Ontario Securities Commission Bulletin

Issue 44/42 - October 21, 2021

Ont. Sec. Bull. Issue 44/42

Table of Contents

Notices

• Consultation -- Climate-related Disclosure Update and CSA Notice and Request for Comment Proposed National Instrument 51-107 -- Disclosure of Climate-related Matters

• Notice of Coming into Force of Amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations to Enhance Protection of Older and Vulnerable Clients

• OSC Staff Notice 11-737 (Revised) -- Securities Advisory Committee -- Vacancies

Notices of Hearing with Related Statements of Allegations

• Michael Paul Kraft and Michael Brian Stein -- ss. 127(1), 127.1

Notices from the Office of the Secretary

• Sean Daley and Kevin Wilkerson

• Mek Global Limited and PhoenixFin Pte. Ltd.

• Michael Paul Kraft and Michael Brian Stein

• Polo Digital Assets, Ltd.

• Miner Edge Inc. et al.

Orders

• Mek Global Limited and PhoenixFin Pte. Ltd.

• Golden Predator Mining Corp.

• Polo Digital Assets, Ltd.

• Miner Edge Inc. et al.

• Briko Energy Corp.

OSC Decisions

• Sean Daley and Kevin Wilkerson -- s. 127(1)

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• Outstanding Management & Insider Cease Trading Orders

• Amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations

• Changes to Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations

• Registrants

SROs

• Investment Industry Regulatory Organization of Canada (IIROC) -- Housekeeping Amendments to the Universal Market Integrity Rules (UMIR) Regarding the Definition of "Marketplace" -- Notice of Commission Deemed Approval

Clearing Agencies

• Canadian Derivatives Clearing Corporation (CDCC) -- Proposed Amendments to the Risk Manual of CDCC to Change the Initial Margin Model for Bond Derivatives -- Notice of Commission Approval

• Canadian Derivatives Clearing Corporation (CDCC) -- Proposed Amendments to the Risk Manual of CDCC to Change the Initial Margin Model for Equity Derivatives -- Notice of Commission Approval

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Consultation -- Climate-related Disclosure Update and CSA Notice and Request for Comment Proposed National Instrument 51-107 -- Disclosure of Climate-related Matters

Consultation -- Climate-related Disclosure Update and CSA Notice and Request for Comment Proposed National Instrument 51-107 -- Disclosure of Climate-related Matters is reproduced on the following separately numbered pages. Bulletin pagination resumes at the end of the Consultation.

Consultation Climate-related Disclosure Update and CSA Notice and Request for Comment Proposed National Instrument 51-107 Disclosure of Climate-related Matters

October 18, 2021

PART 1 -- Introduction

Since the publication of CSA Staff Notice 51-358 Reporting of Climate Change-related Risks in August 2019 (CSA Staff Notice 51-358), the Canadian Securities Administrators (CSA) have continued to follow developments in relation to climate-related disclosure. Most recently, CSA staff have conducted research on domestic and international developments in this area, as well as an issue-oriented review of recent climate-related disclosure by Canadian reporting issuers. Separately, the 2021 Ontario Budget, released on March 24, 2021, discussed Environmental, Social and Corporate Governance (ESG) disclosure requirements, and stated that the Ontario Securities Commission (OSC) would begin policy work to inform further regulatory consultation on ESG disclosure.

The CSA are publishing proposed National Instrument 51-107 Disclosure of Climate-related Matters (the Proposed Instrument) and its companion policy (the Proposed Policy) for a 90-day comment period. The Proposed Instrument would introduce disclosure requirements regarding climate-related matters for reporting issuers (other than investment funds).

We are issuing this notice to provide an update on recent developments regarding climate-related disclosure and to solicit your comments on the Proposed Instrument as set out in Annex A and the Proposed Policy in Annex B. The text of the Proposed Instrument is also available on the following websites of CSA jurisdictions:

www.lautorite.qc.ca

www.bcsc.bc.ca

www.albertasecurities.com

www.osc.gov.on.ca

nssc.novascotia.ca

www.fcaa.gov.sk.ca

www.fcnb.ca

www.mbsecurities.ca

The public comment period expires on January 17, 2022.

PART 2 -- Substance and Purpose of the Proposed Instrument

The focus on climate-related issues in Canada and internationally has grown rapidly in recent years with climate-related risks having become a mainstream business issue. There is growing discussion on moving toward mandatory climate-related disclosures that provide consistent, comparable and decision-useful information to market participants. Investors, particularly institutional investors, and other stakeholders are increasingly focused on climate-related risks and are seeking improved disclosure on issuer governance processes and the material risks, opportunities, and financial impacts of climate change.

The CSA note concerns about current climate-related disclosures, including the following:

• issuers' climate-related disclosures may not be complete, consistent, and comparable;

• quantitative information is often limited and not necessarily consistent;

• issuers may "cherry pick" by reporting selectively against a particular voluntary standard and/or frameworks; and

• sustainability reporting can be siloed and is not necessarily integrated into companies' periodic reporting structures.

Securities regulators have a role to play in promoting disclosures that yield decision-useful information for investors. This is achieved by requiring reporting issuers to disclose material information, which can be used by investors to inform their investment and voting decisions.

The CSA believe that the climate-related disclosure requirements contained in the Proposed Instrument would provide clarity to issuers on the information required to be disclosed and also facilitate consistency and comparability among issuers. Specifically, the climate-related disclosure requirements are intended to:

• improve issuer access to global capital markets by aligning Canadian disclosure standards with expectations of international investors;

• assist investors in making more informed investment decisions by enhancing climate-related disclosures;

• facilitate an "equal playing field" for all issuers through comparable and consistent disclosure; and

• remove the costs associated with navigating and reporting to multiple disclosure frameworks as well as reducing market fragmentation.

We are sensitive to concerns related to the regulatory burden and additional cost of mandatory climate-related disclosure. The CSA believe the Proposed Instrument addresses this concern in three ways:

1. issuers will not be required to disclose scenario analysis, including a 2°C or lower scenario;

2. issuers may disclose their greenhouse gas (GHG) emissions or explain why they have not done so;{1} and

3. the disclosure requirements will be phased-in over a one-year period for non-venture issuers and over a three-year period for venture issuers. It is not anticipated that the Proposed Instrument will come into force prior to December 31, 2022.{2}

PART 3 -- Existing Disclosure Requirements

Current securities legislation in Canada requires disclosure of certain climate-related information in an issuer's regulatory filings if such information is material.

Existing requirements that may apply to climate-related information can be found in the following rules:

• National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102);

• National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109);

• National Instrument 52-110 Audit Committees (NI 52-110); and

• National Instrument 58-101 Disclosure of Corporate Governance Practices (NI 58-101).

In addition, guidance on corporate governance practices is provided in National Policy 58-201 Corporate Governance Guidelines (NP 58-201).

Existing disclosure requirements continue to apply and are not modified by the Proposed Instrument.

Please refer to Annex C for an overview of the relevant existing securities law provisions.

PART 4 -- Summary of findings of 2021 Climate-related Disclosure Issue Oriented Review

In Spring 2021, staff in certain CSA jurisdictions{3} (the review staff) conducted a targeted review of current public disclosure practices of 48 selected large Canadian issuers primarily from the S&P/TSX Composite Index, from a diverse range of industries, with respect to climate-related information (the Disclosure Review).

The Disclosure Review was contemplated as part of the CSA's follow-up work on CSA Staff Notice 51-358 to monitor disclosure of climate-related matters and to evaluate the current state of climate-related disclosure by Canadian issuers since its publication. Review staff assessed the extent to which material climate-related risks, financial impacts and related governance disclosure were provided in continuous disclosure (CD) filings. In addition, review staff reviewed voluntary disclosure reports provided by the selected issuers to gain a better understanding of additional climate-related disclosure being provided, and to assess whether potential material information had been omitted from issuers' CD filings.

Key findings of the review were as follows:

• Generally speaking, when compared to the 2017 review findings published in CSA Staff Notice 51-354 Report on Climate Change-related Disclosures Project (CSA Staff Notice 51-354), issuers are providing more climate-related information in their CD filings and voluntary reports. Risk disclosure increased across all risk types, and there was a marked improvement by issuers in addressing the qualitative financial impact of disclosed climate-related risks.

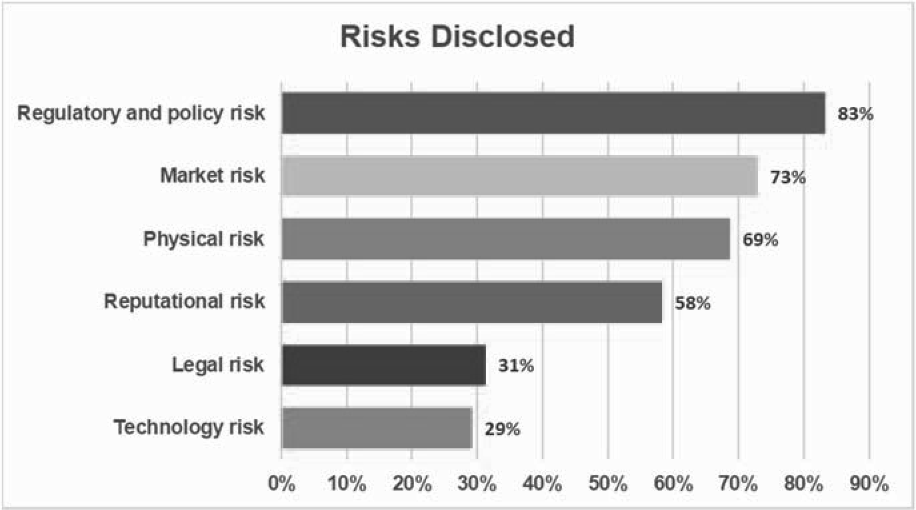

• While the volume of climate-related disclosures has increased and the quality has generally improved, review staff noted areas where disclosures were limited and lacked specificity. Although 92% of issuers disclosed climate-related risks in their CD filings, with regulatory and policy risks being the most commonly disclosed, on average only 59% of the risks were relevant, detailed and entity specific, while the remaining risks were either boilerplate, vague or incomplete. While 68% of the risk disclosures provided a qualitative discussion of the related financial impacts, 25% of risk disclosures did not address the financial impact at all, and no issuers quantified the financial impact of the identified risks.

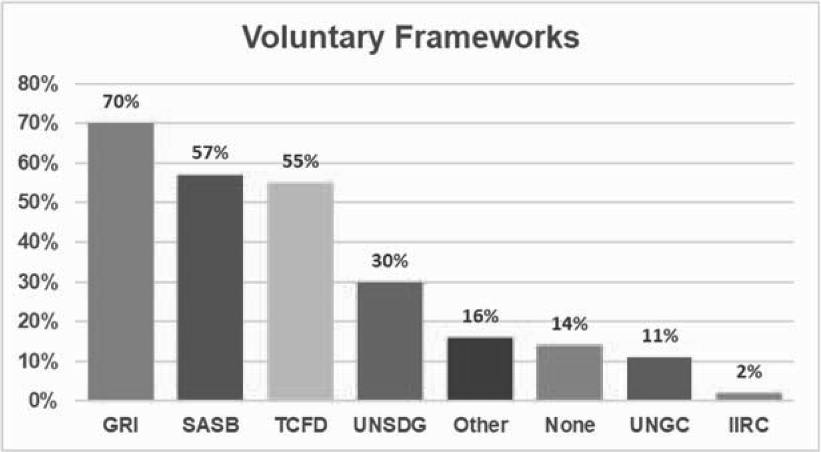

• 92% of issuers provided climate-related disclosures in voluntary reports in a variety of forms, the most common being Sustainability or Environmental, Social, and Governance reports. Where voluntary third-party frameworks were referenced in voluntary disclosures, the Global Reporting Initiative (GRI) framework was the most common, followed by the Sustainability Accounting Standards Board (SASB) and the Task Force on Climate-related Financial Disclosures (TCFD) recommendations. On average, issuers referenced nearly three third-party frameworks in their voluntary reports.

For further information on the findings of the Disclosure Review, please see Annex D.

PART 5 -- Background

CSA Publications

The CSA has issued the following publications regarding climate-related disclosures:

• CSA Staff Notice 51-333 Environmental Reporting Guidance (October 2010) (CSA Staff Notice 51-333);

• CSA Staff Notice 51-354 (April 2018); and

• CSA Staff Notice 51-358.

CSA Staff Notice 51-333, issued in 2010, provided guidance to issuers on existing continuous disclosure requirements relating to environmental matters under securities legislation. CSA Staff Notice 51-358 reinforced and expanded on the guidance provided in 2010. The intent was to provide issuers, particularly smaller issuers, with guidance on how they might approach preparing disclosures of material climate-related risks. The notice did not create any new legal requirements or modify existing ones.

CSA Staff Notice 51-358 followed the work conducted by the CSA to gather information on the state of climate change-related disclosure in Canada, which was reported in CSA Staff Notice 51-354. The work included a disclosure review, online survey, consultations and research. Based on this work, the CSA noted that it would consider further work including:

• proposing new disclosure requirements in the areas of issuers' governance processes in relation to material risks and opportunities, including the board of directors' (the board) responsibility for oversight and the role played by management, and disclosure of how the issuer oversees the identification, assessment and management of material risks;

• revising NP 58-201 to introduce corporate governance guidelines in the areas contemplated by any such new disclosure requirements;

• providing additional staff guidance on how any such new disclosure requirements apply in the context of climate change-related risk; and

• requiring the disclosure of GHG emissions.

Please refer to Annex E for more details on previous CSA publications.

Developments in Ontario

In 2020, the Ontario government appointed the Capital Markets Modernization Taskforce (Modernization Taskforce) to review and make recommendations in relation to modernizing the capital markets regulatory framework in Ontario. Throughout the Modernization Taskforce's consultations, the increased use of ESG disclosure received significant support from industry stakeholders. In its final report, the Modernization Taskforce recommended mandating disclosure by public companies of material ESG information, specifically climate-related disclosure that is compliant with the final TCFD recommendations (discussed below) for issuers through regulatory filing requirements of the OSC.{4}

The 2021 Ontario Budget subsequently noted the Modernization Taskforce consultation and final recommendations. The Budget also stated that the OSC would begin policy work to inform further regulatory consultation on ESG disclosure.{5}

Please refer to Annex E for more details on Canadian developments.

TCFD Recommendations

In 2015, the Financial Stability Board (FSB) established the TCFD in order to develop recommendations for more effective climate-related disclosures that could promote more informed investment, credit, and insurance underwriting decisions, and enable stakeholders to better understand the concentrations of carbon-related assets in the financial sector and the financial system's exposures to climate-related risks.{6}

In June 2017, the TCFD released its final recommendations, providing a framework for companies and other organizations to develop more effective climate-related financial disclosures through existing reporting practices. The TCFD organized its recommendations of climate-related financial disclosures around four core elements: governance, strategy, risk management, and metrics and targets.

Since the release of the TCFD final recommendations in 2017, there has been growing convergence around disclosure aligned with the TCFD recommendations.{7}

Please also refer to Annex F for more details on the TCFD and other notable international developments.

PART 6 -- Summary of the Proposed Instrument and the Proposed Policy

Application of the Proposed Instrument

The Proposed Instrument would apply to all reporting issuers, other than investment funds, issuers of asset-backed securities, designated foreign issuers, SEC foreign issuers, certain exchangeable security issuers and certain credit support issuers.{8}

Disclosure requirements in the Proposed Instrument

The Proposed Instrument would require an issuer to disclose certain climate-related information in compliance with the TCFD recommendations (subject to certain modifications discussed below). The Modernization Taskforce's report noted that the TCFD recommendations are "a widely prevalent framework that has global support and meets investor needs for concise, standardized metrics on material climate-related issues".{9} Several international jurisdictions are working to adopt the TCFD recommendations into their legal and regulatory frameworks.{10}

The disclosure requirements are set out in Part 2 of the Proposed Instrument, Form 51-107A and Form 51-107B and contemplate disclosure related to the four core elements of the TCFD recommendations:

• governance;

• strategy;

• risk management; and

• metrics and targets.

Details regarding the disclosure requirements are set out in the table below.

Core element in TCFD recommendations |

Related disclosure requirements in the Proposed Instrument |

|

Governance |

Reporting issuers would be required to describe the following: |

Disclose the organization's governance around climate-related risks and opportunities |

|

|

|

• |

the board's oversight of climate-related risks and opportunities |

|

• |

management's role in assessing and managing climate-related risks and opportunities |

|

Strategy |

Reporting issuers would be required to describe the following, where such information is material: |

Disclose the actual and potential impacts of climate-related risks and opportunities on the organization's businesses, strategy, and financial planning where such information is material |

• |

the climate-related risks and opportunities the issuer has identified over the short, medium, and long term |

|

• |

the impact of climate-related risks and opportunities on the issuer's businesses, strategy, and financial planning |

|

Risk management |

Reporting issuers would be required to describe the following: |

Disclose how the organization identifies, assesses, and manages climate-related risks |

|

|

|

• |

the issuer's processes for identifying and assessing climate-related risks |

|

• |

the issuer's processes for managing climate-related risks |

|

• |

how processes for identifying, assessing, and managing climate-related risks are integrated into the issuer's overall risk management |

|

Metrics and targets |

Reporting issuers would be required to disclose: |

Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material |

|

|

|

• |

the metrics used by the issuer to assess climate-related risks and opportunities in line with its strategy and risk management process where such information is material |

|

• |

Scope 1, Scope 2, and Scope 3 GHG emissions, and the related risks or the issuer's reasons for not disclosing this information. The CSA is also consulting on an alternative approach, which would require issuers to disclose Scope 1 GHG emissions. |

|

• |

the targets used by the issuer to manage climate-related risks and opportunities and performance against targets where such information is material |

Modifications to the TCFD recommendations

(1) Scenario analysis

Under the Proposed Instrument, reporting issuers would not be required to provide a "scenario analysis". This disclosure would have described how resilient an issuer's strategies are to climate-related risks and opportunities, taking into consideration a transition to a lower-carbon economy consistent with a 2°C or lower scenario and, where relevant to the issuer, scenarios consistent with increased physical climate-related risks. The CSA have heard concerns from stakeholders regarding scenario analysis, including:

• From an investor perspective, there are concerns regarding the usefulness, consistency and comparability of scenario analysis without a standardized set of assumptions.

• From an issuer perspective, there are concerns with the costs associated with developing scenario analysis. In addition, there are also questions surrounding the appropriate approach and methodology as climate-related scenario analysis may not be perceived as mature at this time.

(2) GHG emissions

Reporting issuers would have to disclose Scope 1, Scope 2, and Scope 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information. This would provide reporting issuers with flexibility in complying with these disclosure requirements. As an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions. Under this alternative, disclosure of Scope 2 and Scope 3 GHG emissions would not be mandatory. Issuers would have to disclose either their Scope 2 and 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information.

The Proposed Instrument would also provide issuers with flexibility in providing GHG disclosure in accordance with a "GHG emissions reporting standard". As discussed in the Proposed Policy, a GHG emissions reporting standard is the GHG Protocol, or a reporting standard for calculating and reporting GHG emissions if it is comparable with the GHG Protocol. Where an issuer uses a reporting standard that is not the GHG Protocol, it would also be required to disclose how the reporting standard used is comparable with the GHG Protocol. This approach enables issuers to utilize alternative methodologies, while facilitating comparability between issuers providing GHG disclosure.

Location of disclosure

The climate-related disclosure requirements relating to governance would be included in a reporting issuer's management information circular. For issuers that do not send a management information circular to its securityholders, the disclosure would be provided in the issuer's annual information form (AIF) or its annual management's discussion and analysis (MD&A), if the issuer does not file an AIF.{11}

The climate-related disclosures related to strategy, risk management and metrics and targets specified by the Proposed Instrument would be included in the reporting issuer's AIF, or its annual MD&A, if the issuer does not file an AIF.

Transition

To facilitate a proportionate approach, the Proposed Instrument contemplates a phased-in transition of the disclosure requirements over one and three-year periods. The length of the transition phase would depend on the issuer's status as a venture or non-venture issuer, with non-venture issuers being required to comply with the proposed disclosure requirements first.

The following table sets out when non-venture and venture issuers would be required to comply with the Proposed Instrument.

Category of issuer |

Transition phase |

|

Non-venture issuers |

Financial years beginning on or after January 1 of the first year after the effective date of the Proposed Instrument (one-year transition phase) |

|

Venture Issuers |

Financial years beginning on or after January 1 of the third year after the effective date of the Proposed Instrument (three-year transition phase) |

The following illustrates how the transition periods would work in practice for a reporting issuer with a December 31 financial year-end. The illustration assumes that the Proposed Instrument would come into force on December 31, 2022.

Category of issuer |

Transition requirements |

|

Non-venture issuers |

Disclosure requirements would apply to annual filings in respect of the financial year ending <<December 31, 2023>> |

|

These annual filings would be due in <<March 2024>> |

Venture Issuers |

Disclosure requirements would apply to annual filings in respect of the financial year ending <<December 31, 2025>> |

|

These annual filings would be due in <<April 2026>> |

Summary of the Proposed Policy

The purpose of the Proposed Policy is to provide guidance relating to how the CSA intend to interpret and apply the Proposed Instrument. The Proposed Policy includes a discussion regarding the following:

(1) Summary of TCFD Recommendations

The disclosure requirements of the Proposed Instrument are set out in Form 51-107A and 51-107B and, subject to certain modifications, are consistent with the TCFD recommendations. Notably, the Proposed Instrument does not require issuers to disclose scenario analysis, which is the TCFD recommended disclosure that describes the resilience of an issuer's strategy, taking into consideration different climate-related scenarios. In addition, issuers may elect to not disclose the TCFD recommended disclosure respecting GHG emissions and their related risks, provided they instead disclose their reasons for not including this disclosure. As noted above, as an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions. The alternative requirement is set out in a text box in Annex A.

(2) Materiality

Materiality is the determining factor in any assessment of whether information is required to be disclosed in an issuer's continuous disclosure. Only material information needs to be included in an issuer's Form 51-102F1 Management's Discussion and Analysis (Form 51-102F1) and Form 51-102F2 Annual Information Form (Form 51-102F2). For purposes of those forms, information is likely material if a reasonable investor's decision whether to buy, sell or hold securities in an issuer would likely be influenced or changed if the information in question was omitted or misstated.

Consistent with the TCFD recommendations and with disclosure requirements respecting corporate governance matters under NI 58-101, however, the disclosure required by the Proposed Instrument relating to the climate-related "Governance" and "Risk Management" are not subject to a materiality assessment. Accordingly, issuers must provide this disclosure in the applicable continuous disclosure document as required by the Proposed Instrument.

(3) GHG Emissions

Item 4(a) of Form 51-107B requires an issuer to disclose each of its Scope 1, Scope 2 and Scope 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information. Accordingly, where an issuer has disclosed its Scope 1 and Scope 2 GHG emissions but has elected to not disclose its Scope 3 GHG emissions, the issuer would be required to disclose its reasons for not providing this information. Where an issuer has elected to not disclose any GHG emissions, the issuer may provide its reasons for not doing so in respect of GHG emissions as a whole, as opposed to a separate explanation for each scope.

Certain issuers are already required to disclose GHG emissions under existing reporting programs, including for example, on a per facility basis under the federal Greenhouse Gas Reporting Program. The CSA expect issuers that are subject to an existing GHG emissions reporting program to disclose Scope 1 GHG emissions under the Proposed Instrument. However, should they elect not to disclose Scope 1 GHG emissions under the Proposed Instrument, they should clearly explain their election in light of such preexisting reporting obligations.

Subsection 4(2) of the Proposed Instrument requires an issuer to use a GHG emissions reporting standard to calculate and report its GHG emissions. A GHG emissions reporting standard is the GHG Protocol, or a reporting standard for calculating and reporting GHG emissions if it is comparable with the GHG Protocol. Issuers that provide GHG disclosure using a reporting standard that is not the GHG Protocol, must disclose how such standard is comparable with the GHG Protocol.

(4) Forward-Looking Information

Disclosure provided by issuers pursuant to the Proposed Instrument may constitute forward-looking information (FLI). When an issuer discloses FLI, it must comply with the requirements set out in Part 4A, Part 4B and section 5.8 of NI 51-102.

PART 7 -- Annexes

The following annexes are attached to this notice:

• Annex A -- Proposed Instrument

• Annex B -- Proposed Policy

• Annex C -- Existing Securities Legislation

• Annex D -- CSA Disclosure Review

• Annex E -- Domestic Developments

• Annex F -- International Developments

• Where applicable, Annex G -- Local Matters

PART 8 -- Alternatives Considered and Reliance on Unpublished Studies, etc.

Alternatives considered

At this time, based on our ongoing review of developments in this area, as well as the recommendations of the Modernization Taskforce, the CSA are of the view that it is important to propose climate-related disclosure requirements rather than maintain the status quo. The CSA have previously issued staff guidance in relation to climate-related disclosure. The Proposed Instrument builds on the further work contemplated in CSA Staff Notice 51-354, specifically the contemplation of new climate-related disclosure requirements related to issuer governance processes and material risks and opportunities and GHG emissions. No alternatives to rule-making are being considered by the CSA at the present time.

As described in greater detail in Part 5 and Annex D, the CSA's 2021 Disclosure Review found that issuers are providing more climate-related information compared with the 2017 review findings published in CSA Staff Notice 51-354. While the review found that some aspects of climate-related disclosure have improved, there continue to be areas where reporting issuer disclosure could be improved further. These findings are consistent with some of the concerns noted by the CSA on the current state of climate-related disclosures in Part 2.

Throughout the Modernization Taskforce's consultations, the increased use of ESG disclosure received significant support from a variety of stakeholders, including issuers, investment firms, banks and law firms.

The Proposed Instrument reflects the growing international convergence around the TCFD recommendations. In developing the Proposed Instrument, the CSA reviewed the TCFD recommendations and developments in Australia, New Zealand, Switzerland, the United Kingdom, the European Union and the United States. The CSA also reviewed the recent proposals by the International Financial Reporting Standards Foundation (IFRS Foundation), the prototype climate standard developed by the group of five sustainability reporting organizations and the Report on Sustainability-related Issuer Disclosures Final Report by the International Organization of Securities Commissions (IOSCO) Sustainable Finance Task Force.

We note that the CSA has expressed support for the IFRS Foundation's proposal to establish a sustainability standards board and believe that its development, including its focus initially on climate-related disclosure that builds on the TCFD recommendations, will result in standards that are complementary to the Proposed Instrument. The Proposed Instrument will facilitate the provision of useful information to investors and our market's eventual transition towards international standards. The CSA will continue to monitor international developments, including the developments by the IFRS Foundation, to further inform our approach.

Reliance on unpublished studies, etc.

In developing the Proposed Instrument, the CSA did not rely upon any significant unpublished study, report or other written materials.

PART 9 -- Local Matters

Where applicable, Annex G is being published in any local jurisdiction that is making related changes to local securities laws, including local notices or other policy instruments in that jurisdiction. It also includes any additional information that is relevant to that jurisdiction only.

PART 10 -- Request for Comments

We welcome your comments on the Proposed Instrument and Proposed Policy and also invite comments on the following specific questions. In each instance, please provide an explanation for your answer.

Experience with TCFD recommendations

1. For reporting issuers that have provided climate-related disclosures voluntarily in accordance with the TCFD recommendations, what has been the experience generally in providing those disclosures?

Disclosure of GHG Emissions and Scenario Analysis

2. For reporting issuers, do you currently disclose GHG emissions on a voluntary basis? If so, are the GHG emissions calculated in accordance with the GHG Protocol?

3. For reporting issuers, do you currently conduct climate scenario analysis (regardless of whether the analysis is disclosed)? If so, what are the benefits and challenges with preparing and/or disclosing the analysis?

4. Under the Proposed Instrument, scenario analysis would not be required. Is this approach appropriate? Should the Proposed Instrument require this disclosure? Should issuers have the option to not provide this disclosure and explain why they have not done so?

5. The TCFD recommendations contemplate disclosure of GHG emissions, where such information is material.

• The Proposed Instrument contemplates issuers having the option to disclose GHG emissions or explain why they have not done so. Is this approach appropriate?

• As an alternative, the CSA is consulting on requiring issuers to disclose Scope 1 GHG emissions. Is this approach appropriate? Should disclosure of Scope 1 GHG emissions only be required where such information is material?

• Should disclosure of Scope 2 GHG emissions and Scope 3 GHG emissions be mandatory?

• For those issuers who are already required to report GHG emissions under existing federal or provincial legislation, would the requirement in the Proposed Instrument to include GHG emissions in the issuer's AIF or annual MD&A (if an issuer elects to disclose these emissions) present a timing challenge given the respective filing deadlines? If so, what is the best way to address this timing challenge?

6. The Proposed Instrument contemplates that issuers that provide GHG disclosures would be required to use a GHG emissions reporting standard in measuring their GHG emissions, being the GHG Protocol or a reporting standard comparable with the GHG Protocol (as described in the Proposed Policy). Further, where an issuer uses a reporting standard that is not the GHG Protocol, it would be required to disclose how the reporting standard used is comparable with the GHG Protocol.

• As issuers have the option of providing GHG disclosures, should a specific reporting standard, such as the GHG Protocol, be mandated when such disclosures are provided?

• Is the GHG Protocol appropriate for all reporting issuers? Should issuers be given the flexibility to use alternative reporting standards that are comparable with the GHG Protocol?

• Are there other reporting standards that address the disclosure needs of users or the different circumstances of issuers across multiple industries and should they be specifically identified as suitable methodologies?

7. The Proposed Instrument does not require the GHG emissions to be audited. Should there be a requirement for some form of assurance on GHG emissions reporting?

8. The Proposed Instrument permits an issuer to incorporate GHG disclosure by reference to another document. Is this appropriate? Should this be expanded to include other disclosure requirements of the Proposed Instrument?

Usefulness and benefits of disclosures contemplated by the Proposed Instrument

9. What climate-related information is most important for investors' investment and voting decisions? How is this information incorporated into these decisions? Is there additional information that investors require?

10. What are the anticipated benefits associated with providing the disclosures contemplated by the Proposed Instrument? How would the Proposed Instrument enhance the current level of climate-related disclosures provided by reporting issuers in Canada?

Costs and challenges of disclosures contemplated by the Proposed Instrument

11. What are the anticipated costs and challenges associated with providing the disclosures contemplated by the Proposed Instrument?

12. Do the costs and challenges vary among the four core TCFD recommendations related to governance, strategy, risk management, and metrics and targets? For example, are some of the disclosures more (or less) challenging to prepare?

13. The costs of obtaining and presenting new disclosures may be proportionally greater for venture issuers that may have scarce resources. Would more accommodations for venture issuers be needed? If so, what accommodations would address these concerns while still balancing the reasonable information needs of investors? Alternatively, should venture issuers be exempted from some or all of the requirements of the Proposed Instrument?

Guidance on disclosure requirements

14. We have provided guidance in the Proposed Policy on the disclosure required by the Proposed Instrument. Are there any other tools, guidance or data sources that would be helpful in preparing these disclosures that the Proposed Policy should refer to?

15. Does the guidance set out in the Proposed Policy sufficiently explain the interaction of the risk disclosure requirement in the Proposed Instrument with the existing risk disclosure requirements in NI 51-102?

Prospectus Disclosure

16. Form 41-101F1 Information Required in a Prospectus does not contain the climate-related disclosure requirements contemplated by the Proposed Instrument. Should an issuer be required to include the disclosure required by the Proposed Instrument in a long form prospectus? If so, at what point during the phased-in implementation of the Proposed Instrument should these disclosure requirements apply in the context of a long form prospectus?

Phased-in implementation

17. The Proposed Instrument contemplates a phased-in transition of the disclosure requirements, with non-venture issuers subject to a one-year transition phase and venture issuers subject to a three-year transition phase. Assuming the Proposed Instrument comes into force December 31, 2022 and the issuer has a December 31 year-end, these disclosures would be included in annual filings due in 2024 and 2026 for non-venture issuers and venture issuers, respectively.

• Would the transition provisions in the Proposed Instrument provide reporting issuers with sufficient time to review the Proposed Instrument and prepare and file the required disclosures?

• Does the phased-in implementation based on non-venture or venture status address the concerns, if any, regarding the challenges and costs associated with providing the disclosures contemplated by the Proposed Instrument, particularly for venture issuers? If not, how could these concerns be addressed?

Future ESG considerations

18. In its comment letter to the IFRS Foundation's consultation paper published in September 2020, the CSA stated that developing a global set of sustainability reporting standards for climate-- related information is an appropriate starting point, with broader environmental factors and other sustainability topics to be considered in the future. What broader sustainability or ESG topics should be prioritized for the future?

PART 11 -- How to Provide Comments

Please submit your comments in writing on or before January 17, 2022. If you are not sending your comments by email, please send us an electronic file containing the submissions (in Microsoft Word Format).

Address your submission to the CSA jurisdictions as follows:

Alberta Securities Commission

Autorité des marchés financiers

British Columbia Securities Commission

Financial and Consumer Services Commission, New Brunswick

Financial and Consumer Affairs Authority of Saskatchewan

Manitoba Securities Commission

Nova Scotia Securities Commission

Nunavut Securities Office

Office of the Superintendent of Securities, Newfoundland and Labrador

Ontario Securities Commission

Office of the Superintendent of Securities, Northwest Territories

Office of the Yukon Superintendent of Securities

Superintendent of Securities, Department of Justice and Public Safety, Prince Edward Island

Deliver your comments only to the addresses listed below. Your comments will be distributed to the remaining jurisdictions.

The Secretary

Ontario Securities Commission

20 Queen Street West

22nd Floor, Box 55

Toronto, Ontario

M5H 3S8

Fax: 416-593-2318

comment@osc.gov.on.ca

Me Philippe Lebel

Corporate Secretary and Executive Director, Legal Affairs

Autorité des marchés financiers

Place de la Cité, tour Cominar

2640, boulevard Laurier, bureau 400

Québec (Québec) G1V 5C1

Fax: 514-864-6381

consultation-en-cours@lautorite.qc.ca

Comments received will be publicly available

We cannot keep submissions confidential because securities legislation in certain provinces requires publication of the written comments received during the comment period. All comments received will be posted on the websites of each of the Autorité des marchés financiers at www.lautorite.qc.ca. Therefore, you should not include personal information directly in comments to be published. It is important that you state on whose behalf you are making the submission.

PART 12 -- Questions

If you have any questions, please contact any of the CSA staff listed below.

<<Ontario Securities Commission>> |

|

Jo-Anne Matear |

Samreen Beg |

Manager, Corporate Finance |

Senior Legal Counsel, Corporate Finance |

416 593-2323 |

416 597-7817 |

jmatear@osc.gov.on.ca |

sbeg@osc.gov.on.ca |

|

Katie DeBartolo |

Steven Oh |

Senior Accountant, Corporate Finance |

Senior Legal Counsel, Corporate Finance |

416 593-2166 |

416 595-8778 |

kdebartolo@osc.gov.on.ca |

soh@osc.gov.on.ca |

|

<<Alberta Securities Commission>> |

Timothy Robson |

Tonya Fleming |

Manager, Legal, Corporate Finance |

Senior Legal Counsel, Corporate Finance |

403 355-6297 |

403 355-9032 |

timothy.robson@asc.ca |

tonya.fleming@asc.ca |

|

Kyra Plata |

Jan Bagh |

Securities Analyst, Corporate Finance |

Senior Legal Counsel, Corporate Finance |

403 297-8893 |

403 355-2804 |

kyra.plata@asc.ca |

jan.bagh@asc.ca |

|

<<Autorité des marchés financiers>> |

|

Suzanne Poulin |

Martin Latulippe |

Chief Accountant, |

Senior Policy Advisor, |

Direction de l'information financière |

Direction de l'information continue |

514 395-0337, ext.4411 |

514 395-0337, ext. 4331 |

suzanne.poulin@lautorite.qc.ca |

martin.latulippe@lautorite.qc.ca |

|

<<British Columbia Securities Commission>> |

|

Melody Chen |

Nazma Lee |

Senior Legal Counsel |

Senior Legal Counsel |

Legal Services, Corporate Finance |

Legal Services, Corporate Finance |

604-899-6530 |

604-899-6867 |

mchen@bcsc.bc.ca |

nlee@bcsc.bc.ca |

|

Victoria Yehl |

|

Senior Geologist, Corporate Finance |

|

604-899-6519 |

|

vyehl@bcsc.bc.ca |

|

|

<<Financial and Consumer Services Commission, New Brunswick>> |

|

Ella-Jane Loomis |

|

Senior Legal Counsel |

|

506 453-6591 |

|

ella-jane.loomis@fcnb.ca |

|

|

<<Financial and Consumer Affairs Authority of Saskatchewan>> |

|

Heather Kuchuran |

|

Director, Corporate Finance |

|

306 787-1009 |

|

heather.kuchuran@gov.sk.ca |

|

|

<<Manitoba Securities Commission>> |

|

Wayne Bridgeman |

Patrick Weeks |

Deputy Director, Corporate Finance |

Senior Analyst, Corporate Finance |

204 945-4905 |

204 945-3326 |

wayne.bridgeman@gov.mb.ca |

patrick.weeks@gov.mb.ca |

|

<<Nova Scotia Securities Commission>> |

|

Abel Lazarus |

Jack Jiang |

Director, Corporate Finance |

Securities Analyst, Corporate Finance |

902 424-6859 |

902 424-7059 |

abel.lazarus@novascotia.ca |

jack.jiang@novascotia.ca |

{1} As an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions. Under this alternative, disclosure of Scope 2 and Scope 3 GHG emissions would not be mandatory. Issuers would have to disclose either their Scope 2 and 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information.

{2} Assuming the Proposed Instrument comes into force December 31, 2022 and an issuer has a December 31 year-end, these disclosures would be included in annual filings due in 2024 and 2026 for non-venture issuers and venture issuers, respectively.

{3} The Alberta Securities Commission, Autorité des marchés financiers, British Columbia Securities Commission, Financial and Consumer Affairs Authority of Saskatchewan, Financial and Consumer Services Commission of New Brunswick, and the Ontario Securities Commission.

{4} Capital Markets Modernization Taskforce Final Report (January 2021), online: <https://files.ontario.ca/books/mof-capital-- markets-modernization-taskforce-final-report-en-2021-01-22-v2.pdf>, p. 71.

{5} Ontario's Action Plan : Protecting People's Health and Our Economy (2021 Ontario Budget), online: <https://budget.ontario.ca/2021/pdf/2021-ontario-budget-en.pdf> at p. 113.

{6} Task Force on Climate-related Financial Disclosures, online: <https://www.fsb-tcfd.org>.

{7} For example, the United Kingdom recently adopted disclosure rules for premium listed issuers that require issuers to ensure their disclosures are aligned with the TCFD recommendations. The IFRS Foundation also recently announced that a new sustainability standards board would build on the TCFD recommendations. In Canada, CEOs of Canada's eight largest pension plan investment managers, in a statement released in November 2020, cited the TCFD as one disclosure standard that companies should adopt. In 2018, the federal government's Expert Panel on Sustainable Finance also recommended defining and pursuing "a Canadian approach to implementing the recommendations of the TCFD." Please see Annexes E and F for more information.

{8} Please refer to section 1.2 of the Proposed Instrument.

{9} Capital Markets Modernization Taskforce Final Report (January 2021), online: <https://files.ontario.ca/books/mof-capital-- markets-modernization-taskforce-final-report-en-2021-01-22-v2.pdf>, p. 70.

{10} IOSCO, Report on Sustainability-related Issuer Disclosures Final Report (June 28, 2021), online: < https://www.iosco.org/library/pubdocs/pdf/IOSCOPD678.pdf>, p. 2.

{11} We note that the CSA published for comment in May 2021 Proposed Amendments to National Instrument 51-102 Continuous Disclosure Obligations and Other Amendments and Changes Relating to Annual and Interim Filings of Non-Investment Fund Reporting Issuers, which contemplates amendments to the continuous disclosure regime to combine the financial statements, MD&A and AIF into one reporting document called the annual disclosure statement for annual reporting purposes, and the interim disclosure statement for interim reporting purposes.

Annex A -- Proposed Instrument

PROPOSED NATIONAL INSTRUMENT 51-107 DISCLOSURE OF CLIMATE-RELATED MATTERS

Part 1 |

Definitions and Interpretation |

1. |

Definitions |

2. |

Application |

|

Part 2 |

Disclosure Requirements |

3. |

Climate-related Governance Disclosure Requirements |

4. |

Climate-related Strategy, Risk Management and Metrics and Targets Disclosure Requirements |

|

Part 3 |

Exemption and Effective Date |

5. |

Exemption |

6. |

Effective Date and Transition |

PART 1 DEFINITIONS AND INTERPRETATION

Definitions

1. In this Instrument

"AIF" has the meaning ascribed to it in National Instrument 51-102 Continuous Disclosure Obligations;

"asset-backed security" has the meaning ascribed to it in National Instrument 51-102 Continuous Disclosure Obligations;

"designated foreign issuer" has the meaning ascribed to it in National Instrument 71-102 Continuous Disclosure and Other Exemptions Relating to Foreign Issuers;

"GHG" means greenhouse gas;

"GHG emissions reporting standard" means the GHG Protocol, or a reporting standard for calculating and reporting GHG emissions that is comparable with the GHG Protocol;

"GHG Protocol" means the greenhouse gas reporting standards for calculating and reporting GHG emissions by companies and organizations as developed by the World Resources Institute and World Business Council for Sustainable Development;

"marketplace" has the meaning ascribed to it in National Instrument 51-102 Continuous Disclosure Obligations;

"MD&A" has the meaning ascribed to it in National Instrument 51-102 Continuous Disclosure Obligations;

"Scope 1" means all direct GHG emissions by an issuer;

"Scope 2" means all indirect GHG emissions arising from an issuer's consumption of purchased electricity, heat or steam;

"Scope 3" means all other indirect GHG emissions of an issuer, other than those described in the definition of Scope 2;

"SEC foreign issuer" has the meaning ascribed to it in National Instrument 71-102 Continuous Disclosure and Other Exemptions Relating to Foreign Issuers;

"subsidiary entity" has the meaning ascribed to it in National Instrument 52-110 Audit Committees;

"U.S. marketplace" has the meaning ascribed to it in National Instrument 51-102 Continuous Disclosure Obligations;

"venture issuer" has the meaning ascribed to it in National Instrument 58-101 Disclosure of Corporate Governance Practices.

Application

2. This Instrument applies to a reporting issuer other than a reporting issuer that is any of the following:

(a) an investment fund;

(b) an issuer of an asset-backed security;

(c) a designated foreign issuer or SEC foreign issuer;

(d) an exchangeable security issuer that is exempt under section 13.3 of National Instrument 51-102 Continuous Disclosure Obligations;

(e) a credit support issuer that is exempt under section 13.4 of National Instrument 51-102 Continuous Disclosure Obligations;

(f) an issuer that is a subsidiary entity, if

(i) the subsidiary entity does not have equity securities, other than non-convertible, non-participating preferred securities, trading on a marketplace, and

(ii) the parent of the subsidiary entity is

(A) subject to the requirements of this Instrument, or

(B) an issuer that has securities listed or quoted on a U.S. marketplace, and is in compliance with the corporate governance disclosure requirements of that U.S. marketplace.

PART 2 DISCLOSURE REQUIREMENTS

Climate-related Governance Disclosure Requirements

3.

(1) If management of a reporting issuer solicits a proxy from a security holder of the issuer for the purpose of electing directors to the reporting issuer's board of directors, the issuer must include in its management information circular the disclosure referred to in Form 51-107A.

(2) A reporting issuer that does not send a management information circular to its security holders must include the disclosure referred to in Form 51-107A in its AIF, or if it does not file an AIF, in its annual MD&A.

Climate-related Strategy, Risk Management and Metrics and Targets Disclosure Requirements

4.

(1) A reporting issuer must include the disclosure referred to in Form 51-107B in its AIF, or if it does not file an AIF, in its annual MD&A.

(2) A reporting issuer that includes the disclosure of GHG emissions referred to in Form 51-107B in its AIF or annual MD&A must use a GHG emissions reporting standard to calculate and report its GHG emissions.

PART 3 EXEMPTION AND EFFECTIVE DATE

Exemption

5.

(1) The regulator or securities regulatory authority may grant an exemption from this Instrument, in whole or in part, subject to such conditions or restrictions as may be imposed in the exemption.

(2) Despite subsection (1), in Ontario, only the regulator may grant such an exemption.

(3) Except in Ontario, an exemption referred to in subsection (1) is granted under the statute referred to in Appendix B of National Instrument 14-101 Definitions, opposite the name of the local jurisdiction.

Effective Date and Transition

6.

(1) This Instrument comes into force on [•].

(2) This Instrument applies:

(a) in the case of a reporting issuer other than a venture issuer, in respect of each financial year beginning on or after [January 1 of the first year after [•];

(b) in the case of a venture issuer, in respect of each financial year beginning on or after [January 1 of the third year after [•].

FORM 51-107A CLIMATE-RELATED GOVERNANCE DISCLOSURE

1. Governance

(a) Describe the board of directors' oversight of climate-related risks and opportunities.

(b) Describe management's role in assessing and managing climate-related risks and opportunities.

INSTRUCTION:

This Form applies to corporate and non-corporate entities. Reference to a particular corporate characteristic, such as a board of directors, includes any equivalent characteristic of a non-corporate entity. Income trust issuers must provide disclosure in a manner that recognizes that certain functions of a corporate issuer, its board of directors and its management may be performed by any or all of the trustees, the board of directors or management of a subsidiary of the trust, or the board of directors, management or employees of a management company. In the case of an income trust, references to "the issuer" refer to both the trust and any underlying entities, including the operating entity.

FORM 51-107B CLIMATE-RELATED STRATEGY, RISK MANAGEMENT AND METRICS AND TARGETS DISCLOSURE

1. Strategy

(a) Describe the climate-related risks and opportunities the issuer has identified over the short, medium, and long term.

(b) Describe the impact of climate-related risks and opportunities on the issuer's businesses, strategy, and financial planning.

2. Risk Management

(a) Describe the issuer's processes for identifying and assessing climate-related risks.

(b) Describe the issuer's processes for managing climate-related risks.

(c) Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the issuer's overall risk management.

3. Metrics and Targets

(a) Disclose the metrics used by the issuer to assess climate-related risks and opportunities in line with its strategy and risk management process.

(b) Describe the targets used by the issuer to manage climate-related risks and opportunities and the issuer's performance against these targets.

4. GHG Emissions

(a) Disclose:

(i) the issuer's Scope 1 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information,

(ii) the issuer's Scope 2 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information, and

(iii) the issuer's Scope 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information.

(b) disclose the reporting standard used by the issuer to calculate and disclose the GHG emissions referred to in (a).

(c) If the reporting standard referred to in (b) is not the GHG Protocol, disclose how the reporting standard used by the issuer is comparable with the GHG Protocol.

- - - - - - - - - - - - - - - - - - - -

As an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions either a) when that information is material, or b) in all cases. Under this alternative, disclosure of Scope 2 and Scope 3 GHG emissions would not be mandatory. Issuers would have to disclose either their Scope 2 and 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information. Text reflecting this alternative disclosure requirement for Scope 1 GHG emissions in all cases is set out below.

GHG Emissions

(a) Disclose:

(i) the issuer's Scope 1 GHG emissions and the related risks,

(ii) the issuer's Scope 2 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information, and

(iii) the issuer's Scope 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information.

(b) disclose the reporting standard used by the issuer to calculate and disclose the GHG emissions referred to in (a).

(c) If the reporting standard referred to in (b) is not the GHG Protocol, disclose how the reporting standard used by the issuer is comparable with the GHG Protocol.

- - - - - - - - - - - - - - - - - - - -

INSTRUCTIONS:

(1) This Form applies to both corporate and non-corporate entities. Income trust issuers must provide disclosure in a manner that recognizes that certain functions of a corporate issuer, its board of directors and its management may be performed by any or all of the trustees, the board of directors or management of a subsidiary of the trust, or the board of directors, management or employees of a management company. In the case of an income trust, references to "the issuer" refer to both the trust and any underlying entities, including the operating entity.

(2) An issuer is not required to disclose information that is not material in respect of items 1 and 3. An issuer must exercise judgment when it determines whether information is material in respect of the issuer. Would a reasonable investor's decision whether or not to buy, sell or hold securities in the issuer likely be influenced or changed if the information in question was omitted or misstated? If so, the information is likely material.

(3) An issuer may incorporate information required to be disclosed under Item 4 by reference to another document. The issuer must clearly identify the reference document or any excerpt of it that the issuer incorporates into the disclosure provided under Item 4. Unless the issuer has already filed the reference document or excerpt under its SEDAR profile, the issuer must file it at the same time as it files the document containing the disclosure required under this Form.

Annex B -- Proposed Policy

PROPOSED COMPANION POLICY 51-107CP DISCLOSURE OF CLIMATE-RELATED MATTERS

PART 1 GENERAL

Introduction and Purpose

1. National Instrument 51-107 Disclosure of Climate-Related Matters (the "Instrument") establishes disclosure requirements regarding climate-related matters for reporting issuers (other than investment funds, issuers of asset-backed securities, designated foreign issuers, SEC foreign issuers, certain exchangeable security issuers and certain credit support issuers).

We have implemented the Instrument to require reporting issuers to disclose certain climate-related information in their continuous disclosure documents. We believe that climate-related information is becoming increasingly important to investors in Canada and internationally, and that the disclosure required by the Instrument is an important element to their investment and voting decisions.

This companion policy (the "Policy") provides information regarding the interpretation and application of the Instrument.

PART 2 TCFD RECOMMENDATIONS

TCFD Recommendations

2.

(1) The disclosure requirements of the Instrument are set out in Form 51-107A and Form 51-107B and, subject to certain modifications, are consistent with the recommendations (the "TCFD recommendations") developed by the Task Force on Climate-related Financial Disclosures (the "TCFD") and published in their report entitled Recommendations of the Task Force on Climate-related Financial Disclosures dated June 2017 (the "TCFD Final Report"). Notably, the Instrument does not require issuers to disclose a scenario analysis, which is the TCFD recommended disclosure that describes the resilience of an issuer's strategy, taking into consideration different climate-related scenarios. In addition, issuers may elect to not provide the TCFD recommended disclosure respecting greenhouse gas ("GHG") emissions and their related risks, provided they instead disclose their reasons for not including this disclosure.{12}

(2) The TCFD recommendations are summarized in Figure 4 of Section C of the TCFD Final Report and are reproduced in Table 1 below. Table 1 also illustrates the modifications to the TCFD recommended disclosures required by the Instrument:

Table 1: TCFD Recommendations and disclosure required by the Instrument

TCFD Recommendations |

TCFD Recommended Disclosures |

Disclosure required by the Instrument |

|

Governance |

a) Describe the board's oversight of climate-related risks and opportunities. |

a) Same as TCFD Recommended Disclosures. |

Disclose the organization's governance around climate-related risks and opportunities. |

b) Describe management's role in assessing and managing climate-related risks and opportunities. |

b) Same as TCFD Recommended Disclosures. |

|

Strategy |

a) Describe the climate-related risks and opportunities the organization has identified over the short, medium, and long term. |

a) Same as TCFD Recommended Disclosures. |

Disclose the actual and potential impacts of climate-related risks and opportunities on the organization's businesses, strategy, and financial planning where such information is material. |

b) Describe the impact of climate-- related risks and opportunities on the organization's businesses, strategy, and financial planning. |

b) Same as TCFD Recommended Disclosures. |

|

c) Describe the resilience of the organization's strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario. |

c) Not required. |

|

Risk management |

a) Describe the organization's processes for identifying and assessing climate-related risks. |

a) Same as TCFD Recommended Disclosures. |

Disclose how the organization identifies, assesses, and manages climate-related risks. |

b) Describe the organization's processes for managing climate-related risks. |

b) Same as TCFD Recommended Disclosures. |

|

c) Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the organization's overall risk management. |

c) Same as TCFD Recommended Disclosures. |

|

Metrics and targets |

a) Disclose the metrics used by the organization to assess climate-related risks and opportunities in line with its strategy and risk management process. |

a) Same as TCFD Recommended Disclosures. |

Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material. |

b) Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks. |

b) Not mandatory. An issuer must disclose its GHG emissions and the related risks or the issuer's reasons for not disclosing this information. |

|

c) Describe the targets used by the organization to manage climate-related risks and opportunities and performance against targets. |

c) Same as TCFD Recommended Disclosures. |

(3) Consistent with the TCFD recommendations and with disclosure requirements respecting corporate governance matters under National Instrument 58-101 Disclosure of Corporate Governance Practices, the disclosure required by the Instrument relating to the TCFD recommendation "Governance" and "Risk management" in Table 1 above are not subject to a materiality assessment. Accordingly, issuers must provide this disclosure in the applicable continuous disclosure document as required by the Instrument.

Disclosure under the headings "Strategy" and "Metrics and targets" is only required where such information is material. Information is likely material if a reasonable investor's decision whether to buy, sell or hold securities in an issuer would likely be influenced or changed if the information in question was omitted or misstated.

- - - - - - - - - - - - - - - - - - - -

An issuer must disclose its GHG emissions and the related risks or the issuer's reasons for not disclosing this information. As an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions either a) when that information is material, or b) in all cases. Under this alternative, disclosure of Scope 2 and Scope 3 GHG emissions would not be mandatory. Issuers would have to disclose either their Scope 2 and 3 GHG emissions and the related risks, or the issuer's reasons for not disclosing this information. If necessary, the final form of Policy will be modified to reflect the alternative chosen.

- - - - - - - - - - - - - - - - - - - -

TCFD and Other Guidance

3. The TCFD recommendations and their application are discussed more fully in the TCFD Final Report, as well as in other publications produced by the TCFD, such as:

(a) Implementing the Recommendations of the Task Force on Climate-related Financial Disclosures (June 2017); and

(b) Guidance on Risk Management Integration and Disclosure (October 2020).

In addition to this Policy, issuers should consider the TCFD Final Report and related publications from the TCFD in preparing the disclosure required by the Instrument. Issuers should also refer to guidance published by the CSA relating to assessing materiality and existing disclosure requirements that are consistent with the TCFD recommendations (as discussed below), including:

(a) National Policy 51-201 Disclosure Standards;

(b) CSA Staff Notice 51-333 Environmental Reporting Guidance (October 2010);

(c) CSA Staff Notice 51-354 Report on Climate Change-related Disclosures Project (April 2018); and

(d) CSA Staff Notice 51-358 Reporting of Climate Change-related Risks (August 2019).

Consistency with Existing Disclosure Requirements

4. Certain disclosure requirements contained in the Instrument are consistent with pre-existing disclosure requirements under Canadian securities legislation. For example, item 1 (a) of Form 51-107B requires issuers to describe the climate-related risks and opportunities it has identified over the short, medium, and long term. This disclosure requirement is consistent with risk factor disclosure required under National Instrument 51-102 Continuous Disclosure Obligations. An issuer is required to disclose in its annual information form, if any, risk factors relating to it and its business that would be most likely to influence an investor's decision to purchase the issuer's securities, and an issuer is required to discuss in its annual management's discussion and analysis its analysis of its operations for the most recently completed financial year, including commitments, events, risks or uncertainties that it reasonably believes will materially affect its future performance.

Greenhouse Gas Emissions Disclosure

5.

(1) Item 4(a) of Form 51-107B requires an issuer to disclose each of its Scope 1, Scope 2 and Scope 3 GHG emissions or explain why it has not done so. Accordingly, where an issuer has disclosed its Scope 1 and Scope 2 GHG emissions but has elected to not disclose its Scope 3 GHG emissions, the issuer would be required to disclose its reasons for not providing its Scope 3 GHG emissions. Where an issuer has elected to not disclose any GHG emissions, the issuer may provide its reasons for not doing so in respect of GHG emissions as a whole, as opposed to a separate explanation for each scope.

(2) Certain issuers are already required to disclose GHG emissions under existing reporting programs, including for example, on a per facility basis under the federal Greenhouse Gas Reporting Program. The securities regulatory authorities expect issuers that are subject to an existing GHG emissions reporting program to disclose Scope 1 GHG emissions under the Instrument. However, should they elect to not disclose Scope 1 GHG emissions under the Instrument, they should clearly explain their election in light of such pre-existing reporting obligations.

(3) Subsection 4(2) of the Instrument requires an issuer to use a GHG emissions reporting standard to calculate and report its GHG emissions. A GHG emissions reporting standard is the GHG Protocol, or a reporting standard for calculating and reporting GHG emissions if it is comparable with the GHG Protocol. Accordingly, pursuant to item 4(c) of Form 51-107B, issuers who disclose GHG emissions using a reporting standard that is not the GHG Protocol must disclose how such standard is comparable with the GHG Protocol.

(4) Form 51-107B permits an issuer to incorporate GHG disclosure by reference to another document. If doing so, the issuer must clearly identify the reference document or any excerpt of it that the issuer incorporates into the disclosure provided under Item 4 of Form 51-107B. Unless the issuer has already filed the reference document or excerpt under its SEDAR profile, the issuer must file it at the same time as it files the document containing the disclosure required under Form 51-107B.

Forward Looking Information

6. Disclosure provided by issuers pursuant to the Instrument may constitute forward-looking information ("FLI"). If an issuer discloses FLI, it must comply with the requirements set out in Part 4A, Part 4B and section 5.8 of National Instrument 51-102 Continuous Disclosure Obligations.

Guidance on those requirements can be found in Part 4A of Companion Policy 51-102CP Continuous Disclosure Obligations and CSA Staff Notice 51-330 Guidance Regarding the Application of Forward-Looking Information Requirements under NI 51-102 Continuous Disclosure Obligations.

The FLI requirements do not relieve issuers from disclosing material climate-related risks even if they are expected to occur or crystallize over a longer time frame.

PART 3 TRANSITION

Transitional Periods

7. The Instrument will apply to issuers on a phased-in transition, beginning with issuers other than venture issuers ("non-venture issuers") followed by venture issuers. Non-venture issuers must include the disclosure required by the Instrument in the applicable continuous disclosure document in respect of each financial year that begins on or after January 1 of the first year after the Instrument is made effective. As an example, for a non-venture issuer that has a financial year that begins on January 1 and ends on December 31, if the Instrument becomes effective in 2022, a non-venture issuer would be required to include the disclosure required by Form 51-107B in its AIF for its financial year ended December 31, 2023, and for every financial year thereafter. For venture issuers, the Instrument will apply in respect of each financial year that begins on or after January 1 of the third year after the Instrument is made effective. Using the same example as above (except where the issuer is a venture issuer), the issuer would be required to include the disclosure required by Form 51-107B for its financial year ended December 31, 2025, and for every financial year thereafter.

If a venture issuer becomes a non-venture issuer during the period when the Instrument only applies to non-venture issuers, the disclosure required by the Instrument will not be required in the applicable continuous disclosure document for the financial years in which the issuer was a venture issuer.

{12} As an alternative, the CSA is also consulting on requiring issuers to disclose Scope 1 GHG emissions. Under this alternative, disclosure of Scope 2 and Scope 3 GHG emissions would not be mandatory. Issuers would have to disclose either their Scope 2 and 3 GHG emissions and the related risks or the issuer's reasons for not disclosing this information.

Annex C -- Existing Securities Legislation

The following summary provides a non-exhaustive overview of existing requirements that currently may apply to the disclosure of climate-related information.

1. Materiality

Generally, materiality is the determining factor in considering whether information is required to be disclosed. As provided in Form 51-102F1 and Form 51-102F2, information is likely material where a reasonable investor's decision whether or not to buy, sell or hold securities of the issuer would likely be influenced or changed if the information was omitted or misstated.

2. Material Risk Factor Disclosure

Item 5.2 of Form 51-102F2 requires an issuer to disclose in its AIF, risk factors relating to it and its business that would be most likely to influence an investor's decision to purchase the issuer's securities. Accordingly, any climate-related risks that are determined to be material to the issuer must be disclosed pursuant to this item. In certain instances, securities legislation may require the quantification of these types of risks. For example, Item 5.1(1)(k) of Form 51-102F2 requires an issuer to disclose the financial and operational effects of environmental protection requirements in the current financial year and the expected effect in future years.

Item 1.4(g) of Form 51-102F1 requires an issuer to discuss in its MD&A, its analysis of its operations for the most recently completed financial year, including commitments, events, risks or uncertainties that it reasonably believes will materially affect its future performance.

3. Risk management and oversight

Two sets of disclosure requirements provide insight into how issuers are managing material risks:

• Disclosure of environmental policies fundamental to operations

• Item 5.1(4) of Form 51-102F2 requires issuers to describe environmental policies that are fundamental to their operations and the steps taken to implement them.

• Disclosure of board mandate and committees

• The guidelines in section 3.4 of NP 58-201 state that an issuer's board should adopt a written mandate that explicitly acknowledges responsibility for, among other things: (i) adopting a strategic process and approving, at least annually, a strategic plan that takes into account the opportunities and risks of the business; and (ii) the identification of the principal risks of the issuer's business and ensuring the implementation of appropriate systems to manage these risks.

• Pursuant to section 2 of Form 58-101F1 Corporate Governance Disclosure, non-venture issuers are required to disclose the text of their board mandate, or if the board does not have a written mandate, to explain how they delineate roles and responsibilities.

• NI 58-101 requires both venture and non-venture issuers to identify and describe the function of any standing committees other than audit, compensation and nominating committees (which would include environmental or other committees responsible for managing climate-related issues), and to disclose the text of the audit committee's charter (for some issuers, the audit committee may have responsibility for, among other things, environmental risk management).

With respect to the oversight of disclosure, NI 52-110 requires an issuer's audit committee to review its financial statements and MD&A, and NI 51-102 requires their approval by the board of directors, although the approval of interim filings may be delegated to the audit committee. NI 52-109 requires an issuer's Chief Executive Officer and Chief Financial Officer to certify certain matters in relation to the financial statements, MD&A and, if applicable, AIF. Finally, NP 58-201 and NI 52-110 establish guidelines and requirements intended to assist issuers in the implementation of policies and practices required for effective corporate governance and oversight over their business, including the identification and management of business risks.

4. Controls and Procedures

Under NI 52-109, to support the review, approval and certification process discussed above, an issuer must have adequate controls and procedures in place for its disclosure of material information, including climate-related information. The audit committee and certifying officers have key responsibilities in establishing these controls and procedures. In particular, the audit committee has responsibilities under NI 52-110 in respect of procedures in place for the review of the issuer's public disclosure of financial information extracted or derived from financial statements.

Annex D -- CSA Disclosure Review

A. Features of the Disclosure Review

Feature |

Details from Disclosure Review |

|

Who was selected? |

• |

48 issuers selected primarily from the S&P/TSX Composite Index. |

|

• |

Wide range of industries, including: finance and insurance, communications, consumer products, industrial, life sciences, healthcare, mining, oil and gas, oil and gas services, construction and engineering, pipelines, real estate, technology, and utilities. |

|

• |

Market capitalization ranged from $800 million to nearly $180 billion, with: |

|

|

• |

30% of issuers within the $2 billion to $5 billion range. |

|

|

• |

21% of issuers within the $800 million to $2 billion range. |

|

|

• |

17% of issuers within the $5 billion to $10 billion range. |

|

|

• |

17% of issuers above $25 billion. |

|

|

• |

15% of issuers within the $10 billion to $25 billion range. |

|

Which documents were reviewed? |

• |

CD filings: |

|

|

• |

Financial statements, MD&As, AIFs, and information circulars. |

|

• |