Executive Officer Positions (SN 58-312) was published. SN 58-312 reports the findings of our sixth review of disclosure regarding women on boards and in executive officer positions. Of note, 20% of overall board seats were occupied by women, 79% of Reporting Issuers in the review sample had at least one woman on the board and 65% of Reporting Issuers in the review sample had at least one woman in an executive officer position.

CSA Multilateral Staff Notice 58-313 Report on Seventh Staff Review of Disclosure regarding Women on Boards and in Executive Officer Positions (SN 58-313) provides new guidance on how Reporting Issuers may present the information contemplated by the disclosure requirements in order to improve consistency and comparability amongst Reporting Issuers. During our review, we noted that Reporting Issuers generally provide disclosure addressing the disclosure requirements in different ways. As a result of this, the format and content of disclosure may vary from Reporting Issuer to Reporting Issuer. It may also be difficult to locate the relevant disclosure within an information circular and it may be difficult to interpret some of the disclosure. In order to address this, Reporting Issuers should consider presenting data related to the disclosure requirements in a common format. This would improve consistency and comparability and help investors identify and evaluate the relevant disclosure. SN 58-313 sets out suggested tables for how this data could be presented.

On May 19, 2021 the CSA published a news release announcing that further research and consultation will be conducted with Issuers, investors and other industry stakeholders in the consideration of broader diversity on boards and executive officer positions. These consultations began in the summer of 2021. The CSA will use its findings from these consultations to consider recommendations for any necessary changes to the current diversity disclosure framework. A virtual 'Diversity in Capital Markets' roundtable, moderated and hosted by the OSC, was held on October 13, 2021.

VI) Cease Trade Order -- Content Deficiency

The CSA has developed a harmonized list of deficiencies that will generally result in a Reporting Issuer being noted in default of the securities laws of a particular jurisdiction. We remind Reporting Issuers that these deficiencies include the failure to file certain continuous disclosure documents and content deficiencies in the Reporting Issuer's continuous disclosure. Cease trade orders may be issued where a Reporting Issuer has made a required filing but the required filing is deficient in terms of content.{6}

Under Canadian securities law, to distribute securities, an Issuer must file and obtain a receipt for a prospectus or rely upon a prospectus exemption. Another key component of our compliance work stream is the review of prospectuses in connection with public offerings. This section outlines statistics and trends with respect to public offerings and provides guidance on common issues that arise during our reviews of prospectuses.

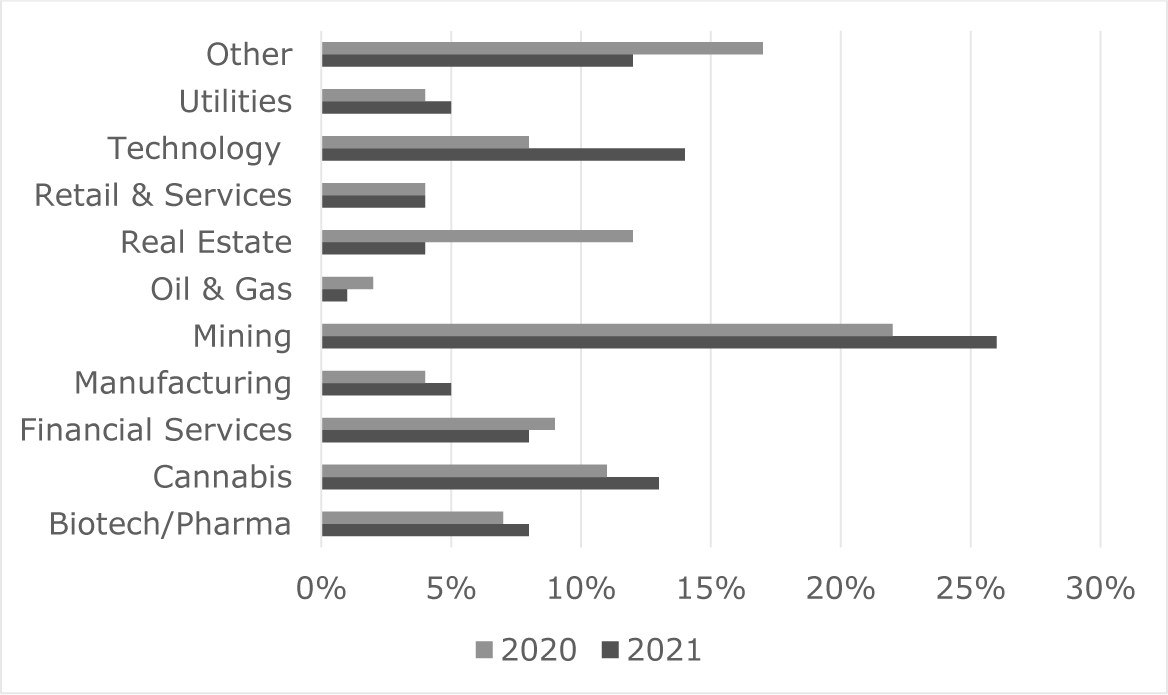

In Fiscal 2021, we completed 574 prospectuses that were filed in Ontario (Fiscal 2020: 388). These filings covered a wide range of industries with mining, technology and cannabis being the most active sectors based on the number of offerings.

Prospectuses completed by industry (%) -- Fiscal 2021 & 2020

60) Trends and guidance

In Fiscal 2021, we observed a significant increase in the number of prospectuses where the OSC was the principal regulator, particularly in the second half of the year. A significant factor in the increase in volume over the year was the overall activity in the market driven by an increase in offerings in the cannabis and psychedelics industries, as well as an increase in offerings in the mining and technology industries.

We also saw an increase in the number of offerings after the initial impacts of COVID-19 in March 2020, and by Q3 and Q4 of Fiscal 2021 we noted a substantial increase in the volumes in offerings.

- - - - - - - - - - - - - - - - - - - -

Tip: The guidance in this section also applies to prospectus-level disclosure included in an information circular in connection with a proposed significant acquisition or a restructuring transaction as required by section 14.2 of Form 51-102F5.

- - - - - - - - - - - - - - - - - - - -

Key takeaways from our reviews of offering documents in Fiscal 2021 are set out below.

I) Primary business in an IPO

Form 41-101F1 requires an Issuer that is not an investment fund to include certain financial statements in its long form prospectus. This includes the financial statements of the Issuer and any business or businesses acquired, or proposed to be acquired, if a reasonable investor reading the prospectus would regard the primary business of the Issuer to be the business or businesses acquired, or proposed to be acquired. The purpose of the primary business requirements is to provide investors with financial history of the business of the Issuer even if this financial history spanned multiple legal entities over the relevant time period.

On August 12, 2021, the CSA proposed changes to Companion Policy 41-101CP related to primary business requirements to harmonize the interpretation of the financial statement requirements for a long form prospectus in situations where an Issuer has acquired a business, or proposes to acquire a business, that a reasonable investor would regard as being the primary business of the Issuer.{7} The proposed changes provide additional guidance on the interpretation of primary business and predecessor entity including in what situations, and for which time periods, financial statements would be required. The proposed changes provide guidance in circumstances when additional information may be necessary for the prospectus to meet the requirement to contain full, true and plain disclosure of all material facts relating to the securities being distributed. The proposal also clarifies when an Issuer can use the optional tests to calculate the significance of an acquisition, and when an acquisition of mining assets would not be considered an acquisition of a business for securities legislation purposes.

The comment period ended on October 11, 2021. Subject to the comment process and required approvals, the proposed changes are expected to become effective in July 2022.

II) Timing for inclusion of financial statements in an IPO venture issuer's prospectus

Under Form 41-101F1, annual financial statements are required to be included in a prospectus for completed financial years ended more than (i) 90 days before the date of the prospectus, or (ii) 120 days before the date of the prospectus if the Issuer is a venture Issuer. Interim financial statements are subject to a similar requirement for periods ended within 45 and 60 days, respectively. Importantly, the extended deadlines applicable to venture Issuers do not apply to IPO venture Issuers. This includes an RTO acquirer in the context of a restructuring transaction that is subject to the requirements of Form 41-101F1.

Type of issuer |

Deadline for inclusion of annual financial statements |

Deadline for inclusion of interim financial statements |

|

||

Non-venture <<Issuer>> |

90 days |

45 days |

|

||

<<IPO>> venture <<Issuer>> |

90 days |

45 days |

|

||

RTO acquirer (i.e. target) |

90 days |

45 days |

|

||

Venture <<Issuer>> (i.e. an existing <<Reporting Issuer>>) |

120 days |

60 days |

- - - - - - - - - - - - - - - - - - - -

Reminder: The 90 and 45 day deadlines are also applicable to any "issuer" financial statements that are included in an IPO venture issuer's prospectus or similar document in compliance with Item 32 of Form 41-101F1.

- - - - - - - - - - - - - - - - - - - -

III) Description of business