Ontario Securities Commission Bulletin

Issue 44/41 - October 14, 2021

Ont. Sec. Bull. Issue 44/41

• OSC Staff Notice 11-793 Hierarchy of Regulatory Instruments in Securities Law

• Notice of Correction -- Macquarie Capital Markets Canada Ltd.

• The Mutual Fund Dealers Association and Omar Enrique Rojas Diaz (also known as Omar Rojas)

• GLMX Technologies, LLC -- s. 15.1 of NI 21-101, s. 12.1 of NI 23-101, s. 10 of NI 23-103

• The Calgary Airport Authority

• Brookfield Business Partners L.P. and Brookfield Business Corporation

• MEMBERS Capital Advisors, Inc.

• Brookfield Property Partners L.P. and Brookfield Property Preferred L.P.

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• GLMX Technologies, LLC -- Application for Exemptive Relief -- Notice of Commission Order

• RG One Corp. -- s. 4(b) of Ont. Reg. 289/00 under the OBCA

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

OSC Staff Notice 11-793 Hierarchy of Regulatory Instruments in Securities Law

In November 2018 the Ontario Securities Commission (the Commission) created a burden reduction task force to refocus our efforts on reducing unnecessary regulatory burden. Consultations were launched on January 14, 2019, with the publication of OSC Staff Notice 11-784 Burden Reduction.

During the public consultations, several market participants expressed a concern that the difference between rules, or legal requirements, and guidance is not always clear. This staff notice clarifies the differences between each regulatory instrument and serves as an informational resource for Commission regulatory staff and market participants.

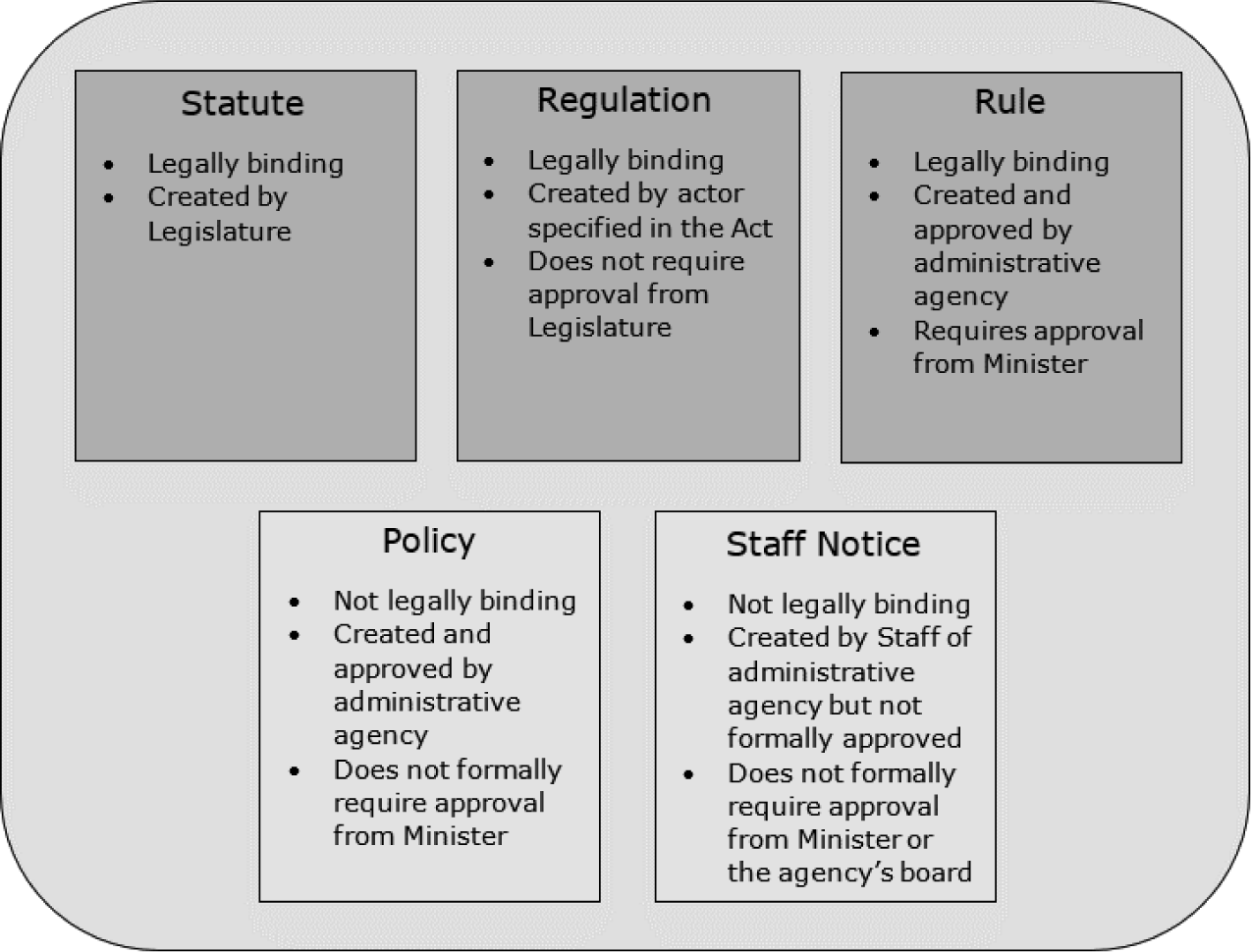

Securities regulators deploy several different types of instruments to govern the conduct of regulated persons and entities. However, not all regulatory instruments have the same legal authority. As illustrated in the diagram below, statutes, regulations, and rules are all legally binding. The requirements set out in these instruments are mandatory and failure to comply may result in enforcement action. Conversely, guidance published by the Commission or staff of the Commission (Staff) is instructive in nature and is not legally binding.

The Commission administers the Securities Act (Ontario) and its General Regulation, as well as the Commodity Futures Act (Ontario) and its General Regulation. These provincial statutes and regulations are legally binding.

Statute

A statute or "Act" is a law passed by the provincial Legislature. The legislative process in Ontario generally requires:

• a first reading where a bill is introduced, and its purpose is explained;

• a second reading where members of the Legislature debate and vote on the bill;

• a committee examination of the bill clause-by-clause;

• a report to the House and order for a third reading;

• a third reading where members vote on whether the bill will be passed; and

• royal assent where the Lieutenant Governor signs the bill.

A bill's provisions can come into force on royal assent, on a specified date, or on proclamation. Some bills are never proclaimed and therefore never become law.

Regulation

A regulation is a law that is made by a person or body whose authority to make such law is set out in a statute. The authority to make regulations is typically provided to the Lieutenant Governor in Council. However, in some statutes, this authority is given to a Minister or to another government official or body.

Regulations are created by the Ontario government ministry that is responsible for administering the parent statute, and are passed by Order in Council. Approval from the Legislature is not required for the creation of a new regulation.

The Legislature has given the Commission explicit authority to make rules in subject areas enumerated in the Securities Act.{1} Rules are drafted by the Commission, are often required to be published for public comment, and require Ministerial approval.{2}

Because securities regulation is provincial, rules are made under each province or territory's Securities Act or equivalent. In the rare instance where only the Commission makes a rule, this is called a local rule.

More commonly, Canadian securities regulators harmonize rules. As a result, most rules appear as national instruments, which apply to all Canadian jurisdictions uniformly, subject to local carveouts. There are also multilateral instruments, which apply only in the subscribing jurisdictions. National instruments and multilateral instruments are essentially consolidations of local rules.

Before the Commission publishes for comment a new rule (or an amendment to an existing rule) dealing with a novel or complex issue, it may publish a consultation paper and request comments. This initial consultation enables the Commission to better understand the need for the new rule or amendment and the potential market impacts.

Following the consultation period, Staff drafts the proposed rule or amendment and the Commission publishes it for comment, unless an exception to the publication requirement applies.{3} In Ontario, the publication must include:

• the proposed rule;

• a statement of the substance and purpose of the proposed rule;

• a summary of the rule;

• a discussion of all alternatives to the proposed rule that were considered and reasons for not proposing their adoption;

• a qualitative and quantitative analysis of the anticipated costs and benefits of the rule; and

• a reference to the authority under which the rule is to be made.{4}

The public is provided at least 90 days to consider a proposed rule and to submit comments to the Commission. If the Commission makes material amendments to a proposed rule after the initial comment period, the Commission must republish the proposed rule for a second comment period.{5}

For a rule to come into force, the Commission must approve the rule in its final form and deliver it to the Minister of Finance for review.{6} Within 60 days after a rule is delivered to the Minister, the Minister may approve or reject the rule, or return it to the Commission for further consideration.{7} If the Minister does not approve, reject or return the rule, it becomes effective 15 days following the conclusion of the 60-day period unless there is a later effective date specified in the rule.{8} The Commission must publish every rule that comes into force in The Ontario Gazette and in its Bulletin.

The Commission produces two types of non-binding guidance: policies and staff notices. These are intended to be instructive and to provide regulated persons and entities with insight into how the requirements are applied.

Like rules, policies and staff notices may apply at the national or local level. National policies and companion policies to a national instrument apply to all Canadian jurisdictions. The Commission can issue local policies that apply only within Ontario.

Regulated persons and entities may also be guided by decisions of the OSC Tribunal, although these decisions are not formally binding on persons or entities who were not parties to the proceeding before the Tribunal.

Policies

The Securities Act authorizes the Commission to adopt policies of a non-binding nature, including the Commission's interpretations of rules.{9} A policy is generally used to address issues that occur frequently or have a broad impact on market participants.

Unlike staff notices, policies must be approved by the Commission and must be published for comment. Publication is not required if the proposed policy would make no material substantive change to an existing policy.{10} Following the notice and comment process, if applicable, the Commission may adopt a proposed policy. While policies do not formally require Ministerial approval, the Commission may consult the Minister when a new policy is proposed.

Unlike rules, policies cannot be prohibitive or mandatory in character. Policies inform market participants of: (a) how the Commission may exercise its discretionary authority, (b) how the Commission interprets Ontario securities law, (c) the practices followed by the Commission in performing its duties under Ontario securities law, and (d) other matters that are not legislative in nature.{11} Policies are also used to communicate the Commission's views of what may be in the public interest regarding a given issue.{12}

Staff Notices

Staff notices are documents issued by the Commission that communicate Staff's views and expectations of operational reviews, emerging issues and trends, and market participant conduct. Staff views are subject to change as Staff are confronted with different factual circumstances. Accordingly, views expressed in a staff notice do not necessarily represent the views of the Commission.

Staff notices are not approved by the Commission and need not be published for public comment. However, Staff notices are often discussed with the Commission and may incorporate feedback from Commissioners. Like policies, staff notices do not require Ministerial approval.

Staff notices generally describe: (a) factors relevant to the exercise of a discretion by Staff, (b) the manner in which statutes, regulations, rules or policies are interpreted by Staff, or (c) the practices generally followed by Staff in the performance of their responsibilities.

The annual Corporate Finance Branch Report is an example of a staff notice that provides issuers with guidance on trends and issues identified during compliance reviews. Branch reports also articulate Staff's expectations and interpretation of regulatory requirements and outline the Branch's operational and policy work.

If you have questions about this notice, please contact:

Robert GaleaActing Associate General CounselGeneral Counsel's Officergalea@osc.gov.on.caTegan RacoLegal CounselGeneral Counsel's Officetraco@osc.gov.on.ca

{1} Securities Act, RSO 1990, c S.5, s 143(1) [Securities Act]. Note, the Commodity Futures Act provides the Commission with similar rule-making authority and process requirements.

{2} Securities Act, ss 143.2-143.6.

{3} Securities Act, s 143.2(5).

{4} Securities Act, s 143.2(2).

{5} Securities Act, s 143.2(7).

{6} Securities Act, s 143.3(1).

{7} Securities Act, s 143.3(3).

{8} Securities Act, s 143.4.

{9} Securities Act, s 143.8.

{10} Securities Act, s 143.8(6).

{11} Securities Act, s 143.8(1). Ontario Securities Commission Policy 11-601 is an example of a policy that addresses matters that are not legislative in nature. This local policy outlines organizational and procedural practices of the Securities Advisory Committee (a group of practicing securities lawyers who provide advice to the Commission and Staff).

{12} National Policy 62-202 is an example of how securities regulators communicate public interest considerations. This policy recognizes that, during a take-over bid, the interests of management may differ from those of shareholders of the target company and provides guidance on when defensive tactics may be subject to scrutiny by securities regulators.

Notice of Correction -- Macquarie Capital Markets Canada Ltd.

The incorrect file number was included in Macquarie Capital Markets Canada Ltd. published in the September 23, 2021 issue of the Bulletin at (2021), 44 OSCB 7885. The correct file number is: OSC File #: 2021/0312.

The Mutual Fund Dealers Association and Omar Enrique Rojas Diaz (also known as Omar Rojas)

FOR IMMEDIATE RELEASE

October 6, 2021

TORONTO -- The Commission issued its Reasons and Decision in the above named matter.

A copy of the Reasons and Decision dated October 5, 2021 is available at www.osc.ca.

For Media Inquiries:

For General Inquiries:

An Application by Wilks Brothers, LLC for the Review of a Decision by TSX Inc. relating to Calfrac Well Services Ltd.

FOR IMMEDIATE RELEASE

October 7, 2021

TORONTO -- The Commission issued its Reasons for Decision in the above named matter.

A copy of the Reasons for Decision dated October 6, 2021 is available at www.osc.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 7, 2021

TORONTO -- Following a hearing held today, the Commission issued an Order in the above named matter approving the Settlement Agreement reached between Staff of the Commission and Daniel Sheehan.

Take notice that the hearing on the merits scheduled to be commence on October 8, 2021 at 10:00 a.m. will not proceed as scheduled.

A copy of the Order dated October 7, 2021 and Settlement Agreement dated October 4, 2021 are available at www.osc.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 8, 2021

TORONTO -- The Commission issued an Order in the above named matter.

A copy of the Order dated October 8, 2021 is available at www.osc.ca.

For Media Inquiries:

For General Inquiries:

FOR IMMEDIATE RELEASE

October 12, 2021

TORONTO -- The Commission issued its Reasons for Approval of a Settlement in the above named matter.

A copy of the Reasons for Approval of a Settlement dated October 12, 2021 is available at www.osc.ca.

For Media Inquiries:

For General Inquiries:

GLMX Technologies, LLC -- s. 15.1 of NI 21-101, s. 12.1 of NI 23-101, s. 10 of NI 23-103

Application for relief under s. 15.1 of National Instrument 21-101 Marketplace Operation, s. 12.1 of National Instrument 23-101 Trading Rules, and s. 10 of National Instrument 23-103 Electronic Trading and Direct Access to Marketplaces -- relief from the application of all provisions of the Marketplace Rules that apply to a person or company carrying on business as an alternative trading system in the Jurisdictions -- relief granted subject to terms and conditions.

October 6, 2021

The securities regulatory authority or regulator in each of the Jurisdictions (Decision Maker) has received an application (the Application) from the Filer for a decision under the securities legislation of the Jurisdictions (the Legislation) that the Filer be:

(a) exempt pursuant to subsection 15.1 of National Instrument 21-101 Marketplace Operation (NI 21-101) from NI 21-101 in whole;

(b) exempt pursuant to subsection 12.1 of National Instrument 23-101 Trading Rules (NI 23-101) from NI 23-101 in whole;

(c) exempt pursuant to subsection 10(1) of National Instrument 23-103 Electronic Trading and Direct Electronic Access to Marketplaces (NI 23-103) from NI 23-103 in whole

(the relief mentioned in paragraphs (a) to (c) being collectively referred to herein as the Exemptive Relief Sought).

Under National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions (for a coordinated review application):

(a) the Ontario Securities Commission is the principal regulator for this application, and

(b) the decision is the decision of the principal regulator and evidences the decision of each other Decision Maker.

Under National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions (for a coordinated review application):

(a) the Ontario Securities Commission is the principal regulator for this application, and

(b) the decision is the decision of the principal regulator and evidences the decision of each other Decision Maker.

Terms defined in National Instrument 14-101 Definitions and Multilateral Instrument 11-102 Passport System have the same meaning if used in this decision, unless otherwise defined.

This decision is based on the following facts represented by the Filer which is sometimes referred to herein as "GLMX":

1. The Filer is a private limited liability company incorporated under the laws of Delaware whose registered and head office is at 330 Seventh Avenue, Floor 17, New York, New York, United States of America.

2. The Filer is an (in)direct wholly owned subsidiary of Global Liquid Markets, LLC (GLM). GLM is a holding company for various GLMX entities. GLM has three subsidiaries: GLMX, LLC, the Filer and GLMX Europe Limited. GLMX, LLC licenses an electronic trading platform (Platform) to GLMX and GLMX operates and maintains it. The Platform facilitates the negotiation of securities financing transactions including repurchase and reverse purchase transactions and securities lending arrangements, sale/buy back agreements and margin lending (collectively, SFTs) between institutional counterparties that have pre-existing contractual relationships with each other.

3. The Filer was formed in June 2017. It is registered as an alternative trading system (ATS) and a broker-dealer registered with the Securities and Exchange Commission (SEC) pursuant to section 15 of the Securities Exchange Act of 1934, as amended, (Exchange Act). The Filer is also a member of the Financial Industry Regulatory Authority (FINRA) and the Securities Investor Protection Corporation. The Filer operates one ATS that is registered with the SEC.

4. The Filer is subject to a comprehensive regulatory regime in the US. The Filer operates as an ATS and a broker-dealer registered with the SEC. The Filer is regulated by the SEC and FINRA as a broker-dealer and an ATS. The SEC and FINRA fulfil their regulatory responsibilities within the framework established by the Exchange Act and FINRA member rules.

5. SFTs are transactions where securities are used to borrow cash, or vice versa. The principal participants in these markets are broker-dealers acting as intermediaries and their diverse institutional clients. In these transactions, securities are exchanged for collateral which can be in the form of cash or different securities. Transactions are driven by a need to lend/borrow specific securities or to lend/borrow cash.

6. Cash lenders use SFTs as a way to securely invest cash. Typical cash lenders include money market funds, central banks, bank investment portfolio and others. Securities lenders enter into SFTs to finance their securities positions or obtain leverage. Typical cash borrowers/securities lenders are hedge funds, mortgage REITs, pension funds, asset managers, insurance companies and sovereign wealth funds.

7. The securities exchanged in SFTs negotiated on the Platform are as follows: major sovereign debt including US Treasuries, UK Government Debts, Euro Government Debt, Japan, Singapore, Australia and New Zealand, debt issued by agency; sub-sovereign and supranational institutions including U.S. agency debentures (FNMA, Freddie, FHLC), provincials, International Finance Corporation (IFC), World Bank, Länder, US Municipal Debt; Mortgage-Backed Securities including Agency Mortgage-Backed Securities Pools, Agency Collateralized Mortgage Obligations (CMOs), CMO Private Label (Investment-Grade And Non-Investment-Grade), Crown; non-Canadian issued corporate debt including Investment Grade, Non-investment grade, asset-backed securities; and re-securitizations including consumer (credit cards, auto loans), collateralized debt obligations, collateralized loan obligations, covered bonds; loans including bank loans, whole loans; money market instruments including term deposits, certificates of deposit, commercial paper; and non-Canadian issued equities including common, preferred, convertible and ETF.

8. In addition, GLMX currently offers and intends in the future to offer SFTs on its platform using Canadian Government Securities, defined as all debt instruments denominated in Canadian dollars and issued domestically by the Government of Canada or provincial governments or municipalities, as an incidental part of its business which will constitute less than 10% measured by total GLMX volume for the last 12 months.

9. The Filer does not have any offices or maintain other physical installations in Alberta, British Columbia, Nova Scotia, Ontario, Québec or any other Canadian province or territory.

10. Prior to getting access to the Platform, a subscriber (customer) must sign an agreement (Subscription Online Services Agreement) with GLMX that covers, among other things, obligations of the subscriber, and termination events.

11. The subscriber identifies to GLMX by name each employee or contractor of subscriber that is authorized to use the Platform. These "named users" are the only individuals within the subscriber licensed to access and use the service (Online Service).

12. GLMX will provide the subscriber access to the online service through a web based interface that can only be accessed when GLMX white lists subscriber's IP addresses. GLMX will provide each named user a unique username and password to enable such named user to access the Online Service.

13. Once a trade is mutually agreed and completed by the counterparties, the GLMX platform will send trade details to the parties of the transaction via a pre-approved method (e.g. email). Subscribers, independently and in advance, notify GLMX that they are properly documented with and able to trade with specific counterparties prior to engaging in transactions with that counterparty. GLMX is not a party to the SFT transaction and is not involved in the direct execution or clearing and settlement.

14. GLMX proposes to offer direct access to its Platform to prospective subscribers in the Jurisdictions (Canadian Subscribers) to facilitate trades. Access to the Platform will be limited to Canadian Subscribers who meet GLMX's eligibility criteria. Subscribers generally fall into the following categories: large multi-national bank; insurance company; US registered investment company; derivatives dealer; and/or any other person (whether a corporation, partnership, trust or otherwise) with total assets of at least $50 million which can include pension funds and hedge funds.

15. Before being provided direct access to the Platform, GLMX will confirm that each Canadian Subscriber is a "permitted client" as that term is defined in National Instrument 31 103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31 103). Retail customers will not be provided with access to the Platform.

16. Once a Canadian Subscriber demonstrates that it satisfies the eligibility criteria, the Canadian Subscriber must execute a Subscription Online Services Agreement in which the prospective Canadian Subscriber agrees to use the online service and the related user documentation only in the ordinary course of its own business for its own internal use and be and remain at all times a "permitted client" as defined in NI 31-103.

17. Under the Subscription Online Services Agreement, a Canadian Subscriber and its affiliates constitute a "Subscriber Group" and the Subscriber Group will authorize named users (Named Users) who are the only persons authorized to use the online service. The Subscriber Group's right to use the Online Service is conditioned upon Subscriber Group obtaining and maintaining all government, legal and regulatory approvals, consents, authorizations, registrations, permits and licenses required for the conduct of its activities and its use of the Online Services and using the Online Service only in compliance with applicable law.

18. GLMX has determined that it may be subject to dealer registration under applicable Canadian securities legislation and so it proposes to rely on the "international dealer exemption" under section 8.18 of NI 31-103 in the Jurisdictions and, subject to observing the revenue/volume ceiling just mentioned, on the specified debt exemption under section 8.21 of NI 31-103.

19. The Filer will ensure that all applicants who become Canadian Subscribers satisfy the Filer's eligibility criteria, including, among other things, that each Canadian Subscriber is a "permitted client" as that term is defined in NI 31-103.

20. The Filer is not in default of securities legislation in any Jurisdiction.

The Decision Maker is satisfied that the decision meets the test set out in the Legislation for the Decision Maker to make the decision.

The decision of the Decision Maker under the Legislation is that the Exemptive Relief Sought is granted provided that the Filer complies with the terms and conditions attached hereto as Schedule A.

1. The Filer will continue to be subject to the regulatory oversight of the regulator in its home jurisdiction;

2. The Filer will either be registered in an appropriate category or rely on an exemption from registration under Canadian securities laws;

3. The Filer will promptly notify the Decision Makers if its status in its home jurisdiction has been revoked, suspended, or amended, or the basis on which its status has significantly changed;

4. The Filer will not provide direct access to a Canadian Subscriber unless the Canadian Subscriber is a "permitted client" as that term is defined in NI 31-103;

5. The Filer will require Canadian Subscribers to provide prompt notification to the Filer if they no longer qualify as "permitted clients";

6. The Filer must make available to Canadian Subscribers appropriate training for each person who has access to trade on the Platform;

7. The Filer will only offer SFTs to Canadian Subscribers and in that context use only the collateral listed in accordance with representation numbers 7 and 8 of this Decision;

8. Trades on the Platform by Canadian Subscribers will be cleared and settled through clearing arrangements used outside the Platform by subscribers;

9. The Filer will only permit Canadian Subscribers to trade those securities which are permitted to be traded in the United States under applicable securities laws and regulations;

10. The Filer will promptly notify staff of the Decision Makers of any of the following:

(a) any material change to its business or operations or the information provided in the Application, including, but not limited to:

(i) changes to its regulatory oversight;

(ii) the access model, including eligibility criteria, for Canadian Subscribers;

(iii) systems and technology; and

(iv) its clearing and settlement arrangements;

(b) any change in its regulations or the laws, rules, and regulations in the home jurisdiction relevant to the products traded;

(c) any known investigations of, or regulatory action against, the Filer by the regulator in the home jurisdiction or any other regulatory authority to which it is subject;

(d) any matter known to the Filer that may affect its financial or operational viability, including, but not limited to, any significant system failure or interruption; and

(e) any default, insolvency, or bankruptcy of any subscriber known to the Filer or its representatives that may have a material, adverse impact upon the Platform, the Filer or any Canadian Subscriber;

11. The Filer will maintain the following updated information and submit such information in a manner and form acceptable to staff of the Decision Makers on a semi-annual basis (within 30 days of the end of each six-month period), and at any time promptly upon the request of staff of the Decision Makers:

(a) a current list of all Canadian Subscribers on a per provincial basis, specifically identifying for each Canadian Subscriber the basis upon which it represented to the Filer that it could be provided with direct access;

(b) a list of all Canadian applicants for status as a Canadian Subscriber on a per provincial basis who were denied such status or access or who had such status or access revoked during the period;

(i) for those Canadian applicants for status as a Canadian Subscriber that were denied access, an explanation as to why access was denied;

(ii) for those Canadian Subscribers who had their status revoked, an explanation as to why their status was revoked;

(c) for each product:

(i) the total trading volume and value originating from Canadian Subscribers, presented on a per provincial Canadian Subscriber basis;

(ii) the proportion of worldwide trading volume and value on the Platform conducted by Canadian Subscribers, presented in the aggregate per province for such Canadian Subscribers;

(iii) the trading volume and value of Canadian Government Securities (as defined in representation 8 of this Decision) used in SFTs and proportion of trading volume in Canadian Government Securities relative to the total volume traded on GLMX for the six month period, calculated in a manner acceptable to the Decision Makers; and

(d) a list of any system outages that occurred for any system impacting Canadian Subscribers' trading activity on the Platform which were reported to the regulator in the home jurisdiction;

12. The Filer will provide to its Canadian Subscribers disclosure that states that:

(a) rights and remedies against it may only be governed by the laws of the home jurisdiction, rather than the laws of Canada, and may be required to be pursued in the home jurisdiction rather than in Canada;

(b) the rules applicable to trading on the Platform may be governed by the laws of the home jurisdiction, rather than the laws of Canada; and

(c) the Filer is regulated by the regulator in the home jurisdiction, rather than the Decision Makers;

13. With respect to a proceeding brought by the Decision Makers, staff of the Decision Makers or another applicable securities regulatory authority in Canada arising out of, related to, concerning or in any other manner connected with such regulatory authority's regulation and oversight of the activities of the Filer in Canada, the Filer will submit to the non-exclusive jurisdiction of (i) the courts and administrative tribunals of Canada, and (ii) an administrative proceeding in Canada;

14. The Filer will file with the Decision Makers a valid and binding appointment of McCarthy Tetrault LLP, or any subsequent agent, as the agent for service in Canada upon which the Decision Makers or other applicable regulatory authority in Canada may serve a notice, pleading, subpoena, summons, or other process in any action, investigation, or administrative, criminal, quasi-criminal, penal, or other proceeding arising out of or relating to or concerning the regulation and oversight of the Platform or the Filer's activities in Canada; and

15. The Filer must, and must cause its affiliated entities, if any, to promptly provide to the Decision Makers, on request, any and all data, information, and analyses in the custody or control of the Filer or any of its affiliated entities, without limitations, redactions, restrictions or conditions, including, without limiting the generality of the foregoing:

(a) data, information, and analyses relating to all of its or their businesses; and

(b) data, information, and analyses of third parties in its or their custody or control; and

16. The Filer must share information and otherwise cooperate with other recognized or exempt exchanges, recognized self-regulatory organizations, investor protection funds and other appropriate legal and regulatory bodies.

National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions -- relief from the prospectus requirement in connection with the distribution of non-convertible debentures, subject to conditions -- non-reporting, not-for-profit issuer unable to rely on the exemption in section 2.4 of NI 45-106.

Securities Act, R.S.O. 1990, c. S.5, as am., s.74.

Citation: Re The Calgary Airport Authority, 2021 ABASC 156

October 7, 2021

The securities regulatory authority or regulator in each of the Jurisdictions (each, a Decision Maker) has received an application from the Filer for a decision under the securities legislation of the Jurisdictions (the Legislation) for an exemption from the prospectus requirement in connection with the distribution (an Offering) of non-convertible debt securities of the Filer (the Exemption Sought).

Under the Process for Exemptive Relief Applications in Multiple Jurisdictions (for a dual application)

(a) the Alberta Securities Commission is the principal regulator for this application,

(b) the Filer has provided notice that section 4.7(1) of Multilateral Instrument 11-102 Passport System (MI 11-102) is intended to be relied upon in each province of Canada, other than Ontario and Alberta, and

(c) the decision is the decision of the principal regulator and evidences the decision of the securities regulatory authority or regulator in Ontario.

Terms defined in National Instrument 14-101 Definitions and MI 11-102 have the same meaning if used in this decision, unless otherwise defined.

This decision is based on the following facts represented by the Filer:

1. The Filer is a private, not-for-profit corporation, formed on 26 July 1990 by way of order in council O.C. 398/90 issued by the Lieutenant Governor in Council of Alberta.

2. The head office of the Filer is located in Alberta.

3. The Filer is governed by articles of incorporation dated 7 October 1998 (the Articles) as well as the Regional Airports Authorities Act (the RAA Act) and the Regional Airports Authorities Regulation (the RAA Regulation).

4. The Filer is not a reporting issuer in any jurisdiction of Canada and is not in default of securities legislation in any jurisdiction of Canada.

5. The Articles provide that there are no restrictions on:

(a) the number of securities or any particular form of securities that the Filer is permitted to issue; or

(b) the right to transfer any of the securities issued by the Filer; however, the Articles do not provide for specific classes of shares or other equity securities issuable by the Filer.

6. There is a strict prohibition on the Filer's ability to issue shares under section 36(2) of the RAA Act, which is not an optional prohibition and cannot be overridden by provisions of the Articles and the Filer is therefore unable to issue share capital. Accordingly, the Filer does not have any shares or other equity securities outstanding and has never issued such equity securities.

7. The outstanding securities of the Filer consist of approximately $2.915 billion in non-convertible debentures (the Prior Offering). Debentures of the Filer were distributed solely to the Government of Alberta in the name of the Alberta Capital Finance Authority. By subsequent assignment, all such debentures under the Prior Offering have been transferred directly to the Province of Alberta.

8. While the RAA Act contemplates the issuance of securities by authorities such as the Filer, section 36(2) of the RAA Act restricts the issuance of share capital by providing that "unless otherwise prescribed, an authority shall not issue any shares". The RAA Regulation does not prescribe anything to the contrary.

9. In order to complete a distribution or trade of securities, the Filer would be required to file a prospectus or rely on an exemption from the prospectus requirements under National Instrument 45-106 Prospectus Exemptions (NI 45-106).

10. The Filer cannot rely on the exemption in section 2.4 of NI 45-106 (the Private Issuer Exemption) with respect to the Offering because it does not technically satisfy subparagraph (b)(i) of the definition of "private issuer" contained in the Private Issuer Exemption, as there are no restrictions on the transfer of the relevant securities of the Filer contained in the Filer's constating documents or security holders' agreement.

Each of the Decision Makers is satisfied that the decision meets the test set out in the Legislation for the Decision Maker to make the decision.

The decision of the Decision Makers under the Legislation is that the Exemption Sought is granted, provided that,

(a) at the time of an Offering,

(i) the Filer satisfies paragraphs (a) and (c) of the definition of "private issuer" contained in the Private Issuer Exemption,

(ii) there has been no amendment to section 36(2) of the RAA Act,

(iii) the RAA Regulation prescribes no exception to section 36(2) of the RAA Act, and

(b) the first trade of any non-convertible debt securities of the Filer issued in reliance on the Exemption Sought will be subject to section 2.6 of National Instrument 45-102 Resale of Securities.

For the Commission:

"Tom Cotter"Vice-Chair"Kari Horn"Vice-Chair

Brookfield Business Partners L.P. and Brookfield Business Corporation

National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions -- Multilateral Instrument 61-101 Protection of Minority Security Holders in Special Transactions -- partnership creates corporation to provide investors with alternative way to hold its units -- corporation issues exchangeable shares whose terms are structured so that each exchangeable share is functionally and economically equivalent to a partnership unit -- each exchangeable share provides an equivalent economic return as a partnership unit -- both the partnership and the corporation are reporting issuers -- related party transactions between the partnership and the corporation are exempt from the related party transaction requirements, subject to conditions -- partnership may include corporation's exchangeable shares when calculating market capitalization for the purposes of using the 25% market capitalization exemption for certain related party transactions, subject to conditions.

Multilateral Instrument 61-101 Protection of Minority Security Holders in Special Transactions, Part 5, ss. 5.5(a), 5.7(1)(a) and 9.1.

October 8, 2021

The principal regulator in the Jurisdiction has received an application from Brookfield Business Partners L.P. (BBU) and Brookfield Business Corporation (BBUC, and together with BBU, the Filers) for a decision under the securities legislation of the Jurisdiction of the principal regulator (the Legislation) that:

(a) BBU be exempt from the requirements of Part 5 of Multilateral Instrument 61-101 Protection of Minority Security Holders in Special Transactions (MI 61-101, and such requirements, the Related Party Transaction Requirements) in connection with any related party transaction of BBU with BBUC or any of BBUC's subsidiary entities (the BBU Related Party Relief);

(b) BBUC be exempt from the Related Party Transaction Requirements in connection with any related party transaction of BBUC with BBU or any of BBU's subsidiary entities (the BBUC Related Party Relief); and

(c) BBU be exempt from the requirements of sections 5.4 and 5.6 of MI 61-101 (the Valuation and Minority Approval Requirements) in connection with any related party transaction of BBU entered into indirectly through Holding LP (as defined below) or any subsidiary entity of Holding LP, if that transaction would qualify for the transaction size exemptions set out in sections 5.5(a) and 5.7(1)(a) of MI 61-101 if the class A exchangeable subordinate voting shares of BBUC (the Exchangeable Shares) were included in the calculation of BBU's market capitalization (the Transaction Size Relief, collectively with the BBU Related Party Relief and the BBUC Related Party Relief, the Exemption Sought).

Under the Process for Exemptive Relief Applications in Multiple Jurisdictions (for a passport application):

(a) the Ontario Securities Commission is the principal regulator for this application; and

(b) the Filers have provided notice that subsection 4.7(1) of Multilateral Instrument 11-102 Passport System (MI 11-102) is intended to be relied upon in Alberta, Manitoba, New Brunswick, Quebec, and Saskatchewan.

Terms defined in National Instrument 14-101 Definitions, MI 11-102 and MI 61-101 have the same meaning if used in this decision, unless otherwise defined.

This decision is based on the following facts represented by the Filers:

Relevant Entities

BBU

1. BBU is an exempted limited partnership established, registered and in good standing under the laws of Bermuda. BBU's registered and head office is located at 73 Front Street, 5th Floor, Hamilton HM 12, Bermuda.

2. BBU is a reporting issuer in all of the provinces and territories of Canada and is an SEC foreign issuer within the meaning of section 1.1 of National Instrument 71-102 Continuous Disclosure and Other Exemptions Relating to Foreign Issuers (NI 71-102) and satisfies its continuous disclosure obligations by complying with U.S. federal securities laws as permitted under NI 71-102. BBU is not in default of any requirement of securities legislation in the jurisdictions in which it is a reporting issuer.

3. The authorized capital of BBU consists of: (a) non-voting limited partnership units (the BBU Units); and (b) general partnership units.

4. The BBU Units are listed on the New York Stock Exchange (NYSE) and the Toronto Stock Exchange (TSX) under the symbols "BBU" and "BBU.UN", respectively.

5. BBU's only substantial asset is its limited partnership interest in Brookfield Business L.P. (Holding LP), a Bermuda exempted limited partnership established, registered and in good standing under the laws of Bermuda.

6. Brookfield Business Partners Limited, a wholly-owned subsidiary of Brookfield Asset Management Inc. (Brookfield), holds the general partner units in BBU.

Brookfield

7. Brookfield is a corporation existing and in good standing under the Business Corporations Act (Ontario). Brookfield's registered and head office is located at Suite 300, Brookfield Place, 181 Bay Street, Toronto, Ontario, M5J 2T3.

8. Brookfield is a reporting issuer in all of the provinces and territories of Canada and is not in default of any requirement of securities legislation in the jurisdictions in which it is a reporting issuer.

9. The Class A Limited Voting Shares of Brookfield are listed on the NYSE and the TSX under the symbols "BAM" and "BAM.A", respectively.

10. Brookfield holds an approximate 64% economic interest in BBU on a fully-exchanged basis through its indirect ownership of redeemable partnership units of Holding LP (the Redeemable Partnership Units).

11. Brookfield indirectly holds 100% of the voting interests in BBU through its ownership of the general partner units of BBU.

12. BBU, Holding LP and certain of their subsidiaries have retained Brookfield and its related entities to provide management, administrative and advisory services under a master services agreement.

BBUC

13. BBUC is a corporation existing and in good standing under the Business Corporations Act (British Columbia), and was incorporated on June 21, 2021. BBUC's registered office is located at 1500 Royal Centre, 1055 West Georgia Street, P.O. Box 11117, Vancouver, British Columbia, V6E 4N7. BBUC's head office is located at 250 Vesey Street, 15th Floor, New York, New York, 10281, United States of America.

14. The authorized share capital of BBUC consists of an unlimited number of common shares (the BBUC Common Shares).

15. All of the BBUC Common Shares are held by Brookfield BBP Canada Holdings Inc. (CanHoldCo), a wholly-owned subsidiary of BBU.

16. BBUC's initial operations will consist of business services and industrial operations primarily located in Australia, the United Kingdom, the United States and Brazil.

17. BBUC is not a reporting issuer in any jurisdiction and is not in default of any applicable requirement of securities legislation.

The Special Distribution

18. BBU believes that certain investors in certain jurisdictions may be dissuaded from investing in BBU because of the tax reporting framework that results from investing in units of a Bermuda exempted limited partnership.

19. BBUC was created, in part, to provide investors that would not otherwise invest in BBU with an opportunity to gain access to BBU's portfolio of services and industrial operations and their associated returns, and to provide investors with the flexibility to own, through the ownership of an Exchangeable Share, the economic equivalent of a BBU Unit.

20. BBU will be distributing Exchangeable Shares to holders of BBU Units (the Special Distribution). The Special Distribution is, in effect, a stock split of the BBU Units.

21. On July 30, 2021, (i) BBUC filed a preliminary long form prospectus to qualify the distribution of the Exchangeable Shares to be distributed pursuant to the Special Distribution, and (ii) BBU filed a preliminary short form prospectus to qualify the BBU Units issuable or deliverable upon the exchange, redemption or purchase of Exchangeable Shares pursuant to their terms.

22. Upon obtaining a receipt for the final prospectus, BBUC will become a reporting issuer in each of the provinces and territories of Canada.

23. BBUC has applied to have the Exchangeable Shares listed on the NYSE and TSX.

24. BBUC filed a registration statement on Form F-1 with the U.S. Securities and Exchange Commission (the SEC), to register the Exchangeable Shares that will be distributed pursuant to the Special Distribution, and BBU will file a registration statement of Form F-3 with the SEC, as amended, to register the BBU Units issuable or deliverable upon the exchange, redemption or purchase of Exchangeable Shares pursuant to their terms.

25. Prior to the closing of the Special Distribution:

(a) BBUC will reclassify its share structure such that, following the reclassification, BBUC's authorized share capital will consist of: (i) an unlimited number of Exchangeable Shares; (ii) an unlimited number of class B multiple voting shares (the Class B Shares); (iii) an unlimited number of class C non-voting shares (the Class C Shares); (iv) an unlimited number of class A senior preferred shares (issuable in series); and (v) an unlimited number of class B junior preferred shares (issuable in series);

(b) the following assets and ownership interests will be contributed or transferred by BBU, or subsidiaries thereof, to BBUC:

(i) an approximate 28% economic interest in Healthscope Pty Limited;

(ii) an approximate 26% economic interest in BRK Ambiental Participações S.A.;

(iii) an approximate 27% economic interest in Westinghouse Electric Company;

(iv) a 100% economic interest in Multiplex Global Limited; and

(v) approximately $212 million in cash (the Cash Proceeds);

(c) BBUC will loan the Cash Proceeds to CanHoldCo; and

(d) BBU will receive Exchangeable Shares through a distribution by Holding LP of Exchangeable Shares, on a proportionate basis, to all the holders of equity units of Holding LP, including Brookfield through its indirect ownership of Redeemable Partnership Units and special limited partnership units in Holding LP.

26. The distribution ratio of one (1) Exchangeable Share for every two (2) BBU Units was based on the fair market value of the businesses to be transferred by BBU to BBUC, the number of BBU Units outstanding at the time of the Special Distribution (assuming exchange of the Redeemable Partnership Units), and the market capitalization of BBU.

27. Each Exchangeable Share has been structured with the intention of providing an economic return equivalent to a BBU Unit and the rights, privileges, restrictions and conditions attached to each Exchangeable Share (the Exchangeable Share Provisions) are such that each Exchangeable Share is as nearly as practicable, functionally and economically, equivalent to a BBU Unit. In particular:

(a) each Exchangeable Share will be exchangeable at the option of a holder for one (1) BBU Unit (subject to adjustment to reflect certain capital events) or its cash equivalent (the form of payment to be determined at the election of BBUC) (an Exchange);

(b) the Exchangeable Shares are redeemable by BBUC at any time (including following a notice requiring redemption having been given by BBU) for BBU Units (or its cash equivalent, at BBUC's election) on a one-for-one basis (subject to adjustment to reflect certain capital events) (a Redemption);

(c) upon a liquidation, dissolution or winding up of BBUC, holders of Exchangeable Shares will be entitled to receive BBU Units (or its cash equivalent, at BBUC's election) on a one-for-one basis (subject to adjustment to reflect certain capital events) and not any remaining property or assets of BBUC following such payment (a BBUC Liquidation);

(d) upon a liquidation, dissolution or winding up of BBU, including where substantially concurrent with a BBUC Liquidation, all of the Exchangeable Shares will be automatically redeemed for BBU Units (or its cash equivalent, at BBUC's election) on a one-for-one basis (subject to adjustment to reflect certain capital events) (a BBU Liquidation); and

(e) subject to applicable law and in accordance with the Exchangeable Share Provisions, each Exchangeable Share will entitle the holder to dividends from BBUC payable at the same time as, and equivalent to, each distribution on a BBU Unit. The Exchangeable Share Provisions also provide that if a distribution is declared on the BBU Units and an equivalent dividend is not declared and paid concurrently on the Exchangeable Shares, then the undeclared or unpaid amount of such dividend accrues and accumulates and is to be paid upon the first to occur of any of the circumstances contemplated by paragraphs (a) to (d) above, if not yet paid.

28. Upon being notified by BBUC that BBUC has received a request for an Exchange, BBU has an overriding call right to purchase (or have one of its affiliates purchase) all of the Exchangeable Shares that are the subject of the Exchange notice from the holder of Exchangeable Shares for BBU Units (or its cash equivalent, at BBU's election) on a one-for-one basis (subject to adjustment to reflect certain capital events).

29. Upon being notified by BBUC that it intends to conduct a Redemption, BBU has an overriding call right to purchase (or have one of its affiliates purchase) all but not less than all of the then outstanding Exchangeable Shares for BBU Units (or its cash equivalent, at BBU's election) on a one-for-one basis (subject to adjustment to reflect certain capital events).

30. Upon the occurrence of a BBU Liquidation or BBUC Liquidation, BBU will have an overriding liquidation call right to purchase (or have one of its affiliates purchase) all but not less than all of the then outstanding Exchangeable Shares on the day prior to the effective date of such BBU Liquidation or BBUC Liquidation for BBU Units on a one-for-one basis (subject to adjustment to reflect certain capital events).

31. Prior to the Special Distribution, Brookfield will enter into a rights agreement (the Rights Agreement) pursuant to which it will agree that, for the five-year period beginning on the date of the Special Distribution, Brookfield will guarantee BBUC's obligation to deliver BBU Units or its cash equivalent in connection with an Exchange.

32. An investment in Exchangeable Shares will be as nearly as practicable, functionally and economically, equivalent to an investment in BBU Units. BBU expects that:

(a) investors of Exchangeable Shares will purchase Exchangeable Shares as an alternative way of owning BBU Units rather than a separate and distinct investment; and

(b) the market price of the Exchangeable Shares will be significantly impacted by (i) the combined business performance of BBUC and BBU as a single economic unit, and (ii) the market price of the BBU Units, in a manner that should result in the market price of the Exchangeable Shares tracking the market price of the BBU Units.

33. BBUC is intended to be an entity through which persons who do not wish to hold BBU Units directly, may hold their interests in BBU, and BBU is the entity through which holders of Exchangeable Shares and BBU Units hold their interests in the collective operations of BBU and its subsidiaries, including BBUC and its subsidiaries.

Ownership and Control of BBUC

34. The Related Party Transaction Requirements do not apply to an issuer carrying out a related party transaction if:

(a) as provided under paragraph 5.1(d) of MI 61-101, the parties to the transaction consist solely of (i) an issuer and one or more of its wholly-owned subsidiary entities, or (ii) wholly-owned subsidiary entities of the same issuer. A person is considered to be a "wholly-owned subsidiary entity" of an issuer if the issuer owns, directly or indirectly, all of the voting and equity securities and securities convertible into voting and equity securities of the person; and/or

(b) as provided under paragraph 5.1(g) of MI 61-101 (the Downstream Transaction Carve-Out), the transaction is a downstream transaction for the issuer. A "downstream transaction" means, for an issuer, a transaction between the issuer and a related party of the issuer if, at the time the transaction is agreed to, (i) the issuer is a control person of the related party, and (ii) to the knowledge of the issuer after reasonable inquiry, no related party of the issuer, other than a wholly-owned subsidiary entity of the issuer, beneficially owns or exercises control or direction over, other than through its interest in the issuer, more than five per cent of any class of voting or equity securities of the related party that is a party to the transaction.

35. Section 1.3 of MI 61-101 provides that, for the purposes of MI 61-101, a transaction of a wholly-owned subsidiary entity of an issuer is deemed to be a transaction of the issuer.

36. Related party transactions among BBU and BBUC will be required for the operation of the Exchangeable Share Provisions and in connection with ordinary course financial support arrangements which may be entered into from time to time.

37. The only voting securities of BBUC are the Exchangeable Shares and the Class B Shares. Holders of Exchangeable Shares are entitled to one (1) vote per Exchangeable Share held and holders of Class B Shares are entitled to cast, in the aggregate, a number of votes equal to three (3) times the number of votes attached to the Exchangeable Shares.

38. Neither the Exchangeable Shares nor the Class B Shares carry a residual right to participate in the assets of BBUC upon liquidation or winding-up of BBUC, and accordingly, are not equity securities under the Legislation. The Class C Shares are the only equity securities of BBUC.

39. All of the Class B Shares and the Class C Shares will be indirectly owned by BBU and none of them will be transferable except to an affiliate of BBU. Accordingly, all of the equity securities of BBUC are held indirectly by BBU.

40. BBUC is not a wholly-owned subsidiary of BBU; BBU will not own, directly or indirectly, all of the voting securities of BBUC because Brookfield and members of the public will hold Exchangeable Shares. However, by virtue of the terms of the Class B Shares, BBU holds a 75% voting interest in BBUC, will control BBUC and the appointment and removal of directors of BBUC; the voting rights attached to the Exchangeable Shares do not allow holders of Exchangeable Shares to affect the control of BBUC. The voting right attached to each Exchangeable Share is expected to assist with index inclusion.

41. BBU is not able to rely on the Downstream Transaction Carve-Out because, upon completion of the Special Distribution, Brookfield will beneficially own or exercise control or direction over, more than five per cent of the Exchangeable Shares, as it will hold, directly or indirectly, approximately 64% of the Exchangeable Shares. Brookfield will accordingly have an approximate 16% voting interest in BBUC.

42. BBUC is a controlled subsidiary of BBU and BBU will consolidate BBUC and its businesses in BBU's financial statements.

43. By virtue of the Exchangeable Share Provisions, the economic rights of the holders of the Exchangeable Shares will not be affected by transactions between BBU and BBUC. BBU, as the sole holder of equity securities of BBUC, will receive any benefit and/or bear any detriment from related party transactions between BBU and BBUC.

44. Minority approval is required of every class of affected securities, being equity securities of the issuer. For BBUC, minority approval of a related party transaction of BBUC with BBU would be sought from the holders of its Class C Shares, all of which are held by BBU. BBU, as the counterparty to such a related party transaction, does not require the protections of MI 61-101.

Market Capitalization Calculation

45. It is anticipated that BBU will, from time to time, enter into transactions with certain related parties, including Brookfield and its affiliates (other than BBU and its related entities, including BBUC) indirectly through Holding LP and its subsidiaries (including BBUC and its subsidiaries).

46. The Valuation and Minority Approval Requirements require, subject to the availability of an exemption, that an issuer obtain: (a) a formal valuation of the transaction in a form satisfying the requirements of MI 61-101 by an independent valuator; and (b) approval of the transaction by disinterested holders of the affected securities of the issuer.

47. A related party transaction that is subject to MI 61-101 may be exempt from the Valuation and Minority Approval Requirements if, at the time the transaction is agreed to, neither the fair market value of the subject matter of, nor the fair market value of the consideration for, the transaction, exceeds 25% of the issuer's market capitalization (the Market Cap Exemption).

48. It is unclear whether BBU would be entitled to rely on the Market Cap Exemption available under the Legislation because the definition of market capitalization in the Legislation does not contemplate securities of another entity that are exchangeable into equity securities of the issuer.

49. The Exchangeable Shares represent part of the equity value of BBU and are functionally and economically equivalent to the BBU Units. As a result of the Exchangeable Share Provisions, holders of Exchangeable Shares have the ability to receive a BBU Unit or its cash equivalent (the form of payment to be determined at the election of BBUC) and will receive identical distributions to the BBU Units, as and when declared by the board of directors of BBUC. Moreover, the economic interests that underlie the Exchangeable Shares are identical to those underlying the BBU Units; namely, the assets and operations held directly or indirectly by BBU.

50. Any costs related to a transaction occurring within the BBUC group would be borne by BBU as the sole holder of the equity securities of BBUC. BBU will consolidate BBU and its businesses in its financial statements and the business of BBU (including BBUC and its subsidiaries) will be the same as it was before the creation of BBUC and the transactions conducted in connection with, and to facilitate, the Special Distribution.

51. If the Exchangeable Shares are not included in the market capitalization of BBU, the equity value of BBU will be understated initially by the value of the Exchangeable Shares, being approximately 33% (assuming a one-for-two distribution ratio). As a result, related party transactions of BBU that are entered into through a subsidiary entity of BBUC may be subject to the Valuation and Minority Approval Requirements in circumstances where the fair market value of the transactions are effectively less than 25% of the fully diluted market capitalization of BBU.

52. BBU has already received relief similar to the Transaction Size Relief in respect of the Redeemable Partnership Units. On June 20, 2016, the Ontario Securities Commission granted BBU an exemption from the Valuation and Minority Approval Requirements in connection with any related party transaction of BBU entered into indirectly through Holding LP or a subsidiary of Holding LP if that transaction would qualify for the Market Cap Exemption if the Redeemable Partnership Units were included in the calculation of BBU's market capitalization.

The principal regulator is satisfied that the decision meets the test set out in the Legislation for the principal regulator to make the decision.

The decision of the principal regulator under the Legislation is that the Exemption Sought is granted provided that:

1. in respect of the BBU Related Party Relief and BBUC Related Party Relief:

(a) all of the equity securities of BBUC are owned, directly or indirectly, by BBU;

(b) all of the voting securities of BBUC (other than the Exchangeable Shares) are owned, directly or indirectly, by BBU;

(c) there are no material changes to the Exchangeable Share Provisions, as described above; and

(d) BBU consolidates BBUC and its businesses in BBU's financial statements;

2. in respect of the Transaction Size Relief:

(a) the transaction would qualify for the Market Cap Exemption if the Exchangeable Shares were considered an outstanding class of equity securities of BBU that were convertible into BBU Units;

(b) there are no material changes to the Exchangeable Share Provisions, as described above; and

(c) any annual information form or equivalent of BBU that is required to be filed in accordance with applicable securities laws contain the following disclosure, with any immaterial modifications as the context may require:

Multilateral Instrument 61-101 Protection of Minority Security Holders in Special Transactions ("MI 61-101") provides a number of circumstances in which a transaction between an issuer and a related party may be subject to valuation and minority approval requirements. An exemption from such requirements is available when the fair market value of the transaction is not more than 25% of the market capitalization of the issuer. Brookfield Business Partners L.P. ("BBU") has been granted exemptive relief from the requirements of MI 61-101 that, subject to certain conditions, permits it to be exempt from the minority approval and valuation requirements for transactions that would have a value of less than 25% of BBU's market capitalization, if Brookfield Asset Management Inc.'s ("Brookfield") indirect equity interest in BBU, and the class A exchangeable subordinate voting shares of Brookfield Business Corporation ("BBUC") are included in the calculation of BBU's market capitalization. As a result, the 25% threshold, above which the minority approval and valuation requirements apply, is increased to include the approximately 47% indirect interest in BBU in the form of redeemable partnership units of Brookfield Business L.P. (assuming exchange of such redeemable partnership units) held by Brookfield and the approximately 33% indirect interest in BBU in the form of class A exchangeable subordinate voting shares of BBUC held by Brookfield and the public.

MEMBERS Capital Advisors, Inc.

Application to the Ontario Securities Commission for a ruling pursuant to subsection 74(1) of the Securities Act (Ontario) (the Act) for a ruling that the Applicant be exempted from the adviser registration requirements in subsection 25(3) of the Act. The Applicant will provide advice to its Canadian affiliate in Ontario only for so long as such affiliate remains an affiliate of the Applicant.

UPON the application (the Application) of MEMBERS Capital Advisors, Inc. (the Applicant) to the Ontario Securities Commission (the Commission) for a ruling pursuant to subsection 74(1) of the Act that the Applicant be exempted from the adviser registration requirements in subsection 25(3) of the Act;

AND UPON considering the Application and the recommendation of staff of the Commission;

AND UPON the Applicant having represented to the Commission as follows:

Background

1. The Applicant is a corporation existing under the laws of the State of Iowa, with its principal office located in Madison, Wisconsin. The Applicant does not have an office or employees in Canada.

2. The Applicant is part of a group of companies owned by CUNA Mutual Holding Company, a mutual insurance holding company that is a provider of insurance and financial services to credit unions and their members, headquartered in Madison, Wisconsin and collectively known as "CUNA Mutual Group". The Applicant is a wholly-owned investment adviser subsidiary of CUNA Mutual Group.

3. The Applicant is registered as an adviser with the United States Securities and Exchange Commission under the United StatesInvestment Advisers Act of 1940. The Applicant has assets under management of over US$28 billion for CUNA Mutual Group entities.

4. The Applicant is in compliance in all material respects with securities laws of the United States of America. The Applicant is not in default of any requirements of securities legislation of any jurisdiction in Canada.

5. The Applicant is an affiliate of Assurant Life of Canada (the Ontario Affiliate). The Ontario Affiliate is incorporated under the laws of Ontario and is indirectly wholly-owned by CUNA Mutual Holding Company. The Ontario Affiliate is licensed to carry on the business of an insurance company in all provinces and territories in Canada, and provides funeral insurance, final expense insurance and executor insurance. The head office of the Ontario Affiliate is located in Toronto, Ontario.

6. The Applicant proposes to provide investment advice and portfolio management services to the Ontario Affiliate and any other affiliates in Ontario which may be formed or acquired in the future that (i) are licensed or otherwise duly permitted or authorized to carry on the business of an insurance company in Canada or a branch of a foreign insurance company in Canada, or (ii) are holding companies that have as their principal business activity to hold securities of one or more affiliates that are each licensed or otherwise duly permitted or authorized to carry on business as an insurance company in Canada. The investment advice and portfolio management services will be with respect to the portfolio assets of the Ontario Affiliate or any future affiliate. It is expected that the Applicant will provide investment advice and portfolio management services on approximately US$1.9 billion of assets of the Ontario Affiliate.

7. The Applicant is not registered as an adviser in any jurisdiction of Canada and cannot rely on the international adviser registration exemption set out in section 8.26 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103) because the Applicant may provide advice on securities that are not a "foreign security" (as defined in Section 8.26(2) of NI 31-103) and that is not incidental to advice on a foreign security.

8. The Ontario Affiliate is a "permitted client" as defined in section 1.1 of NI 31-103.

9. There is no requirement for employees of a corporation to be registered as advisers under the Act if such employees provide investment advice to their employer with respect to the portfolio assets held by such employer. The Ontario Affiliate currently employs an individual who provides investment advice and direction with respect to its Canadian portfolio assets, but the Ontario Affiliate intends to outsource the adviser function to the Applicant, an affiliate of the Ontario Affiliate. Outsourcing the investment function is permitted under the Insurance Act (Ontario).

10. The Canadian portfolio assets held by the Ontario Affiliate and expected to be managed by the Applicant are owned by the Ontario Affiliate. There are no external stakeholders (such as, for example, holders of variable annuity contracts or segregated funds/separate accounts for policyholders) that have any direct interest in the performance of such portfolios. Accordingly, there is no stakeholder in Ontario or elsewhere other than the Ontario Affiliate that would be directly affected by the investment advice provided by the Applicant.

11. Subsection 74(1) of the Act provides that a ruling may be made by the Commission that a person or company is not subject to section 25 of the Act, subject to such terms and conditions as the Commission considers necessary, where the Commission is satisfied that to do so would not be prejudicial to the public interest.

AND UPON the Commission being satisfied that to do so would not be prejudicial to the public interest;

IT IS RULED, pursuant to subsection 74(1) of the Act, that the Applicant is exempt from the adviser registration requirements of subsection 25(3) of the Act in respect of it acting as an adviser to its affiliates in Ontario, provided that:

1. the Applicant provides investment advice and portfolio management services in Ontario only to its affiliates that:

(a) are licensed or otherwise duly permitted or authorized to carry on business as an insurance company in Canada or a branch of a foreign insurance company in Canada; or

(b) are holding companies that have as their principal business activity to hold securities of one or more affiliates that are each licensed or otherwise duly permitted or authorized to carry on business as an insurance company in Canada; and

2. with respect to any particular affiliate, the investment advice and portfolio management services provided in Ontario are provided only as long as that affiliate remains:

(a) an "affiliate" of the Applicant as defined in the Act, and

(b) a "permitted client" as defined in NI 31-103.

DATED at Toronto, Ontario, this 12th day of October, 2021.

Brookfield Property Partners L.P. and Brookfield Property Preferred L.P.

National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions -- Filers want to put in place a credit support issuer structure, but are unable to rely on the exemption for credit support issuers in applicable securities legislation -- Relief granted from continuous disclosure requirements, certification requirements, insider reporting requirements, audit committee requirements and corporate governance requirements -- Relief also granted from incorporation by reference requirements, earnings coverage requirements and subsidiary credit supporter requirements -- Filers unable to rely on exemption for credit support issuers in applicable securities legislation since the Holding LP and Brookfield Property Partners are partnerships, as well as the fact that Brookfield Property Partners satisfies its continuous disclosure obligations by complying with U.S. federal securities law as is permitted under NI 71-102 -- Relief granted subject to conditions.

Securities Act, R.S.O. 1990, c. S.5, ss. 107 and 121(2)(a)(ii).

National Instrument 44-101 Short Form Prospectus Distributions, ss. 2.4 and 8.1(2).

Form 44-101F1 Short Form Prospectus, ss. 6.1, 11.1(1), 12.1 and 13.3.

National Instrument 51-102 Continuous Disclosure Obligations, ss. 13.1 and 13.4.

National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings, ss. 8.5 and 8.6.

National Instrument 52-110 Audit Committees, ss. 1.2(g) and 8.1.

National Instrument 55-102 System for Electronic Disclosure by Insiders (SEDI), s. 6.1.

National Instrument 58-101 Disclosure of Corporate Governance Practices, ss. 1.3(c) and 3.1(2).

July 2, 2021

The principal regulator in the Jurisdiction has received an application (the Application) from Brookfield Property Partners and the Issuer (collectively, the Filers) for a decision under the securities legislation of the principal regulator (theLegislation) granting exemptive relief for the Issuer and, in respect of (c), the insiders of the Issuer, from certain requirements including:

(a) the continuous disclosure requirements contained in the Legislation, including requirements under National Instrument 51-102 -- Continuous Disclosure Obligations (NI 51-102), as amended from time to time (the Continuous Disclosure Requirements);

(b) the certification requirements contained in National Instrument 52-109 -- Certification of Disclosure in Issuers' Annual and Interim Filings, as amended from time to time (the Certification Requirements);

(c) the insider reporting requirements contained in the Legislation under section 107 of the Securities Act (Ontario) (the Act) as well as the requirement to file an insider profile and insider reports under National Instrument 55-102 -- System for Electronic Disclosure by Insiders, as amended from time to time, in respect of insiders of the Issuer (the Insider Reporting Requirements);

(d) the requirements of the Legislation relating to audit committees, including, without limitation, National Instrument 52-110 -- Audit Committees, as amended from time to time (the Audit Committee Requirements);

(e) the corporate governance disclosure requirements contained in National Instrument 58-101 -- Disclosure of Corporate Governance Practices, as amended from time to time (the Corporate Governance Requirements and together with the Continuous Disclosure Requirements, Certification Requirements, Insider Reporting Requirements and Audit Committee Requirements, the Reporting Issuer Requirements);

(f) the disclosure requirements contained in paragraphs 1 to 4 and 6 to 8 of item 11 of Form 44-101F1 -- Short Form Prospectus (Form 44-101F1) (the Incorporation by Reference Requirements);

(g) the disclosure requirements contained in item 6 of Form 44-101F1 (the Earnings Coverage Requirements); and

(h) the disclosure requirements contained in item 12 of Form 44-101F1 (the Subsidiary Credit Supporter Requirements and together with the Incorporation by Reference Requirements and the Earnings Coverage Requirements, the Prospectus Disclosure Requirements),

(collectively, the Exemption Sought),

in each case to accommodate the issuance by the Issuer of Class A Cumulative Redeemable Preferred Units (the New LP Preferred Units). The first series of New LP Preferred Units will be issued in connection with the Arrangement (as defined below). The New LP Preferred Units will be guaranteed by Brookfield Property Partners as well as Brookfield Property L.P. (the Holding LP), and each of the Holding Entities (as defined below).

Under the Process for Exemptive Relief Applications in Multiple Jurisdictions (for a passport application):

(1) the Ontario Securities Commission is the principal regulator for this Application; and

(2) the Filers have provided notice that section 4.7(1) of Multilateral Instrument 11-102 -- Passport System (MI 11-102) is intended to be relied upon in British Columbia, Alberta, Saskatchewan, Manitoba, Quebec, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, the Northwest Territories, Yukon and Nunavut (collectively with the Jurisdiction, the Reporting Jurisdictions).

Terms defined in National Instrument 14-101 -- Definitions and MI 11-102 have the same meaning if used in this decision, unless otherwise defined. In this decision, "Brookfield Property Partners Related Entities" means, collectively, the Holding LP and subsidiary entities (as this term is defined in Multilateral Instrument 61-101 -- Take-Over Bids and Special Transactions) of the Holding LP.

This decision is based on the following facts represented by the Filers:

Brookfield Property Partners

1. Brookfield Property Partners is a Bermuda exempted limited partnership that was established on January 3, 2013.

2. The limited partnership units of Brookfield Property Partners (the BPY Units) are listed on the Nasdaq Stock Market (Nasdaq) and the Toronto Stock Exchange (TSX) under the symbols "BPY" and "BPY.UN", respectively. As of June 8, 2021, there were 440,808,732 BPY Units issued and outstanding, and approximately 236,285,505 BPY Units, representing approximately 54% of the total issued and outstanding BPY Units, were beneficially and directly held by Canadian residents. In addition, the Class A Cumulative Redeemable Perpetual Preferred Units of Brookfield Property Partners (the BPY Preferred Units), Series 1, 2 and 3 trade on Nasdaq under the symbols "BPYPP", "BPYPO" and "BPYPN", respectively.

3. Brookfield Property Partners is a reporting issuer in the Reporting Jurisdictions and is not in default of any requirements under applicable securities legislation or the rules and regulations made pursuant thereto in the Reporting Jurisdictions.

4. Brookfield Property Partners is a SEC foreign issuer within the meaning of section 1.1 of National Instrument 71-102 -- Continuous Disclosure and Other Exemptions Relating to Foreign Issuers (NI 71-102) and satisfies its continuous disclosure obligations by complying with U.S. federal securities laws as is permitted under NI 71-102.

5. The general partner of Brookfield Property Partners is Brookfield Property Partners Limited (BPY General Partner), a Bermuda company and also a wholly-owned subsidiary of Brookfield Asset Management Inc. (BAM). BPY General Partner holds a 0.02% general partnership interest in Brookfield Property Partners. The mind and management of BPY General Partner is located in Bermuda.

6. BAM, a Canadian company, is Brookfield Property Partners' largest holder of BPY Units. As of June 8, 2021, BAM owned, directly or indirectly, 139,699,123 BPY Units and 451,365,017 Redemption-Exchange Units (defined below), collectively representing approximately 66% of the BPY Units (assuming the exchange of the Redemption-Exchange Units) or 61% on a fully-exchanged basis assuming the exchange of the Redemption-Exchange Units, the issued and outstanding class A preferred limited partnership units of the Holding LP (the Class A Preferred Units), series 1, 2 and 3 and the issued and outstanding exchangeable limited partnership units (the Exchange LP Units) of Brookfield Office Properties Exchange LP not held by subsidiaries of Brookfield Property Partners. As of June 8, 2021, BAM also owned, directly or indirectly, 138,875 general partner units of Brookfield Property Partners and 4,759,997 special limited partnership interests in the Holding LP.

7. Brookfield Property Partners' assets consist of a 100% managing general partnership interest in the Holding LP, a Bermuda exempted limited partnership that was established on January 4, 2013 and an interest in BP US REIT LLC.