Ontario Securities Commission Bulletin

Issue 43/04 - January 23, 2020

Ont. Sec. Bull. Issue 43/04

• Frontenac Mortgage Investment Corporation

• Capital International Asset Management (Canada), Inc.

• Pengrowth Energy Corporation

• Temporary, Permanent & Rescinding Issuer Cease Trading Orders

• Temporary, Permanent & Rescinding Management Cease Trading Orders

• CSE -- Amendments to Trading System Functionality & Features -- Notice of Approval

• Canadian Securities Exchange -- Proposed Amendments to Trading System -- Notice of Withdrawal

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

CSA Notice 23-325 Trading Fee Rebate Pilot Study

January 23, 2020

The Canadian Securities Administrators (the CSA or we) have either approved or not objected to{1} the Trading Fee Rebate Pilot Study that applies temporary pricing restrictions on marketplace transaction fees applicable to trading in certain interlisted and non-interlisted securities (the Pilot Study). The implementation of the Pilot Study will be conditional on the implementation of a similar study in the United States (the SEC Fee Pilot).{2} In the event the SEC Fee Pilot does not proceed, the CSA will not move forward with the implementation of the Pilot Study.

We are publishing the design of the Pilot Study (the Final Design Report) at Appendix A and the form of an order for the implementation of the Pilot Study at Appendix B to this Notice. The Final Design Report will also be available on the websites of other CSA jurisdictions, including:

www.lautorite.qc.cawww.albertasecurities.comwww.bcsc.bc.cawww.fcnb.canssc.novascotia.cawww.osc.gov.on.cawww.fcaa.gov.sk.cawww.mbsecurities.ca

The Pilot Study will begin on a date concurrent with the implementation of the SEC Fee Pilot. Once we have confirmation that the SEC Fee Pilot is proceeding, we will publish a notice of implementation that will provide additional details including the start date of the Pilot Study. See Part IV of this Notice for additional information regarding timing and duration.

The CSA is concerned that the payment of rebates by marketplaces may be affecting the behaviour of marketplace participants by:

1. creating conflicts of interest for dealer routing decisions that may be difficult to manage;

2. contributing to increased segmentation of order flow; and

3. contributing to increased intermediation in actively traded securities.

The purpose of the Pilot Study is to determine the effects of the prohibition of rebate payments by Canadian marketplaces.

The CSA has been considering a pilot study on the payment of trading fee rebates for a number of years as part of our continued work to foster fair and efficient capital markets and confidence in capital markets. On May 15, 2014, we published a Notice and Request for Comment (the 2014 Notice) that proposed amendments to National Instrument 23-101 Trading Rules (NI 23-101) in relation to the order protection rule (OPR).{3} On April 7, 2016, as a result of our review of OPR, we published a Notice of Approval of Amendments to NI 23-101 and Companion Policy 23-101CP (the 2016 Notice).{4} In the 2016 Notice, we acknowledged that we had been considering a pilot study to analyse the impact of the payment of trading fee rebates. However, despite stakeholder support, feedback from commenters and academics suggested that there are certain risks to running a pilot study independent of the United States due to the interconnected nature of North American markets and Canadian equity securities that are interlisted in the United States. Therefore, we decided not to move forward with a pilot study unless a similar study was undertaken in the United States.{5}

On March 14, 2018, the United States Securities and Exchange Commission (SEC) proposed new Rule 610T of Regulation National Market System (NMS) that would conduct a transaction fee pilot for NMS securities,{6} resulting in an opportunity for a Canadian pilot study.

On March 16, 2018, we published CSA Staff Notice 23-322 Trading Fee Rebate Pilot Study{7} to provide an update on our plans to study the impacts of transaction fees and rebates on order routing behaviour, execution quality, and market quality, and noted that we have been engaged in dialogue with SEC Staff. In July 2018, we retained three Canadian academics (the Academics){8} to design the Pilot Study and measure the results. Then, on September 12, 2018, the Capital Markets Institute at the Rotman School of Management held an event where the Academics provided a presentation of their preliminary thoughts on the structure of the Pilot Study, followed by a panel discussion and open forum.

On December 18, 2018, we published CSA Staff Notice and Request for Comment 23-323 Trading Fee Rebate Pilot Study (the 2018 RFC){9} to obtain feedback on the design, specifications, and implementation of the then proposed pilot. The 2018 RFC was published for a 45-day comment period, which, following stakeholder feedback,{10} was extended to March 1, 2019 by way of CSA Staff Notice 11-340 Extension of Comment Period.{11} A list of those who submitted comments and a summary of the comments and our responses are attached at Appendix C to this Notice. Copies of the comment letters are available at www.osc.gov.on.ca. Notably, a joint letter submitted by nine Canadian pension plans and global asset managers expressed strong support for the Pilot Study. In contrast, all but one marketplace do not support it. However, the majority of stakeholders, including dealers, are in favour of the Pilot Study.

On December 19, 2018, the SEC published new Rule 610T of Regulation NMS to conduct the SEC Fee Pilot. The SEC Fee Pilot allows for coordination with the Pilot Study and we will continue our discussions with SEC Staff to align the two pilot studies.

a. Timing and Duration

The Pilot Study will be implemented on a staggered basis consisting of two stages:

1. interlisted securities in tandem with the implementation of the SEC Fee Pilot, if possible; and

2. non-interlisted securities and exchange-traded products (ETPs) three months following the introduction of interlisted securities.

We intend to provide market participants with as much notice as is possible prior to implementation of the first stage of the Pilot Study. However, it is important that the implementation of the Pilot Study be aligned with the timing of the SEC Fee Pilot. Given the uncertainty regarding the SEC Fee Pilot, we note that implementation timing may need to be expedited. Once we have confirmation that the SEC Fee Pilot is proceeding, we intend to issue orders in the form at Appendix B of this Notice for each of the applicable marketplaces, outlined in further detail below. These orders will be accompanied by a public notice that sets out additional details of implementation, including the start date of the Pilot Study.

With respect to the duration of the Pilot Study, we expect that it will conclude in tandem with the SEC Fee Pilot, at which point the fee structures of all marketplaces are expected to revert to those in place prior to the Pilot Study. Marketplaces will then be permitted to file any fee change that accords with Canadian securities laws subject to further regulatory action that may result from the analysis of the Pilot Study.

Throughout the Pilot Study, the Academics will review the market quality metrics identified in the Final Design Report on an ongoing basis. Where these metrics indicate that the Pilot Study is having a significant and extended detrimental impact on market quality, the CSA will respond promptly and the Alberta Securities Commission, British Columbia Securities Commission, and Ontario Securities Commission (together, the Commissions) will proceed to issue orders under their respective securities legislation revoking or varying the orders implementing the Pilot Study, effectively ending or varying it.{12}

b. Applicable Marketplaces

The Pilot Study will be applicable to all trading fee rebates paid by Canadian marketplaces, both exchanges and alternative trading systems (ATSs), for the execution of orders with respect to certain equity securities and ETPs, outlined in greater detail below. The Pilot Study will apply to all trading fee models, including "maker-taker" and "inverted maker-taker."

c. Pilot Study Securities

The Pilot Study will consist of two samples:

1. A set of securities selected from a list of highly liquid securities that is prepared and published by the Investment Industry Regulatory Organization of Canada (IIROC);{13} and

2. A set of actively traded, medium liquidity securities that has been constructed by the Academics.

These sample securities include both interlisted and non-interlisted common stocks, as well as ETPs, that are listed on the TSX and TSXV. The list of Pilot Study securities will be appended to the orders implementing the Pilot Study.

Half of the sample securities will be assigned to a treatment group for which a prohibition of trading fee rebates will be applied. Each security in the treatment group will be matched with a control security that has similar characteristics, including firm size, share price, and trading volume. Trading fee rebates will continue to be permitted for those securities in the control group.

The selection of ETPs in the sample will follow the approach described in the Final Design Report. ETPs with the same underlying index will be placed together into either the treatment or control group. ETPs in the treatment group will be matched with other ETPs with the same underlying security type (i.e. fixed income, equity, commodities etc.), but a different underlying index.

d. Pilot Study Design

The Pilot Study prohibits the payment of trading fee rebates, including linked pricing, by marketplaces with respect to trading in treated securities.{14} The Academics will conduct an empirical analysis based on market quality metrics and compare the treated securities with the control securities. This statistical analysis will investigate the effects of the prohibition of rebates by comparing changes in market quality for the treatment and control group securities.

In the event that the SEC Fee Pilot does not proceed, the CSA considered conducting the Pilot Study with only non-interlisted securities. However, we ultimately determined that we should not do so largely because we were not confident of the extent to which the results of such a pilot study could be extended across all securities for policy-making purposes. In addition, it is questionable whether such a pilot study would result in sufficient data to analyze the impact and justify the technology-related costs that would be incurred by industry.

Please see Appendix A for the Final Design Report. Please also refer to GitHub for ongoing code and data analysis from the Academics as the Pilot Study moves forward.{15}

e. Market Making Programs under the Pilot Study

We believe that exchange market makers play an important role in enhancing liquidity and ensuring an orderly market. However, to avoid possible distortion of the Pilot Study and interference with the ability to meaningfully analyze data collected, we are of the view that the payment of trading fee rebates by marketplaces with respect to trading in treated securities for all market participants, including exchange market makers, should be prohibited.

While the payment of rebates for treated securities will be prohibited, we will review fee proposals filed by exchanges for other non-rebate incentives offered as part of an exchange market making program and make decisions according to the customary approval process. Although we believe that the prohibition of linked pricing supports the integrity of the Pilot Study in generating useful market quality metrics, we are of the view that an exception to a linked pricing prohibition to permit non-rebate linked pricing to exchange market makers is appropriate. We believe that non-rebate incentives applicable to registered market making activities are less likely to interfere with the objectives of the Pilot Study and may further encourage the participation of market makers and enhance liquidity provision. Similar to the SEC Fee Pilot, these incentives can be offered only to registered market makers and only for their market making activity. As an example, a marketplace could offer its market makers volume-based incentives on a monthly basis. For clarity, the CSA intends to closely align its approach here with that taken by the SEC.{16}

Certain jurisdictions are publishing other information required by local securities legislation. In Ontario, the Pilot Study will be implemented by orders of the Commission under ss. 21(5) and 21.0.1 of the Securities Act (Ontario), as applicable for each exchange and ATS carrying on business in Ontario. The Alberta and British Columbia Securities Commissions will also issue orders implementing the Pilot Study, as applicable for exchanges recognized in those jurisdictions. In each of these three jurisdictions, the respective orders will provide that where a marketplace pays a trading fee rebate with respect to trading in a security that is included in a treatment group in the Pilot Study, that marketplace shall file a fee amendment that would eliminate the rebate payment for the duration of the Pilot Study.

The Commissions will also order that for the duration of the Pilot Study, where a marketplace seeks any amendment to its Form 21-101 F1 or Form 21-101 F2, including the exhibits thereto, that marketplace will file submissions that satisfy the applicable Commission that any proposed amendments do not negatively impact the objective of the Pilot Study. The form of an order, representative of the orders that will be presented to the Commissions to be signed once implementation is confirmed, is attached at Appendix B.

A. Final Design Report;

B. Form of an order for the implementation of the Pilot Study; and

C. List of commenters along with chart summarizing comments and CSA response.

Questions and comments may be referred to:

{1} The Autorité des marchés financiers and the Ontario Securities Commission have approved the Trading Fee Rebate Pilot Study. In addition, the Alberta Securities Commission, the British Columbia Securities Commission, the Financial and Consumer Affairs Authority of Saskatchewan, the Financial and Consumer Services Commission of New Brunswick, the Manitoba Securities Commission, the Nova Scotia Securities Commission, the Office of the Superintendent of Securities, Service Newfoundland and Labrador, the Prince Edward Island Office of the Superintendent of Securities, the Department of Justice of the Government of Nunavut, the Office of the Superintendent of Securities of the Northwest Territories and the Office of the Yukon Superintendent of Securities have not objected to the Trading Fee Rebate Pilot Study.

{2} Published at: https://www.sec.gov/rules/final/2018/34-84875.pdf. Please also see the "Notice Establishing the Commencement and Termination Dates of the Pre-Pilot Period of the Transaction Fee Pilot for National Market System Stocks," published at: https://www.sec.gov/rules/other/2019/34-85906.pdf.

{3} Published at: (2014) 37 OSCB 4873.

{4} Published at: (2016) 39 OSCB 3237.

{5} Please refer to section 7 Pilot Study on Prohibition on Payment of Rebates by Marketplaces in (2016) 39 OSCB 3237.

{6} Published at: https://www.sec.gov/rules/proposed/2018/34-82873.pdf.

{7} Published at: http://www.osc.gov.on.ca/en/SecuritiesLaw_sn_20180316_23-322_trading-fee-rebate-pilot-study.htm.

{8} The CSA selected the following group of researchers with expertise in Canadian equity market structure to design and conduct the pilot study: Katya Malinova, Andriy Shkilko, and Andreas Park. The announcement regarding the retaining of the Academics was published at: http://www.osc.gov.on.ca/en/NewsEvents_nr_20180801_csa-trading-fees-rebates-pilot-study.htm.

{9} Published at: http://www.osc.gov.on.ca/en/SecuritiesLaw_csa_20181218_23-323_trading-fee-rebate-pilot-study.htm.

{10} Please see Comment Letter from Deanna Dobrowsky, Vice President, Regulatory Office of the General Counsel of TMX Group dated January 9, 2019, available at http://www.osc.gov.on.ca/documents/en/Securities-Category2-Comments/com_20190109_23-323_tmx.PDF.

{11} Published at: http://www.osc.gov.on.ca/en/SecuritiesLaw_csa_sn_20190117_11-340_rebate-pilot-study.htm.

{12} In Ontario, the Ontario Securities Commission will issue orders under s. 144 of the Securities Act (Ontario), revoking or varying the orders issued under ss. 21(5) and 21.0.1, as applicable.

{13} Please see: http://www.iiroc.ca/industry/rulebook/Pages/Highly-Liquid-Stocks.aspx.

{14} This will include the prohibition of rebate payments for intentional crosses.

{15} See: https://github.com/mps-consulting/CSA-feepilot.

{16} See supra note 6 at pp. 77-83.

First version: July 24, 2018

This version: August 15, 2019

The CSA has proposed a pilot study to better understand the effects of the prohibition of rebate payments by Canadian marketplaces (the Pilot). The United States Securities and Exchange Commission (SEC) has announced its intention to conduct a pilot study examining a similar set of issues (the SEC Pilot).

Rebates are often paid to market participants to attract their orders to a particular platform. The CSA has commissioned the authors of this report to develop the methodology for the Pilot, analyze the results, and complete a final research report detailing the findings. In this document, we propose a design and discuss the framework for the analysis. In particular, we cover the following issues: timing, sample construction, empirical measures, statistical tools, and anticipated challenges. We also address feedback received during public consultations.

An important feature of the Pilot is design simplicity. A complex design that aims to address too many questions may confound the analysis to the detriment of drawing policy-relevant conclusions. Consequently, key conditions for the Pilot to be successful are as follows:

• for a group of securities selected using objective and transparent criteria (hereafter, treated securities), marketplaces are prohibited from paying fee rebates{1} to dealers, including offering discounts on liquidity removal fees if such discounts are linked to the dealers' liquidity-providing activities. For all remaining securities, the rules remain unchanged;

• the prohibition applies to all marketplaces trading equity securities;

• with respect to interlisted securities, the timing of the Pilot and the set of the Pilot securities are coordinated with the SEC to the extent possible;

• the Pilot is introduced in two stages, if possible, to mitigate the effects of unexpected market-wide events that may coincide with the Pilot start date;

• in the analysis stage, a set of market quality and order routing metrics is computed using detailed audit-trail-level data;

• a set of standard techniques is applied to examine this data; and

• the codes used in the analysis are publicly available through GitHub, and comments are encouraged.

The sample will be selected from corporate equity securities and Exchange Traded Products (ETPs). The corporate equity securities will be split into highly liquid and medium liquid. Each treated security will be matched with a control security that has similar characteristics, e.g., firm size, share price, and trading volume. The control securities will not be treated. The sample selection will be governed exclusively by statistical considerations. We expect the sample to consist of:

• 50-60 highly liquid and 20-30 medium liquid, interlisted securities, with an equal number of interlisted matches,

• 60-80 highly liquid and 80-100 medium liquid, non-interlisted securities, with an equal number of non-interlisted matches, and

• 20-30 ETPs, with an equal number of matches selected from among ETPs that follow distinctly different security baskets.

The precise numbers of securities will be determined on the date the sample is finalized prior to the start of the Pilot.

In the analysis stage, we will use standard market quality metrics (e.g., quoted spreads and depths, effective and realized spreads, implementation shortfall, volatility, trade and order autocorrelation, time to execution for competitively priced limit orders, etc.). We will examine these metrics before and after rebate prohibition for the market overall and for several types of market participants separately (e.g., market makers, dealers, retail investors, institutional participants, participants using high frequency strategies, etc.). The final report will present the results taking care to preserve anonymity of the participants.

A. Background

In its 2014 Request for Comments on Proposed Amendments to NI 23-101 Trading Rules,{2} the CSA points out that concerns had been raised about the maker-taker model's ability to "distort transparency of the quoted spread, introduce inappropriate incentives and excessive intermediation, and create conflicts of interest" and proposes conducting a pilot study to formally examine these issues. The CSA specifically states that any pilot should "examine the impact of prohibiting the payment of rebates by marketplaces."

In proposing the Pilot design, we seek to better understand how the prohibition of rebates may affect dealers' routing practices, the level of intermediation, and standard measures of market quality. The analysis will be carried out for the market overall and for various groups of market participants separately. We anticipate that this analysis will facilitate future policy decisions with respect to rebates and allow these decisions to be made in the most fair and transparent manner, reflecting the interests and views of all stakeholders.

In what follows, we provide a detailed description of the data, variables, and methods that will allow us to address the issues raised by the CSA. For the results to be meaningful and policy-relevant, it is important to have sufficiently large and well-structured treatment and control samples. Where possible, a staggered introduction of treatment would help minimize the likelihood of an exogenous event confounding the results. Furthermore, we will seek close coordination with the SEC, since trading in Canada may be affected by the implementation of the SEC Pilot.

B. Merits of a Canadian Pilot

Although the U.S. and the Canadian equity markets are similar, there are several key differences that may affect dealer routing decisions. Examples include the practice of retail order internalization in the U.S. and broker-preferencing in Canada. Therefore, while we expect rebate prohibition to have a similar impact on market-wide measures of market quality in both countries, changes in routing practices and the extent to which different groups of market participants are affected may differ. Consequently, a Canadian Pilot, in combination with sufficiently granular data, will substantially improve our understanding of the existing fee system and will be necessary for a well-informed Canadian regulatory policy.

C. Required Data

The Pilot aims to examine discretionary routing practices and the impact of fees on different groups of market participants. Using detailed data, we will define a trader ID as the combination of the dealer ID, user ID, and account type (specialist, client, inventory, etc.). Once defined, we will use trader IDs following the classification of market participants proposed by Devani, Tayal, Anderson, Zhou, Gomez, and Taylor (2014).

A. Background

There are about 3,800 securities listed on Canadian stock exchanges, some of which are interlisted on foreign exchanges. Trading characteristics differ significantly across securities and in constructing the sample we must ensure that such differences do not confound the results.

First, many securities trade almost exclusively in rebate-free environments. Examples include CSE-listed securities, as well as TSX-- and TSXV-listed securrities priced under $1 that trade on the TSX, TSXV, and MatchNow. Such securities will not be included in the sample.

Second, we expect that our analysis will provide the most statistically reliable results for the highly liquid securities. However, we recognize that there is significant interest in examining the impact of a rebate prohibition on securities with medium activity levels. Therefore, we will analyze a sample of such securities, but we caution that the resulting market quality measures may be statistically noisy. We will also examine the effect of a rebate prohibition on ETPs. We will not examine very illiquid securities, as such an analysis will not yield statistically meaningful insights. We will split the corporate equities into two subsamples: U.S.-interlisted equities and non-interlisted equities. In our analysis, we will present the results separately for the two subsamples.

B. Sample Selection and Matching Criteria for Corporate Securities

The two subsamples of corporate equities will be further split into highly liquid and medium liquid securities. IIROC defines a security to be "highly liquid" if it trades on average at least 100 times per day and with an average trading value of at least $1,000,000 per trading day over the past month.{3} Highly liquid securities account for more than 90 percent of TSX market capitalization and as such are reasonably representative of the wealth invested in publicly-listed Canadian corporate equities. We will define a security as "medium liquid" if it trades on average at least 50 times a day and with an average daily trading value of at least $50,000 over the past month.

To select the treatment and control groups, we will use a procedure that finds stocks similar to each other based on a set of predefined characteristics and then randomly selects a stock to treat from each pair. We will use the following matching characteristics captured prior to the Pilot start date: listing status (single market vs. interlisted), liquidity status (highly liquid vs. medium liquid), firm size (market capitalization), price, and dollar trading volume, with the last three characteristics averaged over the month preceding the selection date. The list of Pilot securities will be appended to the orders implementing the Pilot.

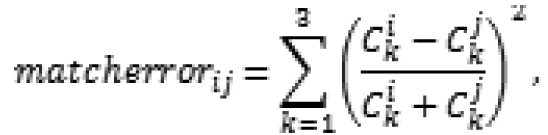

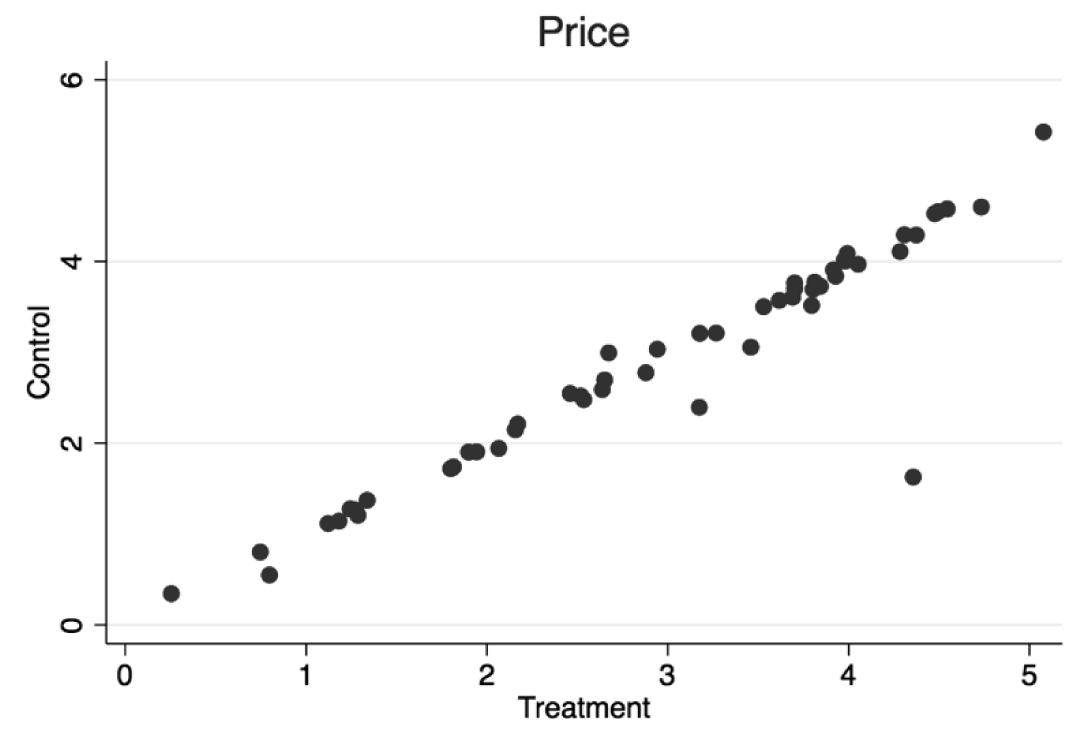

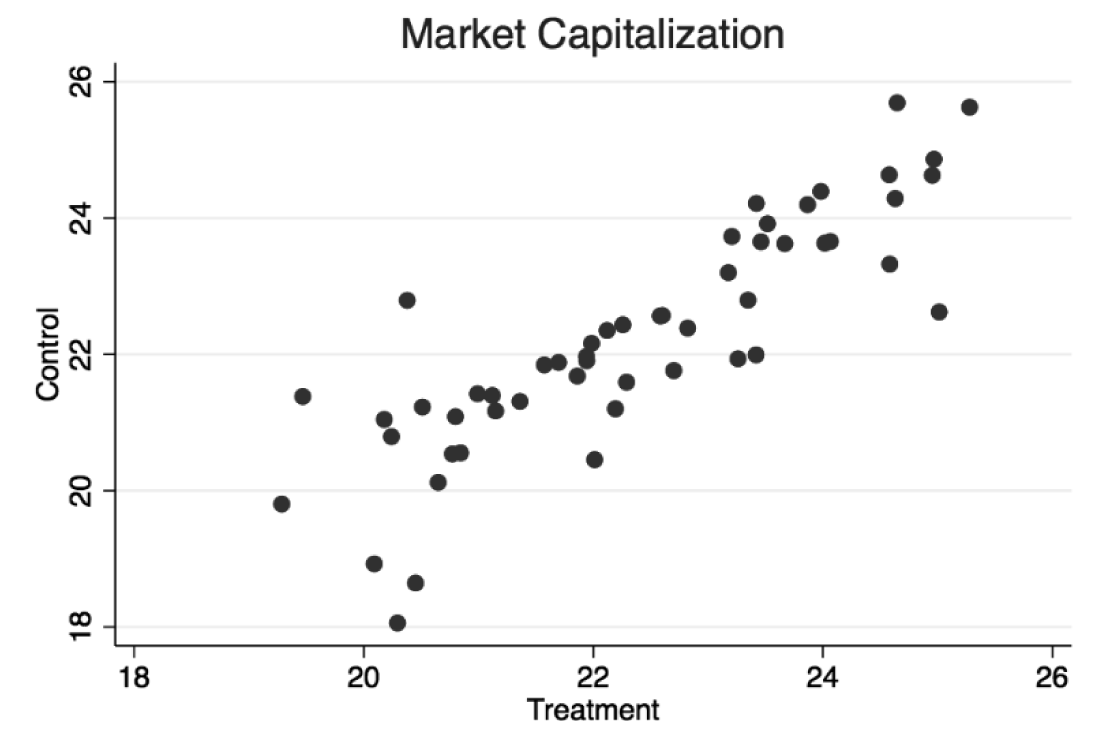

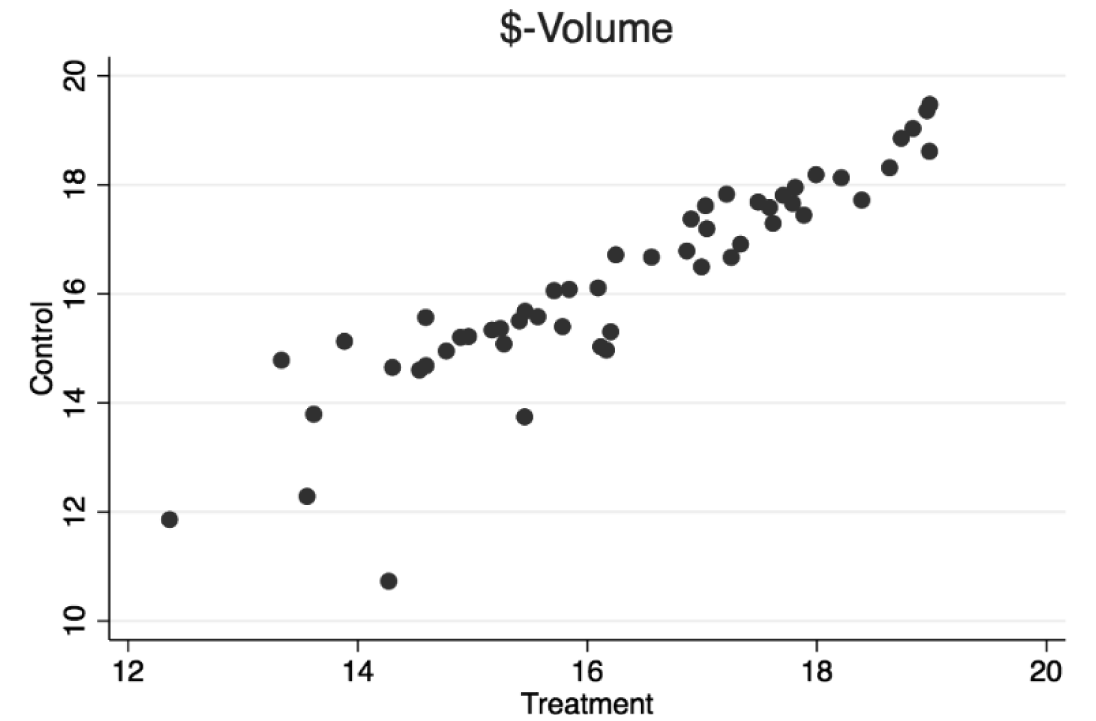

We will follow the approach known as the nearest-neighbour matching. Specifically, for each possible pair of securities, i and j, we will compute the pairwise scaled matching error as follows:

where Ck is one of the above-mentioned matching characteristics, e.g., firm size, price, and trading volume. We will then sequentially select pairs with the lowest matching errors until all stocks are allocated a pair. Finally, we will randomly assign one stock in each pair for treatment and retain the other stock as a control.

C. Sample Selection and Matching Criteria for ETPs

The comments on the original pilot design were mixed, although largely in support of including ETPs in the study. This said, respondents were concerned that the necessary partition of ETPs into a no-rebate and a control sample could create "winners and losers." As an example, consider two fictional ETPs that have the same underlying basket of securities: ATSX and ZTSX. The similarity of the underlying basket makes it tempting to assign these ETPs as matches, with one in the no-rebate group and the other in the control group. Such an assignment may, however, result in investors favouring one product over the other. If the current system of rebates is beneficial to liquidity, the control product will benefit. If the current system is not beneficial, the treated product will benefit.

To address respondents' concerns and avoid influencing investor preferences for similar ETPs, we will use the underlying index as one of the criteria to assign ETPs into the treatment and control groups. More specifically, both ATSX and ZTSX in the example above will be assigned into either a treatment or a control group. Their matches will be selected from ETPs with different underlying baskets. Further, we expect to match ETPs with the same underlying security type: equity ETPs to equity ETPs, fixed income to fixed income, etc. The rest of the matching procedure will resemble that described earlier for the corporate securities. In particular,

• we will separate ETPs into categories based on the underlying security type;

• within these categories, we will identify ETP groups that have the same underlying basket;

• we will match these groups with the ETP groups that have the same security type but a different underlying basket. Matching will be done by traded volume and price; and

• once matches are identified, we will randomly assign one of the matched groups to be treated and the other as a control.

We do not anticipate active ETPs to be included in the Pilot.

A. Empirical Measures

Quoted Liquidity. The quoted spread will be computed as the difference between the Canada-wide best ask and bid prices (the CBBO). We will compute this metric in two ways: (i) across all markets and (ii) for the markets with protected quotes. The quoted spread at time t for security i is defined as:

We will drop instances of locked markets, when the bid and the ask are equal, and instances of crossed markets, when the bid is greater than the ask.

Spreads usually vary by stock price. As such, it is common practice to compute the proportional spread as:

where mit is the CBBO midquote defined as:

To aggregate the spread metrics to the daily level, we will compute the time-weighted quoted spread on day d as follows:

where [DGR]t,t+1 is the number of time units during which the quote is active. For instance, if a quote is active from 14:35:00.002 to 14:35:08.004, then [DGR]t,t+1 = 8,002 milliseconds (ms).

Some of the stocks in our sample will likely be constrained by the minimum tick size of one cent. To account for this possibility, we will compute the fraction of the day that a stock is quoted with a one cent spread.

We will compute quoted depth as the sum of the number of shares posted on both sides of the CBBO. We will compute quoted dollar depth as the sum of the dollar value of shares posted on both sides of the CBBO. We will time-weight both depth metrics.

In addition, we will examine the breadth of liquidity provision and diversification of passive liquidity by counting the number of market participants that provide liquidity and the level of competition among them based on presence at the best quotes and the frequency as well as degree of price improvement.

Price Efficiency. The finance literature has developed a number of metrics that capture the speed with which (and the extent to which) prices incorporate new information. Generally speaking, the faster the price discovery process, the more informationally efficient the prices.

Autocorrelation of Returns. Similarly to Hendershott and Jones (2005), we will compute the autocorrelation of midquote returns for 30-second, 1-minute, and 5-minute intervals. A lower absolute value of autocorrelation is associated with greater market efficiency as prices better resemble a random walk.

Variance Ratios. If prices are efficient and follow a random walk, the variance of midquotes is linear in the time horizon. Campbell, Lo, and MacKinlay (1997) define the scaled ratio of variances over k time horizons as: |(stk/kst) -- 1| and suggest that the closer this ratio is to 0, the more efficient the market. We will follow the existing literature and compute the variance ratios for two intervals: 30-seconds to 1-minute and 1-minute to 5-minutes.

Intra-Day Volatility. We will compute two volatility metrics: range-based and variance-based. The range-based metric is the daily average of the high-low price range computed over ten-minute intervals, scaled by the interval's midquote defined in equation 4 above. Aggregated over many securities, this metric is usually strongly correlated with overall market volatility as measured by the CBOE Volatility Index (VIX).{4} The variance-based metric is the standard deviation of the one-minute midquote returns for the day.

Activity Levels. To measure market activity, we will compute several trading volume metrics such as volume at the open and close, volume during the continuous market, volume in intentional crosses, and dark volume.

We will further compute a set of order-related metrics, such as the number of orders and their value, the proportion of canceled and executed orders, the proportion of executed order value, the number of orders that match or improve the CBBO, and the proportion of orders one and two cents away from the best quotes, as well as one percent and five percent of the midquote away from the best quotes. We will pay particular attention to changes in order routing practices to examine the effects of incentive changes related to rebate prohibition.

We note that there are no agreed upon economic measures that determine whether a change in market activity levels is beneficial or harmful. Therefore, volume and order submission figures must be interpreted with caution.

Effective Spreads. Effective spreads measure the costs that market participants incur when they trade. It is conventional to base the computation of effective spreads on the midquote of the prevailing CBBO. For security i, the proportional effective spread for a trade at time t is:

where pit is the transaction price, mit is the midquote of the CBBO prevailing at the time of the trade, and qit is an indicator variable that equals 1 if the trade is buyer-initiated and -1 if the trade is seller-initiated. The factor 2 is used to make the estimate comparable to the quoted spread by capturing the cost of a round-trip transaction. We will also examine a variation of the effective spread, entitled investable spread, which is the dollar cost of trading of a standard size order.

To obtain a daily effective spread estimate, it is common to volume-weight transaction-specific estimates, i.e., for trades of volumes vit, the effective spread on day d is the sum of the trades' effective spreads weighted by the trades' shares of total daily volume:

The purpose of the Pilot is to gain a better understanding of the effects of the prohibition of rebate payments by Canadian marketplaces, and we will therefore compute the "cum fee" effective spread (often referred to in the industry as the "economic" spread):{5}

Price Impact and Realized Spread. It is common practice to decompose the effective spread into the price impact and the realized spread. The price impact measures by how much the trade moves the price and is formally defined as:

where mi,t+t is the CBBO midquote t time units after the trade. The idea behind this measure is that trades reveal information about the fundamental value of the underlying security and the market needs time to incorporate this information into prices. The time horizon t usually varies between five milliseconds for frequently traded stocks and five minutes for less frequently traded ones.

The price impact is directly related to the realized spread, which is defined as:

and is interpreted as the revenue that liquidity providers receive net of the adverse selection costs captured by the price impact. Analogously to the cum fee effective spreads, we will account for the rebates that liquidity providers are eligible to receive and will compute the cum rebate realized spreads as follows:

Implementation Shortfall. Buy-side institutions often trade amounts that are larger than the depth available at the best prices and therefore commonly slice large "parent" orders into smaller "child" orders. The child orders may move market prices away from the price prevalent at the beginning of the large trade and as such increase the total cost of the parent order. Buy-side traders therefore worry about the total cost of their parent orders, which is usually measured by the implementation shortfall (IS).

While we likely cannot identify buy-side trades directly, we will proxy for parent orders by identifying instances where a single trader executes several trades in the same direction on a given day and trades only in that direction. The total cost associated with such a string of trades will be measured by the implementation shortfall defined as:

where qit is +1 for a string of buys and -1 for a string of sales that begins at time t in stock i, $volit is the total dollar volume for the string, pi0 is the prevailing midquote at the time of the first trade in the string, and volit is the total share volume for the string.

A positive shortfall indicates that prices move in the same direction as the parent order. In our reporting, the aggregate shortfall will be computed in basis points of the aggregate dollar volume traded. We will consider two types of trade strings: (i) those that originate from marketable orders only and (ii) those that originate from marketable and non-marketable orders.

Passive Order Execution Quality. We will examine the impact of the Pilot on orders of a variety of different types, paying particular attention to liquidity-providing orders. For retail orders and for large trade strings, we will compute the resting time of non-marketable orders. We will specifically focus on orders with prices that suggest that the submitter is interested in a timely execution. As such, we will consider orders that are submitted at prices that match or improve the CBBO.

For large trade strings, we will also report the average fraction of volume that is traded with marketable orders. A change in this measure captures the possibility that institutional investors may change their strategies and choose to "cross the spread" more/less often.

We will also examine the ratio of traded to submitted orders; this ratio captures how many orders an institution needs to submit to fill a position. We will consider only the orders submitted at prices matching or improving the CBBO. We will also compute this ratio for share volume. Finally, we will examine the opportunity costs of passive, as well as marketable, orders that are not filled by comparing prices at the time of submission to prices obtained through post-cancellation execution of similar directional volume by the same trader ID.

B. Statistical Analysis

The basis of our statistical approach is a conventional difference-in-differences analysis of a panel dataset (securities×days). Analyses of this kind usually rely on two approaches to examine the treatment effect (i.e., the effect of rebate prohibition). We discuss these approaches below using the bid-ask spread as an example.

In the first approach, the dependent variable [DGR]DVit is the value of the bid-ask spread for the treated security i at time t less the value for the matched security. Using this dependent variable, we will estimate the following regression:

where Pilott is an indicator variable set to 1 on the Pilot start date, controlst are time series controls such as the VIX, and di are security-pair fixed effects. The coefficient of interest [AGR] captures the effect of the Pilot on treated securities.{6}

In the second approach, the dependent variable DVit is the value of the bid-ask spread for each security from the treatment and control groups. Using this dependent variable, we will estimate the following regression:

where Pilott is the indicator variable set to 1 on the Pilot start date, treatedi is 1 if the security is from the treatment group and 0 otherwise, controlst are time series controls such as the VIX, and di are security fixed effects. The coefficient of interest is [A GR]2; it estimates the incremental effect of the Pilot on the treated securities. For instance, with quoted spread as the dependent variable, a positive [AGR]2 will indicate that the spreads for the treatment group increased relative to the control group.

We will conduct inference in all regressions using double-clustered Cameron, Gelbach, and Miller (2011) standard errors, which are robust to cross-sectional correlation and idiosyncratic time-series persistence.{7}

Each approach will use two controls for the market-wide effects that are known to affect trader behaviour and market quality. First, we will use the VIX to control for the level of market-wide volatility. We acknowledge that Canada has its own volatility index, but note that this index may be directly affected by trading in the sample securities, while VIX is less likely to be similarly affected. Second, we will use the cumulative return for the S&P GSCI commodity index. Comerton-Forde, Malinova, and Park (2018) show that this index is highly correlated with the Canadian TSX Composite index, but is unlikely to be significantly affected by trading in Canada and therefore serves as a proxy for Canadian market-wide returns.

We caution that several possible scenarios may affect our ability to deliver meaningful conclusions. First, individual firms in the sample may experience events during the Pilot that render them unusable for the subsequent statistical analyses (e.g., mergers, bankruptcies, or delistings). We will mitigate the impact of such events by building the sample as close as possible to the start of the Pilot, while providing market participants with sufficient time to prepare for the Pilot's implementation. This said, if one of the above-mentioned events occurs after the sample is finalized, we may omit the affected security and its match from further analyses.

Second, all securities may be affected by major market-wide confounding events. Examples are a failure of a major financial institution, a market crash, or a political event. While a staggered introduction, the use of control groups, and a sufficiently long Pilot period alleviate some of the concerns regarding such events, the CSA will reserve the right to extend the Pilot or to delay the start of the Pilot should it be necessary.

Third, the marketplaces may develop workarounds for rebate prohibitions that undermine the Pilot, e.g., differentiated fees, bulk discounts, new order types, new venues or order books, etc. The orders implementing the Pilot aim to prevent such workarounds so as to preserve the scientific integrity of the Pilot.

We propose that the Pilot for the interlisted stocks match the duration of the SEC Pilot. We also propose that the Pilot proceed in two stages, with treatment introduction for the non-interlisted stocks and ETPs separated from the treatment introduction for the interlisted stocks by two to three months.

As described above, the staggered introduction may alleviate concerns that arise if the Pilot start date is close to an unexpected market-wide event. For example, in July 2011, the SEC adopted a new rule that restricted some aspects of direct market access (DMA). Several research teams endeavored to analyze this event. Unfortunately, about two weeks after the DMA rule adoption, the U.S. credit rating was downgraded, creating a substantial amount of noise in the data. No research team was able to produce meaningful conclusions because the noise completely confounded the results (Chakrabarty, Jain, Shkilko, and Sokolov, 2019). We caution that a similarly unpredictable event may confound the results if all stocks are introduced into the Pilot at once.

Our conversations with market participants suggest that they share this concern and we received feedback that the difference between the two-stage and all-at-once alternatives is immaterial in terms of technical implementation.

We believe that transparency is integral to conducting pilot studies and commit to providing timely and comprehensive updates to the CSA for disclosure to market participants. We will continuously monitor the empirical measures described in section IV, share the ongoing statistical analysis with the CSA, and discuss any adverse trends that may be indicative of a decrease in market quality.

In the interest of transparency, we will make all codes publicly available via GitHub (the online code depository). GitHub includes a comment function and feedback on code improvement is welcome. Where possible, we will also provide the data (e.g., the non-proprietary data that will be used for the matching process). We believe that this level of transparency will bring added trust in the integrity of our analysis. However, we will not publish the matched securities to prevent possible gaming.

We have received excellent feedback from the CSA, the members of the OSC Market Structure Advisory Committee, the Canadian Security Traders Association, participants at the Rotman Capital Markets Institute Panel Discussion, and respondents to the Request for Comments. This report reflects this feedback.

This appendix provides an example of the matching procedure used to assign Canadian stocks interlisted in the U.S. into the treatment and control groups.

Trading volume, price, and market capitalization figures are the latest available from the Canadian Financial Markets Research Centre (CFMRC).{8} Trading volume is the average daily dollar volume, price is the closing price, and market capitalization is the product of the price and the number of shares outstanding. We use Canadian dollars for variables that require a price component.

We arrive at the matched sample using the following procedure:

1. We begin with a sample of 181 Canadian securities that are also interlisted on the NYSE, NYSE Arca, NYSE MKT, Nasdaq GM, and Nasdaq CM.

2. Among these, we identify 18 securities that trade at prices below $1 and refer to them as low-priced (LP). Price volatility in such securities is rather high, and as mentioned previously, LPs will not be included in the Pilot. We however discuss them here for the sake of completeness.

3. Among the remaining securities, we identify 107 that are on IIROC's "highly liquid" list. We refer to these as HL stocks and the remaining 56 securities are nHL (not highly liquid). We match HL stocks to HL stocks and nHL stocks to nHL stocks.

4. For each possible pair of i and j securities, we estimate a match error as follows:

where Ck are natural logs of trading volume, price, and market capitalization as defined above.

5. From the matrix of match errors that spans all stock-pairs, we then select stock-pairs with the lowest errors, for a total of 53 HL pairs, 28 nHL pairs, and 9 LP pairs.

6. Finally, to assign stocks into the treated and control groups, for each pair we generate a random number between 0 and 1. If this number is below 0.5, we assign the first stock in the pair to be treated and vice versa.

Figure 1 provides an illustration of match quality. The horizontal and vertical axes represent logarithms of market capitalization, dollar volume, and stock price for pairs of securities, with a random assignment of one member in the pair to the treatment and the other to the control group. A good match obtains if the points are on or close to the 45-degree line. A formal t-test shows no evidence that the treatment and control samples are different for any of the matching criteria.

Battalio, Robert, Shane Corwin, and Robert Jennings, 2016, Can brokers have it all? On the relation between make-take fees and limit order execution quality, Journal of Finance 71, 2193-2238.

Battalio, Robert, Brian Hatch, Mehmet Saglam, 2019, The cost of routing orders to high frequency traders, Working paper.

Brogaard, Jonathan, Terrence Hendershott, and Ryan Riordan, 2014, High-frequency trading and price discovery, Review of Financial Studies 27, 2267-2306.

Brogaard, Jonathan, Terrence Hendershott, and Ryan Riordan, 2019, Price discovery without trading: Evidence from limit orders, Journal of Finance, forthcoming.

Cameron, A. Colin, Jonah B. Gelbach, and Douglas L. Miller, 2011, Robust inference with multi-way clustering, Journal of Business Economics and Statistics 29, 238-249.

Campbell, John Y., Andrew W. Lo, and A. Craig MacKinlay, 1997, The Econometrics of Financial Markets (Princeton University Press).

Chakrabarty, Bidisha, Pankaj Jain, Andriy Shkilko, and Konstantin Sokolov, 2019, Unfiltered Market Access and Liquidity: Evidence from the SEC Rule 15c3-5, Management Science, forthcoming.

Cimon, David, 2019, Broker Routing Decisions in Limit Order Markets, Working paper.

Comerton-Forde, Carole, Katya Malinova, and Andreas Park, 2018, Regulating dark trading: Order flow segmentation and market quality, Journal of Financial Economics 130, 347-366.

Devani, Baiju, Ad Tayal, Lisa Anderson, Dawei Zhou, Juan Gomez, and Graham W. Taylor, 2014, Identifying trading groups -- methodology and results, Discussion paper, IIROC Working Paper.

Hendershott, Terrence, and Charles M. Jones, 2005, Island goes dark: Transparency, fragmentation, and regulation, Review of Financial Studies 18, 743-793.

Hendershott, Terrence, and Pam Moulton, 2011, Automation, speed, and stock market quality: The NYSE's hybrid, Journal of Financial Markets 14, 568-604.

Korajczyk, Robert, and Dermot Murphy, 2018, High-frequency market making to large institutional trades, Review of Financial Studies 32, 1034-1067.

Malinova, Katya, and Andreas Park, 2015, Subsidizing liquidity: The impact of make/take fees on market quality, Journal of Finance 70, 509-536.

Menkveld, Albert, 2013, High frequency trading and the new market makers, Journal of Financial Markets 16, 712-740.

Petersen, Mitchell A., 2009, Estimating Standard Errors in Finance Panel Data Sets: Comparing Approaches, Review of Financial Studies 22, 435-480.

Thompson, Samuel B., 2011, Simple formulas for standard errors that cluster by both firm and time, Journal of Financial Economics 99, 1-10.

{*} We thank the Canadian Securities Administrators (CSA), the Canadian Security Traders Association, the Market Structure Advisory Committee of the Ontario Securities Commission, participants at the Rotman Capital Markets Institute Panel Discussion, and respondents to the Request for Comments on the original Design Report for their input. Katya Malinova -- DeGroote School of Business, McMaster University, malinovk@mcmaster.ca. Andreas Park -- Rotman School of Management, University of Toronto, Institute of Management and Innovation@UTM, andreas.park@rotman.utoronto.ca (corresponding author). Andriy Shkilko -- Lazaridis School of Business and Economics, Wilfrid Laurier University, ashkilko@wlu.ca.

{1} This will include the prohibition of rebate payments for intentional crosses.

{2} http://www.osc.gov.on.ca/en/SecuritiesLaw_csa_20140515_23-101_rfc-pro-amd.htm.

{3} http://www.iiroc.ca/industry/rulebook/Pages/Hightly-liquid-Stocks.aspx

{4} The VIX is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, midquote prices of S&P 500 Index call and put options.

{5} This measure will be computed per transaction. We caution that it will be difficult to determine precisely which fees apply; dark, lit, and post-only orders may all command different fees, market-makers may receive bulk-discounts, etc. We will apply a uniform rule by employing only the "most common" fee that applies on the specific venue.

{6} This regression methodology is similar to that in Hendershott and Moulton (2011) and Malinova and Park (2015).

{7} Cameron, Gelbach, and Miller (2011) and Thompson (2011) developed the double-clustering approach simultaneously. See also Petersen (2009) for a detailed discussion of (double-)clustering techniques.

{8} http://clouddc.chass.utoronto.ca/ds/cfmrc. In rare cases when CFMRC does not have a valid record for a security, we obtain the missing data from https://www.tmxmoney.com/en/index.html.

WHEREAS [Exchange/ATS short form] is an exchange/alternative trading system (ATS) carrying on business in Ontario;

AND WHEREAS if it considers it to be in the public interest, the Ontario Securities Commission (Commission) has the authority to make any decision with respect to the manner in which a recognized exchange/an alternative trading system carries on business;

AND WHEREAS the payment of rebates by a marketplace may be changing behaviours of marketplace participants and creating unnecessary conflicts of interest for dealer routing decisions that may be difficult to manage, contributing to increased segmentation of order flow, and/or contributing to increased intermediation on highly liquid securities;

AND WHEREAS in light of the information set out in the paragraph above, it is the Commission's opinion that it is in the public interest to conduct a pilot study on the prohibition of the payment of rebates by marketplaces for a sample of securities (the Pilot);

AND WHEREAS the Pilot will apply to [insert number] of securities;

AND WHEREAS the objective of the Pilot is to gain a better understanding of the effects of the prohibition of rebate payments by Canadian marketplaces (the Objective) to determine whether the Commission should facilitate the transition to an amended rule regarding the payment of rebates by marketplaces;

IT IS ORDERED that, pursuant to subsection 21(5)/section 21.0.1 of the Act:

1. On [insert Pilot start date], [insert Exchange/ATS] shall implement the Pilot according to the design set out at Appendix A appended to this Order, by eliminating rebates for those securities set out at Appendix B until [insert Pilot end date].

2. Between [insert Pilot start date] and [insert Pilot end date], if [insert Exchange/ATS] seeks any amendment to its Form 21-101F1/2, including the exhibits thereto (the Proposed Amendments), [insert Exchange/ATS] shall file submissions which satisfy the Commission that the Proposed Amendments do not negatively impact the Objective of the Pilot.

DATED this ___ day of __________, 202___, to take effect ____________________, 202___.

____________________ |

____________________ |

[Name] |

[Name] |

[Title] |

[Title] |

Ontario Securities Commission |

Ontario Securities Commission |

Topic |

Summary of Comments |

CSA Response |

||

|

||||

The Merits of the Pilot Study |

The majority of commenters supported the Pilot Study. |

|||

|

||||

Respondents in support of the Pilot Study asserted that |

Support for the Pilot Study |

|||

|

||||

• |

The approach is consistent with the CSA's statutory mandate to foster fair and efficient markets and that the solicitation of public input and feedback has given rise to a transparent and appropriately designed Pilot Study; |

We agree with the benefits of conducting the Pilot Study. In particular, doing so will provide evidence to support any future policy decisions with respect to rebates. |

||

• |

An academic study is a necessary step to understanding any inherent potential dealer conflicts and that data driven approaches to rule making are appropriate and desirable; |

|||

• |

Removal of rebates would likely simplify market structure and foster fair and efficient markets since an environment without rebates should result in less unnecessary intermediation, more reliable liquidity provision, cost reductions, and marketplaces and dealers competing on the basis of the quality of execution; and |

|||

• |

The results of the Pilot Study could lead to a reduction in marketplace incentives that encourage excessive complexity and fragmentation and exacerbate agency concerns between investors and dealers. |

|||

|

||||

Respondents not in support of the Pilot Study were concerned that |

Concerns with the Pilot Study |

|||

• |

The approach is inconsistent with the principle of proportionate regulation and with the CSA's statutory mandate to foster fair and efficient markets; |

We acknowledge commenters' concerns and intend to closely monitor the markets following implementation of the Pilot Study to determine whether any of these concerns are realized. However, we believe the best and only way to address these concerns is by conducting the Pilot Study as only through the Pilot Study can the CSA determine the impact of rebates. Should the Pilot Study prove detrimental to the markets, then we can terminate it immediately through Commission orders, where applicable. |

||

• |

The need for a Pilot Study has not been substantiated with data analysis and experimentation should not be undertaken unless there is a compelling reason for regulatory intervention; |

|||

• |

Viable alternatives to better manage or avoid the associated risks have not been considered; |

|||

• |

The Pilot Study may have negative impacts on investors and issuers, may stifle competition among marketplaces, and may increase net trading fees for certain dealers; |

|||

• |

Liquidity providers may withdraw from the markets, which could cause spreads to widen; |

|||

• |

The Pilot Study may have unintended consequences and undermine the transparency and integrity of the Canadian capital markets, including trading flow arbitrage between Canadian and U.S. marketplaces which in turn may impact the attractiveness and competitiveness of Canadian markets; and |

|||

• |

The Pilot Study could weaken displayed versus non-displayed markets and enable uneven trading patterns in the market. |

|||

|

||||

The Overall Design of the Pilot Study |

General Structure of the Pilot Study |

General Structure of the Pilot Study |

||

A number of commenters generally agreed with the timing, duration, matched pairs design, and scope of the Pilot Study. Some commenters emphasized the importance of having a test group where no rebates are permitted. Other comments discussed the importance of including all marketplaces in the Pilot Study. |

||||

|

||||

Some commenters were of the view that restricting rebates would likely not answer all questions concerning conflicts of interest, segmentation, or excessive intermediation (causality, temporary versus permanent behaviour changes). |

The Pilot Study is designed to provide a comprehensive understanding of the current system of rebates and its effects on market quality. Given the duration of the Pilot Study, we expect it to lead to longer term changes in market participant behaviour. |

|||

|

||||

Included/Excluded Securities |

Included/Excluded Securities |

|||

|

||||

A number of commenters were supportive of excluding securities priced under $1 on the basis that they would not yield statistically meaningful insights. |

As set out in greater detail below, the CSA conducted extensive consultations with a broad range of stakeholders. Respecting issuer consultations, Staff met with Commission advisory committees to solicit additional feedback. No issuers raised concerns about the Pilot Study at either these meetings or any time thereafter, including in response to the 2018 RFC. As reflected in the 2018 RFC, the CSA remains of the view that the Pilot Study will not harm issuers. |

|||

|

||||

The majority of commenters expressed strong support for not including an issuer opt-out as doing so could impact sample selection and results. Another commenter wished to ensure that the CSA consulted with issuers prior to the implementation of the Pilot Study given the concerns of issuers in the United States. Another commenter was concerned that deteriorating liquidity could harm issuers, while another commenter suggested including an issuer opt-out in the Pilot Study. |

||||

|

||||

Symmetrical Pricing |

Symmetrical Pricing |

|||

One commenter supported the CSA's proposal not to mandate symmetrical pricing, while another was concerned that symmetrical pricing might be the only way to eliminate conflicts. |

The CSA will not mandate symmetrical pricing as doing so, in our view, would be overly prescriptive. |

|||

|

||||

Confidentiality |

Confidentiality |

|||

|

||||

One commenter requested that the audience of the confidential data required for the Pilot Study be strictly limited to the Academics and regulators and that market participants or other third parties do not access client trading information that may include their proprietary data pertaining to their trading strategies. Another commenter expressed general privacy concerns with regards to the identity of dealers being reverse engineered based on public data made available in connection with the Pilot Study. |

The CSA can assure all market participants that the data required to conduct the Pilot Study will remain confidential to the CSA, IIROC, and the Academics. The CSA will take appropriate precautions to ensure that there is no information leakage. Furthermore, data will be anonymized and only aggregate data will be published. |

|||

|

||||

The Legal Framework of the Pilot Study |

The Purpose of the Pilot Study |

The Purpose of the Pilot Study |

||

|

||||

One commenter was generally concerned about the appropriateness of a securities regulator involving itself in fee-setting or rate-capping. Another commenter noted that the CSA had historically not engaged in such a role and indicated that there should be a clear public interest rationale for the Pilot Study to proceed. A number of commenters believe that the CSA should clearly define certain aspects of the Pilot Study at the outset, including defining the problem that the CSA is trying to solve and how it will measure market and execution quality (e.g. what are good outcomes with respect to liquidity, volume, and ability to trade) and the overall success of the Pilot Study (what are statistically significant results). |

The purpose of the Pilot Study is to examine the effects of rebates on market quality and participant behaviour. It is the CSA's view that rebates may create conflicts that are difficult to manage and may lead to behaviour that negatively impacts market quality and the investor experience. The CSA is also of the view that the payment of rebates may lead to excessive intermediation and segmentation of order flow, which we are concerned may also be negatively impacting market quality. Therefore, the Pilot Study has been designed to test the effects of the prohibition of rebate payments by Canadian marketplaces. The metrics used will measure market quality. Should the Pilot Study prove detrimental to the markets, then the CSA can terminate it immediately through Commission orders, where applicable. |

|||

|

||||

The Consultation Process |

The Consultation Process |

|||

|

||||

One commenter was concerned that the CSA had not meaningfully addressed comments received on the proposed pilot in response to the 2014 Notice and that the CSA appeared to have unilaterally decided to proceed with the Pilot Study. Several commenters also indicated that the CSA had not conducted a cost-benefit analysis of the Pilot Study. |

The comments received in response to the 2014 Notice were responded to and addressed through the 2016 Notice. At that time, the CSA had determined not to proceed with the proposed pilot based on the feedback received at the time about coordinating with the United States to the extent possible. The CSA only considered a potential pilot study as likely in mid-2018. Since that time, the CSA has conducted more than ten outreach actions, providing market participants with substantial opportunity to provide feedback on the Pilot Study and responding to participants' comments and any concerns. Included among these consultation actions was the publication of the 2018 RFC, which specifically sought comments on the design of the Pilot Study and whether to proceed with it. While the CSA intends to proceed with the Pilot Study, this decision was made in response to all of its outreach through which it was determined that all but a handful of market participants support proceeding with the Pilot Study. For a chart setting out the outreach conducted to date, please see Appendix 1 to this chart. |

|||

|

||||

The Implementation Process |

The Implementation Process |

|||

|

||||

A few commenters were supportive of requiring marketplaces seeking to implement either a fee or major market structure change throughout the implementation period of the Pilot Study to demonstrate to the CSA that such a change does not interfere with the objective of the Pilot Study. In contrast, one commenter had significant concerns with this requirement, noting that it may provide the CSA with an unreasonable level of discretion to deny marketplace changes and is not applied to all marketplace participants. This commenter also believed the requirement to be too broad in that it could apply to any marketplace change. |

We have broad authority to make decisions in the public interest. Marketplaces will have the opportunity to provide submissions as to the rationale for any proposed changes and if the proposed change does not negatively impact the objective of the Pilot Study, then a decision will be made in the normal course. We have no intention of limiting marketplaces' ability to compete. The Pilot Study may lead marketplaces to find new ways to compete with one another. |

|||

|

||||

This same commenter was concerned that the implementation of the Pilot Study will circumvent the established process for imposing new obligations and rules on marketplaces. In particular, this commenter believes that the implementation scheme violates the Ontario Securities Commission's (OSC) prohibition on blanket orders and circumvents the formal rule-making process. |

It is not necessary to implement the Pilot Study through the rule-making process as the Pilot Study is specific to certain securities and will only be in place for a limited time. As acknowledged by the commenter, it is also not practical to implement the Pilot Study through the rule-making process because of its time limited nature and because implementing the Pilot Study as a rule will make it difficult to cancel should there be detrimental effects on the market. We also note that the Pilot Study is not being implemented by way of blanket orders. |

|||

|

||||

General Comments |

Difficulties with Implementing the Pilot Study |

Difficulties with Implementing the Pilot Study |

||

|

||||

One commenter was sensitive to the technology costs that the Pilot Study will impose on industry and asked that the CSA consider this burden and try to minimize impact. Another commenter was concerned that some trading platforms cannot support two SOR settings, which could impact the results of the Pilot Study. |

All efforts will be made to reduce the costs of implementing the Pilot Study. The Academics conducted outreach with vendors prior to the publication of the 2018 RFC and understand that they already route differently depending on the security that is traded (for example, securities priced above versus below $1.00). In addition, marketplaces regularly and frequently adjust their trading fees with limited cost to themselves or participants. |

|||

|

||||

Policy Implications of the Pilot Study |

Policy Implications of the Pilot Study |

|||

|

||||

A number of commenters expressed support for taking action where the results of the Pilot Study suggest doing so. One of these commenters noted that such action could include the substantial limitation, if not prohibition of, rebates for more liquid securities where data supports the conclusion that liquidity incentives are no longer necessary. |

We agree with the comments on this issue. The purpose of the Pilot Study is to determine the effects of the prohibition of rebate payments by Canadian marketplaces. If the results of the Pilot Study suggest that policy changes should be made to improve Canada's capital markets, then the CSA intends to evaluate and identify possible courses of action. Any proposal will follow the normal course, including a comment period. |

|||

|

||||

Possible Reliance on the Findings of the SEC Fee Pilot |

Possible Reliance on the Findings of the SEC Fee Pilot |

|||

|

||||

Some commenters suggested that rather than implement the Pilot Study, the CSA should rely on the findings of the SEC Fee Pilot to assess whether and what policy changes should be made in Canada. Commenters were split as to whether the CSA could simply rely on the findings of the SEC Fee Pilot or would need to conduct the Pilot Study in tandem with the SEC Fee Pilot. Those in support of the latter position were particularly concerned that key differences in market mechanics and regulatory fabric will mean that the lessons observed from the SEC experience do not necessarily translate in the manner anticipated. |

The CSA considered relying on the findings of the SEC Fee Pilot, but due to significant differences in Canadian and American market structure, as well as certain necessary differences in the design of the two studies, determined that it is imperative that the CSA proceed with its own Pilot Study. |

|||

|

||||

Alternative Approaches |

Alternative Approaches |

|||

|

||||

Some commenters suggested that rather than conduct the Pilot Study, the CSA should use IIROC's data, including historical data, to assess the routing practices of dealers and best execution policies that address how routing decisions are made. One commenter recommended studying IIROC's data from May 2017 when the CSA introduced reduced fee caps for ETFs and non-interlisted equities. |

The Pilot Study will include an analysis of existing routing practices, but this information will not be sufficient to establish a nexus between fees and routing decisions. Existing routing practices are the result of interactions between marketplaces, brokers, and clients and constitute an equilibrium. A rebate prohibition will affect these interactions, such that we can study the behavioural changes and the new equilibrium. Relying on IIROC's data from the introduction of the reduced fee caps will also prove insufficient to meet the purpose of the Pilot Study for a number of reasons. In particular, most marketplaces reduced their fees gradually from 2015 through 2017 to prepare for the fee cap. During this time, two new marketplaces with drastically different structures, namely speedbumps, were introduced, making it impossible to isolate the effects of the fee cap on the markets. |

|||

|

||||

One commenter suggested gradually reducing the current fee cap across all securities, rather than proceeding with the Pilot Study. |

A key component of the Pilot Study is the control group of securities which serves as a benchmark for changes in the treatment securities. A gradual reduction in the fee cap for all securities would be suboptimal due to the absence of a control group. A gradual reduction for the treatment group only would require that the Pilot Study be conducted over a very long time period. We expect that market participants would require several weeks to adjust behaviour as a result of each fee change, so that it will take time for each new equilibrium to emerge. Moreover, each adjustment imposes costs on market participants. Finally, a gradual roll out will make it impossible to coordinate meaningfully with the SEC Fee Pilot. We therefore believe that the single change is the best solution. In addition, the purpose of the Pilot Study is to study the impact of no rebate -- i.e. the removal of the conflict of interest -- to see whether the rebate drives behaviour. A gradual decrease does not measure or enable us to fulfil the primary purpose of the Pilot Study. |

|||

|

||||

The view was expressed that even if the SEC Fee Pilot does not move forward, the CSA should undertake the Pilot Study with non-interlisted securities. |

If the SEC Fee Pilot does not proceed, then the CSA will not move forward with a Pilot Study of non-interlisted securities. We do not believe that we will be able to make meaningful policy decisions post-study when analyzing the impact of a rebate prohibition on only non-interlisted securities. |

|||

|

||||

The Academics propose to define a security as medium-liquid if it trades at least 50 times a day on average and more than $50,000 on average per trading day over the past month. Do you believe that this definition is appropriate? If not, please provide an alternative definition and supporting data, if available, to illustrate which securities your definition captures. |

There is widespread support for the definition of medium-liquid securities. Some respondents indicate that the Pilot Study should be mindful of possible industry biases. Some raised concerns that the medium-liquid securities may be too illiquid to warrant analysis. |

The Academics will use the definition discussed in the 2018 RFC.{1} The analysis will separate the highly liquid from the medium-liquid securities. Since the goal of the analysis is to fully understand the impact of the rebate prohibition, the Academics will carefully examine if further analysis is warranted. The Academics are mindful of possible industry biases, which they will control for both at the analysis stage and at the randomization stage. |

||

|

||||

The Academics propose to introduce the Pilot Study in two stages, with non-interlisted securities first, followed by interlisted securities. Do you believe that such staggered introduction will cause material problems for the statistical analysis and the results of the Pilot Study? If so, please describe your concerns in detail. |

Very few concerns were identified with the proposed staggered introduction of the Pilot Study. The predominant view was that the most important timing consideration was to align the inclusion of interlisted securities in the Pilot Study with the timing of the SEC Fee Pilot. Partly as a result of this concern, some commenters suggested that the CSA conduct the non-interlisted phase of the Pilot Study after the interlisted securities phase is complete. Other commenters were concerned with ensuring that firms were given sufficient lead time to prepare for the Pilot Study. Some commenters suggested a lead time of 90-120 days between the issuance of orders that would implement the Pilot Study and the actual Pilot Study start date. |

The Academics will, where possible, maintain the staggered introduction of the Pilot Study. However, due to the likely limited lead time between the announcement that the SEC Fee Pilot will proceed and the implementation of the SEC Fee Pilot, the Pilot Study will likely proceed first with interlisted securities. We intend to provide market participants with as much notice as is possible prior to implementation of the first stage of the Pilot Study. However, it is important that the implementation of the Pilot Study be aligned with the timing of the SEC Fee Pilot. Given the uncertainty regarding the SEC Fee Pilot, we note that implementation timing may need to be expedited. Non-interlisted securities and ETPs will then be introduced into the Pilot Study three months after the introduction of interlisted securities. |

||

|

||||

One commenter was concerned that any major market event would skew the results such that comparability of the two data sets would be compromised. That commenter indicated that running a one-stage fee pilot would ensure variables apply to both sets equally and facilitate an easier implementation. |

The Academics note that the purpose of the staggered approach is precisely to avoid the skewing of the results, and that a staggered approach allows a meaningful analysis even if there is a major market event. Specifically, a major market event around the start of the Pilot Study hampers the ability to attribute observed changes to the Pilot Study. A staggered introduction substantially reduces this risk because the likelihood of a major market event occurring on both introduction dates is lower than on one date. |

|||

|

||||

Several Canadian marketplaces offer formal programs that reward market makers with enhanced rebates in return for liquidity provision obligations. On the one hand, such programs may benefit liquidity. On the other hand, one of the primary objectives of the Pilot Study is to understand if rebates cause excessive intermediation. In your opinion, should exchanges be allowed to continue using rebates or similar arrangements for market making programs during the Pilot Study? Do you believe any constraints on such programs during the Pilot Study to be appropriate? |

There was no consensus amongst comments received regarding the functioning of designated market maker and liquidity programs under a rebate prohibition. Comments range from forbidding incentives entirely to leaving them materially unchanged. Several commenters highlight the nuanced nature of liquidity provision incentives, which come in the form of: (a) rebates available to all traders, (b) rebate supplements for particular types of traders, and (c) monthly non-rebate performance incentives. A number of comments highlight that unchanged market maker incentives or exceptions to market maker incentive programs could lead to distortions. Other comments highlight that incentive schemes designed to apply only to the treatment securities could create distortions. Some commenters indicated that liquidity provision involves costly risk-taking and should be compensated commensurately. |

We are mindful of the costs and risks associated with liquidity provision and believe that market makers play an important role in ensuring an orderly market. However, we are concerned that certain types of incentives can inadvertently distort the Pilot Study and bias data collection and analyses. As such, for the pilot securities in the no-rebate group, rebates of types (a) and (b) are on their face considered to negatively impact the objective of the Pilot Study. |

||

|

||||